"...when it seems to good to be true... it probably is..."

What is

the Sortino Ratio?

It turns out we can. In finance there’s a metric called the Sortino Ratio. It

measures return relative to downside volatility (a variation of standard

deviation). A higher number is better than a lower number, but

the number can get higher in a few different ways –

returns can go up, downside volatility can go down, or both returns can go up

and volatility can go down simultaneously. Higher returns by themselves

are not enough to make the metric move, if they come with more downside

volatility.

Sortino

Ratio = Return / Downside Volatility

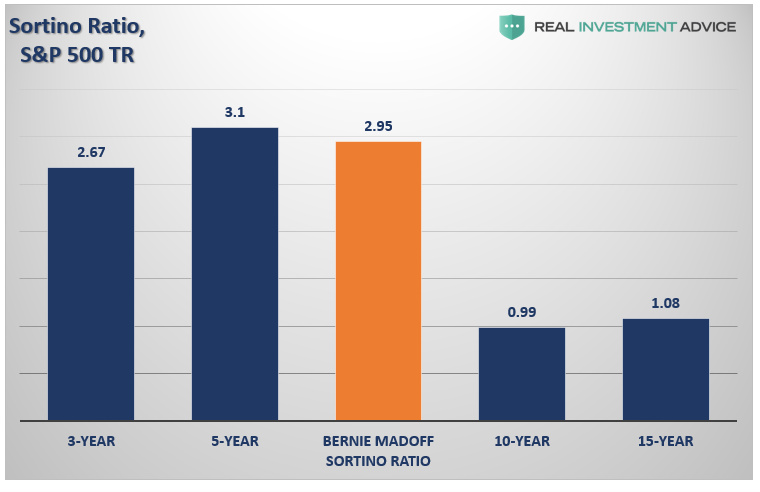

Over the 10- and 15-year periods ending January 31, 2018, the Sortino Ratio for the S&P 500 Index was 0.99%

and 1.08%, respectively, according

to Morningstar. But over the past 3- and 5-year periods, the Sortino Ratio for the index has been 2.67% and 3.10%,

respectively. Clearly we’ve been spoiled with 3-

and 5-year periods of high returns with little downside volatility –

around triple the ratio of the longer term periods. Over long periods of time,

the market doesn’t deliver such robust high volatility-adjusted returns.

See chart

Source:

Morningstar

Ironically, the fraudulent Sortino Ratio of Bernie Madoff’s

hedge fund was 2.95%.

Madoff didn’t advertise market-beating returns, but returns that were close

enough to the market’s with hardly any volatility. Somehow

– probably with the help of very low interest rates and investor psychology – we’ve gotten a Sortino Ratio over the last 3 and 5 years that

roughly matches that of the Madoff fraud

Lessons

for Investors

The first obvious lesson for

investors during this bout of volatility is that

periods of uninterrupted returns don’t last. A

correction is a normal part of investing. It’s not that investors get paid for enduring

volatility, as some theories suggest; it’s that volatility is simply the price

of admission into the stock market. Returns or getting paid comes

from being careful about how much you pay for stocks.

2nd. Another lesson is that investors should have an

appetite to start buying when prices drop. If you don’t feel like buying, but,

instead, want to sell, it’s very likely your allocation wasn’t correct to begin

with. Nobody likes to see any part of their portfolio decline, but if the decline has hit a piece of your assets that

doesn’t make you want to throw in the towel, that’s a good sign. Stocks

may still be to expensive, but a good investor should at least be thinking

about buying during and after big declines. In fact, if you’re still employed

and making automatic contributions to 401(k)s and other accounts, take some satisfaction

in knowing that you’re contributing new money to your retirement accounts, and

buying stocks at lower prices.

Third,

take this bout of volatility as an invitation to rebalance your portfolio and

reassess how much stock exposure is really appropriate for you. Many people fill

out asset allocation questionnaires when they set up financial plan, and those

are generally good things to do.

Last, get updates from your

advisor about the market’s Sortino Ratio. It’s been around 1 for a long time. If it starts flashing anything over 2, and gets near 3, you

know things have been too calm and returns have come too easily.

….

----

----

No hay comentarios:

Publicar un comentario