ND

SEP 14 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

Questioning “mutual assured destruction,” Charles Kupperman

called nuclear conflict “in large

part a physics problem.” [[ Physics: Idiotic view of nuke-war ]]

----

Any nuclear-war at this time lead to MAD (Mutual

Assured Destruction). It leads to genocide of both contenders RU-China ++ and

US-NATO supporters. To believe that nuclear war is “winnable” is

a sing of serious psychological disorder. It is

a delusional disorder that mixed schizophrenia + paranoia = criminal mind. Trump need to be put under psychiatric custody.

His sickness is a prove that he is not our President

any longer. The Supreme Court

has to demand his immediate resignation, put him in jail for crime against Peace and put the Nation under temporary-regimen in charge of calling immediate elections.

----

----

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

...there's a "very clear

cyclical downturn in jobs growth, there's really no debating that,

and it looks set to continue."

The Economic

Cycle Research Institute's (ECRI) Lakshman Achuthan recently

sat down with CNBC's Michael Santoli to discuss the jobs growth downturn. Keep

in mind, this conversation was held on Wednesday, several days before

Friday's disappointing jobs

report.

Achuthan told Santoli there's a "very clear cyclical downturn in jobs growth,

there's really no debating that, and it looks set to continue."

Achuthan said January 2019 marked the cyclical peak in jobs

growth, has been moving lower ever since, and the trend is far from over. Both nonfarm payrolls and the

household survey year-over-year growth are in cyclical downturns, he said.

See Chart:

JOB GROWTH DOWNTURN

{kind=link}

Achuthan emphasized to Santoli that ECRI's recession call won't be

"taken off the table. We've been

talking about a growth rate cycle slowdown.We're slow-walking toward -- some recessionary window of vulnerability --

we're not there today -- but this piece of the puzzle

[jobs growth downturn] is looking a bit wobbly. This is the main message that

Wall Street is missing."

As Wall Street bids stocks to near-record highs on

"trade optimism" and the belief that the consumer will save the day,

in large part because of solid jobs growth. ECRI's Leading Employment Index, which correctly

anticipated this downturn in jobs growth, is at its worst reading since the

Great Recession.

However, this time around, the

inflation downturn signal arrived in September 2018, the moment when the Fed

should have started the cut cycle. With a ten-month lag in the cut cycle, belated

rate cuts have always been associated with recession.

See Charts:

Inflation Downturn Signals and Rate Cuts

{kind=link}

And now it should become increasingly clear to readers why President Trump has sounded the alarm about the need for

100bps rate cuts, quantitative easing, and emergency payroll tax cuts - it's

because he's been briefed about the economic downturn

that has already started.

….

----

----

"The headwinds for retail are gaining hurricane force."

The collapse of the

brick and mortar retail space is continuing at a breakneck pace in 2019. The

latest victim, Forever 21, is expected to file for bankruptcy as soon as

Sunday, according to the Wall

Street Journal. JP Morgan is the company's most senior lender and has

agreed to roll over its loan to the retailer into a bankruptcy financing

package, according to the report.

But despite "people familiar with the matter"

claiming that bankruptcy is imminent, the company has come out and said that it

doesn’t have any plans to file for bankruptcy.

Let’s revisit that statement early next week.

This bankruptcy marks the latest in what has been nothing

short of carnage so far this year for the retail industry. Between January and

June in 2019, more than 7,000 retail stores closed. This

amounts to more than all of the

stores that closed throughout the entire year of 2018. Many were hurt by

a lackluster holiday shopping season at the end of 2018.

See Link address:

Robert Feinstein, a bankruptcy lawyer who represents

creditors in major retail bankruptcies, including Payless and Gymboree said:

"The headwinds for retail are gaining hurricane force."… Jeffrey

Gennette, CEO of Macy's said: “The competition is fierce. Retail is

certainly not for the faint of heart.”

In the first six months of 2019, companies like Payless,

Gymboree and Charlotte Russe all filed for bankruptcy. Fourteen total retailers

with at least twenty stores each have filed for bankruptcy this year, according

to BDO. The list also includes Charming Charlie Holdings Inc., Barneys New

York, A’Gaci and Avenue Stores.

See Graph at:

Many of these companies have closed down stores as a result

of their respective bankruptcies. Some retailers are dropping their

well-known flagship stores and instead opting for smaller locations in urban

areas.

During the first half of 2019, 19 retailers said that they would close a

combined 7200 stores. Payless, Gymboree and

Charlotte Russe accounted for about 3,700 of these on their own.

For comparison, last year, there weren’t even 6,000 total

store closings announced. There were 6,600 closings in

2017. Recall, we reported in mid 2019 that 12,000 stores were forecasted to close this

year.

Marshal Cohen, chief retail analyst at NPD Group, says the

U.S. simply has too many stores per capita. He said: “We don’t need as many stores as we

have. Bankruptcies used to be a dirty word. Bankruptcies is a way to clean

up your challenged business.”

….

----

----

OFICIAL DATA : U.S.

POVERTY LEVELS FALL TO PRE-RECESSION LOW

...poverty has now fallen for

the fourth consecutive year, thanks to the healthy

state of the economy and it has hit pre-recession lows.

The U.S. Census Bureau has published

a report into income and poverty levels across

the United States, finding that median

household income in 2018 was $63,179 while median earnings for all workers was

$40,247.

Additionally, as

Statista's Niall McCarthy notes, poverty has now fallen for the fourth consecutive year, thanks to the healthy

state of the economy and it has hit

pre-recession lows.

See Chart at:

….

----

----

Vs. NON Official data

Michael SNYDER DATA 19 Facts About Current US Economic

Performance: I Dare You to Tell Me the Economy Is “Booming” By Michael

Snyder, May 05, 2019

----

----

CTA

positioning is currently extreme mostly in the bond space rather than in

equities or other asset classes, and as a result the violent reversal is taking

place in the 10Y Treasury, not the S&P500.

When the inevitable unwind comes, it will be fast and

furious: in fact, according to JPMorgan, this was one of the largest 3-day

Momentum-Value rotations in over 30 years (99.8%-ile), triggered by a

combination of

i) better than

expected economic data (something we also warned about last weekend),

ii) monetary and fiscal stimulus,

iii) easing trade

tensions,

iv) stabilization in

yields,

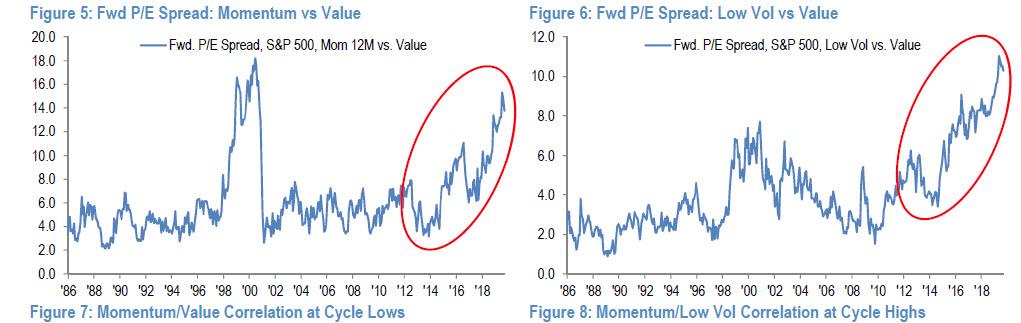

All at a time when factor positioning (long Momentum and

Short Value) was extreme as the following charts show.

See Charts:

Fwd P/E Spread Momentum vs. Value

{kind=link}

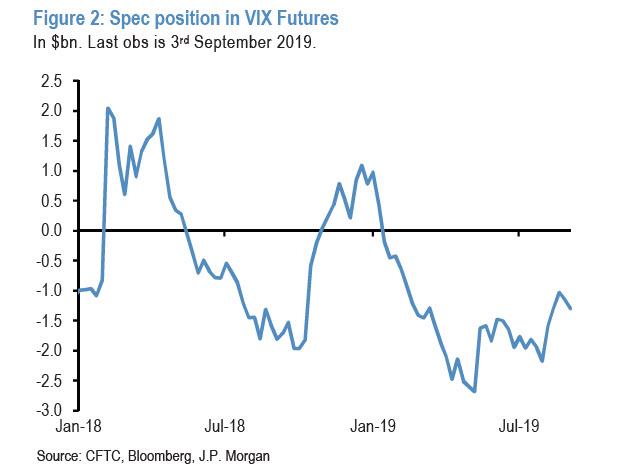

This in turn prompted JPM's Nikolas Panagirtzoglou to ask why, given

these sectoral and style shifts, the sharp losses suffered by CTAs and the

chatter about a Quant Quake, are equity markets so benign and calm... Especially compared to the

last time we had a Quant Quake in February 2018. As a reminder, back then not

only did global equities briefly enter a correction, slumping by 9% in a week

but the resulted rise in equity volatility – the VIX had spiked to close to 40%

– had induced capitulation on short volatility

positions causing a Quake in Volatility funds also. Furthermore, similar to

now...

See Chart:

Spec position in VIX Futures

{kind=link}

BUT

The current

backdrop is very different, for the simple reason that CTA positioning is

currently extreme mostly in the bond space rather than in equities or other

asset classes, and as a result the violent reversal is taking place in the 10Y

Treasury, not the S&P500.

We can see this in the following momentum signal tables which show the z-score as a proxy for the

strength of the momentum signal for each asset class. With the exception

of some niche commodities such as Nickel, extreme z

scores of 1.5 stdevs or above were only found in the bond space up until the

end of August.

See Charts:

{kind=link}

[ We’re in September and it didn’t

happen.. Why? ]

Yet while equities were insulated from a violent move, bonds

were not. In fact, the rise in bond yields since the start of the month, when

the 10Y dropped to a near record low 1.43%, induced CTAs to start cutting previously

extreme long bond futures positions, amplifying the move in yields.

At the same time, and unlike Feb 2018, there was no extremity in equity futures positioning to be unwound by

CTAs as they were only modestly long equities. As a result, the CTA losses

this month did not spill over to the equity market or equity volatility. As a

result, by being confined to the bond space, the CTA losses so far this month are close to

a third of what we had seen previously during February 2018.

[In short:] A similar

analogy can be observed for risk parity funds, an important component of the

Quant fund universe, which like CTAs are little changed MTD again contrasting

with the heavy losses they had suffered during February 2018.

Finally, what about equity hedge

funds? As Panigirtzoglou explains, the equity hedge fund universe is

dominated by the $900bn universe of Equity Long/Short hedge funds which are

more susceptible to equity sector shifts than other hedge funds. These Equity

Long/Short hedge funds are largely directional exhibiting a beta of close to

0.5 on average relative to the global equity market. Around 15% are

Quantitative, including the Equity Market Neutral category which typically

exhibits a very low equity beta.

So what did we learn from the

performance of Equity Long/Short hedge funds this week? On Monday HFR

released the performance of monthly reporting funds for August, when Equity

Long/Short hedge funds lost 1.63% (or 1.8% asset weighted) which implies a beta

higher than 0.5 relative to the MSCI AC World index which lost 2.6% of August. This suggest that, contrary to what that "other"

JPM quant claimed last week, Equity

Long/Short hedge funds were caught up with above rather than below average

equity exposures in August.

In other words, as Panigirtzoglou notes, the daily reporting

Equity Long/Short hedge funds appear to have been practically unaffected by

this month’s rotation, "casting doubt on the idea that they were at the heart of this month’s

rotation, thus shifting the blame to other equity investors outside Equity

Long/Short funds."

So where does the above discussion leave JPMorgan's

"bad cop" quant (not to be confused with the "good cop") in

terms of equity market positioning? Here, Panigirtzoglou makes five

observations:

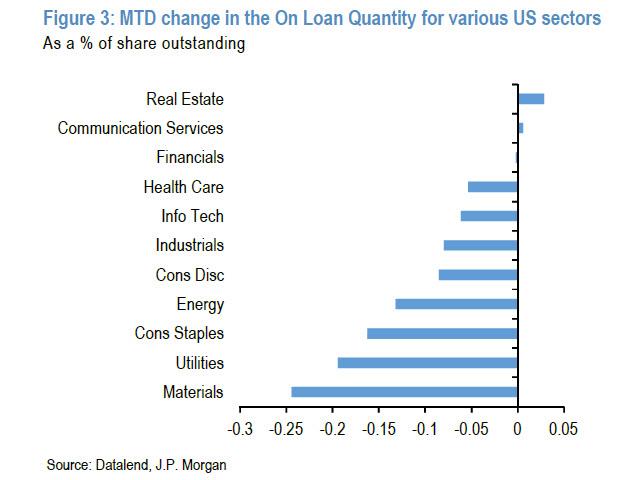

1) Not all of the sectors that outperformed MTD, i.e.

Financials, Energy, Industrials and Materials, were driven by short

covering. … Materials saw

the biggest short covering. Energy and Industrials saw some short covering also. But Financials saw little change in its short interest, suggesting

that the latter might have been boosted by new buying

rather than covering of shorts (Figure 3).

See Figure 3

MTD change in the On Loan Quantity

for various US sectors

{kind=link}

2) Figure 3 shows that most sectors saw short covering MTD

suggesting that overall equity positioning shifted to significantly less

bearish or more bullish stance relative to last August. This

is consistent with JPMorgan position metrics related to the overall US equity

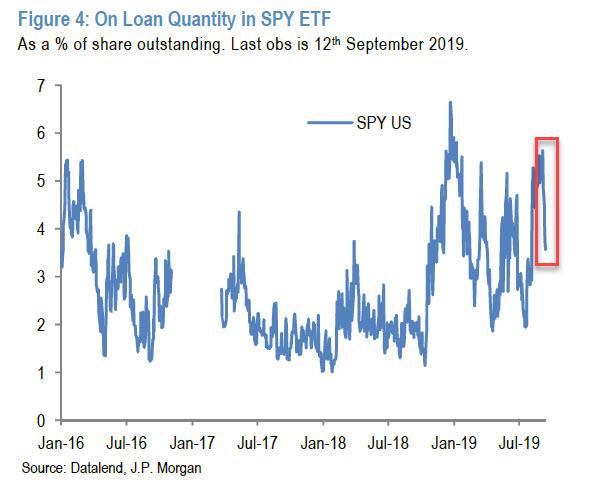

market. In fact, the bank's short interest proxy on SPY ETF (Figure 4) declined

sharply this month from the high levels of last August and stood at a fairly

neutral "middle of the past year" range.

See Fig 4

On Loan quantity in SPY ITF

{kind=link}

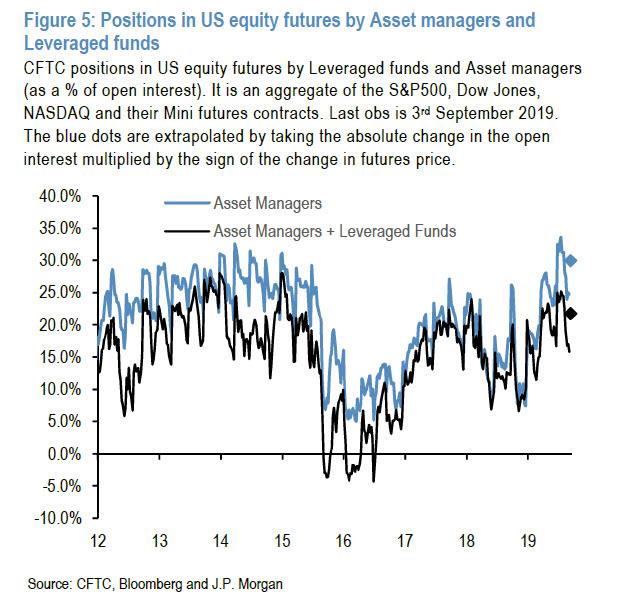

The US equity futures positions by

Leveraged Funds and Asset Managers (Figure 5) have also reversed last month's

decline and stand at the upper end of the past year's range.

See Figure 5

Positions in US equity futures by

asset managers and leveraged funds

{kind=link}

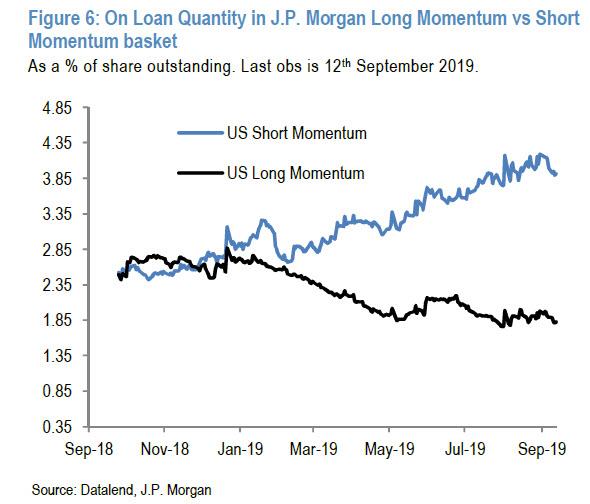

3) Across Long/Short equity style baskets, the biggest gap was

between the short interest of Short Momentum and Long Momentum equity

baskets. This gap remains wide even after this week’s

covering (Figure 6).

See Figure 6

On Loan quantity in JP Morgan Lonf momentum vs. Short Mom

basket

{kind=link}

4) There was little gap in JPM's short interest proxy between

Long Value and Short Value equity baskets before this week’s

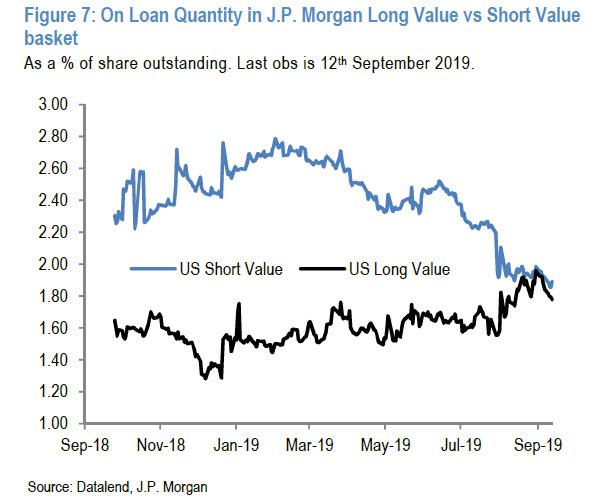

rotation as this gap had closed from last August already (Figure 7).

See Fig 7 This is very

important: I did believe that only middle-class investor give life to this system.

When loans for short term value equity & long term

values are similar: it create perfect balance:

F7. I do believe before that middle size investment is the only key for

prosperity. BUT IF big corp nasty

greed-gluttony prefer Long Term

values(bonds) it breaks the Econ balance. E-Warren said

‘is a matter of putting cups to them (limits). Is it possible to limit the

voracity of big Corp? I don’t thing so..but FDR got it with NEW DEALS when big

corp were weakened by recession, then after they put down FDR. IF the crash

comes before election big corp will buy all values of current system,

unless Potus is putting down. What E-Warren has to do is empower middle classes

& depower Trump & big Corp BEF election

Now see FIG 7:

On Loan quantity in JP Morgan Long

value vs. short value basket

{kind=link}

5) The gap between the bank's short interest proxies for Short

Momentum vs. Long Value equity baskets remains large (3.9% vs. 1.8%)

So with all that in mind, and with the lack of a broader

market shock (and reset) as compared to Feb 2018, Panigirtzoglou notes that -

similar to Kolanovic - he sees more room from a

technical point of view for the gap between Short Momentum and Long Value

equity baskets to close assuming the fundamental triggers of this rotation

continue to be in place.

Said otherwise, despite this month’s shocking sector and

style rotations, JPMorgan is not seeing evidence of a

Quant Quake, with CTA losses so far close to just a third of what we saw in the

Quant Quake of February 2018; meanwhile, daily reporting Equity

Long/Short hedge funds including Quants appear to have been practically

unaffected by this month’s rotation, casting doubt on

the idea that Equity Long/Short hedge funds were at the heart of this

rotation...

….

----

----

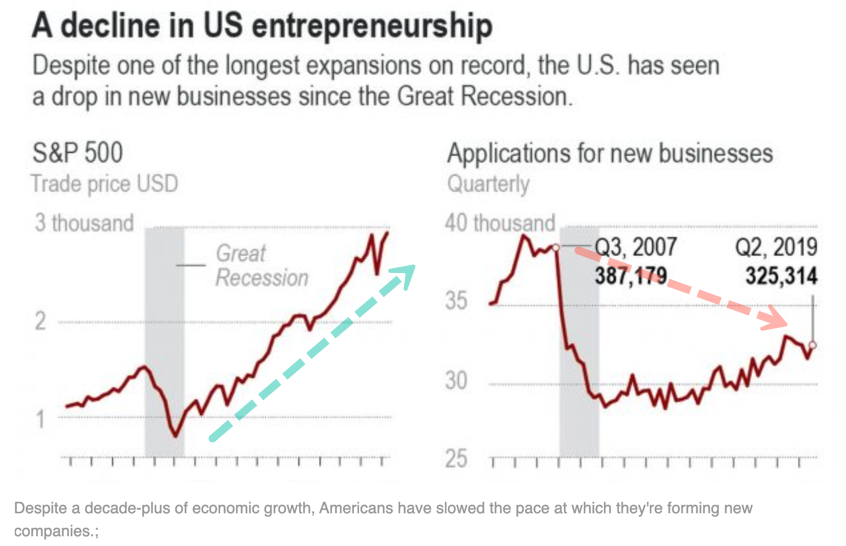

This is

just more bad news for the "greatest

economy ever."

Applications

to start

new businesses that would eventually hire employees

plunged 16% between 2007 and 1H19. The

pace of applications did tick up in 2012 but fell again in 2019 despite

President Trump's constant promotion that his tax cuts, deregulatory actions,

record-high stock market, and a trade war against China would allow

American companies to prosper. Applications dropped

2.6% in 1H19 YoY.

See Chart:

A decline in US Entrepreneurship

{kind=link}

And according to John Dearie, founder of the Center for

American Entrepreneurship, the decline in business

formation "amounts to nothing less than a national emergency."

….

SOURCE: https://www.zerohedge.com/news/2019-09-08/national-emergency-us-business-formation-goes-negative

----

----

Consumers "may not have

the capacity to take on much more debt without running into

trouble."

====

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

POMPEO HAS TO GET OUT FOR LIES OF THIS MAGNITUDE:

Saudi

Aramco describes the Buqyaq facility as "the largest crude oil

stabilization plant in the world."

…..

It is totally irresponsible to put

the world at the risk of WW3. IF Trump is involved in this lie he has to be put

down too. We have to STOP war-mongerism, It is a crime against PEACE since the

agreed rules of Nurenberg Trial. If we do not care for International Laws we

don’t deserve to exist.

----

----

Trump is losing the chances of winning elections 2020 &

now is out of his mind

Questioning “mutual assured destruction,” Charles Kupperman

called nuclear conflict “in large

part a physics problem.” [[ Physics: Idiotic view of nuke-war ]]

----

Any nuclear-war at this time lead to MAD (Mutual

Assured Destruction). It leads to genocide of both contenders RU-China ++ and

US-NATO supporters. To believe that

nuclear war is “winnable” is a sing of

serious psychological disorder. It is a delusional disorder that

mixed schizophrenia + paranoia =

criminal mind. Trump need to be put under psychiatric custody. His sickness is a prove that he is not our President any

longer. The Supreme Court has to demand his immediate resignation,

put him in jail for crime against Peace and put the Nation under temp-regimen in

charge of call immediate elections.

----

----

"[H]e would spin around in his chair, showing me nudes of

whatever target's wife he's looking at. And he's

like: "Bonus!""

====

...not buying the Democrat

narrative.

====

FASCISM?

Our worst fears about automatic license plate readers (ALPR) are much worse than we could have imagined...

Check this: REKOR

{kind=link}

AND LISTEN THIS VIDEO ON REKOR

The article goes on

to say that police had no reason to track Mr. Richard,

but they did so because they could. And that should frighten everyone.

Rekor lets law enforcement know where your friends and

family are, where your doctor's office is, where you worship and where you buy

groceries.

How is that for Orwellian?

….

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

Saudi Aramco

describes the Buqyaq facility as "the largest crude oil stabilization

plant in the world."

====

Netanyahu, feeling the increasing unpopularity of his alliance with the

religious parties, dangles the

carrot of sovereignty extension only possible in the Trump era...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

-Tehran 'Ready for War': US Bases, Carriers

Stationed Around Iran Within Range of Its Missiles - IRGC

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

RT EN ESPAÑOL

- "Estamos listos para una guerra en toda regla": Comandante iraní dice que bases y portaviones de EE.UU. están al alcance de los misiles de Teherán

- La Armada rusa acompaña al catamarán militar de EE.UU. que entró en el mar Negro

- El hijo de Osama bin Laden, abatido por EE.UU.

- Snowden: "Las fotos de desnudos interceptadas eran una especie de moneda informal en la NSA"

- Irán: "Las acusaciones de EE.UU. de que somos culpables del ataque a las refinerías sauditas son incomprensibles y sin sentido"

- Riad asegura que los ataques con drones redujeron a la mitad la producción en las refinerías de Aramco

- NBC: Bolton manifestó a Trump su desacuerdo con aliviar sanciones a Irán un día antes de su salida

- Keiser Report "Hemos normalizado la idea de que los civiles sean el objetivo en una guerra"

----

----

PRESS TV

Resume of Global News described by Iranian observers..

----

----

No hay comentarios:

Publicar un comentario