FEB 4 18 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Econ

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

Something

strange is going on in the market according to DB's cross-asset desk, and it

could be a recipe for disaster if current trends do not change.

As we further noted, judging by the major correlation

regime shift between stocks and bonds that started on

Monday, this is something considerably more worrisome for investors...

SEE chart:

{kind=link}

----

----

"The

next bull market is coming, it just won’t

be in stocks..."

It will be in the U.S. Treasury market which will

coincide with the next recessionary drag in the economy

within the next 12-18 months (at the most).

See chart:

{kind=link}

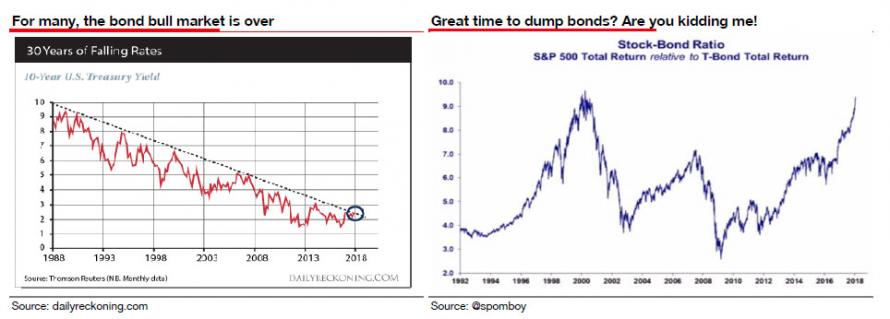

I agree with Albert Edwards:

“Every man,

woman, and child seems to have decided that the US 10y

bond yield has broken out of its long-term downtrend and we are in a bond bear market. Our own excellent Technical Analyst, Stephanie

Aymes, shows that 3% (not 2.6%) is the key long-term breakout yield we should

be watching. But she thinks that 2.64% was also significant

as this means the RSI downtrend has now been broken and a run to 3% is now perfectly

plausible. That

though does not mean the bond bull market is over.”

With yields now closing on 2¾% and

the 30y closing on 3.0%, many see this as a great time to

dump bonds and switch into equities. Really?

Check charts below:

{kind=link}

“Well, I expect that the

true extent of how close the US is to actual outright deflation, and hence how

high real yields currently are, will soon be revealed. But before US 10y yields turn negative,

expect them to visit 3% first.“

See chart:

{kind=link}

The Next Bull Market

Edwards is correct. There are several important points to

understand about bonds.

- All interest rates are relative. With more than $10-Trillion in debt globally sporting negative interest rates, the assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields in U.S. debt attracts flows of capital from countries with negative yields which push rates lower in the U.S. Given the current push by Central Banks globally to suppress interest rates to keep nascent economic growth going, an eventual zero-yield on U.S. debt is not unrealistic.

- The coming budget deficit balloon. Given the lack of fiscal policy controls in Washington, and promises of continued largesse in the future, the budget deficit is set to swell back to $1 Trillion or more in the coming years. This will require more government bond issuance to fund future expenditures which will be magnified during the next recessionary spat as tax revenue falls.

- Central Banks will continue to be a buyer of bonds to maintain the current status quo, but will become more aggressive buyers during the next recession. The next QE program by the Fed to offset the next economic recession will likely be $2-4 Trillion which will push the 10-year yield towards zero.

The next bull market is

coming, it just won’t be in stocks.

It will be in the U.S. Treasury market which will coincide with

the next recessionary drag in the economy within the next 12-18 months (at the most).

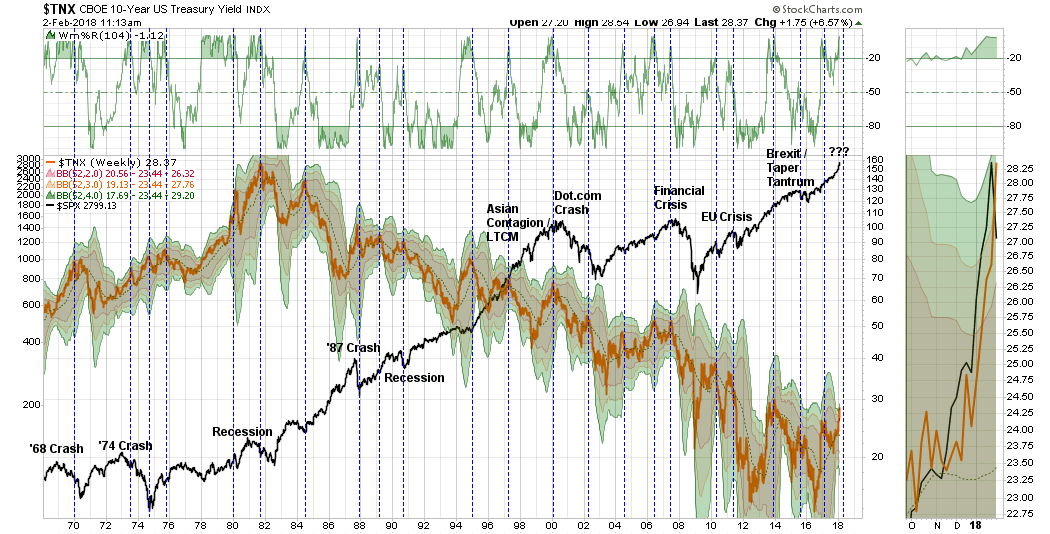

The chart below goes to my point.

Currently, interest rates are 4-standard deviations above their 1-year moving

average. (For an explanation read this.)

See chart:

{kind=link}

How often has this happened going back to 1965?

Never.

Negative events such as the

S&L Crisis, Asian Contagion, Long-Term Capital Management, etc. all drove

money out of stocks and into bonds pushing rates lower, recessionary environments are especially prone

at suppressing rates further. Given the

current low level of interest rates, the next

recessionary bout in the economy will very likely see rates near zero.

Furthermore, given rates are already negative in

many parts of the world, which will likely be even more negative during a

global recessionary environment, zero yields will still remain more attractive

to foreign investors. This will be from both a potential capital

appreciation perspective (expectations of negative rates in the U.S.) and the perceived

safety and liquidity of the U.S. Treasury market.

Over the next several

months, higher interest rates, if they remain elevated for long, will have a deleterious effect on the economy.

Valuations will become problematic.

Summarizing: the safety of bonds

becomes much more attractive when the yield is significantly above the dividend

yield in stocks. (Why take the risk with a sub-2% yield when I

can get 3% in a U.S. Treasury?)

That’s not hard math.

Things are finally

starting to get interesting.

…

----

----

With

the 10y jumping 43bp since the start of the year, investors have begun to

question how much convexity-related selling could result from the extension in

mortgages.

SEE Chart: Bloomberg-Barclays MBS Index Duration -and others-at the source below

.. just as the long-running correlation between

equities and yields finally snapped this week as higher yields are now seen as

a risk to stocks..

See chart:

.. traders are increasingly worried, after the

worst week for stocks since Jan 2016, what further Treasury selling could

mean for equities as a result of a potential violent deleveraging of

risk-parity strategies, which will be forced to significantly reduce

their gross exposure following last week's drubbing.

So what is the potential selling overhang as a

result of recent rate moves?

Based on Barclays' model, at the

start of the year, a 50bp sell-off in rates would have led to a $667bn

extension for the MBS universe expressed in 10y Treasury equivalents (chart

below).

Chart:

{kind=link}

Alleviating the risk of a selloff is the fact that a smaller

portion of the MBS universe dynamically hedges its duration exposure than it

did before 2008. In particular, the Federal

Reserve ($1.7trn in MBS holdings), many money managers (~$700bn in MBS

holdings), and several overseas investors (~$800bn in MBS holdings) do not

actively hedge duration in their MBS portfolios.

Part of the reason is that the average

mortgage rate for the universe has continued to decline over the past several

years.

See charts below:

{kind=link}

As such, Barclays concludes, at this

point, even a further substantial sell-off in rates would not materially reduce

the percentage of refinanceable borrowers.

In summary, this is good news for those

worried about further self-reinforcing selling at least out of convexity

hedgers. The bad - or at least so far

undetermined - news, is that forced selling by

"everyone else" may be sufficient to tip the overall market,

mostly via vol-sellers, CTAs and risk-parity funds, into

the next correction.

…

Source https://www.zerohedge.com/news/2018-02-04/will-convexity-hedgers-unleash-next-round-treasury-selling

----

----

The man who

predicted the collapse of GM, Fannie, and Freddie says the

next big bankruptcy is going to catch everyone by surprise. Learn more

here.

----

----

POLITICS

Seudo democ y sist

duopolico in US is obsolete; it’s

full of frauds & corruption. Urge cambiarlo

The

US economy is threatened by two

giant problems which cause all others to pale into insignificance...

We are

referring to A ROGUE CENTRAL BANK that has become an absolute

enemy of capitalist prosperity and A FISCAL DOOMSDAY

MACHINE that is hostage to the ceaseless budgetary demands of the Warfare State, the

Welfare State and the Baby Boom's demographic imperatives.

Read more at:

https://www.zerohedge.com/news/2018-02-04/stockman-exposes-two-elephants-room-gop-has-completely-forgotten

----

----

"...the

cockroaches have run out of corners to hide in... Time to put on our

pointy shoes and start kickin’..."

----

----

WORLD ISSUES and M-East

Global depression is on…China, RU, Iran search for State

socialis+K- compet. D rest in limbo

===

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars: its profiteers US-NATO

----

----

----

----

----

----

----

----

COUNTER PUNCH

----

Serge Halimi

The Pentagon’s Useful Idiots

----

Ralph Nader

The Paradox of Equal Justice

----

Ron Jacobs A History of Resistance

----

Mel Gurtov The Middle East Peace Process: A

Cruel Joke

----

Jill Richardson

How Colleges are Screwing Both

Teachers and Students

----

----

SPUTNIK and RT SHOWS

Geopolitics & the nasty business of US-NATO-Global-wars

uncovered ..

Obama Should Give Back His Peace Prize and Trump -

His Presidency' – Analyst https://sputniknews.com/analysis/201802041061348614-obama-give-back-peace-prize-trump-presidency/

-----

The New Nuclear Posture review said Trump wants nuclear weapons more useable

RELATED:

----

----

----

----

----

----

----

----

----

----

----

----

Cementery S-story-tale: Israel to

Build Settl in West Bank in Resp to Rabbi Murder - Neta

----

Affairs

can’t be the excuse alone.. Money plus could be .. Female-pride vs Partner Polit-failure

sums-up all of them. If so, it stands to reason

----

----

RT SHOWS

----

----

NOTICIAS IN SPANISH

Latino America looking for alternatives to neoliberalism to

break with Empire:

50

aniversario Mayo 68: From Viento Sur http://www.vientosur.info/

----

Respuesta a Daniel

Cohn-Bendit y Romain Goupil Alain

Krivine

----

Kurdos

Ent a Maryam Fathi: “Me sorprende ver part de izq apoy iran

----

----

----

----

----

----

----

----

----

Keiser Report Masacre

en Davos

----

----

PRESS

TV

Global situation described by Iranian observers..

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

No hay comentarios:

Publicar un comentario