Something else is restraining trade well

beyond any Chinese goods heading toward the United States waiting to be further

tariffed. This is widespread, very

close to universal...

Trade

between Asia and Europe has dimmed considerably. We

know that from the fact Germany and China are the two countries out of the

majors struggling the most right now. As a consequence of the slowing, shipping

companies have had to make adjustments to their fleet schedules over and above

normal seasonal variances.

It was reported last week that Maersk and MPC would “temporarily suspend”

their sailings on one of the biggest routes between

Europe and Asia.

This

followed a material downgrade in Mexico, of all places, another economic system

highly dependent at the margins on the whims of global trade.

Everywhere you turn,

there are references to global demand while at the same time, by my own

unscientific count, fewer and less emphatic protests over trade wars.

Something

else has to be restraining trade well beyond any Chinese goods

heading toward the United States waiting to be further tariffed. This is widespread, very

close to universal.

That’s why US

exports, for example, are struggling. By conventional terms, that should be the

case – the dollar began rising in the middle of last year making US goods less attractive meaning relatively more expensive on

world markets. That is a reason why US

Presidents claim a strong dollar policy (as if there could be one) in public and in private (and sometimes public) cheer whenever it falls in exchange value.

But as the struggles

in the rest of the world show, the American loss is no

one’s gain. That’s the part none of them ever get – this isn’t the

losing end of beggar-they-neighbor. The rising dollar

leaves no winners in its wake. None.

Rather than

redistribute stable purchasing power and reflect strong demand toward relative

changes in costs, what’s left is only weakening demand

in all cases. Europe, Asia, Central and South America, even the United

States.

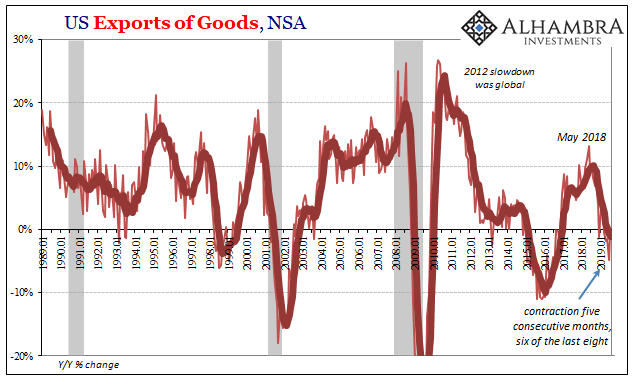

According to

estimates released by the Census Bureau this week, US

exports are now routinely falling. Unadjusted, exports to the rest of

the world have contracted in each of the last five months (through July 2019).

Not by huge amounts, though in June it was just about

-5%, more importantly the 6-month average has reached -1.2%.

See Chart:

US exports

of Goods, NSA

{kind=link}

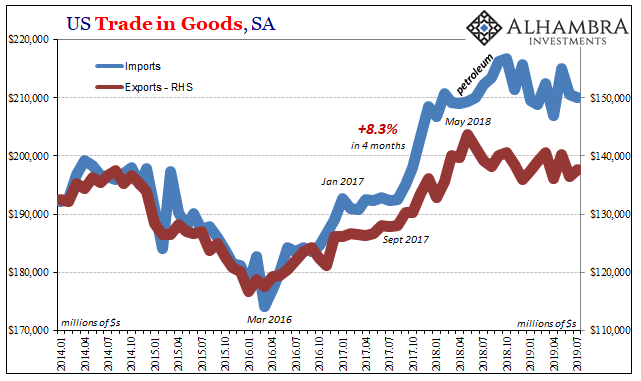

Seasonally-adjusted,

the Census Bureau leaves no doubt as to the cause. The peak in the reflation

export cycle was unsurprisingly May 2018 (29th). The

dollar goes up, and collateral draws tight, global trade suffers not because of

trade wars or the cost of US goods relative to alternatives but because the

lack of sufficient dollar availability slowly squeezes the life out of global

demand.

See Chart:

US Trade

in Goods, SA [ Less exports than imports ]

{kind=link}

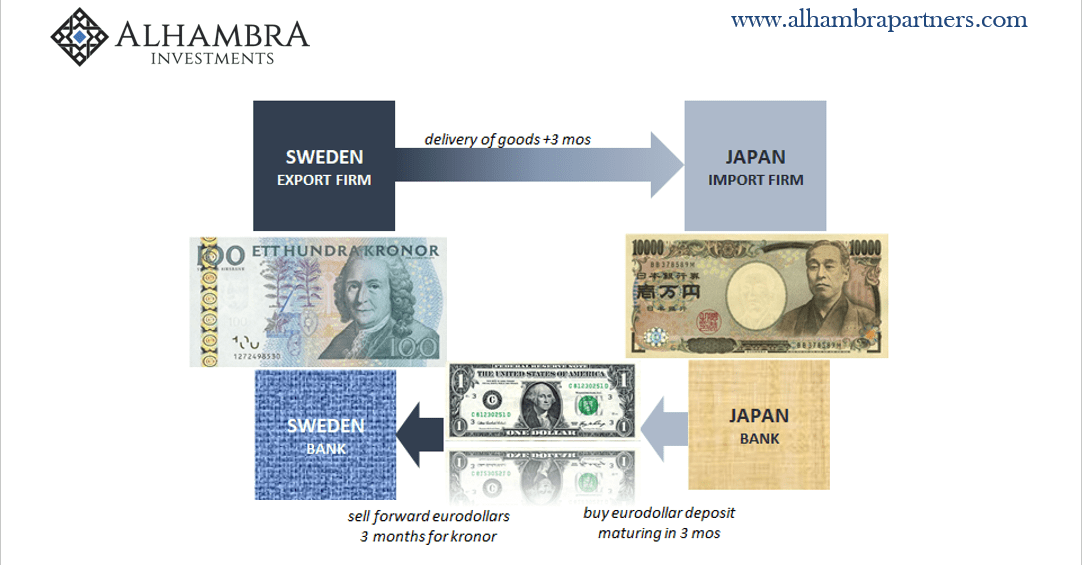

Trade suffers

first because the global reserve currency is its first requirement, the ability

to fluently, efficiently translate economic factors from one system to another. There’s almost no appreciation for the

functions – and what those actually are – of a

global reserve.

A reserve currency is an intermediator, more

than a buffer between national systems often with very little in common.

Starting with currency denomination and monetary terms. The example I

often use is an export firm in Sweden obtaining goods in that country to be

shipped to Japan for final use. The trade can certainly happen without a global

reserve, but not efficiently…

If, however, both sides can use a currency

that is common in both areas it then obviates the need for either of their

national denominations. Should Japanese as well as Swedish banks both hold balances of this

middle currency as a regular part of their business, no special concessions

required, then trade becomes easy and (very nearly) free.

The downside is that this requires a whole lot

of that middle currency to be made available practically everywhere.

See Graph

ALHAMBRA

Investments

{kind=link}

You can

then see why global trade downshifted in and around the Great “Recession” and

never really came back – though it was predicted to, and everyone especially in

the EM’s was counting on it. Before

the Global Financial Crisis in that eurodollar system, the middle currency was

freely available for use anywhere. Nowadays, it’s so much harder to source and

maintain funding.

It doesn’t shut off trade

completely, but it does slowly squeeze the life out of it over time. The global regime is starved of its

monetary oxygen. That’s why there are no winners; the dollar shortage isn’t a redistribution of demand, it is

the slow erosion and even destruction of it (as it infiltrates the supply side,

like in China).

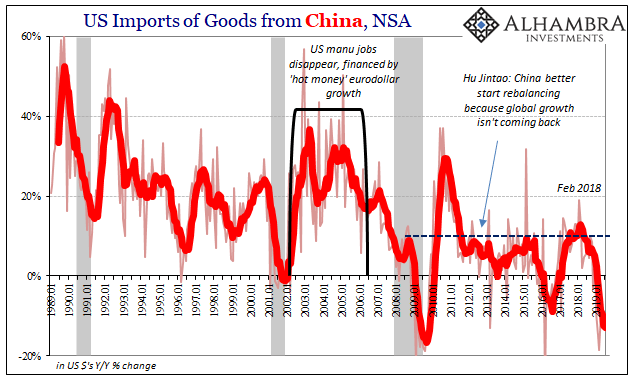

See Chart:

US Imports of Goods from China

{kind=link}

We see these same effects on the other side of the US

merchandise ledger, too. While American importers are bringing in fewer Chinese

goods because they are being marked up by levies, they aren’t making up for

them by buying extra anywhere else. Imports into the US are falling as

inventory builds up across the domestic supply chain.

The global

slowdown is a global slowdown. The monetary squeeze is not entirely fixated on

global trade, that’s just where it is most visible and easily discernible. It

therefore proposes a far different set of solutions (from a US perspective)

than kill the dollar.

If only it was that easy.

Macro Voices Podcast

….

----

====

----

No hay comentarios:

Publicar un comentario