ND SEP

3 19 SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

"Unprecedented

and extensive."

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

Global Manufacturing massacre

catches up to 'Murica and stocks and bond yields tumble (after markets were seemingly

surprised that Trump and Xi shot tariffs at each other - as they said they

would - over the weekend)

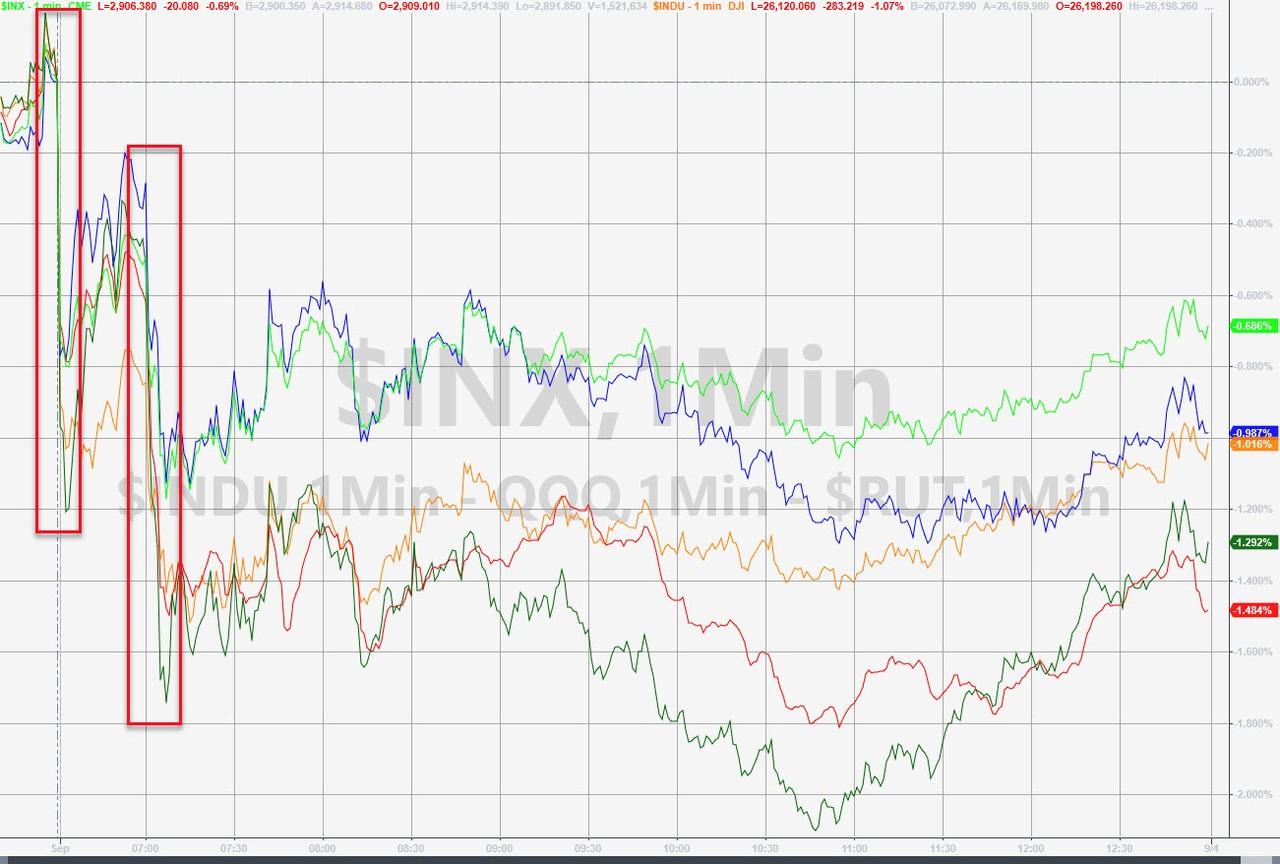

On the

day, all US major indices were red (with Small Caps and Trannies

underperforming)...

See Chart:

{kind=link}

NOTE - the initial

down opening was weakness from trade headlines and the second leg down was the

ISM manufacturing contraction

Stocks

have erased all of last week's "fake" phone call with China spike and

are back in the red from Trump's tariff tantrum

See Chart:

{kind=link}

Treasury

yields tumbled on the day (with the short-end outperforming)...

See Chart:

{kind=link}

30Y

Yields briefly topped 2.00% overnight but rejected that quickly to end the day

notably lower...

See Chart:

{kind=link}

After 6

straight days higher, the DOLLAR INDEX slipped lower today...

See Chart:

{kind=link}

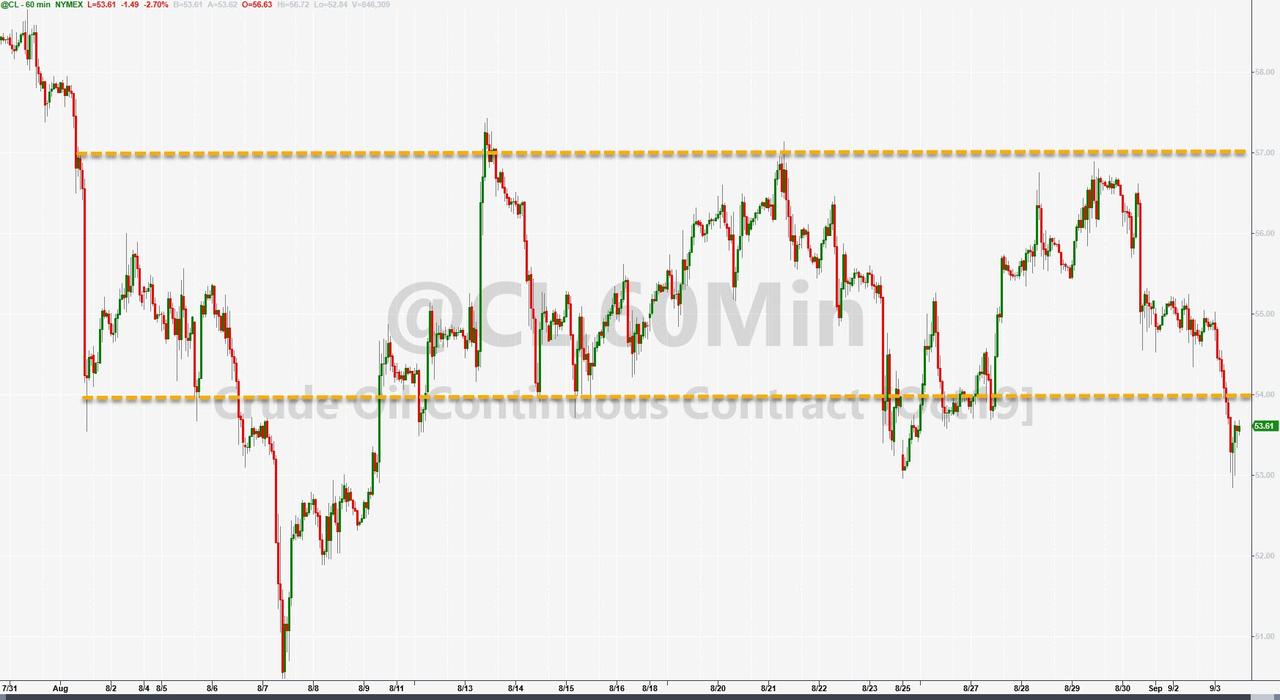

WTI

Crude plunged 3% intraday, back below $54, will it pull back into the recent

range?

See Chart:

{kind=link}

Finally,

we note that it's not like the ISM Manufacturing signal should have been

unexpected as Trucking indicators and Treasury yields have been signaling this

was imminent for weeks...

See Chart:

{kind=link}

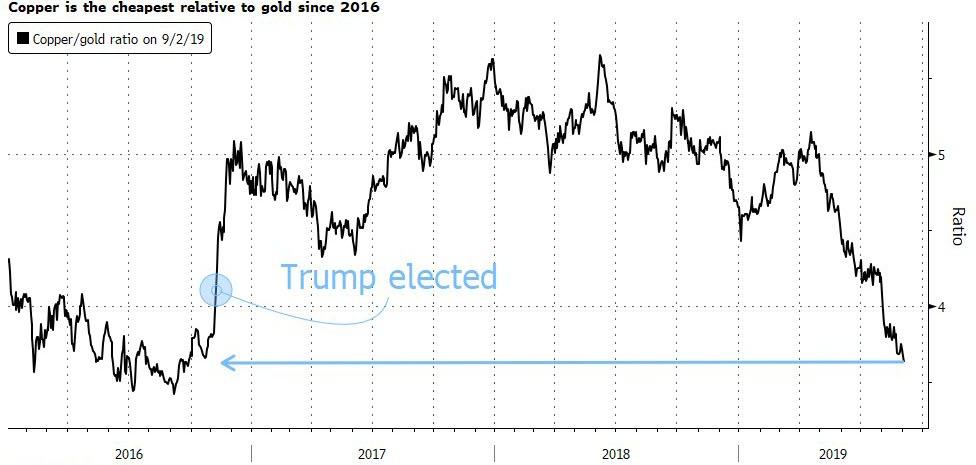

And as

Bloomberg's Eddie van der Walt notes, the copper/gold ratio is extending the year's declines, turning

its back on the Trump-trade era and now focusing lingering economic risks, with

2016 lows coming into play.

See Chart:

{kind=link}

It now takes only 3.6 ounces of

gold to buy a ton of copper, that's down from more than 5 ounces earlier this

year. Changes in the ratio between the two metals are a useful barometer of investor risk appetite,

as the one acts as a haven and the other is an input into industrial

applications.

….

----

----

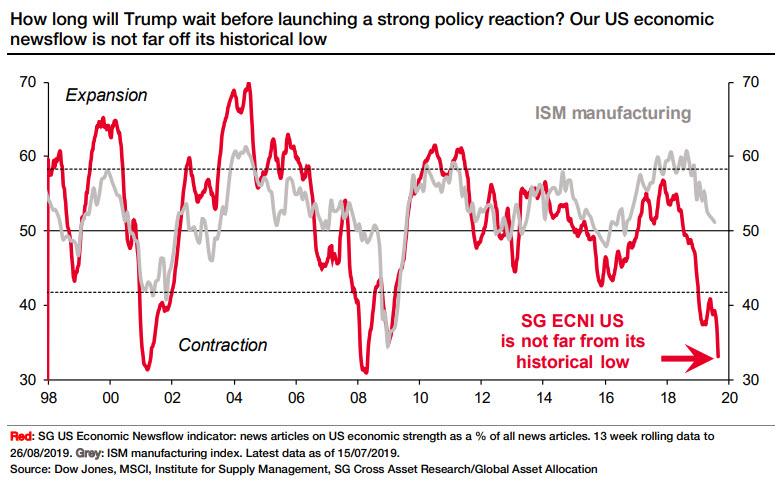

If Trump is serious about his chances

of re-election next year, it seems increasingly likely that, at some

not-too-distant point in the future, he will have to choose between winning the

trade war or lending maximum support to ailing economic growth.

See Chart:

How

long will Trump wait before launching a strong policy reaction?

{kind=link}

….

See more charts at:

----

----

"...it

was a huge mistake for the Federal

Reserve to cut interest rates last month."

====

DYNAMIC & EFFECTS OF NEGATIVE INTEREST RATE.

Where we are? Where we go? What to do?

Hugo Adan. Sep 9/2019

I’m responsible of all that comes into brackets

This is Ponzi finance; it has turned time preference on its head, driving us to borrow from tomorrow to consume today...

Whit

Government spending, much of which is nonproductive,

With the

currency and interest rates manipulated by the State .

LITTLE REMAINS FREE.

[ Key Question: Are we in the path to American Fascism? ]

[ IF so, what to do? ]

[ Or better: What is the best way to organize a

Socialist REV? ]

….

Following on from my previous

article — “The

Pension Fund Apocalypse” - these are just a few of last month’s

stories.

- Danske Bank of Denmark introduces the first negative 10-year fixed-rate mortgage.

- The German Finance Ministry voices disappointment at the lack of demand for 30-year zero-coupon bonds.

- The U.S. and Sweden contemplate issuing 50-year and 100-year bonds.

These are all cause for concern.

In an excessively low–interest rate environment,

financial sleight of hand trumps improvement in total factor productivity every

time.

Are We Nearly There Yet?

Since the great financial

crisis of 2008–9, global economic growth has been sluggish when compared with past recoveries. The slashing of

interest rates spawned a new credit cycle, protecting the overextended

corporations and individuals who, during the previous boom, borrowed too

heavily.

The problem in 2008 was too much debt, and the

predictable knee-jerk regulatory response was to tighten bank capital

requirements.

The actual policy response took different forms from country to country.

Denmark was the first country to adopt negative

interest rates (July 2012), but it was Japan, which had been wrestling with the

fallout from the twin forces of an aging population and a credit bubble since

1989, that became the petri dish

in which financial alchemy was tested. Quantitative and Qualitative Easing

(QQE) followed, allowing the Bank of Japan (BoJ)

to buy corporate bonds and even equities. Negative–interest rate policy

followed in January 2016.

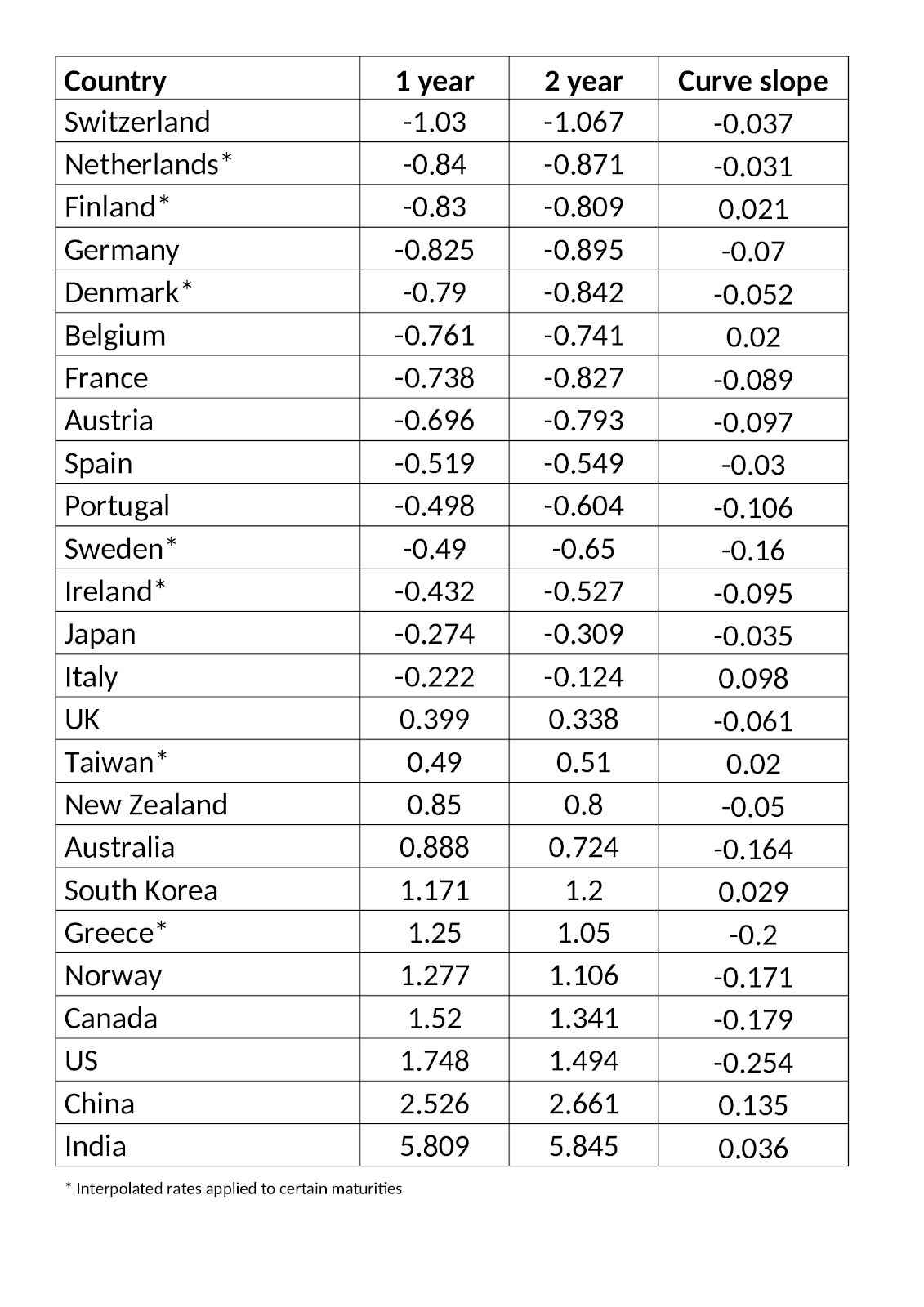

In Switzerland, and the less profligate countries

of the Eurozone, it may be too late to follow the Japanese. As

the table below shows, rates are too negative and expectations, to judge by the

slope of the one-year/two-year yield curve, are that rates will either become

more negative or remain at current levels. If an

inverted yield curve is the harbinger of recession, there may be trouble

ahead.

See Table:

{kind=link}

For finance ministries, zero interest rates on

government bonds are a blessing and a curse. For

the first time in history, they can raise capital for nothing or even receive

an interest payment for their trouble. However, a large

proportion of that gain is due to purchases by their own central banks, which,

in purchasing these bonds at negative yields and holding them to maturity,

incur actual losses that will have to be met by their governments. There

are, of course, other bond buyers, such as pension funds and insurance

companies, that are obligated to purchase their

government’s debt obligations. Central banks do not operate in

isolation.

The Leveraged-Asset Bubble

The effect that an artificially

low interest rate has on an economy is pernicious. Asset markets are supported, and it raises the

point at which they clear, but it also reduces the need for companies to

improve internal efficiency. For

corporates, borrowing becomes preferable to issuing

equity. Firms become more leveraged. The managers of these businesses

have an incentive to improve profitability per share by issuing debt and

retiring equity capital.

For households, lower interest rates encourage

borrowing to buy assets. The

most efficient form of collateralized borrowing available to individuals is

that which is secured against property. With falling interest rates comes more

affordable mortgage financing, boosting property prices. As mortgage-servicing

costs fall, those who are able to borrow get ahead of those who are excluded by

virtue of low income or lack of regular employment. A

rentier class has always existed, but artificially low interest rates swell

their ranks substantially.

And what of the poor, the unemployed, those unable

to clamber onto even the first rung of the property ladder? Populist

politicians will seize the opportunity to pander to the dispossessed voter. They will promise boldly, knowing that, once

elected, they can lean on their notionally independent central banks and be

paid to borrow at no apparent cost. [ Why?.. to

avert rebellion and buying loyalty ]. “Until the cycle of leverage needs

to be unwound, the gravy train will rumble inexorably

onward”.

Gravy Train Still Creates Chaos

The next step in the central bank experiment may be to embrace really negative rates, not just a handful of basis

points but several percentage points. Banks will have to

charge individual customers higher fees for current account services. A bank solvency crisis may ensue as customers withdraw cash

to stuff mattresses. The velocity of circulation of money will trend

even lower.

In a recent publication from

the Federal Reserve Bank of San Francisco — “Negative Interest Rates and

Inflation Expectations in Japan” — the authors observe

that cutting rates at or near the zero bound in Japan has led to lower anchored

inflation expectations. They

advocate that central banks take preemptive action to

avoid the uncertain impact on economic activity and inflation of reducing rates

toward or below the zero bound.

In the long run, the deleterious effect of

negative interest rates turns economic theory on its head. The

concept of time preference dictates that, all other things equal, there has to

be an incentive for homo economicus to defer consumption. Positive interest rates are that incentive, and in an

unhampered market they will always be positive. If, however, interest rates are driven negative by the actions of the

state or its central bank, time preference is inverted and traditional

economic incentives are corrupted. Individuals and corporations are paid to

borrow and consume goods or assets.

The unalloyed power of this corruptive process was

evident during the asset boom of the last decade, long before interest rates

turned negative. What is not seen amid the credit-and-asset bubble

is that, for the economy to grow sustainably,

productive investment is required. Before

there can be capital available for investment, there has to be saving. In

the thrall of negative interest rates there is a clear incentive to borrow and

a disincentive to save. THIS IS PONZI FINANCE; it has turned time preference

on its head, driving us to borrow from tomorrow to

consume today.

Negative interest rates

may be driving us toward the Go-t-ter-damme-rug of the market-based

economy. Government spending, much of

which is nonproductive, is fast becoming the only driver of economic

growth. With the currency and interest rates

manipulated by the state, LITTLE

REMAINS FREE.

….

READ the full article at the source below:

----

----

"Banks,

pensions and other private institutional reservoirs of savings die in a low or no interest rate environment.

How is this helpful to promoting growth?"

====

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

"I started feeling sorry for him when he announced he would

run for President of the United States.You see, I had inside

information..."

====

DARPA declares war on memes...

====

"...the

Federal Reserve I think are much

more aware of what's happening than they're willing to admit..."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

The

conclusion of the recent G7 summit in Biarritz could be a marker of the world order’s future – ending not with

a bang, but with a whimper.

====

They're all panicking as the global economy

implodes...

====

Guyana will be used as an "insurance policy"

if regional conflicts break out in the region.

====

The basic

issue is that the economy is very much interconnected under the laws of

physics, because energy

is required for every activity that is considered part of GDP...

----

….

Ni los precios en un mercado libre, ni el GDP

tienen que ver nada con ”laws of physics” . Decir eso es un disparate. Lo real

es que los precios del oil y el gas están siendo manipulados por grandes

corporaciones vinculadas a 2 bloques: al

aparato militar del US-NATO (Saudis) y al

bloque de empresas ligadas al SOEs

(state owned enterpreises) del Estado Ruso-Chino + aliados (Iran, Ven y otros)

quienes han logrado control de OPEC. Una honesta

relación diplomática entre ambos dos

bloques podría crear un punto medio en el precio, lo que se denominaría “potential-output-price” (otros le denominan a

este precio medio :“optimo Pareto” or “Pareto Optimality Price” (VER:

‘Economics: Marxian versus Neoclasical”). Se trata de medir los

potenciales de producción y sus límites según sean los recursos de capital,

tecnológicos, limites ecológicos y otras variables implicadas en la producción

de este recurso energético. Los neoclásicos del neoliberalism (desde Smith para

adelante) trazaron una curva en el diagrama cartesiano y le llamaron

“production posibility curve”. Pero jamás pudieron

medir nada con precisión dado los monopolios e intereses privados que

distorcionaron data a su capricho. Imposible medir eso, dijeron los Paretianos. Para estos en vez de medir con

más o con menos variables, no soluciona nada. En vez de variables hay que medir

con una constante y le cruzaron la línea en medio a la curva neoclásica para significar el óptimo de producción. Es lo

que se usa hoy para medir precios como los del Petroleo y gas. Se obvio así el problema que hoy existe: el interés

Geo-Politico en el tema. El bloque US-NATO quiere apropiarse del petróleo Ven donde ya

existe inversión RU-China. Este factor o variable debe ser desmontado y olvidado

pues está en juego la soberanía de un Estado-Nacion que tiene toda libertad

para decidir sobre sus recursos. Y sobre todo, porque

el tema Ven, pondría en peligro la paz mundial, el WW3. Lo mismo podría ocurrir

si se usa el tema “petróleo” en el medio oriente. Allí están implicados Siria,

Iran, Israel, además de turcos, saudis y el Uk.

----

----

The premise for China's new strategy

is two-fold: (1) frictions between the US and China have gone far beyond trade,

reducing China's potential gains in a trade deal; and (2) damage from the

higher US tariffs to China's economy has been manageable.

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

FEM: Mujeres

invisibles 5 Vivian Maier David

Torres

===

ALAI ORG

====

RT EN ESPAÑOL

- Trump: "Cuando yo gane, los negocios, los puestos de trabajo y el dinero de China desaparecerán"

- El Parlamento británico se rebela contra Jonhson y le obliga a debatir una prórroga del Brexit

- La economía de Macri: lo que dijo que haría (y no hizo) frente a lo que hizo (y dijo que no haría)

- Hong Kong anuncia la retirada formal del proyecto de ley de extradición que provocó las protestas masivas

- El Pentágono desbloquea casi 4.000 millones de dólares para construir un tramo del muro de Trump

- El retorno de las FARC: cuando las élites sabotean la paz para mantener la impunidad Luis Gonzalo Segura

- Keiser Report Producir más energía al precio de "una extinción prematura" de la humanidad, y otras metas de EE.UU.

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political

crisis: neofascism & internal conflicts that favor WW3

No es

amenaza.. es tendencia al suicidio de los inservibles en ISR

-American Gulag: Brick by Brick, Our Prison

Walls Get More Oppressive by the Day

By John W. Whitehead

By John W. Whitehead

-Is the Fed Preparing to Topple US Dollar? By F. William Engdahl

-I Feel Sorry For President Trump By Paul Craig Roberts

----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

Nick

Pemberton Replacing

Ideology With Class

Andrew

Moss The

Many Faces of Immigration Resistance

Elliot

Sperber Revolution

or Death

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

----

PRESS

TV

Resume of Global News described

by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario