ND

SEP 5 19 SIT

EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

Stronger and a little larger, Hurricane Dorian is

gradually leaving Florida behind, setting

its sights on the coasts of Georgia and the Carolinas...

….

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

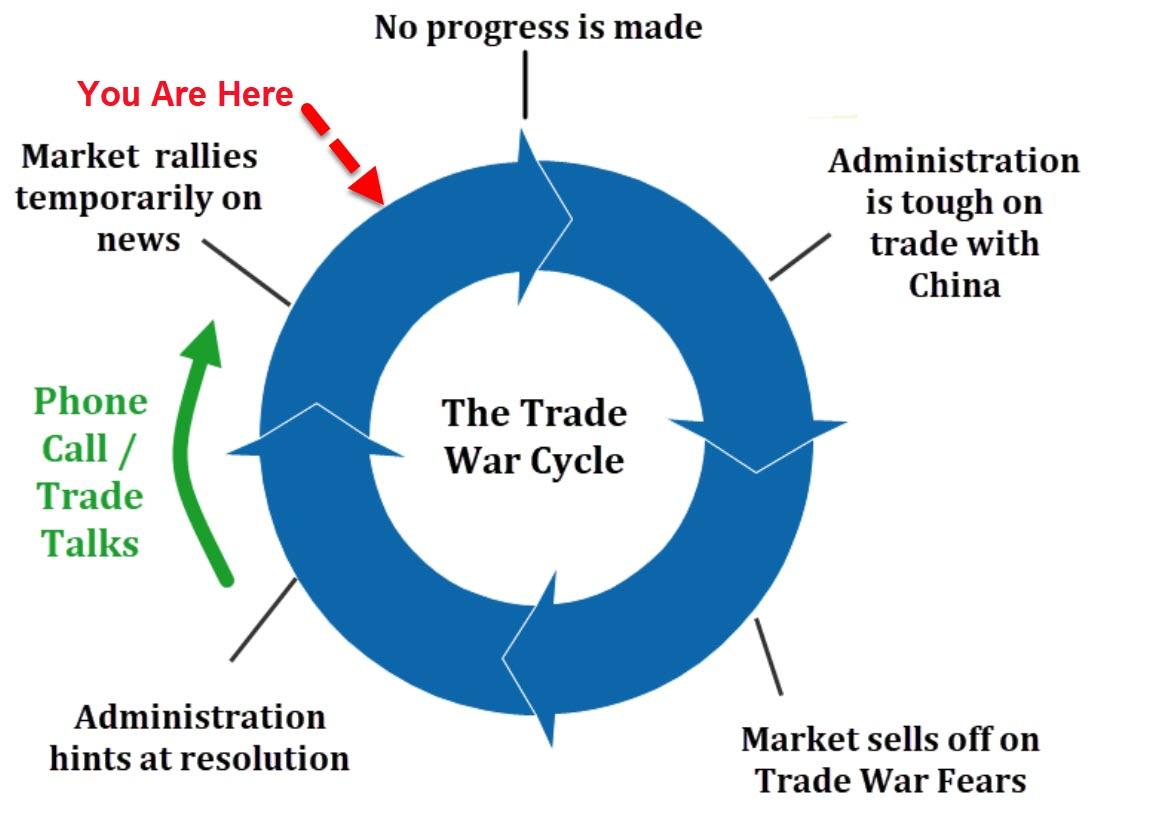

Trade-Talks

are on again... on

like Donkey Kong if markets are to be believed.

So to explain what happened today, the following chart should help (trade accordingly):

See Chart:

The trade world cycle: No Progress

is made

{kind=link}

Cyclicals dominated as the odds of a

China trade deal surged...

See Chart:

Market-Implied Odds of a US-China

Trade Deal

{kind=link}

Trade Deal is either T’wishful thinking or Trick to ‘boost’

US Econ & then blame China So far,

we haven’t seen any evidence from China to agree on DEAL next M or Next Y.

Bonds don't seem to be buying it

though...

See Chart:

{kind=link}

Today was among the biggest absolute

spikes in 10Y (above 1.50%) and 30Y (above 2.00%) Yields since the election in

2016...

See Chart:

UST 30Y Yield.. start going down

{kind=link}

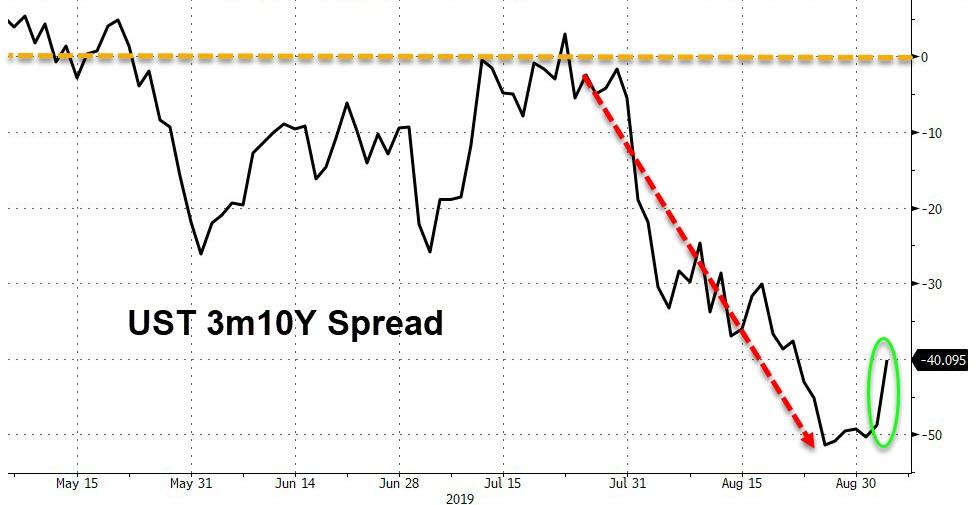

The yield curve steepened on the day

but 3m10Y remains deeply inverted...

See Chart:

UST

3m 10Y Spread

{kind=link}

The dollar ended the day lower, but

roundtripped off overnight lows...

See Chart:

Blooomberg Dollar Index

{kind=link}

Yuan is higher overnight but well

off the highs, notably divergent from US stocks...

See Chart:

{kind=link}

Finally, we should note that while

the market has pushed for more and more easing in recent weeks, since The Fed

first cut, the macro-economic data has beaten (admittedly low) expectations

dramatically...

See Chart:

{kind=link}

….

----

----

"...

add in the impact of a loss of confidence in the Fed (just as there was a loss

of confidence in the BoJ and MoF in Japan), and there is a realistic prospect

of a decline below the March 2009 666 low."

Back in August, we

wrote that after decades of waiting, for Albert Edwards vindication

was finally here - if only outside the US for now - because as per BofA calculations, average non-USD sovereign yields on $19 trillion in global debt had, as

of Monday, turned negative for the first time ever at -3bps.

See Fig 1:

Global IG Fixed Income

{kind=link}

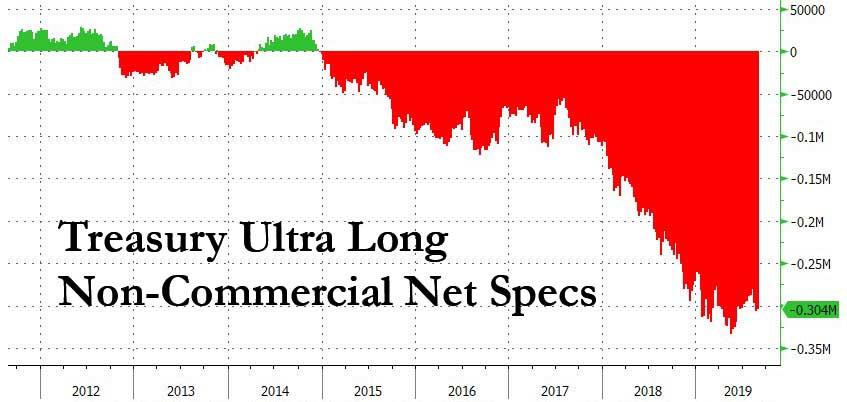

So instead of diluting Edward's

message with trivial tangents, we focus on several key points, the first of

which is why if Edwards got the bond bull market so spectacularly right at a

time when virtually everyone remains short bonds...

See Chart:

Treasury Ultra Long Non

Commercial Net Specs

{kind=link}

.. has he been wrong on stocks, with his calls to short the

equity market, which is also explains the genesis of his "permabear"

moniker (alternatively, Edwards is the biggest bond permabull in existence).

This is what Edwards said:

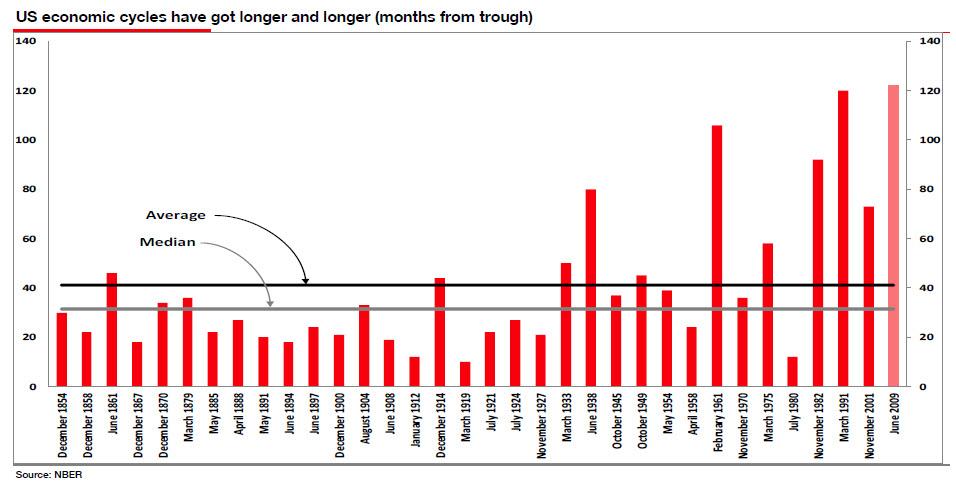

... my biggest Ice Age mistake was to assume that the US would be like Japan and that subsequent to the

2008 GFC, US policymakers would find it much harder to manipulate the economic

and credit cycles. I

thought we would return to ‘normal’ economic cycles with lengths nearer to 40 months.

See Chart:

US economic cycles have got long

longer & longer months

{kind=link}

If everyone buys bonds, won't stocks also be bid? After all,

that's the basis of the Fed model, is it not? Well, here too Edwards has

something to say.

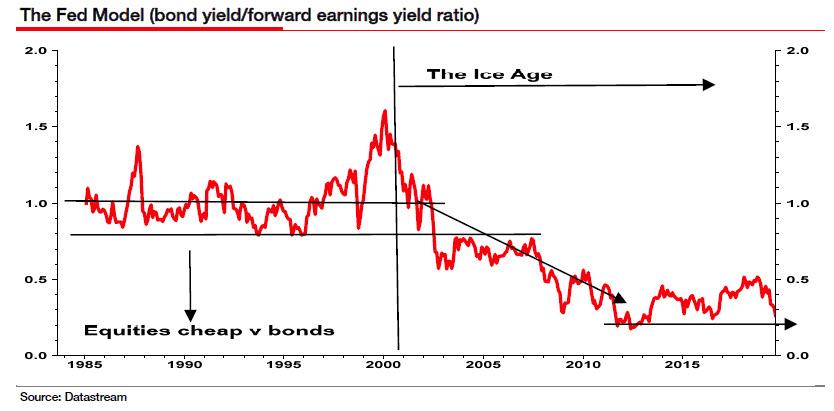

The so-called Fed Model (below) was an essential asset allocation

reference tool in the 1980s and 1990s. It was thought that this ratio of 10y US

bond yield and forward earnings yield (inverse of PE) enjoyed some sort of ‘equilibrium’ level at 1.0, as for most of that period the ratio oscillated above

and below 1.0 (until the Nasdaq/TMT bubble).

See Chart:

The FED model (bond yield/forward

earning Yield ratio)

{kind=link}

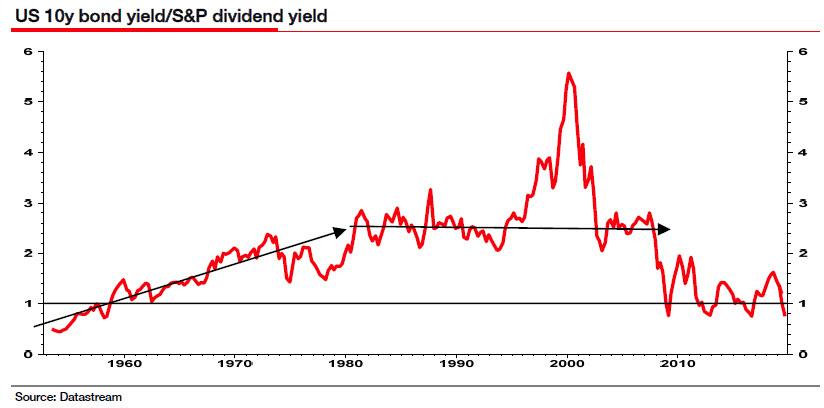

Indeed you see from

the chart below that the nominal bond yield/equity yield was not ever stable in

the long run if you go back to the 1950s (this chart uses dividend rather than

forward earnings yield). The 1982-2000 period was an anomaly in the longer-term

context. A fundamentally

important Ice Age forecast was that we were going to return to a world where

the equity dividend yield would rise above the bond yield and stay above

it. It was the 1965-2000 period that I thought was the anomaly. So while market commentators have recently noted that the US

30y bond yield has fallen below the dividend yield – I believe that is the natural order.

See Chart:

US 10Y

bond yield /S&P dividend yield

{kind=link}

But experience has

shown us that in a post-bubble world a cyclical recovery could lead to a pause

or even reversal of the two PE depressing drivers. And the longer the economic

recovery continues the more the markets will believe there is a return to Great

Moderation ‘normality’ and the more it can

ignore the Ice Age. That

is exactly what has happened, aided by QE.

Indeed the chart below shows that US long-term earnings expectations

have done exactly what they did during the late 1990s Nasdaq bubble. The echoes of that time are unerringly

similar. Belief in this equity market has been centred

around the new large technology, growth stocks typified by the large-cap FAANGs

(Facebook, Apple, Amazon, Netflix and Alphabet's Google), rather than TMT

generally.

See Chart:

In the late 1990 Nasdaq bubble, Greenspan justified high

PEs…

https://www.zerohedge.com/s3/files/inline-images/nasdaq%20bubble.jpg?itok=0pm5ITff

And finally, there is the issue of a decade of accumulated

non-GAAP gimmickry to catch down to:

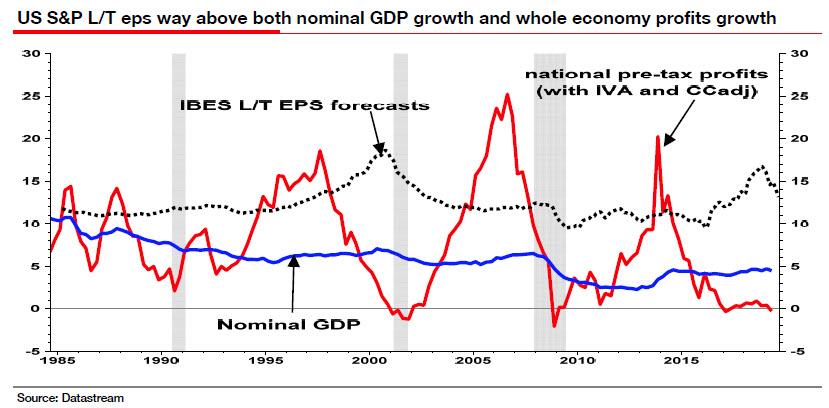

Despite the recent downtick, S&P Composite long-term eps

expectations are still way out of line with both nominal GDP and particularly whole

economy profits growth (see chart below, both 5y trailing to match the 5y

projection for long-term eps expectations). In a

recession, expect the dotted line in the chart below to lurch down sharply as

it did in both the last two recessions (shaded areas). That is when you will

see equity prices melt away.

See Chart:

US S&P L/T eps way above both

nominal GDP growth & whole Econ profit growth

{kind=link}

Which brings us back to Edwards' cataclysmic forecast, that

the S&P will tumble below the 666 "generational low" of March

2009. Here is the SocGen strategist's defense of that extremely controversial

claim:

How can we possibly believe that the S&P

could fall back below its 666 March 2009 low. Simple: I believe the 12-month forward PE will decline to a new lower low

compared to the profits nadirs of 2002 (15.5x) and 2009 (10.5x). At the height

of a bear market, during the eye of the storm, the equity market does not trade

like an auto stock or a copper stock. It does not go to peak PEs of infinity at

the bottom of the earnings cycle. Quite the reverse – the market in its panic goes to trough PEs on close

to trough earnings.

Which brings us to the doom and gloom conclusion: how Albert envisions the next recession. In a nutshell, it

will be right out of Dante's inferno:

In the next recession, as the secular forces of the Ice Age thesis combine

with the cyclical chaos of another deep GFC-like event, I would expect the

S&P 12m forward PE to collapse from a QE inflated 16½x currently to around

a 7x trough eps - while forward earnings fall something like 40% to $100/sh,

just as they did in the last recession. Add in the impact of a loss of

confidence in the Fed (just as there was a loss of confidence in the BoJ and

MoF in Japan), and there is a realistic prospect of a decline below the March

2009 666 low. And with that I must stop.

It took about 20 years but Albert Edwards was eventually

proven correct in his bond forecast. For the sake of

civilization, one can only hope that his equity forecast is wrong.

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Bernie Sanders: 2020

ELECTION COULD PUT OIL OUT OF BUSINESS

...the baseline in the Democratic Party is a complete phase out of fossil fuels in the

medium- to long-term. The Overton window has very much been moved...

====

Maybe the rate cut was

meant as much to give policymakers something to feel good about for

themselves. It certainly has done nothing as far as markets go...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

“I told Donald, ‘if you want,

we’ll sell them to you’”

====

Delusional?

====

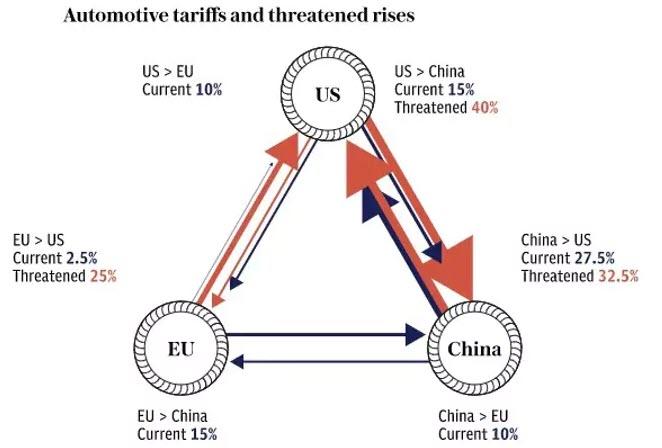

The global

repercussions of Trump's trade

wars have a new casualty: US

and European car manufacturers.

See Chart:

{kind=link}

….

SOURCE: https://www.zerohedge.com/news/2019-09-05/car-manufacturers-caught-crossfire-trumps-trade-war

----

----

...any state agency who wins

the arms race in developing a quantum-resistant cryptocurrency

couldsecure an appreciable geopolitical

edge for its country.

====

"Having

failed at piracy, the US resorts to outright blackmail..."

====

Taxpayer money is subsidizing frog-mating studies in Panama, Pakistani ‘woke’ films, and a ‘Green New Deal’ in Peru...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELLION

====

ALAI

ORG

====

RT EN

ESPAÑOL

- El Gobierno venezolano acusa a Guaidó de planificar "el robo de CITGO" desde antes de enero . Basta de niñerías : métanlo en la cárcel.

- Putin ofreció a Trump comprar nuevas armas hipersónicas de Rusia

- Alejandro Giammattei a RT: "El problema de la migración no se resuelve criminalizándola"

- López Obrador triunfó en las elecciones, pero ¿ha conseguido ganar el poder?

- "Los bancos centrales son la nueva Iglesia y son tratados como santos y apóstoles"

- Putin advirtió a Bush del riesgo de un ataque terrorista contra EE.UU. 2 días antes del 11S

- Maduro denuncia que Guaidó pretende entregar el Esequibo venezolano

- ¿Por qué falla la estrategia de seguridad de López Obrador en México?

- Encuesta global revela el país más infeliz del mundo: ARG

- Denuncian asesinato de otros tres líderes indígenas en Colombia

- Keiser Report "Los bancos centrales son nueva Iglesia y sus jefes son tratados como santos y apóstoles"

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

-Why Washington Won't Reduce Its Military

Footprint By Ted Galen

-Untold Story of Christian Zionism’s Rise to

Power in the US By Whitney Webb

-Now It’s Official: US Visa Can Be Denied If

You or Your Friends Are Critical of American Policies By Philip Giraldi

-FBI’s terrorism watch list violates the

Constitution By Timothy Bella

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

Jacques R. Pauwels The

Hitler-Stalin Pact, a Reply

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

-Biden : He’ll

Attend a Fossil Fuel Exec’s Fundraiser. Dime quien te compra..te

dire Q-e

-After

DNC Rejects Climate Debate, Candidates Discuss Green New Deal, Environmental

Justice at Forum

----

----

PRESS TV

Resume of Global News described by Iranian observers..

- Sudan's PM unveils first cabinet since fall of Bashir

- Macron starts pension rollback despite protests

- Iran officially informs EU of plan to expand nuclear R&D

- Italy's new coalition government sworn in

- US reaches out to Houthis to end war as Saudi struggles

- Netanyahu in UK to meet Johnson before Israeli votes

- Racial discrimination on the rise in US: Studies

- US blocks anti-Israel statement at Security Council

- PROGRAMS

- Lebanese-Israeli front heats up az hezbollah vows retaliation

- US-Taliban talks

----

===

No hay comentarios:

Publicar un comentario