JUN

20 ND SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

$10.4

trillion in fiscal stimulus and $7.9tn in monetary stimulus - for a grand total

of 20.8% of global GDP, injected mostly in just the past 3 months!

On Friday, we relayed the latest

observations from BofA chief investment officer, Michael Hartnett who concluded that there is just one bull market to short - namely credit -

"and the Fed won't let you" by which he means all central

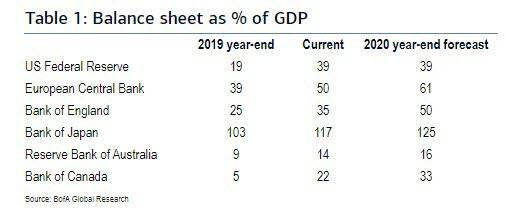

banks. As the following table shows, the balance

sheet of the G-6 central banks has exploded, with the Fed's total asset

expected to double in 2020 amid an avalanche of money printing.

SEE TABLE:

{kind=link}

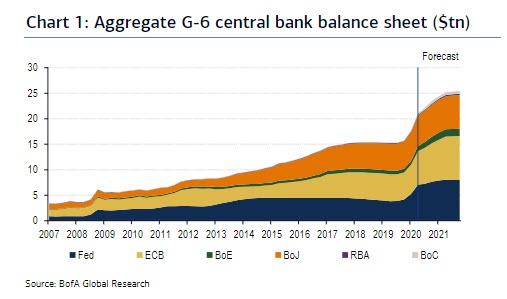

And

visually:

SEE CHART:

{kind=link}

Of course, it's not just central

banks: as Hartnett also explained there is also the

2020 fiscal bazooka which has a way to go, with the massive fiscal stimulus

unleashed post-covid taking 3 forms in 2020: spending, credit guarantees, loans

& equity.

Hartnett also noted that according

to BIS data, US & Australia lead spending (>10%

GDP), Europe is using aggressive credit guarantees (e.g. Italy 32% GDP), while

Japan/Korea are stimulating via government loans/equity injections.

But the most staggering fact was

when one puts it all together.

According to BofA calculations, in

addition to the record 134 rate cuts YTD, the amount of total global stimulus, both fiscal

and monetary, is now a "staggering" $18.4 trillion in 2020 consisting

of $10.4 trillion in fiscal stimulus and $7.9tn in monetary stimulus - for a

grand total of 20.8% of global GDP, injected mostly in just the past 3 months!

And to think none of this would

have been possible if officials had not collectively decided

to shutdown the global economy in response to the ‘coronavirus pandemic’.

….

----

----

U.S.’ energy dominance agenda is dead as the country’s shale

industry is looking at a steep production decline...

·

U.S.’ energy dominance agenda is dead as the

country’s shale industry is looking at a steep production decline.

·

The U.S. tight oil or shale rig count has fallen

69% this year from 539 in mid-March to 165 last week.

·

U.S. oil import dependence is set to grow in

the next couple of years.

U.S. energy dominance is over. Output is probably going to drop by 50%

over the next year and nothing can be done about it. It has nothing to do

with the lack of shale profitability or other silly memes cited by people who

don’t understand energy.

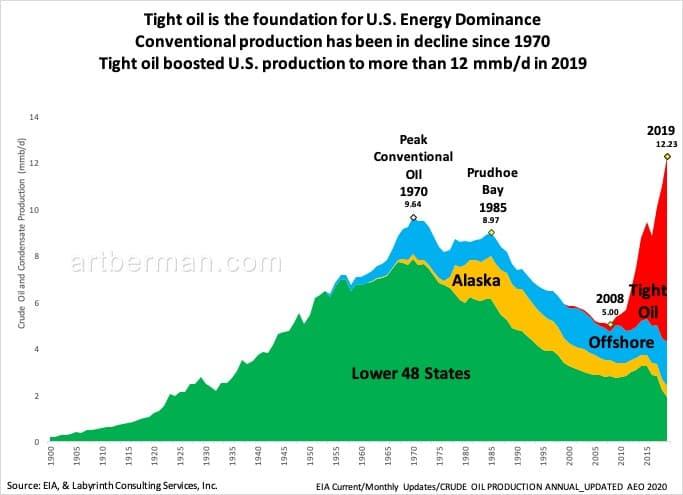

Conventional production has been declining since 1970. It fell from

almost 10 mmb/d in 1970 to 5 mmb/d in 2008.

Figure 1. Tight oil is the foundation for U.S.

Energy Dominance.

SEE CHART:

{kind=link}

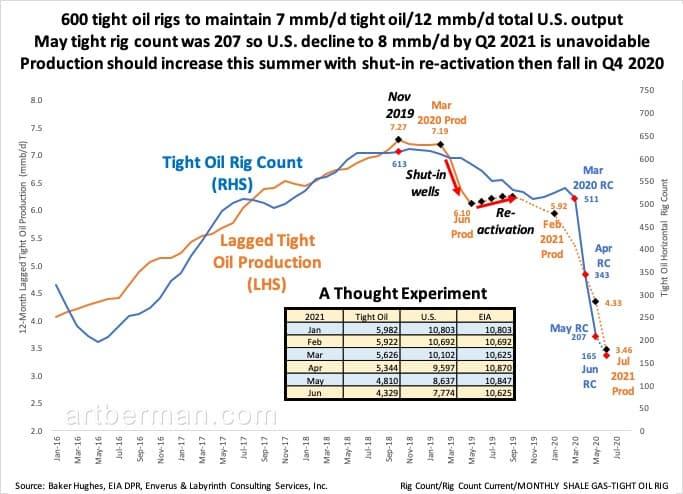

The horizontal rig count is now 165

so it is unavoidable that production will fall. The considerable lags and leads

mean that production decline cannot be expected to reverse until well into 2021

assuming that it starts to increase immediately. That

won’t happen because of constrained budgets and low oil prices.

Figure 2. 600 tight oil rigs to maintain 7

mmb/d tight oil/12 mmb/d total U.S. output.

{kind=link}

Killer Decline Rates Require Lots of Rigs

Lower U.S. crude and condensate production is unavoidable with rig counts

where they are today. That is because tight oil decline rates are really high.

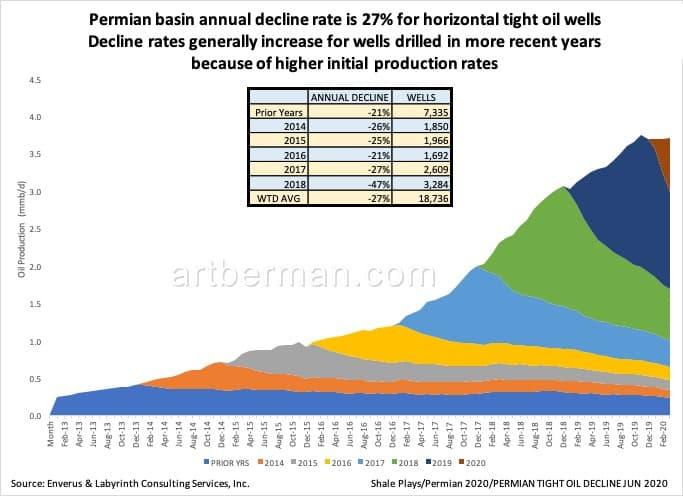

Figure 3 shows Permian basin shale play decline rates by year of first

production. The average of all years is 27% per year. More recently drilled wells decline at

higher rates because of better drilling and completion technology. The problem

is that the wells don’t have greater reserves—they just produce the reserves

faster. That means higher decline rates.

Figure 3. Permian basin annual decline rate is

27% for horizontal tight oil wells

SEE CHART:

{kind=link}

The current June rig count of 165 will continue to fall for several

months because of low oil price & capital budgets.

Figure 4. It took 2.5 years for tight oil rig

count to increase from 193 in May 2016 to 618 in November 2018.

SEE CHART:

{kind=link}

June rig count of 165 will fall for several

months based on oil price & capital budgets.

Source: Baker Hughes, IEA DPR, Enverus and

Labyrinth Consulting Services, Inc.

Rigs Don’t Produce Oil,

Wells Do

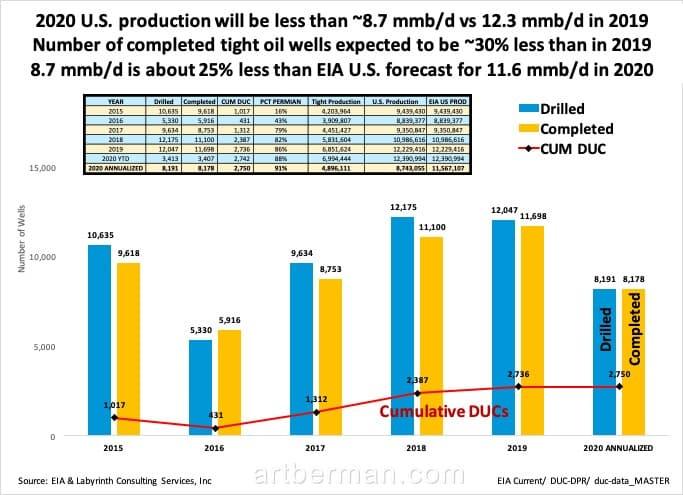

This approach suggests that 2020 tight oil production will be about 30%

less than in 2019 (Figure 4). Since tight oil represented 56% of total U.S.

output in 2019, we may then estimate that U.S. production will average about

8.7 mmb/d in 2020.

Figure 5. 2020 U.S. production will be less

than ~8.7 mmb/d vs 12.3 mmb/d in 2019.

SEE CHART:

{kind=link}

Energy Dominance and Green Paint

Much lower U.S. oil production is bad for Trump’s Energy Dominance anthem

and its corollary that the U.S. is energy independent. It’s even worse for oil

prices and the U.S. balance of payments once demand recovers. We will have to

import even more oil than we do today and it will cost more.

But a new phase of economic reality and oil pricing is unfolding and no

one knows where it will lead. Lower demand may mean that reduced U.S. oil

output is appropriate. The only thing that seems certain is that the U.S. will

not be the oil super power it was before 2020.

….

----

----

"I’m sharing this trade ... so you

can hail me as the obliterating moron that infamously shorted the greatest

rallyfloating weightlessly ever higher above the worst economic and

corporate crisis imaginable..."

I hate shorting. The

risk-reward relationship is out of whack. It feels crappy. I lost a ton of

money shorting the worst highfliers a little too early in late 1999.

I’m sharing this trade so that everyone gets

to ridicule me and hail me as a moron and have fun at my expense in the

comments for weeks and months every time the market goes up. And I do

not recommend shorting this market; it’s nuts. But here’s why I did.

The stock market had just gone through what

was termed the “greatest 50-day rally in history.”

There are now 29.2

million people on state and federal unemployment insurance. There are

many more who’ve lost their work who are either ineligible for unemployment

insurance or whose state hasn’t processed the claim yet, and when they’re all

added up, they amount to over 20% of the labor force. This is horrible.

But stocks just kept surging even as millions

of people lost their jobs each week. The more gut-wrenching the

unemployment-insurance data, the more stocks soared.

Then there is the desperate plight many

companies find themselves in, and not just the airlines – Delta warned of a

host of existential issues including that revenues

collapsed by 90% in the second quarter – or cruise lines –

Carnival just reported a revenue collapse of 85% in Q2, generating a $4.4

billion loss, and it is selling some of its ships to shed the expense of

keeping them.

These companies are in sheer survival

mode. This crisis hit manufacturers

whose plants were shut down. It hit retailers and

sent a number of them into bankruptcy court. It crushed clinics and

hospitals that specialize in elective procedures. It shut down dental offices.

It sent two rental car companies into bankruptcy court.

The situation has gotten so silly in the stock

market that the shares of bankrupt Hertz [HTZ]

– which will likely become worthless

in the restructuring as creditors will end up getting the company –

were skyrocketing from something like $0.40 a share on May 26 to $6.28

intraday on June 8, which may well go down in history as the craziest moment of

the crazy rally.

Even during the crazy dotcom bubble in late

1999 and early 2000, the day-trader frenzy hadn’t reached these levels. But

back in 1999, the economy was strong. Now this is the worst economy of my lifetime.

These are the times of record Federal Reserve

money printing. Between March 11 and June 17, the Fed printed $2.8

trillion and threw them at the markets – frontloading the whole thing by

printing $2.3 trillion in the first month.

But over the past six weeks something new was

developing: While the Fed was talking about all the asset purchase programs it

would establish via its new alphabet-soup of SPVs, it actually curtailed the

overall level of its purchases.

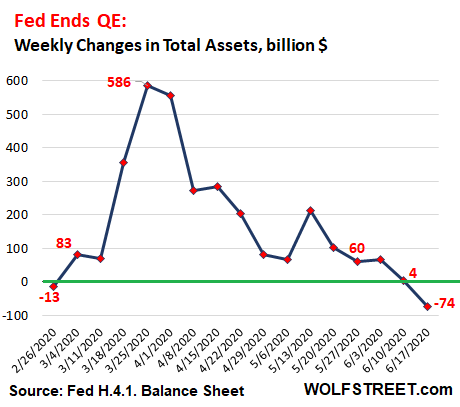

Then in the week ended June 10, the Fed’s

total assets of $7.1 trillion increased by less than $4 billion. And in the

week ended June 17, its total assets actually fell by $74 billion (you

can read my

analysis of the Fed’s balance sheet here). This chart of the

week-over-week change in total assets shows how the Fed frontloaded its QE in

March and April, and how it then systematically backed off.

SEE CHART:

FED ENDS QE:

{kind=link}

And there is another big shift in how the Fed

is now approaching the crisis. It’s shifting its

lending and asset purchases away from propping up financial markets toward

propping up consumption by states and businesses, and ultimately

spending by workers/consumers via its municipal lending facility, its PPP loan

facility, and its main-street lending facility. These funds are finally flowing

into consumption and not asset prices.

So the superpower that created $2.8 trillion

and threw it at this market, and that everyone was riding along with, has

stopped propping up asset prices.

And now the market, immensely bloated and

overweight after its greatest 50-day rally ever, has to stand on its own feet, during the worst

economy in my lifetime, amid some of the worst corporate earnings approaching

the light of the day, while over 30 million people lost their jobs. It’s a terrible gut-wrenching scenario all around.

And so I stuck my neck out, and I’m sharing

this trade for your future entertainment when it goes awry, and you get to have fun at my expense and hail me as the

obliterating moron that infamously shorted the greatest stock market rally of

all times as it was floating weightlessly ever higher above the worst economic

and corporate crisis imaginable.

….

SOURCE:

https://www.zerohedge.com/markets/i-who-hates-shorting-just-shorted-entire-stock-market-heres-why

----

----

"The April/May strategy of owning

anything is unlikely to perform as well going forward."

In the latest weekly JPMorgan View report by

John Normand, the strategist answers the four most common questions that

have arisen after such strong market performance:

1. how much

longer will the growth boom last;

2.

how much of that recovery is already discounted in

asset prices;

3. which

wildcards, both negative and positive, are most material in coming months; and

4.

why not just own anything when growth is improving,

policy hyper-stimulative and cash holdings extraordinary.

Before we get to the answers, a quick rundown

of where the markets are today: [ Get this info by opening the SOURCE

AT HE END OF THIS ART ]

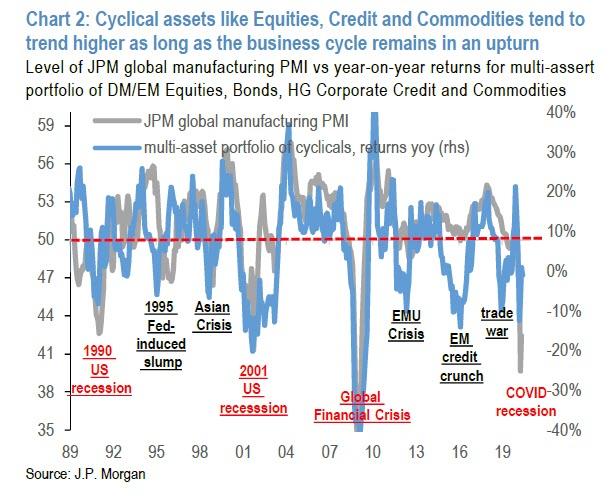

1. How much longer will

this "growth boom" last? According to Normand, what will matter for

most asset prices over Q3 and possibly Q4 is "the near-term momentum

rather than the medium-term malaise." This judgement reflects a simple

observation that most cyclical assets tend to rise in price/tighten in spread

as long as the global business cycle is in an upturn which for now it is due to

the tremendous drop in March and April.

SEE CHART:

{kind=link}

2. Is the recovery priced

in, or "what is the completeness of the growth/profits recovery." That is why the bank has judged valuations

from a few perspectives: (1) a long-term

framework based on generally mean-reverting measures like forward P/Es for

Equities, spreads for Credit and real (inflation-adjusted) levels of exchange

rates, commodity pries and bond yields for the rest of the FICC universe; (2) a short-to-medium term framework that scores

markets on the degree of retracements they tend to experience in the last month

of recession and the first few quarters of an expansion.

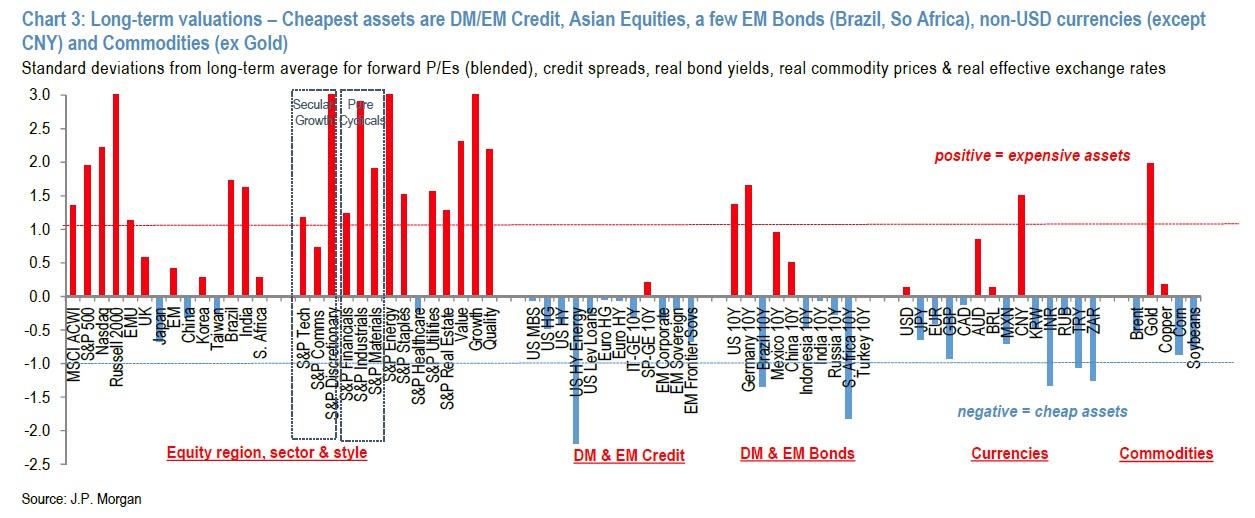

Long-term measures, where

valuations for each asset class, sector or security are expressed in standard

deviations from their multi-decade averages (chart 3), suggest that the

cheapest markets are DM/EM Credit followed by Asian Equities; a few EM Bonds

(Brazil, South Africa); non-USD currencies (ex CNY); and some Commodities (Oil,

Agriculture).

SEE CHART

{kind=link}

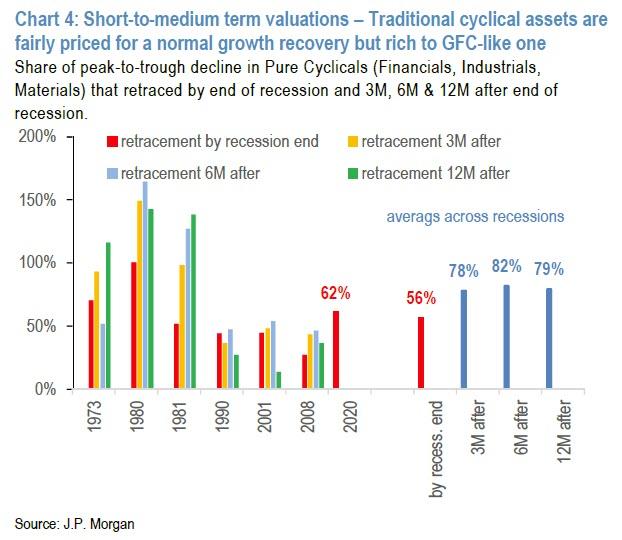

Short-to-medium term measures, which compare

recent market retracements to those that typically occur at business cycle

turning points, suggest fair value if the global economy recovers lost output

extremely quickly, but broad expensiveness if the malaise sets in.

So if the emerging recovery mirrors all

previous recessions from 1970 to 2001, then markets are fairly valued. But

if the recovery proves more anemic like the post-Global Financial Crisis years

were due to impaired balance sheets, then markets have overshot. JPM thinks the GFC is the proper template and are therefore

concerned about valuations, which is why its portfolio strategy is conservative.

SEE CHART:

{kind=link}

The wildcards, both positive and negative. This potential

valuation problem makes more relevant the role of wildcards. Perhaps because

market momentum has been so strong in recent months, the sources of

downside risk in H2 seem more abundant than the sources of upside.

The most material ones to JPM are COVID

infections because these are indeed rising in a few US states...

SEE CHART:

{kind=link}

the Democratic

sweep because swing state polls favor both Biden versus Trump and Democrats

versus Republicans in vulnerable Republican Sentate seats...

SEE CHART:

Voting intentions favor Dems but only by a thin margin

{kind=link}

and broader US sanctions on China will affect US

public and both sides of the US political spectrum that hold an overwhelming negative impression of

China (66% of Americans have an unfavorable view of China, according to an

April Pew Research Center poll). The bank then admits that it isn't properly

hedged against a second wave that triggers lockdowns, other than through a

preference for the Tech and Healthcare sectors, because there is sufficient

hospital capacity to accommodate the inevitable rise in infections as mobility

increases.

This brings us to JPM's punchline: does any of

the above actually matter at a time when there has been an unprecedented

liquidity injection in the markets? The answer is that while the rising tide

has indeed lifted all boats, it can only do so much:

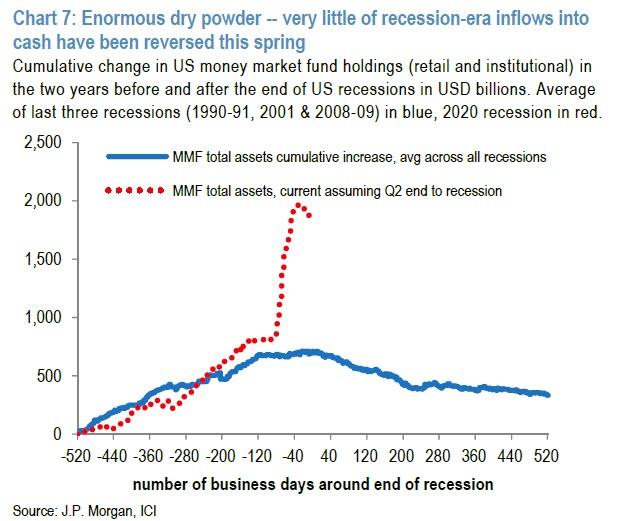

The case for selectivity: According to

Normand, "liquidity cannot paper over specific weaknesses

indefinitely." When the business cycle is turning

higher, policy hyper-stimulative and downside risks manageable, the obvious

investment strategy might be to own anything but cash, holdings of which remain

extraordinarily high.

SEE CHART:

{kind=link}

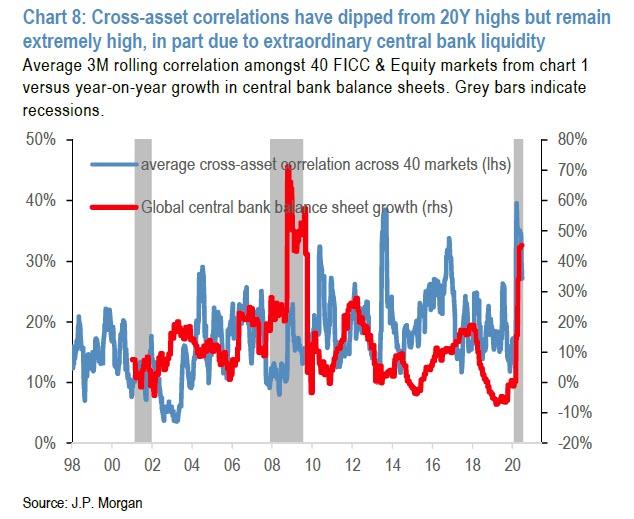

Massive central bank asset purchases can also

boost correlations due to a combination of scarcity created by central bank

asset purchases and rising growth expectations from central bank easing.

SEE CHART:

https://www.zerohedge.com/s3/files/inline-images/cross%20asset%20correaltion%20jpm.jpg?itok=r-Ssbe-1

{kind=link}

However, typically such high correlations

mean-revert to their long-term averages within a few months, in part because

the pace of QE slows and in turn allows country, sector and company-specific

factors to reassert themselves. H2 should bring

this sort of differentiation, which is why the April/May strategy of owning

anything is unlikely to perform as well going forward.That would mean these

choices:

But typically these high correlations

mean-revert to their long-term averages within a few months, in part because

the pace of QE slows and in turn allows country, sector and company-specific

factors to reassert themselves. H2 should bring this

sort of differentiation, which is why as JPM concludes, "the April/May

strategy of owning anything is unlikely to perform as well going forward."

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Younger voters worry most about another civil war...

====

Censorship :

If you’re looking ahead and the future looks bright, that might be because you’re

seeing the country on fire...

====

The Furer don’t accept sacking,, only total obedience &

quiet fear.. unless all resign

"I

will be leaving the U.S. Attorney’s Office for the Southern District of New

York, effective immediately."

….

Si los demás tienen alma de lacayos, no van a renunciar: footman enjoy opres

====

Smart money

is getting the hell out of the city.

====

One death is nothing compared to the hundred killed under a

fascist regimen

CHAZ, CHOP,

or whatever you want to call it

has just

suffered its first fatality...

====

The Weimar regime didn’t

print too much fake money to get similar results: 20% GDP

$10.4

trillion in fiscal stimulus and $7.9tn in monetary stimulus - for a grand total

of 20.8% of global GDP, injected mostly in just the past 3 months!

====

Los ricos

saquean la Nación en complicidad con el Gbno y nunca les ponen handcuffs.

Even though the note was clearly

identified as pretend money, shop staff felt obliged to call the police...

====

Irony time:

Put there all members of the executive + Senate &

warmongers of the House then sink

"..gently used..."

….

YES.. gently sink it or gently blow it up.. then accuse the RU+ China communist IF not

enough reason to initiate WW3, put their families in this “vacation trip”.

It’s my favor to Penta-Nato clowns who still didn’t got a plan to use

Ch-Ind war. Mr POTUS is already fostering WW3,

you should not disappoint our Furer.

He can dismiss all of you ‘immediately’ as happen with US Attorney Berman. IF you want better suggestion ask Bolton, he

know better the dances in this circus

====

"...worried the

rally could become a'super spreader'

event and recommended it be postponed"

====

'The government

is likely to succeed in its case against the former National Security Adviser.'

====

Yes, we will see economic numbers go up and down over the coming

months, but a return to “the good

times” is not in the cards...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

Beijing is

turning a blind eye...

====

Full-blown 'intercept war' developingas

for first time in recent memory the US has flown bombers this close to

Russia's far eastern territory...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

- 'Improper

Motives' Behind Berman's Firing, AG Barr 'Must Be Held Accountable', Speaker

Pelosi Says

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

RT EN ESPAÑOL

Bolton dice: UK coopera con US para congelar depósitos

de oro de Ven en Banco UK https://actualidad.rt.com/actualidad/357334-bolton-reino-unido-encantado-cooperar-eeuu-congelar-oro-venezuela

Tres mueren un apuñalamiento masivo en un parque del

Reino Unido https://actualidad.rt.com/actualidad/357316-tres-muertos-heridos-apunalamiento-protetas-reino-unido

Teherán envía buque con alimentos a Caracas e inaugura

1er supermercado iraní en Ven https://actualidad.rt.com/actualidad/357325-teheran-envia-buque-alimentos-venezuela-inaugurar-supermercado

temblor de mag 4,2 sacude Oklahoma poco después de

un mitin de Trump en Tulsa https://actualidad.rt.com/actualidad/357345-sismo-magnitud-sacudir-oklahoma-mitin-trump

Presidente cubano recibe a médicos que combatieron

el coronavirus en Italia https://actualidad.rt.com/video/357335-presidente-cuba-recibir-medicos-combatir-coronavirus-italia

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

- The Global Reset – Unplugged By Peter Koenig

- Get Rid of the Presidency By Matthew Stevenson

----

----

CROSS TALK https://www.rt.com/shows/crosstalk/

In this

episode of the Keiser Report, Max and Stacy discuss the congressional

testimony of US Federal Reserve Chairman Jerome Powell, who is warning about

the risk to the recovery he has printed. They look at the explosion of Zombie

companies on the US stock exchange and the largest pension fund leveraging up

to meet their 7 percent returns. In the second half, Max talks to bitcoiner

Stephen Cole about inflation and war. They also discuss the bitcoin vs gold

debate.

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

- Juneteenth: A

Celebration of Black Liberation & Day to Remember “Horrific System That Was

Slavery”

====

====

No hay comentarios:

Publicar un comentario