FEB 24 18 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Econ

PENTA-NATO want to start WW3..

this FACT demands IMMEDIATE response: ORGANIZE PEACE Mov worldwide

Read this:

QUESTION: Can you

rule out the United States boarding and inspecting N- Korean ships...

MNUCHIN: No, I -- I cannot rule that out.

THE US NUKE BACKMAIL IS SET: WE

can have different opinions while observing facts, but

we can’t change the facts.

----

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

"Predicting

a regime change to much higher GDP growth, and hence higher inflation, could simply be a case of looking for, and

then seeing, something that isn’t there..."

Summing up the current conventional wisdom:

- Global GDP growth has bottomed and is accelerating systematically higher,

- Which will cause the inflation rate to accelerate higher.

- Bond markets hate higher inflation, so interest rates have bottomed and will move even higher.

- The stock market, dependent on low rates for high valuations, will fall if rates move higher,

- Which is why the stock market peaked on January 26, 2018, and then declined dramatically,

- Ushering in an era of systematically higher volatility

1. Global GDP Growth Is Accelerating?

Unless GDP can be exported from

another planet to Earth, the main drivers of global GDP growth are in four

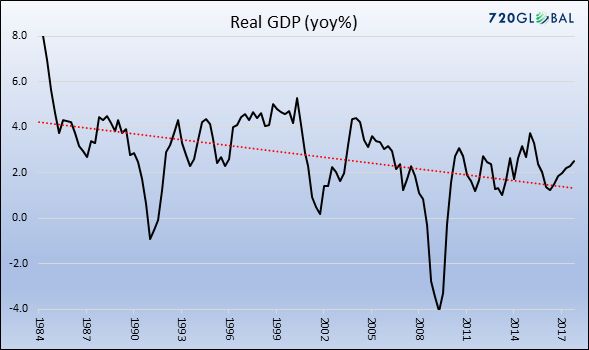

large economic zones. Here are the past 30 years of GDP growth in the

U.S……

See chart:

{kind=link}

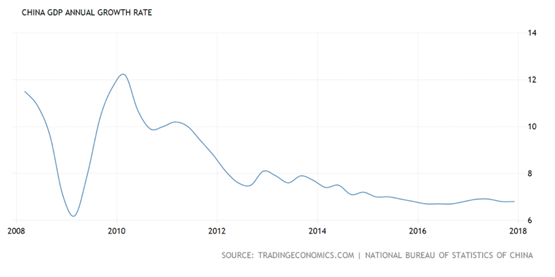

The past ten years in China……

See chart:

{kind=link}

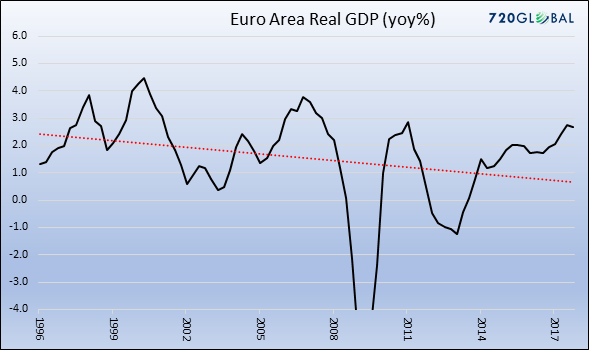

The past 20 years in Europe…..

See Chart:

{kind=link}

2. Rising Inflation

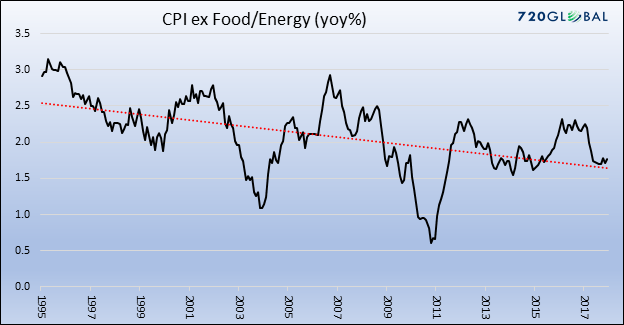

Below is the chart of US annual inflation rate since the

mid-1990s’ during which time it has fluctuated between

1.0% and 2.4%, and is currently at 1.5%. Nothing significant seems to

have changed here.

See chart:

{kind=link}

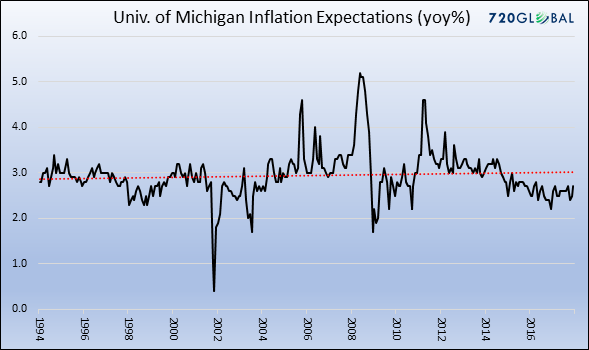

Consumers don’t seem too worried about a rise in inflation

either. The current expectation is a little below

3%, which is near the average of the past 20 years, in addition to being

consistent with the past several years.

See chart:

{kind=link}

- Bond Market Reaction

Summing up the data presented so far, neither global GDP

growth nor US inflation are systematically higher, and to believe they will

rise sharply out of the range of the past 10-20 years, you would have to

believe that GDP growth and inflation will overcome the two main constraints on

economic growth, which are a high and rising debt burden, and an aging

population.

So why

would interest rates be moving higher over the past couple of months, and why

would there be so much noise about that fact in the financial media? We

can think of two alternative explanations.

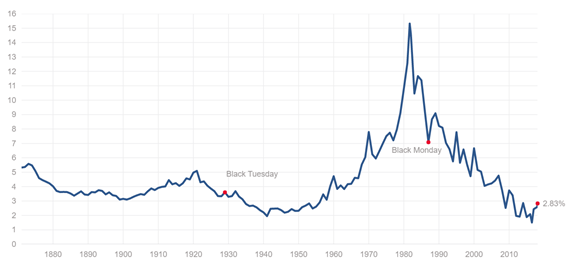

The first explanation is

behavioral, meaning that it is rooted in how and why

humans act and interact in markets, a subject of focus for the authors of the

Epsilon Theory articles. The chart below shows the history of the

10-year Treasury bond yield over the past 140 years.

See Chart:

{kind=link}

Forecasts of higher GDP growth and inflation don’t make

actual GDP and inflation rise, a lesson that should have been learned over the

past decade. Instead, economic events will

happily come and go regardless of who or how many financial market observers

call for an inflection point in GDP growth, inflation, and interest rates.

Viewed from this perspective,

it is easy to envision a scenario in which rise in rates during the first half

of 2018 and is followed by yet another lurch lower in the second half of 2018

when the expected rises in GDP growth and inflation do not materialize. Recent fund flow data supports the potential for a change in

view (and price/yield), because a record short position has been amassed in

bonds, as shown below.

See chart:

{kind=link}

CONCLUSIONS

It is possible that the mainstream narrative is correct and that the recent rise

in rates is foreshadowing a future of higher GDP growth and inflation.

If so, then markets are discounting a future not yet seen, which is how market

sometimes operate. But sometimes they don’t.

The current levels of GDP growth and inflation are well within their

recent ranges, and those recent ranges are lower than

they were 10-20 years ago. More importantly, the underlying

problems of high debt levels and aging demographics will continue to constrain

the potential for GDP growth and inflation to systematically rise, which are

the main reasons that interest rates have persistently declined over the past

several decades. Predicting

a regime change to much higher GDP growth, and hence higher inflation, could

simply be a case of looking for, and then seeing, something that isn’t there.

Instead, there are two alternative explanations for the recent rise in

US Treasury rates.

One is the inevitable temptation of high-profile investors to burnish

their professional reputations by “calling the bottom”

in rates, which has the power to change the narrative (and prices) in financial

markets but it doesn’t have the power to change underlying economic reality.

That is, if high-profile investors put their money where their mouths are, it will affect prices in financial markets, which will

affect the perception of other investors, who may tag along with similar

strategies. But there is a short shelf life for

that type of process because economic reality will eventually unfold, revealing

whether the forecasts of high-profile investors are correct. As

unlikely as it seems now, it is quite possible that

they won’t be correct, and that slow GDP growth

and low inflation are here to stay awhile longer. Or, given

the length of the tepid economic expansion and high indebtedness, it is even possible that recession arrives prior to the

visions of a systematic rise in GDP growth and inflation. That is

one of the implications of the Rinehart and Rogoff study.

Another explanation for rising rates is the

emergence of credit risk in US Treasury bonds, the result of the simultaneous and unprecedented experiments of

monetary policy (unwind of QE) and fiscal policy (a borrowing

binge with a high debt-to-GDP ratio). The concept of credit risk

in US Treasury prices is outlawed in financial theory. But other aspects

of today’s financial landscape, such as negative

interest rates or European junk bonds trading at lower yields than US Treasury

bonds, also weren’t supposed to occur and cannot be explained by orthodox

financial theories. Theories can change how we observe facts,

but they can’t change the facts.

….

----

----

"I show that if job polarization had not changed the composition

of jobs in the labor market in the past two decades, 1.9 million more men would likely be employed in 2016..."

See Chart:

{kind=link}

…

----

----

"...a solid majority of

the American population feels no direct impact from stock market performance.

The inverse is different. Long-term stock market performance depends heavily on

the US population’s economic health. Stocks

are businesses that need customers, so how are the customers doing?"

Zero Exposure

So who does own

stocks?

The first surprise:

A big slice of the US stock market

isn’t American at all. Foreigners own about

35% of US stocks by value—and their ownership grew considerably over the last

few decades.

See Chart:

{kind=link}

Everybody Isn’t Average

The government’s average wage growth

numbers include both workers and supervisors. Looking at them separately shows a whole different picture since the last

recession.

See Chart:

{kind=link}

Where else

might people draw spending money? They can take it out of savings if they have

any. But that’s getting harder too.

See chart:

{kind=link}

If you

can’t increase your spending with higher wages or pull cash out of savings, the

only other option is debt. That usually means credit cards. Here, we finally

see some growth.

See chart:

{kind=link}

…

----

----

POLITICS

Seudo democ y sist

duopolico in US is obsolete; it’s

full of frauds & corruption. Urge cambiarlo

PENTA-NATO want to start WW3..

this FACT demands IMMEDIATE response: to organize PEACE Mov worldwide

Read this:

QUESTION: Can you rule out the United States

boarding and inspecting North Korean ships...

MNUCHIN: No, I -- I cannot rule that out.

THE US NUKE BACKMAIL IS SET: WE can have different opinions while observing facts, but we can’t change the facts.

----

----

"I’ve never been to Russia. I’ve never been to Moscow. I’ve never

met a Russian operative or agent. I’ve never done business in Russia. I’ve never taken money from

Russia....but I may be guilty of drinking the odd Russian vodka..."

----

----

WORLD ISSUES and M-East

Global depression is on…China, RU, Iran search for State

socialis+K- compet. D rest in limbo

"Any way you look at it, Russiagate is ridiculous. Of course it serves some

people’s interests. But it harms the most of all

by bringing us closer to conflict with

Russia, perhaps even to nuclear war."

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars: its profiteers US-NATO

----

----

----

----

----

COUNTER PUNCH

Richard D. Wolff Capitalism

as Obstacle to Equality and Democracy: the US Story

----

Charles Pierson Nuclear

Nonproliferation, American Style

----

W. T. Whitney US

and Allies Look to Military Intervention in Venezuela

----

----

SPUTNIK and RT SHOWS

Geopolitics & the nasty business of US-NATO-Global-wars

uncovered ..

RELATED 1:

RELATED 2:

SEE MORE VIDEOS AT:

----

----

----

----

----

----

----

----

----

----

----

RT SHOWS

----

----

----

----

----

----

----

NOTICIAS IN SPANISH

Latino America looking for alternatives to neoliberalism to

break with Empire:

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

Keiser Report

"Los terroristas de nuestra

era"

----

----

----

----

PRESS TV

Global situation described by Iranian observers..

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario