ND

SEP 2 19

SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

"The

roof was blown off, with wind and rain battering inside the house..."

====

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

For equity markets, August was the most violent month of

2019, with the S&P tumbling 2.6% or more on at least three occasions, the

same as the number of instances when the Dow plunged almost 1000 points - the

worst since Q4 of 2018 when the S&P briefly entered a bear market - only to

rebound furiously after Mnuchin's infamous Christmas Eve phone call. Worse, in August the number of days when the S&P moved up

or down by more than 1% was the highest since the February 2018 inverse VIX ETN

implosion.

See Chart:

{kind=link}

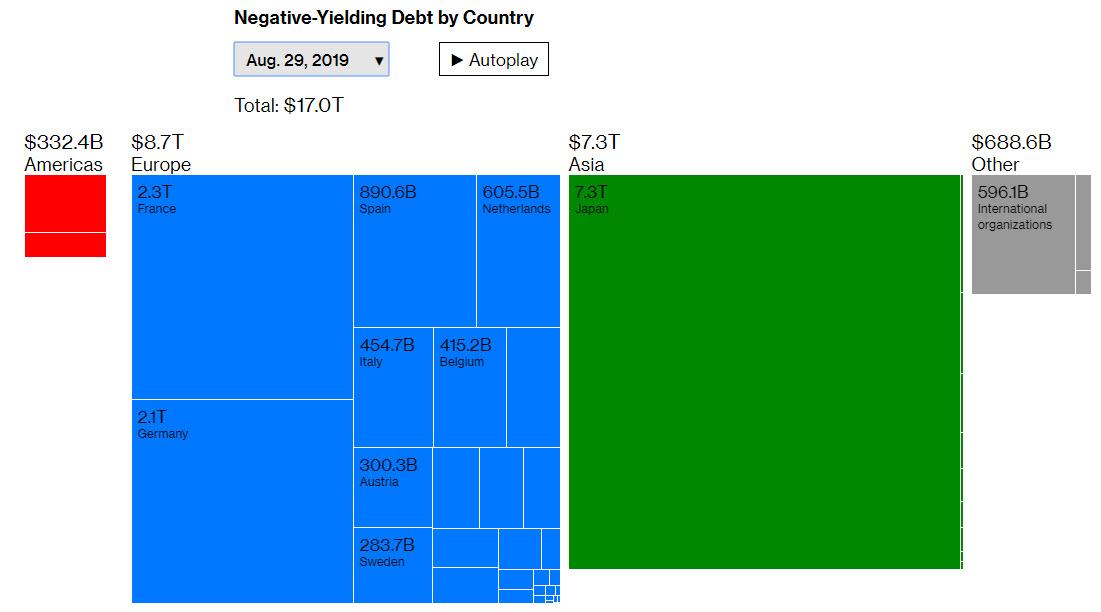

One constant in August for markets however was the

unstoppable rally for government bonds. Indeed last month saw the amount of

negative yielding debt in the world touch a new all-time high

above $17 trillion, as the majority of European countries

saw their 10y yields hit new record lows with BTPs even closing below 1.00% for

the first time ever.

See Graph:

{kind=link}

The last

time Bunds had a stronger month was June 2016 while for Treasuries you have to

go all the way back to November 2008.

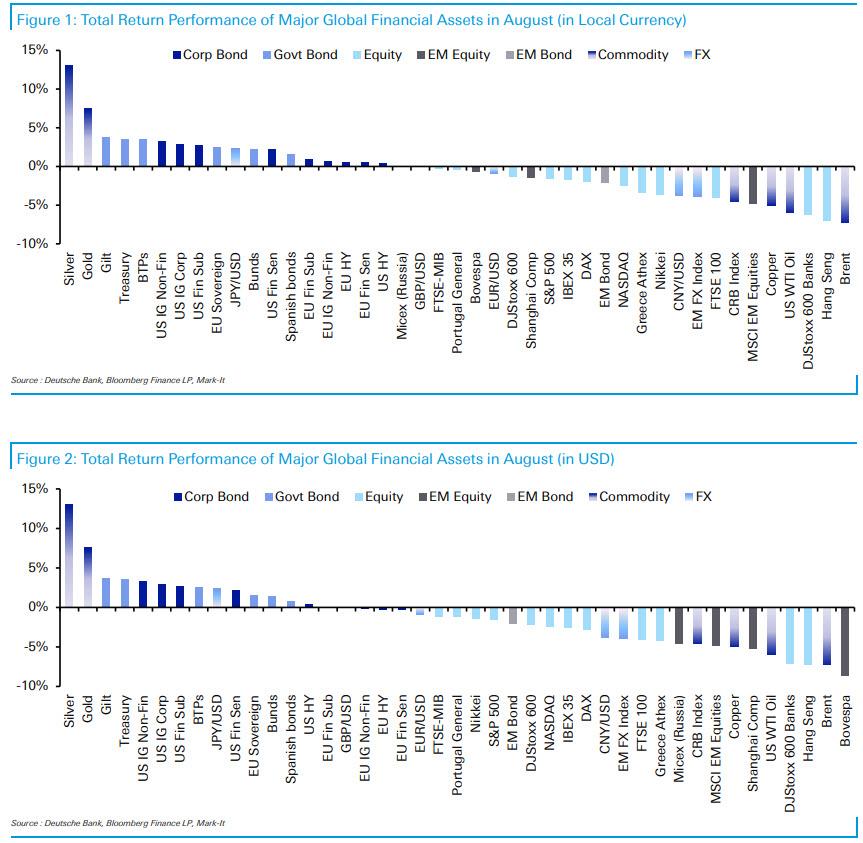

As Deutsche Bank further notes, the big rally in rates also

helped investment grade credit to strong total returns last month. Indeed USD

IG returned +3.3% while sub and senior financials returned +2.7% and +2.2%

respectively. EUR IG on the other hand returned a more modest +0.7%. Wider

spreads in HY limited returns with USD and EUR HY returning +0.4% and +0.6%

respectively.

While credit and government bonds made up the bulk of the

assets which delivered positive total returns last month, Silver (+13.0%) and

Gold (+7.5%) actually occupied the top two spots on the returns leaderboard as

precious metals benefited from the risk-off in equity markets. All-in-all, 18 out of 38 assets

(excluding FX) in Deutsche Bank's asset scorecard that finished with a positive

total return in local currency terms while 14 did so in dollar terms.

See Charts

{kind=link}

In terms

of where that leaves us year to date, there are still 36 out of 38 assets

with a positive total return in both local currency and dollar terms. The two laggards are Copper (-3.7%) and now

European Banks (-4.0%) following the move in August. Top of the leaderboard is the

Greek Athex (+44.1%) which is a fair way ahead of the next equity market in

Russia's MICEX (+22.0%). The S&P 500 and STOXX

600 have returned a solid +18.3% and +16.0% respectively.

See Charts:

{kind=link}

Meanwhile, USD credit is up +10.5%

to +15.3% with IG outperforming HY while EUR credit is up +6.4% to +10.2%. As

for bonds, BTPs (+12.5%) lead the way while Treasuries and Bunds have returned

+9.0% and +7.6% respectively. Finally in commodities, outside of the decline

for Copper, Gold (+18.5%) and WTI Oil (+21.3%) have seen a big rally this year.

….

----

----

----

----

"Against

this geopolitical backdrop we return from the summer to continue to see global

markets which now aggressively buy equities for their yield and bonds for

capital appreciation."

The Context today

How about Germany’s far-right AfD being projected to

achieve 27.8% of the vote in Saxony and 23.5% in Brandenburg? Yes,

they are not in power, or even close to power, but this is with low

unemployment and what had been until recently a healthy German economy. Quite the worrying historical irony there.

How about former Far-right Italian

Deputy PM Salvini, now out of power, calling for his supporters to march

on Rome? True, that’s more 1920s than 1930s, but given the technocratic PD look

like they will be running the finance ministry again, where they did so well

last time that we ended up with a populist government, many are betting that

Salvini will be back with a majority at some point.

How about Argentina reintroducing capital controls (yet

again)? Well, they have. Exporters now have to repatriate

USD within five days, and central-bank authorization is now required to buy

USD, except in the case of foreign trade. Individuals will be limited to

purchasing USD10,000 per month. Correct

me if I am wrong, but wasn’t the Argentina bail-out the

benchmark achievement of one Christine Lagarde, now about to run the ECB? I am

asking for a friend…

And literally talking of ‘back with

a bang’, yesterday we came

perilously close to the start of a full-blown conflict between Israel and

Hezbollah, which fortunately appears to still be lurking for some

future date for now. That might sound irrelevant for a market already looking

at the map with an expression like Munch’s ‘The Scream’ and asking “Where next?”, but when/if that war occurs it risks a far larger

regional conflagration.

Meanwhile, against this geopolitical backdrop we return from

the summer to continue to see global markets which now aggressively buy equities for their yield and

bonds for capital appreciation: which is a brilliant strategy until rates have

been cut to new negative terminal lows and stock multiple expansion is at new

highs: at which point the music stops and someone is left holding

seriously over-priced and under-delivering cans. And

nobody makes any returns at all – which will be a real big bang.

….

----

----

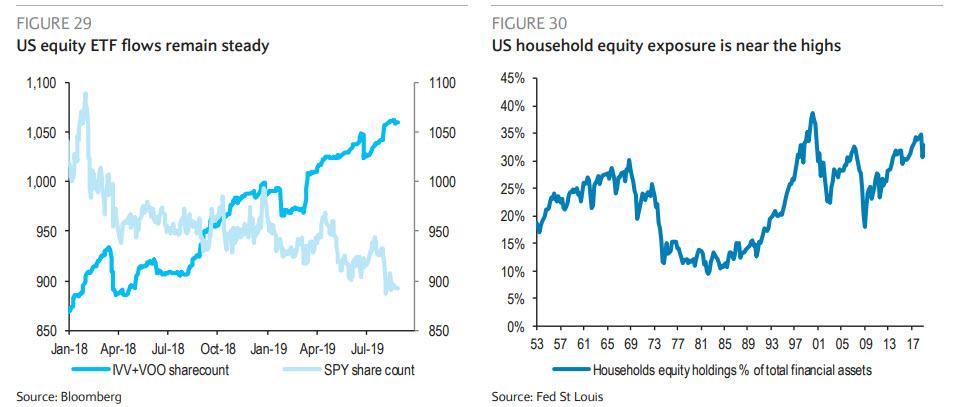

As a

recession seems to be on everyone’s lips, allocation to bonds and cash keeps

growing and while Institutional investors are moving further away from

equities, retail investors are splurging on stocks, supported by stock buybcacks.

Finally, there is the most reliable "bagholder" in

the world to sell to: retail investors. Barclays also notes that retail

investors have not reduced equity exposure during the recent correction; in

fact quite the opposite. Flows into the most popular US

equity ETFs, which are a good proxy for retail exposure, have remained steady

in August, while they fell during the previous corrections of February ’18,

December’18 and May ’19. In other words, when it comes to believers in

BTFD, it's most retail that is left.

See Charts:

{kind=link}

….

----

----

Inequality get worse

...the soaring

CEO-to-worker pay ratio is not an example of why capitalism is

inherently flawed... it is a

byproduct of central banking and fiat currency rather than capitalism.

See Chart:

{kind=link}

….

SOURCE: https://www.zerohedge.com/news/2019-09-02/why-has-us-ceo-worker-pay-ratio-increased-so-much

----

----

A lingering

risk is that global macro hedge funds may be due for a reality check. Global

macro hedge funds look isolated in their bullishness; other speculative traders

appear less than eager to take on risk.

See Charts:

{kind=link}

….

SOURCE: https://www.zerohedge.com/news/2019-09-02/market-thin-ice-have-stocks-sucessfully-averted-crisis

----

----

Disappointing global

outlook:

The

business cycle transition matrix is very sticky meaning that as soon as the

leading indicators on the business cycle enters the recession phase (below

trend and declining) then its stays in this state with an 87% probability.

Summary:

Our main view remains to underweight equities vs bonds as

leading indicators on the global economy continues to weaken. The drivers of

the next recession will centre on the US-China trade war which inherently

cannot be modeled and thus Fed's macro models will not flash red on aggressive

rate cuts before it's too late. The highly correlated market structure we have

observed in 2019 is cause for concern if investors switch into risk-off mode

during the coming months.

* * *

Still

underweight equities

Global equities in local currency were down 2% in August as

the US-China trade war escalated reminding investors that we might be a long

way from a resolution to the biggest geopolitical confrontation since the fall

of the Berlin wall. In August global government bonds

rose 2.9% in local currency playing into our Q3 Outlook theme that investors

should be underweight equities relative to bonds. This outlook remains our view.

But how underweight equities should investors be?

See Chart:

{kind=link}

South Korea-China trade is going

down

See Chart:

{kind=link}

Over the weekend a new round of US tariffs worth $112bn went

into effects on consumer goods such as shoes, nappies and food. This comes on

top of new tariffs from China and Trump administration has more tariffs in the

pipeline with the intention to go into effect in mid-December. Also, China will

celebrate on October 1, 2019 the 70th anniversary of the founding of the

People’s Republic of China which means that Xi

Jinping will most likely not soften any stance against the US as this is an

important milestone for China.

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

“...it can’t be Warren and it can’t be

Sanders.” That’s

the decision from Wall Street. The decision fromMain Street is yet to be heard...

====

"What a fascinating

environment; each week bringing something extraordinary. Yet there is

this dreadful feeling that things are advancing toward some type of cataclysm..."

The Fed’s

political problem will not end with Donald Trump or Chinese trade negotiations.

I expect

Trump's attacks are the first salvo in what will be only more intense political

pressure directed at the Fed to employ aggressive stimulus measures.

The rise

of populism is in its initial stage. The

situation turns much more serious when the current Bubble deflates. There are

major costs associated with the Fed’s loss of independence – independence from

politics as well as from market pressure. For now, however, markets are trading on the

prospect of aggressive global monetary stimulus (rate cuts and QE).

====

Without a

doubt, the market is more primed

for a crash than it has been at any point since 2008, and it definitely

will not take much to make this a “September

to remember”...

====

"The 34 passengers were

trapped below decks... The fire was so intense that even after it

was put out, we're not able to actually embark the vessel..."

====

"I characterize that as a reset, and it does have the potential to fall farther."

====

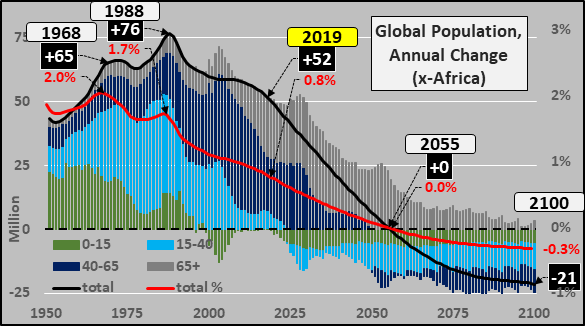

Elon Musk continues to suggest a population collapse is in store within a few decades

time...and he is 110% correct if you make two caveats...

The Big Picture

Annual global

population change, excluding Africa, peaked in 1988 and growth has decelerated

since. However, growth really

decelerates from here and is projected to end entirely by 2055...and global

depopulation (excluding Africa) is the primary global feature there-after

See Chart:

{kind=link}

….

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

5.7% of all energy companies with junk rated bonds are defaulting as of

August, the highest level since

2017. The metric is "considered a key indicator of the industry’s financial stress."

====

Bitcoin trading has hit a giant new record yet again in Venezuela as the country’s crippling hyperinflation

continues to play out...

====

"I

have not been on the streets, not in shopping malls, can’t go to a hair salon.

I can’t do anything..."

====

"The

end is coming for those attempting to disrupt Hong Kong and antagonize

China."

====

OPEC’s

production increased in August thanks to Iraq and Nigeria a Reuters survey

found on Friday.

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

- It's Necessary to Find Way to Counter US,

Otherwise Nuclear Deal Won't Be Only Loss, Iranian FM Says

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

====

ALAI ORG

Polit-Econ: Wallerstein sin anestesia Atilio

Boron

Polit-Econ: Immanuel Wallerstein: In

Memoriam Ana Esther Ceceña

====

RT EN

ESPAÑOL

- Primer ministro de Bahamas: El huracán Dorian ha generado una "devastación sin precedentes" en las islas Ábaco

- Bolsonaro cancela asistencia a cumbre regional sobre la Amazonía por recomendación médica

- Desaparece la medallista olímpica española Blanca Fernández Ochoa: ¿qué se sabe?

- "¿Para qué he sobrevivido?": Recuerdos de la trágica toma de rehenes en la escuela de Beslán

- Descubren dentro de un meteorito un mineral nunca antes visto en la naturaleza

- VIDEO: Roger Waters de Pink Floyd canta en apoyo a Assange ante el Ministerio británico de Interior

- Registran la segunda mayor tormenta magnética del año que está afectando a la Tierra

- El huracán Dorian se acerca a Florida tras su devastador paso por Bahamas

- Keiser Report "Insurrección mundial": la nueva era del oro y el bitcóin y la rebelión contra el dinero fíat y los bancos

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

- A Society Is Only As Free Is Its Most

Troublesome Political Dissident

By Caitlin Johnstone

By Caitlin Johnstone

- The end of the dollar as we know it By Andy Langenkamp

- The Last Act of the Human Comedy By Chris Hedges

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

Christine Owens Democracy

Needs Unions

Ralph Nader From

Trump Tower to Trump Power Over Law

Binoy Kampmark Justifications

for Inequality: The Neuroses of Kochland

Robert Koehler We Are

All Indigenous

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

----

----

PRESS TV

Resume of Global News described by Iranian observers..

- ‘Hezbollah raid was game changer, sent warning to Israel’

- Huawei denies US allegations of technology theft

- Iran, France hold intensive expert-level talks on JCPOA

- China takes US to WTO amid escalating trade war

- 2 politicians killed with long-range weapons in Colombia

- IMF calls for negotiated solution to US-China trade dispute

- UN official blasts Nigeria’s use of ‘lethal force’ on Muslims

- Bahama PM confirms Dorian deaths on Abaco Islands

- PROGRAMS

- 'Fear: Trump in the White House' by Bob Woodward

- Recent confrontation between Lebanon's Hezbollah and Israel

- Another Saudi massacre in Yemen: over 100 killed

- Hezbollah shattered Israel's sense of impunity: Expert

- Hezbollah hits back

- Is Modi targeting Muslims in India?

----

===

No hay comentarios:

Publicar un comentario