ND

SEP 1 19

SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

Maximum

sustained winds of 220 mph

….

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

Authored

by Michael Wilson, chief US equity strategist at Morgan Stanley

The bullish

narrative today is that while the US industrial/manufacturing part of the economy

is weak, the US consumer remains strong, so the US economy can avoid a further

slowdown or recession.

The estimate for

3Q19 was +10% a year ago. Most importantly, 4Q19 and 2020 estimates still look

way too high and far above the normal “overestimate” that bulls argue is always

the case. In particular, the positive operating

leverage baked into current consensus estimates seems fantastical to me.

See Chart:

Small and mid-cap companies saw negative earnings growths in

1H19

{kind=link}

An even broader measure of US corporate profits, the

National Income and Products Account (NIPA), shows the same trends as the

S&P small and mid-caps. This matters because the bullish narrative today is

that while the US industrial/manufacturing part of the economy is weak, the US

consumer remains strong, so the US economy can avoid a further slowdown or

recession. Though that may be true for now, this profit trend is unequivocally bad, and getting

worse. Such a broad profits recession, if it doesn’t get better

soon, is exactly what could lead to layoffs. Obviously, such an outcome would

negatively affect the US consumer and is really all that separates the US

economy from a recessionary outcome. On that score, we’re already seeing companies take action on labor by

reducing the number of hours worked and hiring at a much slower pace than last

year.

While it’s not yet clear whether layoffs are coming, the

risk is elevated, and it’s unlikely that the third quarter earnings season will

bring much comfort, given the newly enacted tariffs that kick in this week. Therefore, I

continue to expect further downside in US equity markets this quarter and

believe that the S&P 500 will trade to 2700.

….

----

----

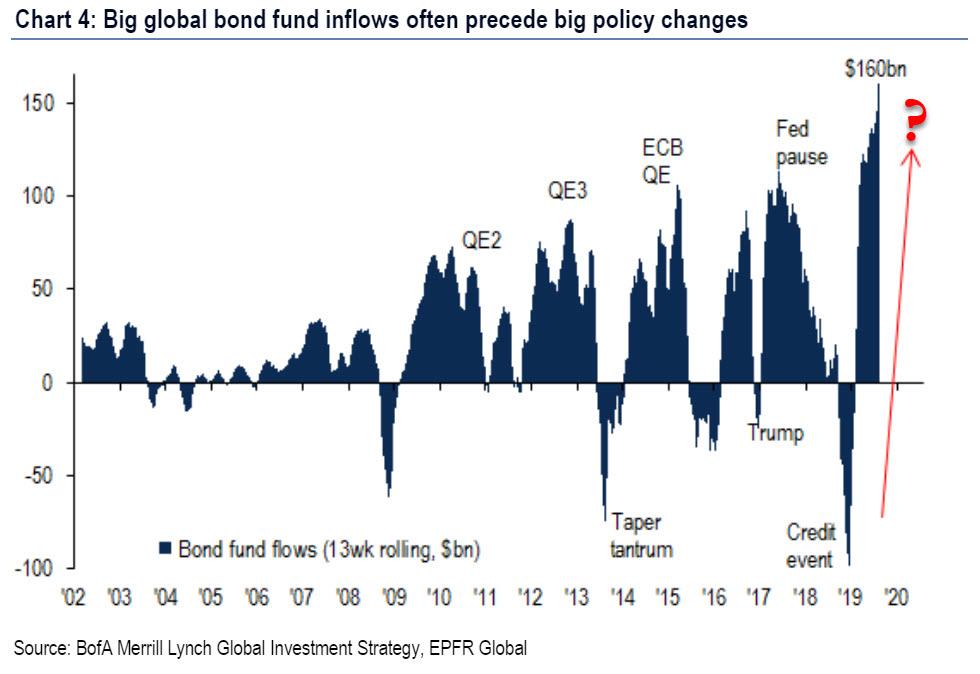

There has

been a record $160 billion in inflows to bond funds over the past 3 months,

which reveal deep global recession fear & global capitulation into

"Japanification" theme; such

big bond inflows often precede big policy changes.

See Chart:

Big global Bond fund inflows

often precedes big policy changes

{kind=link}

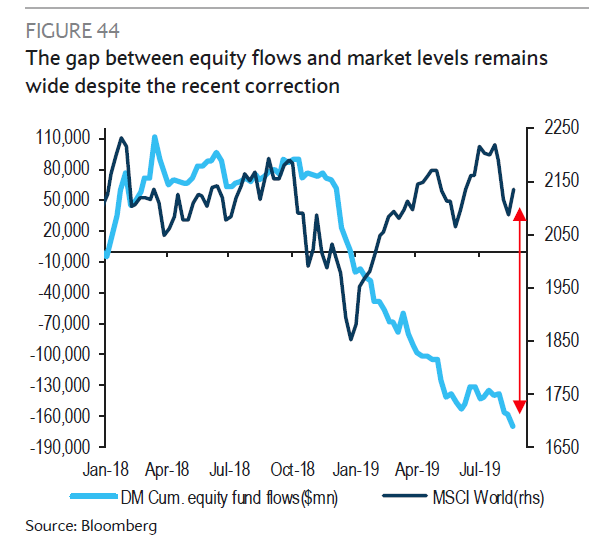

... even if it does pose the

question: just who is buying stocks here?

See Chart:

The gap between equity flows & market levels remains wide

despite recent correct

{kind=link}

See more interesting charts at

…

----

----

...it’s akin to the government admitting it has

no intention to ever pay back the debt. 100 years, for all

intents and purposes, is akin to a permanent bond. Government

is asking to take the principle and never pay it back, only interest.

With

central banks globally once again suppressing the borrowing cost of sovereign

entities to near zero rates, with yields in

some countries even going negative, there is

significant talk of issuing a 100-year bond to take advantage of these rates. Part of the argument is to lock in low

rates now to hedge against future increase; though if the past decade is

any consideration, central banks globally will fight until they collapse to

keep sovereign borrowing near zero permanently because they legitimately

have no choice in the matter. Even if governments do lock in these rates

now, it won’t matter considering interest

rate manipulations have placed banks on shaky ground. But if we assume this is a good

idea on a purely financial basis (it’s not, I’ll get into that later), the

concept of these ultra-long bonds are highly unethical.

One of the key reasons behind the

relatively short maturity rates of United States debt instruments is to maintain the illusion that the federal

government is a responsible debt payer. While debt may be

formally paid, it’s done by borrowing additional funds to cover the maturity of

the bond. This is demonstrated by examining

the federal cash flow statements, which show that $9 trillion was

spent paying debt, or over twice the formal federal outlays. Two-thirds of all

cash that transitions through the US Treasury today is related to debt

maintenance.

However,

with the issuance of the 100-year bond or even a perpetual bond, such

as this incredible bond that was issued 371 years ago and is still

being paid by the Netherlands to this day, is that it’s akin to the government

admitting it has no intention to ever pay back the debt. 100 years, for all intents and purposes, is akin

to a permanent bond. Government is asking to take the principle and never pay

it back, only interest.

It’s

Financially Foolish

A major concept in organizational finance, be it a

for-profit or non-profit, is maturity

matching. The term of any debt should match, or be shorter than, the

productive life of the asset it is used to buy. Organizations generally want to

avoid paying debt on obsolete assets as this is a dead-weight loss. Setting

aside for a moment that the vast majority of debt activity by modern

governments is to give it away as a hand-out, the 100-year bond blows up this

concept.

With the

typical four-year bond issued by the government, the initial issuance fits

perfectly with the concept of maturity matching.

Taxation without

Representation

The major issue here is that the 100-year bond throws out

the entire notion that no prior governing body can bind a future governing body

to any activity. The 100-year bond is a solemn promise

that people a century from now are obligated to cover the expenses of today’s

borrowings. Obligating hundreds of millions of unborn people to pay for

our expenses today is the very meaning of taxation without representation. The only option handed to the future generation is to either

pay for today’s excesses or default on that debt and undermine their own

priorities in the process.

While the four-year

bond has some questionable elements since the life of these bonds do extend

beyond the life of both the current and subsequent Congress, the ethical impact is limited to whoever turned 18 during the

following Congressional session. That

Congress can then decide at the time to either pay it or roll-over to what are

still, effectively, the same people it represents. Congress

today doesn’t even have this overlap as no one of voting age now will likely be

alive when the debt is due.

The concept of public debt is already on shaky ethical

grounds, but those ethics are generally limited by the short-term nature of

those debts. They do give the option to those who issued the debt to eventually

pay it off. However, the 100-year debt is highly questionable as they’re

designed to safely insulate the beneficiaries from the costs.

In the immortal words of John Maynard Keynes, “In the long run, we’re all dead.” And what better way to

leverage that long run than by issuing a century bond? We’ll be dead when it

comes due, SO WHO CARES?

….

----

----

SO WHO CARES?.. about BONDS WRECK PENSION PLANS.. YOU will know it

SOON

“It is financial vandalism and the government and central banks need to wake up

to this.”

….

YES it is financial vandalism or pillage. People WILL REVOLT… no doubts about

Unnaturally Low and negative yield

bond yields are wrecking pension plans.

See Chart:

Bloomberg Barclays Global Agg

Sovereign Bond Yields

{kind=link}

Negative-yielding debt has spread to

more than 30% of the world’s investment-grade bonds -- the most ever.

See Chart:

{kind=link}

Pension World

Reeling

Most US pension plans assume returns

of six to seven percent. They have shied away from government bonds

because yields have been too low.

“The true madness is pension funds being

forced to invest in assets which will be guaranteed to lose, such as in the

case of long dated inflation-linked gilts at real yields of -3%,” said Mark Dowding, chief investment officer

at BlueBay Asset Management, which has pension-fund mandates.

“It is financial

vandalism and the government and central banks need to wake up to this.”

Vandalism or Fraud?

Five Choice Terms

- Fraud

- Theft

- Counterfeiting

- Robbery

- Vandalism ( as pillage & intentional plundering)

I discussed this

setup in detail in Negative

Yield Curves to Infinity and a Reader Question Regarding Fraud

Please read the

above link if you don't understand why negative yields constitute fraud, theft,

or counterfeiting, and why negative yields can never

occur in the absence of manipulation.

….

----

----

RELATED:

"This, on its face, is blatant price fixing..."

====

Changes in the prices of sushi offers one example where prices are rising much faster than is reflected

in the 'official' data...

Prices are

rising much

faster than the CPI would have you believe.

====

The official story:

well documented. El Coronel

Trump tiene quien le escriba

...this isn’t 1995.

From a short-term

market perspective, the risk is to the downside next week:

- Historically, September is one of the weakest months of the year, particularly when it follows a weak August.

- The market remains range bound and failed at both the 50-dma and downtrend line on Friday

- The oversold condition has now reversed. (Top panel)

- Volatility is continuing to remain elevated.

- Important downside support moves up to 2875

- The bulls regain control of the narrative on a breakout above 2945.

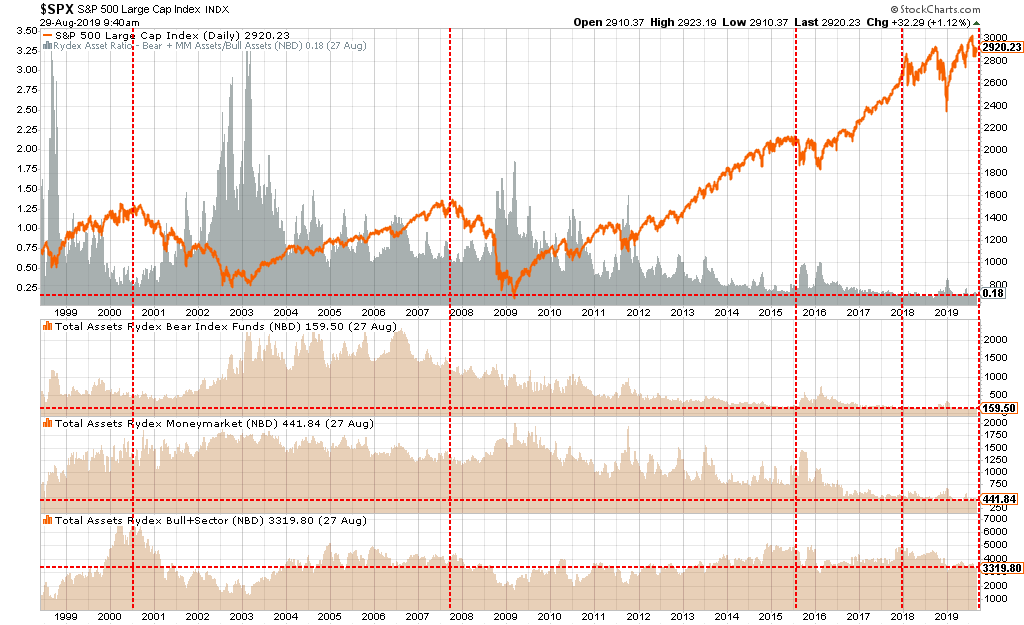

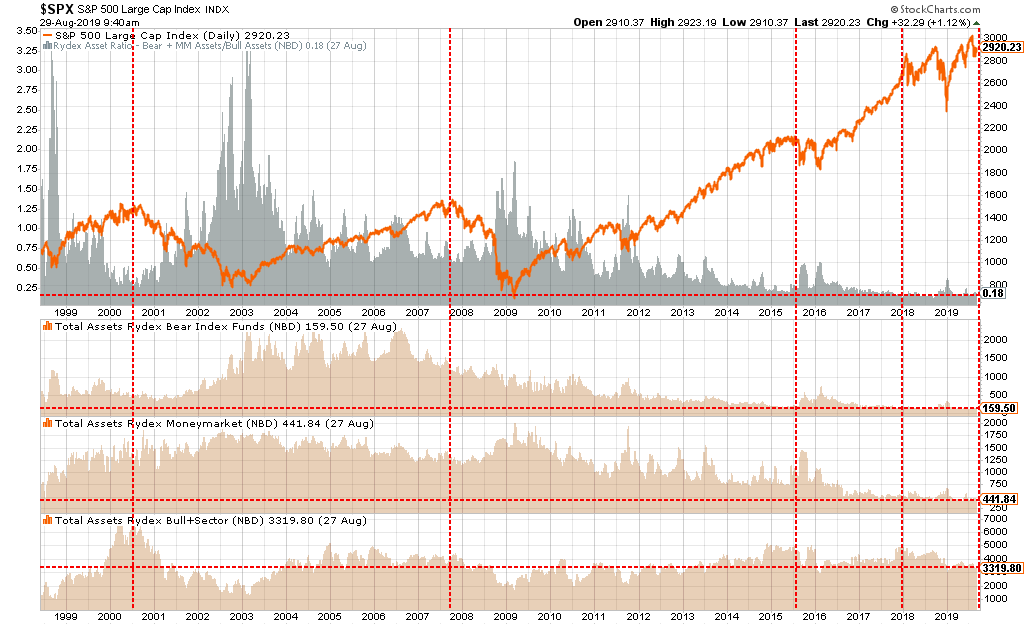

See Chart:

$SPX S&P 500 Large Cup Index

{kind=link}

BREAKING

DOWN THE BULL/BEAR ARGUMENT

Here few of

the “myths” which prevail

in the markets currently.

1) Sentiment Is

Hardly Bearish

Currently, individuals could not be more confident about the

markets or the economy. As shown in the chart below both investor confidence

about the economy, and expected returns from stocks

over the next 12-months, are near record highs, not lows.

See Chart:

Consumer Composite Indices

{kind=link}

2) Record Outflows?

In total, long-term fund flows collected $224

billion in the first half of the year, slightly ahead of 2018’s $219 billion.”

See Chart:

{kind=link}

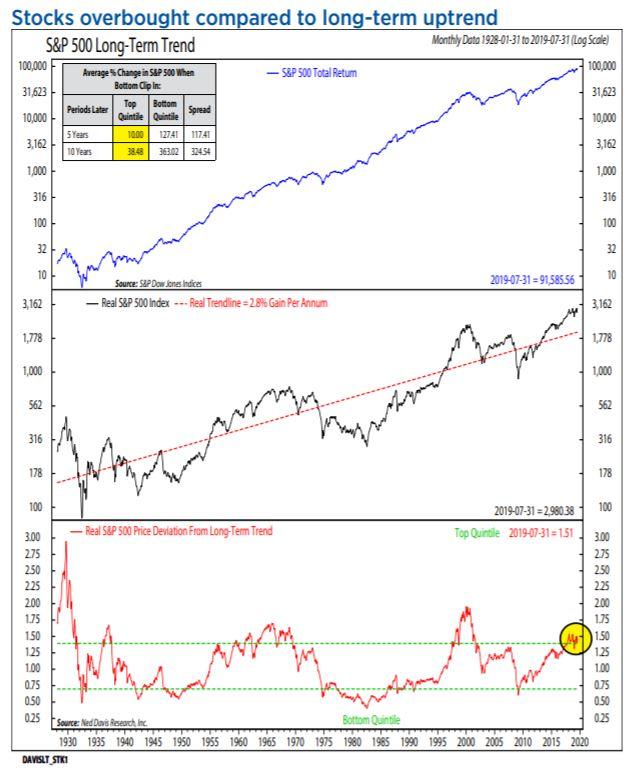

Furthermore,

it is hard to suggest there are record outflows when the market is extremely

overbought. As Ned Davis noted:

“Stock market bulls have been

arguing for months that muted stock market valuations and consistent

equity-fund outflows are proof-positive that stock-market investors are not feeling the sort of euphoria that

typically exists before the start of an economic recession or bear

market. But a longer-term view of equity valuations and allocations

indicates ‘excessive optimism.'”

See Charts:

https://www.zerohedge.com/s3/files/inline-images/NedDavis-Stocks-Overbought-083019.jpg?itok=d9ShsWy5

{kind=link}

Davis, in

a note, said that the value of the S&P is much higher today than the

index’s average growth would predict. In fact, it’s higher relative to the

average than it has been 80% of the time.

3) The Myth Of Cash

On The Sidelines. To wit:

“Underpinning gains in both stocks and

bonds is $5 trillion of capital that is

sitting on the sidelines and serving as a reservoir for buying on weakness. This

excess cash acts as a backstop for financial assets, both bonds and equities,

because any correction is quickly reversed by investors deploying their excess

cash to buy the dip,”

However, the reality

is if they haven’t done it by now after 3-consecutive

rounds of Q.E. in the U.S., a 300% advance in the markets, and ongoing global

Q.E., exactly what will that catalyst be?

Clifford Asness previously touched on this issue as well.

“There are no sidelines. Those saying this seem to envision a seller of stocks

moving her money to cash and awaiting a chance to return. But they always

ignore that this seller sold to somebody, who presumably moved a

precisely equal amount of cash off the sidelines.”

Every

transaction in the market requires both a buyer and a seller with the only

differentiating factor being at what PRICE the transaction occurs. Since this is required for there to be

equilibrium in the markets, there can be no “sidelines.”

Furthermore, despite

this very salient point, a look at the stock-to-cash ratios also suggest there

is very little available buying power for investors current.

See

Charts:

{kind=link}

The

reality is that investors remain more invested in riskier assets than

has historically been the case. And, as Ned Davis noted:

“Cash is low, meaning households are fairly fully

invested.”

See Charts:

{kind=link}

4) Not A Bull In

Sight

“Our full year GDP is on pace for 2.6%, which

is stronger than the average annual GDP of this entire 10½ year expansion.

Unemployment is near record lows. Consumer confidence is near record highs. And

corporate earnings continue to impress.

None of that says recession.

But let me just play along for a moment and

pretend that the inverted yield curve actually meant something this time around

– the fact of the matter is that the economy often

expands after an inversion, and the stock market goes up on average of

double-digits afterwards.

If anything, the inverted yield curve is one

of the best buy signals of all time.”– Kevin Matras, Zacks Research

Or, this:

“Despite recent recession fears and yield

curve inversions, the bull market should live on until early 2021, analyst Tom

McClellan said Thursday on CNBC’s ‘Closing

Bell. ‘ Everyone needs to just keep their pants on for now and realize that

the yield curve gives a really long early warning about trouble. It doesn’t say

that trouble is upon us now. It takes several

months to over a year before we get the final price high after a yield curve

inversion. If you get an instance like 1995, there was a very

momentary yield curve inversion and then it backed off and the bull market kept

on going. So that is possible.” – CNBC

You can’t get much more

bullish than that.

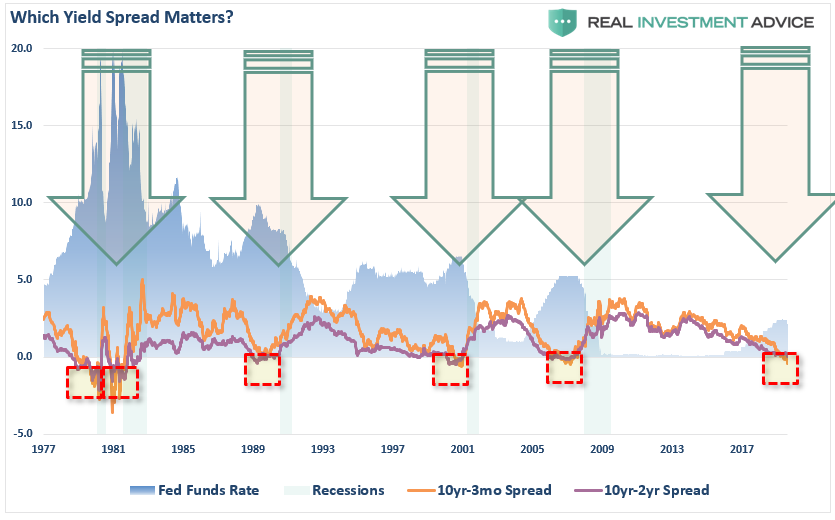

However, as I wrote

previously in “The Yield Curve Is Sending A Message:”

“While everybody is ‘freaking out’ over the

‘inversion,’ it is when the yield-curve

‘un-inverts’ that is the most important.

The chart below, shows that when the Fed is

aggressively cutting rates, the yield curve un-inverts as the short-end of the

curve falls faster than the long-end. (This is because

money is leaving ‘risk’ to seek the absolute ‘safety’ of money markets, i.e.

‘market crash.’)”

See Chart:

{kind=link}

Lastly, this isn’t

1995.

The Fed is

cutting rates with the “yield curve” inverted.

I wouldn’t dismiss that too quickly.

Kevin Matras is

correct. The stock market DOES indeed go up double

digits following a yield curve inversion. The only issue is that it is the

first step in recovering from the bear market that preceded it.

[ Interesting .. I will re-read it to make my

comments ]

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

"If I

had hair, I’d be pulling it out. I’m really concerned about the financial

performance of the business, knowing that if we continue to eat this cost, how

much it hurts."

====

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

Hezbollah

claims successful attack on an Israeli military vehicle which "killed and wounded those inside"...

====

The People’s Bank of

China (PBoC), the

country’s central bank, has announced that

it is planning to launch a central

bank digital currency (CBDC), inspired in

part by Facebook’s Libra project...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

-London Mulls Sending Drones to Persian Gulf

Amid Escalation of Tensions With Iran - Reports The whole middle East will be burned

& then London & Jerusalem bunkers +

- 'Catastrophic'

Hurricane Dorian Pounds Bahamas, Prompts South Carolina, Georgia Coastal

Evacuation

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

RT EN ESPAÑOL

- PRIMERAS IMÁGENES: El huracán Dorian destruye casas, autos y árboles en su potente paso por las Bahamas

- Trump sobre Dorian: "Las Bahamas, golpeadas como nunca antes"

- MINUTO A MINUTO: El huracán Dorian azota a Bahamas

- VIDEO: Irán presenta su nuevo dron de alta precisión que puede atacar blancos lejos de sus fronteras

- "Las Ábaco van a ser borradas": Expertos prevén "devastación y un impacto catastrófico" del huracán Dorian en las Bahamas

- El Gobierno argentino anuncia controles a la compra de dólares desde el 2 de septiembre

- 'Jesús Santrich' reaparece en un nuevo video de las FARC y llama a crear una nueva constituyente en Colombia

- Keiser Report "Insurrección mundial": la nueva era del oro y el bitcóin y la rebelión contra el dinero fíat y los bancos

----

----

PRESS TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario