JUN 19 ND SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

WHO Director-General Tedros

acknowledged people worldwide wereweary

of lockdown measures...

….

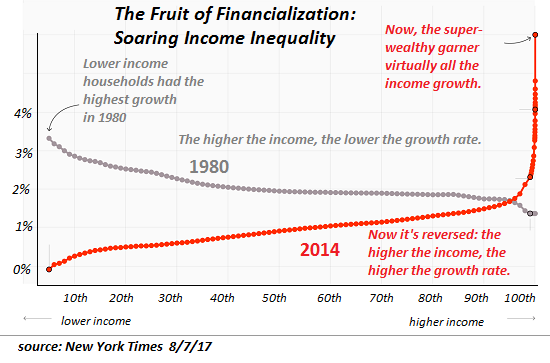

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

Generating goods, services and jobs is for chumps. Get over it. The real money is made

bellying up to the Fed's free money for financiers spigot...

SEE CHART:

{kind=link}

====

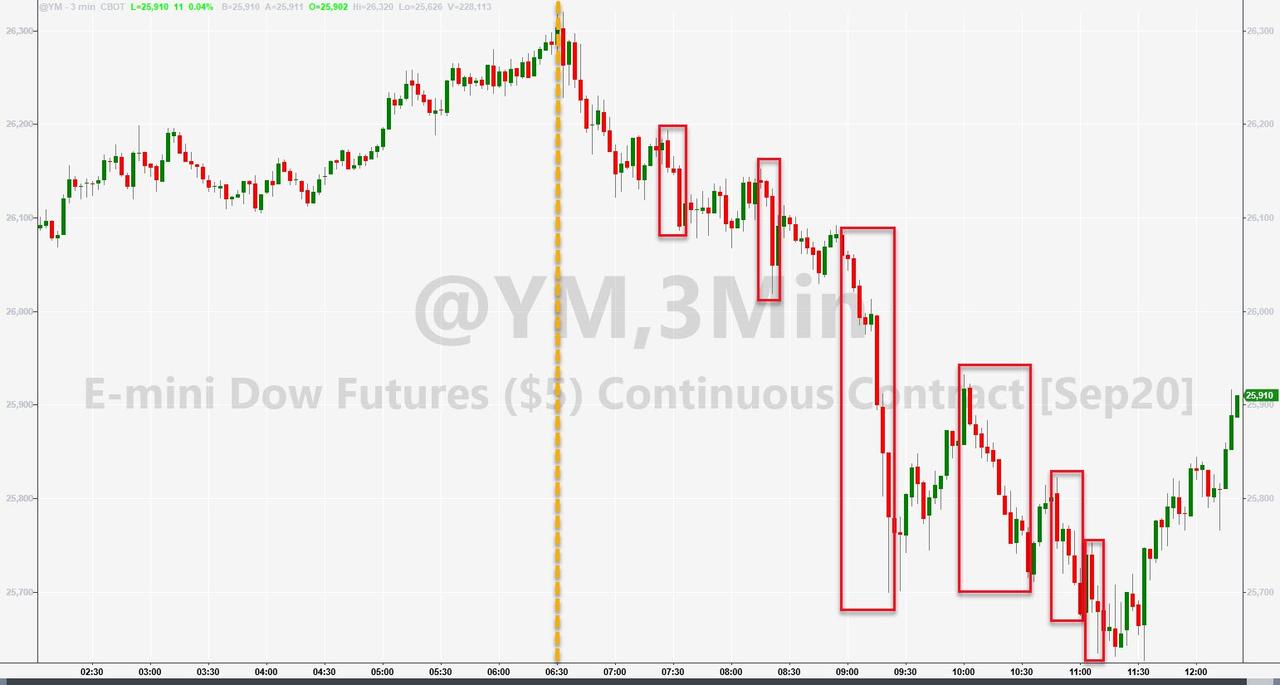

Well that was a week of

worrisome headlines (from World War 3 to global COVID reawakenings),

awe-inspiring US macro-economic beats (which lose all context in relation to

the collapse) as earnings outlooks remain just "off the lows", and a

stock market that refuses to go down despite bonds, the dollar, and commodities

all signaling anything but strong growth ahead...

Given

the mean-reverting nature of the US macro surprise index (3 standard deviations

above the mean), this could be as good as it gets...

SEE Chart:

US

Macro Surprise Index

{kind=link}

Leaving

the gap between macro and micro at its greatest ever...

See Chart:

{kind=link}

All

hell broke loose this morning as the June S&P futures contract expired...

See Chart:

{kind=link}

The market started lower the

moment the June contract expired, but there were a

number of triggering headlines for the legs lower...

- 1055ET *FLORIDA COVID CASES +4.4% VS. PREVIOUS 7-DAY AVG. 3.2%

- 1125ET *ARIZONA REPORTS A RECORD 3,246 NEW VIRUS CASES: ABC-15

- 1215ET *APPLE TO CLOSE SOME U.S. STORES AGAIN DUE TO COVID-19 SPIKES

- 1302ET *Fed's Quarles Says Market Reaction to Covid-19 Is Not Over

- 1345ET *CRUISE LINES SUSPEND TRIPS OUT OF US PORTS TIL SEPT. 15: CNBC

- 1405ET *CALIFORNIA RECORDS LARGEST SINGLE-DAY INCREASE OF COVID CASES

See Chart:

{kind=link}

On the week, all the US majors

were higher with Nasdaq leading and The Dow lagging.

On the

day only Nasdaq managed to close green...

See Chart:

{kind=link}

With the late-day panic..

Nasdaq

is up 6 days in a row and up 17 of the last 20 days..

See Chart:

{kind=link}

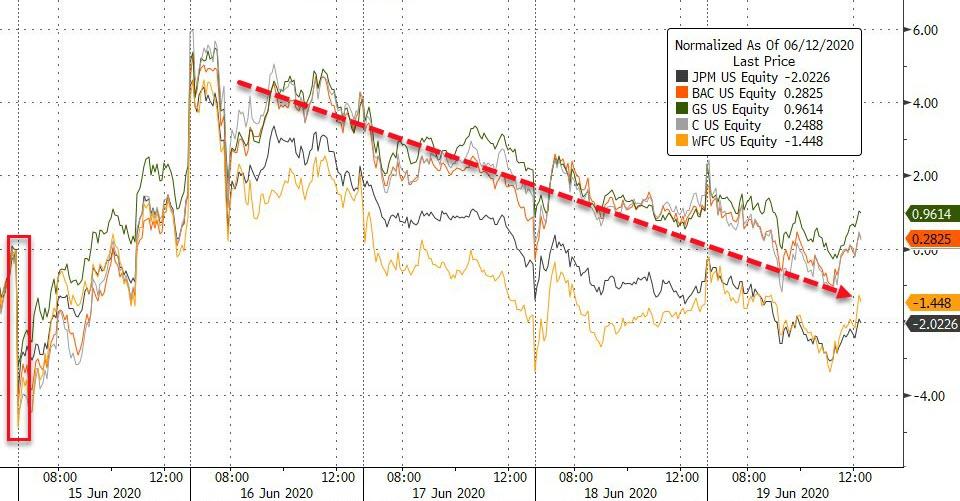

Banks

started the weak with a panic-bid off opening weakness but that faded as the

week proigressed and yields slid...

See Chart:

{kind=link}

Treasury

yields fell today to end the week unch...

See Chart:

{kind=link}

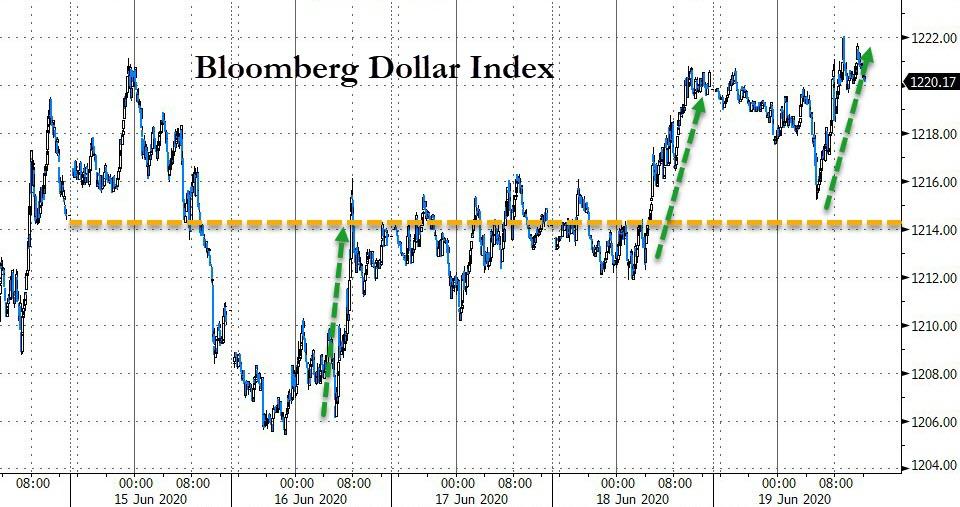

The

B-dollar Index ended the week higher (up

6 of the last 7 days and 2nd up-week in a row)

See Chart:

{kind=link}

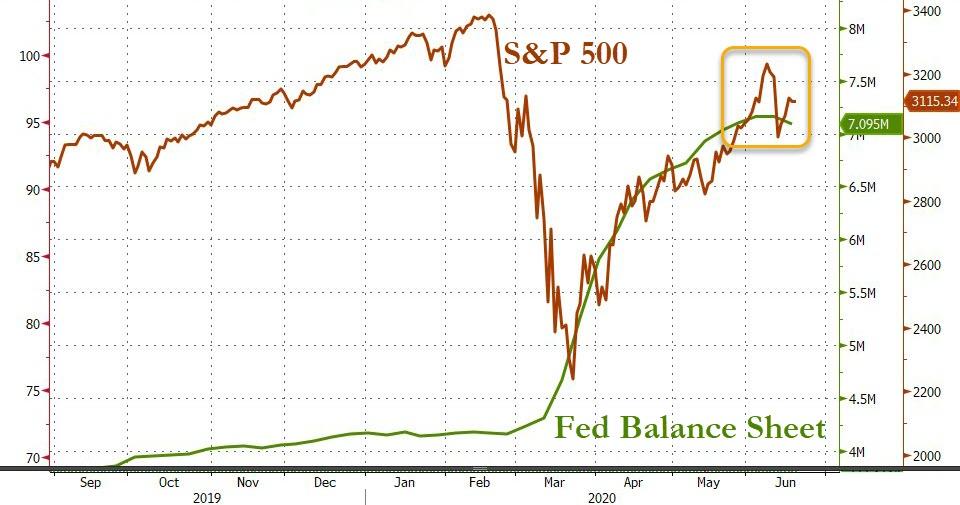

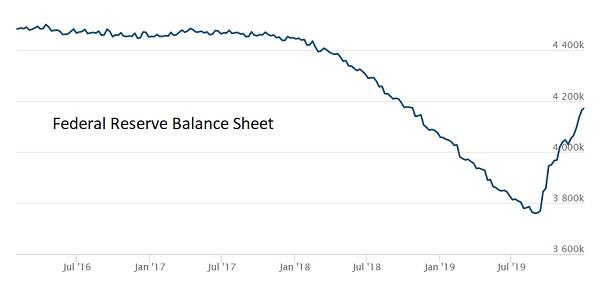

And

finally, don't forget, The Fed's balance sheet shrank the most since 2009 this

week...

See Chart:

{kind=link}

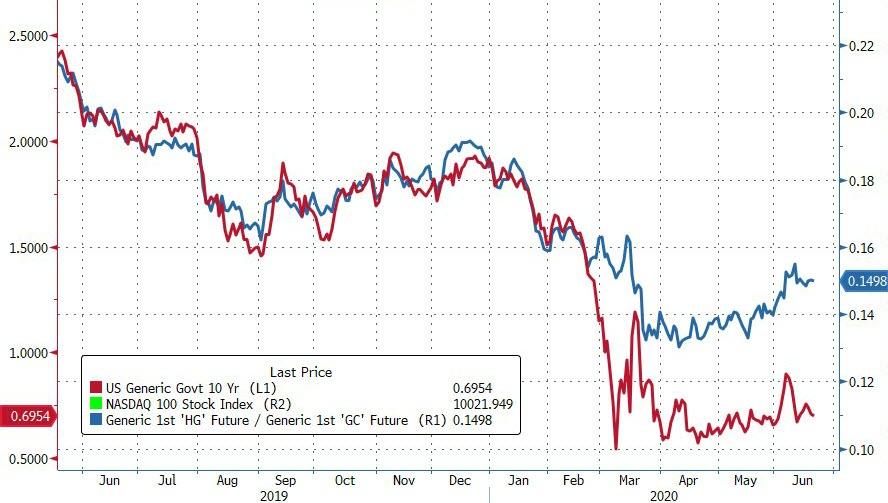

Either

TSY yields are dramatically too low or Dr.Copper is way over his recovery skis

relative to gold...

See Chart:

{kind=link}

Is

volatility about to be resurrected?

….

----

----

The Fed has spent just $173bn out of

its potential $495bn in firepower (and it can always add more).

Is it time to go short?

With the Fed's balance sheet posting

its biggest weekly drop in 11 years, and hitting a plateau of sorts (at least

until the next major QE push)...

SEE CHART

{kind=link}

Hartnett also warns that Fed rhetoric has been bigger than

wallet thus far, which means Powell can easily crush shorts. Here's why - the Fed's facilities are operating at just a

fraction of potential, and as Table 1 below shows, the Fed has spent just $173bn out of its potential $495bn in firepower

(and it can always add more).

SEE TABLE

{kind=link}

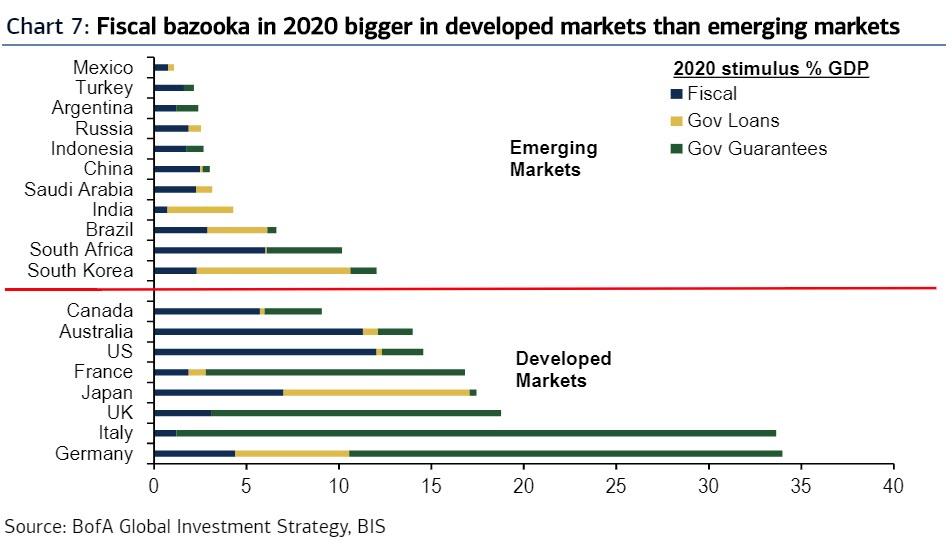

It's not just the Fed: there is also the 2020 fiscal bazooka

which has a way to go.

As Hartnett adds, the fiscal stimulus is taking 3 forms in

2020… spending, credit

guarantees, loans & equity. BIS data

shows US & Australia lead

spending (>10% GDP), Europe is using aggressive credit

guarantees (e.g. Italy 32% GDP), while Japan/Korea are stimulating via

government loans/equity injections.

SEE CHART:

{kind=link}

And while Hartnett echoes what we said last month, that it is

"notable how Emerging Markets lagging in terms of fiscal ability to

address pandemic/recession", recall that last night we reported that China

has now vowed to inject global credit amounting

to 30% of GDP in the economy this year.

So does that mean don't short under

any conditions? Not exactly. As Hartnett summarizes, the tactical risk remains to the upside:

positioning,

policy, credit markets all still point to potential for or above 30Y TSY above 2%, IG CDX 60, SPX 3250, while

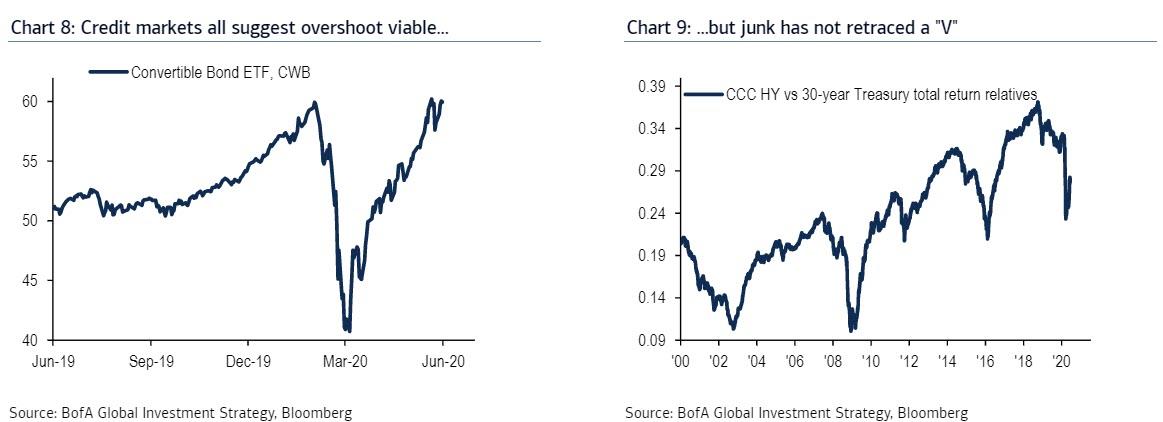

credit markets are still too strong (see LQD, PFF, CWB)...

SEE CHARTS:

{kind=link}

... to short stocks, even if

like stocks, junk has only retraced partially versus quality bonds (see

relative performance of CCC HY bonds vs 30-year Treasury - Chart 9); summer risk remains to upside driven by central bank

repression of credit spreads (positive for "growth"…see

world's best performing market, Chinese Nasdaq (ChiNext), threatening to breakout to new highs - Chart 10), or via big

RoW macro surprise to upside via fiscal stimulus (see soaring Baltic Freight

Index); barbell of credit/tech and EU/US small cap value & banks.

SEE CHART

{kind=link}

But the structural risk is to the downside: Fall

2020 risks will be 1. Fear of double-dip recession & default risk, 2.

Debasement of US dollar & disorderly bond markets, 3. Politics threatening

2021 EPS;

His parting advice for a tipping point back into shorts: watch the

yield curve: a failure of the curve to steepen

>80bps in June/July would signal "peak policy stimulus" and

reinvigorate shorts.

….

SOURCE: https://www.zerohedge.com/markets/bofa-there-just-one-bull-market-short-and-fed-wont-let-you

----

----

Over the last several decades, the Federal Reserve and the US

government havealmost exclusively directed their policies toward “stimulating”

spending. Artificially low interest rates incentivize borrowing

and discourage savings.

Saving is integral to a sound economy. But the government

and central bank policies today undermine savings – and thus the overall

economy. Instead of a robust economic system, we end up with a series of

bubbles. We get the illusion of wealth without the actual wealth.

====

...a flock of black swans still on approach vector has

investment implications. Put simply, how can anyone be buying growth

stocks and ignoring gold in this world?

Why bring up these past examples of multi-part crises? Because the

universe seems to like them. And we seem to be entering another one.

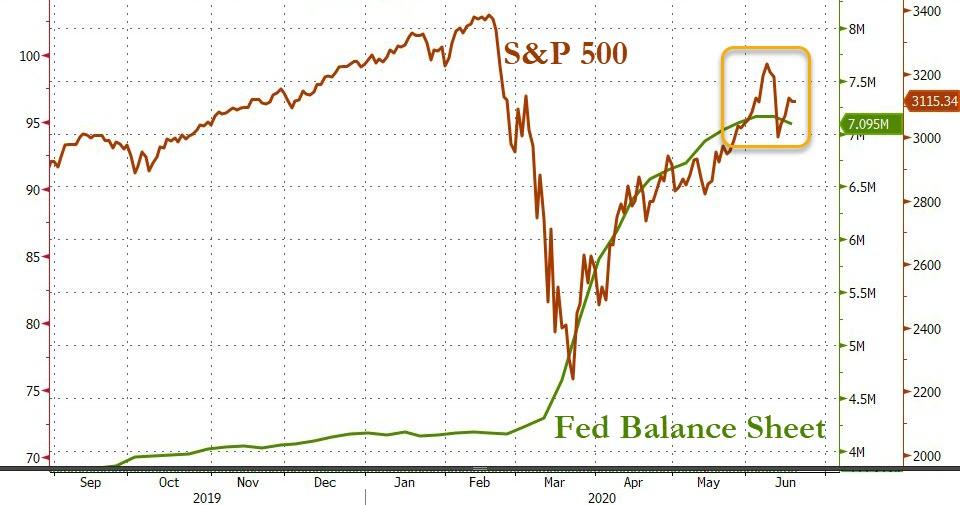

Though it’s been largely forgotten in all the recent turmoil, the US financial system was already in crisis last year, as

the repo market – where banks lend money to each other –

locked up, forcing the Fed to reinstitute quantitative easing. The following

chart screams “emergency!”.

SEE CHART:

Federal Reserve Balance Sheet

{kind=link}

Then came the pandemic, which sent the global

economy into freefall. The Atlanta Fed’s GDPNow reading

currently shows the US contracting at an annual rate of over 45%.

See Chart:

{kind=link}

Too much of a bad thing

So here we are.

- The Fed can’t print new small businesses once the existing ones die.

- The police can’t stop riots without shooting the rioters.

- Corporate profits are cratering with no obvious path to recovery.

- Stock markets are up, but only because financial asset prices are the sole part of the current mess that monetary policy can influence.

Most Americans are no doubt praying that this is it for a while.

But the universe, don’t forget, has a nasty sense of humor. So it

might have a few more surprises up its sleeve.

Consider:

Indian

and Chinese troops are pouring into a disputed border region and

there is more than rumors Of Wars: China, India: North

Korea, South Korea, Israel And Turkey All Move Toward War. An

on top the US is now entering its hurricane/ wildfire season which raises the prospect of mass-evacuations

during new pand.

Put simply, how can anyone be buying

growth stocks and ignoring gold in this world?

….

----

----

Despite

the bounce in retail sales,

there

will still be no “V-shaped” recovery...

As long as individuals have a paycheck; they will spend it. Give them a

tax refund; they will spend it. Issue them a credit card; they will max it out.

Give them a government stimulus check; they will spend it as well. Don’t believe me, then why is consumer debt at record levels?

SEE CHART:

{kind=link}

Debt-Driven Consumption

If consumers were even partially responsible, financial guru’s like

Dave Ramsey wouldn’t have a job selling products to get people out of debt.

However, consumers spending themselves further into debt is what keeps

stock markets going higher and the economy going. Note,

that I said “going,” and not “growing,” Take

a look at the chart below:

SEE CHARTS

{kind=link}

The Mirage Of Economic Growth

The ‘gap’ between the ‘standard of living’ and real disposable incomes

is shown below. Beginning in 1990, incomes alone were no longer able to meet

the standard of living so consumers turned to debt to fill the ‘gap.’ However, following the ‘financial crisis,’ even the

combined levels of income and debt no longer fill the gap. Currently,

consumers cannot fill the record $2654 annual deficit to maintain their

lifestyle without more debt.”

SEE CHART:

Debt Driven consumption Retards Economic Growth

{kind=link}

The gap between the standard of living and incomes is another

reflection of the wealth inequality which is pervasive in the economy.

Less Then Meets The Eye

While there was a massive jump in retail sales in May, a look below the

headlines revealed a different picture. As noted by Mish

Shedlock:

“Despite the surge, sales numbers are back to levels seen in late 2015

and early 2016. On a year-over-year basis, sales are 6.1% below May

2019. Total sales

for the March 2020 through May 2020 period are down -10.5% from the

same period a year ago.

The stimulus checks are gone and more checks may be problematic to get

through a deeply divided Congress. The additional $600 in unemployment benefits

runs out next month, and there is only talk of a bill to extend them at reduced

levels.

Unemployment is still a problem.

See later on.

What the headlines miss is the growth in the

population. The chart below shows retails sales divided by the current

16-and-over population. (If you are alive, you consume.)

SEE CHART:

Annual % chg in Retail Sales per capita

{kind=link}

“Before the “Financial Crisis,” the economy had a linear growth

trend of real GDP of 3.2%. Following the 2008

recession, the growth rate dropped to the exponential growth trend of roughly

2.2%. Instead of reducing the debt problems, unproductive debt, and leverage

increased.”

SEE CHART:

Real GDP vs Lineal & Exponential Trends

{kind=link}

EMPLOYMENT PROBLEM

There are two reasons for this, which are continually overlooked or

worse simply ignored, by the mainstream media and economists. The first is that

despite the “longest run of employment growth in U.S. history,” those

who are finding jobs continues to grow at a substantially slower pace than the

growth rate of the population. The

economic shutdown exposed this weakness.

“Since the beginning of the last economic expansion, the working-age

population has grown by 25.3 million while employment has fallen by 1.14

million through May. As the BLS confirms above, there are over 26 million who

are “missing” due to how employment is calculated.”

SEE CHART:

{kind=link}

“What is crucially important to the economy is full-time employment,

which creates enough income to expand economic growth. The

number of full-time employees to the working-age population is at 44.81%, which

is not high enough to support economic growth.”

SEE CHART

Full Time Employees Relative to Working age Population

{kind=link}

Consumers Are All Tapped Out

Secondly, while stimulus checks and extra-benefits may provide a

temporary boost to incomes, that income boost is only temporary. The reality is that 80% of Americans continue to live

paycheck-to-paycheck and have little saved in the bank. With years of

wage stagnation, the cost of living now exceeds what

incomes and debt increases can sustain.

SEE CHART:

Debt Driven Consumption Retards Economic Growth

{kind=link}

It is also why despite the annual hopes of “stronger economic

growth,” the 3-year average of economic growth continues to

deteriorate. With consumers forced to consume more

on credit, such will lead to a slower economic recovery as the ability to tap

additional credit becomes problematic.

SEE CHART:

CONSUMERS using Credit to Consume

{kind=link}

The impact on the economy from record levels of unemployment will have

a wide range of impacts forestalling an economic recovery. The first, is a deep suppression of wage growth, which is

derived from both recessionary drags and job losses.

SEE CHART:

OMPENSATION Wage & Salary Disbursements

{kind=link}

Tightening Up

As stated, with reduced incomes, it is harder to make ends meet harder

to obtain additional credit. Given consumers are

dependent upon credit to “fill the gap,” and with banks

tightening lending standards, access to credit will become more difficult.

SEE CHART:

Lending standards Getting Much

Tighter

{kind=link}

Conclusion

As I

discussed last week, the current detachment of the stock market from the

economy is likely an illusion that will not last long.

“The economic destruction playing out in real-time will eventually

weigh on markets. There is a negative feedback loop between employment and

consumption. As unemployment rises, consumption falls due to a lack of income.

Since businesses operate based on demand for goods and services, the

correlation between PCE, fixed investment, and employment is high.”

SEE CHART:

Businesses Operate Against Actual Demand

{kind=link}

As noted, even with the reopening of the economy, businesses will not

immediately return to full operational activity, until consumption returns to

normalized levels. Without a ready vaccine, if there is

a second wave of the virus, consumer confidence would likely reverse. Such

would put further pressure on sales and, ultimately, corporate profits.

SEE CHART:

Link Between Corporate Profits &GDP

{kind=link}

As I concluded in a note last year:

“It is hard for consumers to remain ‘confident’ and continue spending

when they have lost their source of income.“

While the markets have indeed managed a strong “rally” from

the March lows, there are reasons to be cautious.

We are just entering into what will likely be a more protracted,

deeper, and more damaging recession than what we saw in 2008.

Despite the bounce in retail sales, there will still be no “V-shaped” recovery.

Invest accordingly.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

Inventing “majorities”, typical from nazis

Famous bases long named after

Confederate generals

undergoing Pentagon review...

====

Parson recommended to adapt to

your context 1st, otherwise

you are an idiot

Not since Nixon went

to China have relations been so bad...

The

reasons are many...

….

Nixon was one of the

most horrible dictators in America. While in China the dictator MAO was replaced

or cleaned by Lin Piao. Since then China mixed socialism with capitalism, as

Lenin did it with the NEP (New Economic Policy) in Rusia. In America the best

President we had was FDR and he mixed capitalism with socialism. Then only

idiots (non sense of history) believe

that capitalism with socialism cannot be mixed. This is what happen with idiots like

Buchanan. Does BB knows that the communist manifesto of MARX was defeated by

the 2nd International and that instead the word “communism” was

adopted the word “socialism” (that in fact reflected a more objective

reality since socialism existed in

Europe 3 centuries before the Manifesto).

Then use “ socialism” instead communism , if your narrow mind has

trouble digesting ‘words’.

----

----

AMERICAN LIFE MATTERS!!

By Hugo Adan

6/19/20.

This is my answer to one person who has no sense of

history:

In short,

the 2020 recession will usher in a new “Progressive Era” of the early 1900s,

or, more accurately, another

“Regressive Era.”

….

….

The progress of history doesn’t happen in direct line (from A to B to

C-D.. etc) , it goes in spiral and in

ascending way (from worse to best). When

history is repetitive is bad sign, it mean that critical contradiction inside

our system was not solved.

The old duopoly political system

we have is repetitive (Dems & Reps-reproduce the same militaristic stupidity

of the past: state invest in weapons & wars, not in best health nor

education for all.

That type of history has arrived

to its end since ‘our assumed enemies’ has similar power & similar end too:

not winners, but MAD plus total destruction of the world with new pandemics,

ZERO economic progress.

All this is symptom that a new REV is coming in America & the world

too, since it is the end of neo-

liberalism what is at stake. Neo-liberalism in fact doesn’t exist anymore. That we have

instead is different types of monopolies,

all controlled by huge

billionaires. This is the history that is arriving to its end.

The contradictions of upper classes with middle and lower classes (the

labor) will be resolved when the

oppressed make a UNITED FRONT to defend their interest, then we will talk of a real

REVOLUTION in process.

Radical change is ubiquitous, nothing can stopped (much less fraudulent

elections: buying votes mascaraed with invented pools). Most people in America

has decided ABSTENTION instead of going

to the ballot box.

History progress doesn’t move in close circles, its spiral move may

have little set backs , but never total

regression to the pass, only brief step back to soon make two steps forward.

SO, after the coming REVOLUTION there will not be total ‘regresive era’ to

the past. History in America proved so and is going to do it again after a

socialist revolution coming.

The new revolution will not look

like others in our past not in the world. This one will be heroic creation of

our new nation. We won’t die bending our knee to the

ruling class, nor will die in the bed of pandemics, said young people.

The

coming revolution is going to be a new creation of our Nation, different to

previous types of Revolution in the world. Young people in America has already

decided their destiny. That why

we said : AMERICAN LIFE MATTERS!

====

====

As city politicians continue to push their

bailout and statehood agenda, it’s important to note that most would

take a substantial pay cut if

they actually mirrored the salary scale from the states...

====

"I don’t really understand

why he decided to take that risk."

====

"The news media on the left has

completely ignored all of these Biden speeches that clearly show some kind ofcognitive decline."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

Ruso-phobia behind?

Sen.

Menendez: “This drawdown weakens America and Europe. And Vladimir Putin understands and appreciates that

better than anyone.”

====

SPUTNIK and RT SHOWS

GEO-POL

n GEO-ECO ..Focus on neoliberal

expansion via wars & danger of WW3

-Live Updates: Statues Attacked and Dismantled

as Protests Continue in US After George Floyd's Death

----

----

THE REST FOR TOMORROW

====

====

No hay comentarios:

Publicar un comentario