FEB 18

18 SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Econ

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

"Whether

the administrations of

the Government, The Fed, and select benefactors on Wall Street (among

others) are serially incompetent

or (more likely) criminally culpable for abusing their positions and power to benefit a small minority at

the expense of the vast majority is a

question in need of asking... "

See

Chart:

{kind=link}

See more charts at:

Source: https://www.zerohedge.com/news/2018-02-18/how-did-america-go-bankrupt-slowly-first-then-all-once

----

----

"... one thing which has

fueled the illusion of "recovery" is the fact that much of the data coming out of Washington has

been impregnated with Keynesian bias... this isn't merely a matter of intellectual sloth or even honest error.

There has been nothing remotely like a true

'recovery'... "

As we point out below, this isn't merely a

matter of intellectual sloth or even honest error. ..As we pointed out in this

series earlier, business cycle causation has been reversed in the era of

Bubble Finance. The Fed no longer has the

capacity to inflate the main street economy with unsustainable, credit-driven

booms.

Its monetary stimulus, in fact, never escapes

the canyons of Wall Street, where it fuels rampant speculation and pure

financial wagering until the resulting bubbles finally burst.

That is a recession

that neither the FOMC or Wall Street sees coming because they are essentially

focussed on the wrong data----the deltas, not the trends and levels----and because they mistakenly believe that monetary

stimulus actually stimulates the main street economy.

See chart:

{kind=link}

Read more n see more charts at:

----

----

“All these currencies, there is nothing backing the currencies except

the government’s force...They are all going to have a catastrophic drop... the

whole underlying structure of our economy is destabilizing..."

LISTEN VIDEO:

...

----

----

In the US,

there is little top tier data of note, only the FOMC minutes on Wednesday night

where the market will be looking for affirmation of a highly anticipated rate

hike in March.

See chart:

{kind=link}

Source https://www.zerohedge.com/news/2018-02-18/fx-weekly-preview-time-start-pricing-risks-away-usd

----

----

"The only thing more dangerous to investors long-term outcomes

than being overly optimistic, is ignoring history..."

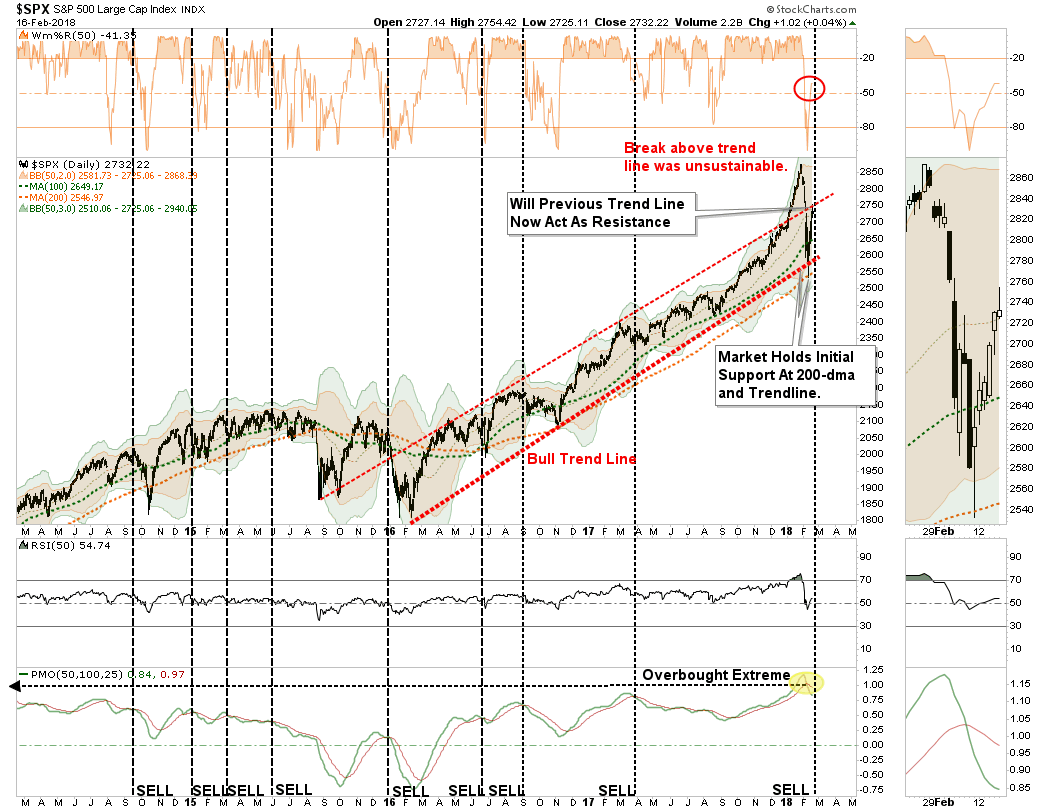

Let’s start with where we left off last weekend:

“Currently, we do not know whether the current corrective action is JUST

a normal, healthy correction, or the beginning of something bigger.

BUT – this is the expected correction we have been discussing

over the last several weeks. It is also something we had planned for by

reducing overweight positions and adding a short-hedge to portfolios.

With the markets on a short-term sell signal (noted by black

vertical dashed lines in the chart above,) the current correctional

process is underway. But, with the market now oversold on a VERY

short-term basis a counter-trend rally over the next week, or two, should be

expected.”

Well, we did indeed get a very nice rally last week with the market

breaking above the 50-dma on Thursday.

See Chart:

{kind=link}

While the immediate consensus is the “bear market of 2018” is now

over, there are several important points about the chart above that should

be considered.

- Despite

the correction, the market did hold support at the 200-dma

- The bullish

trend line, which goes back to the beginning of 2016, has also not been

violated.

- However,

the upper red “trendline” may provide some overhead resistance temporarily

and is worth watching closely.

- While the

market did get oversold on a short-term basis, which suggested a bounce

was likely, the longer-term overbought condition, and subsequent “sell

signal” remain intact.

The bottom line is that while there was much “angst” in the

markets last week, the market has not violated any

important trend lines that would suggest the current sell-off is anything more

than just an ordinary “garden variety” correction.

The greenish triangle shows the path of the accelerated bullish trend

that began last August which currently remains the most likely path for now.

See chart:

{kind=link}

The Real Bear Is Still Coming

The good news, for those who remain ever bullishly

inclined, is on a long-term, monthly basis, the bull market remains intact for

now.

Unfortunately, despite the rather harrowing

correction, little was done to relieve any of the underlying pressures.

- Valuations

still remain elevated

- Bearishness

and volatility, despite the recent spike, remain at historically low

levels, and;

- Investors

simply could not jump “back” into the markets fast enough.

These are not signs of a

real, lasting bottom, which long-term investors should aggressively buy into.

Given the current extension of the market, and the

deviation between the current price and long-term average, a real reversion to the mean is still coming.

If you thought the 10% decline over the last two weeks was painful, you should

be reconsidering the risk you are currently carrying in your portfolio.

See chart:

{kind=link}

….

See more chart & comments at:

----

----

"If

credit spreads do indeed reprice to higher volatility, the drawdown in credit

ETFs could trigger meaningful liquidation, resulting in further pressure on

spreads." - Deutsche

Bank

Going back to Deutsche Bank's volatility model, which maps the impact of

VIX on IG and HY spreads, the bank estimates that a 1

point rise in VIX is worth -0.6% to IG ETFs in aggregate, and -1.3% to the

universe of HY funds.

Such sharp moves have yet to be observed: thus

far, an index of IG ETF’s has fallen 1.2%, whereas the VIX shock should have

pushed it 3.3% lower, and an index of HY funds is down just 2% versus a VIX

implied drop of 7.2%.

See chart:

{kind=link}

…

----

----

“Inflation

is always and everywhere a monetary phenomenon.” —Milton Friedman

"...

it’s important to remember that the money–GDP correlation is merely a byproduct

of a lending–GDP correlation. Bank

lending, not money, is the driving force... economists built a

discipline (mainstream macro) on a false premise so significant it can’t be

corrected without starting over..."

Have you ever questioned Milton Friedman’s

famous claim about inflation?

Ever

heard anyone else question it?

Unless you read obscure stuff written for the

academic community, you’re probably not used to Friedman’s quote being challenged.

And that’s despite a lousy forecasting

record by economists who bought into his Monetarist methods.

Consider the following:

- When Friedman’s strict Monetarism fizzled in the 1980s,

it was doomed partly by his own forecasts. Instead of the disinflation the decade delivered, he expected inflation to

reach 1970s levels, publicizing that prediction in 1983 and then again in

1984, 1985 and 1986. Of course, years earlier he foresaw the 1970s jump in

inflation, but the errant forecasts that came later left him wide open to

a “clock twice a day” dismissal.

- Monetarists suffered an even harsher blow in 2012, when the Conference Board finally threw in

the towel on Friedman’s favorite indicator, removing M2 from its Leading Economic Index (LEI).

Generally speaking, forecasters who put M2 in their models are like

bachelors who put “live with mom” in their dating profiles—they haven’t

been successful.

- The many economists who expected quantitative easing

(QE) to wreak havoc on inflation are, of course, on the defensive. Nine years after QE began, core inflation

remains below the Fed’s 2% target, defying their Monetarist beliefs.

When it comes to explaining inflation, Monetarism

hasn’t exactly nailed it. Then

again, neither has Keynesianism, whose Phillips Curve confounds those who rely on it. You can toss

inflation onto the bonfire of major events that mainstream theories fail to

explain.

But

I’ll argue there might be a better way.

In three articles, I’ll try to convince you that we can develop a better

theory by interpreting Friedman’s research differently than he did. Maybe you’ll like the theory, or maybe you won’t,

but I promise this: the indicator that falls from it has a better

record predicting major inflation trends than any other serious indicator I’ve

studied. It’s not the only way to

think about inflation, but it’s realistic and practical, and I’m interested in

the reader reaction.

Round, Round, Get Around

In pictures, we can compare the traditional,

mainstream view to the alternative approach by sketching a “circular flow”

between spending and income. Here’s an example I’ve simplified from charts that

appear in my recently published book, Economics for Independent Thinkers, which

covers the topic in more detail:

SEE Chart:

{kind=link}

Even

more importantly, these bank loan effects cumulative over time. If we say the chart above is the

current time period or period 1, then the next chart (below) shows that period 1’s new bank credit (or at least a portion of

it) is now part of the circular flow, and then it gets joined by period 2’s new bank credit. And

then periods 1 and 2 join period 3’s new bank credit and the flow gets fatter

and fatter.

See Chart:

{kind=link}

....

----

----

POLITICS

Seudo democ y sist duopolico in US is obsolete; it’s full of frauds & corruption. Urge

cambiarlo

A former Trump campaign aide and

longtime business partner of Paul Manafort, Rick Gates, will plead guilty to

fraud-related charges in the coming days, and has indicated that he will

testify against Manafort in upcoming proceedings.

----

----

"The press has played an active role in

the Trump-Russia collusion story since its inception. It helped birth it... When the reckoning comes, Russia gate is

likely to be seen not as

a symptom of the collapse of the American press, but as

one of the causes for it."

----

----

WORLD

ISSUES and M-East

Global depression is on…China,

RU, Iran search for State socialis+K- compet. D rest in limbo

Washington is moving inevitably on a global war plan. That’s the grim conclusion one has

to draw from three unfolding war scenarios...

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars:

its profiteers US-NATO

----

----

----

----

----

----

INFORMATION

CLEARING HOUSE

----

American Violence: Disorganized and Organized

By

Frank Scott

----

----

Anti-T Use Mueller Indict to Escalate

Tensions With RU By Caitlin Johnstone

----

----

SPUTNIK

and RT SHOWS

Geopolitics & the nasty

business of US-NATO-Global-wars uncovered ..

RELATED 1:

RELATED 2:

RELATED 3:

Ex-CIA Chief of Russia Ops: US Has Carried

Out Election Meddling Historically : “If you ask an intellig

officer, did the Russians break the rules or do something bizarre, the answer

is no, not at all,”

----

----

RELATED:

----

----

RELATED1:

Extreme 1.2: US' New Nuclear Doctrine Shows Country is 'No

Longer a Superpower' - Analyst So, we arrived to a new “end of history”… If you don’t accept US, we nuke you =

Terrorism at global scale?

----

----

----

----

----

----

Do the worms of decomposition

have cameras to reproduce similar worms? Just kiting

----

----

----

----

NOTICIAS

IN SPANISH

Latino America looking for

alternatives to neoliberalism to break with Empire:

----

----

----

----

----

----

….

"¿Reconoce

este dron?": Netanyahu 'trolea' a Irán (VIDEO) Payaso sin par

----

----

----

----

----

----

----

----

PRESS

TV

Global situation described by

Iranian observers..

----

----

----

----

----

----

----

----

----

----

----

----

----

-----

-----

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario