ND MAR 13 20 SIT

EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

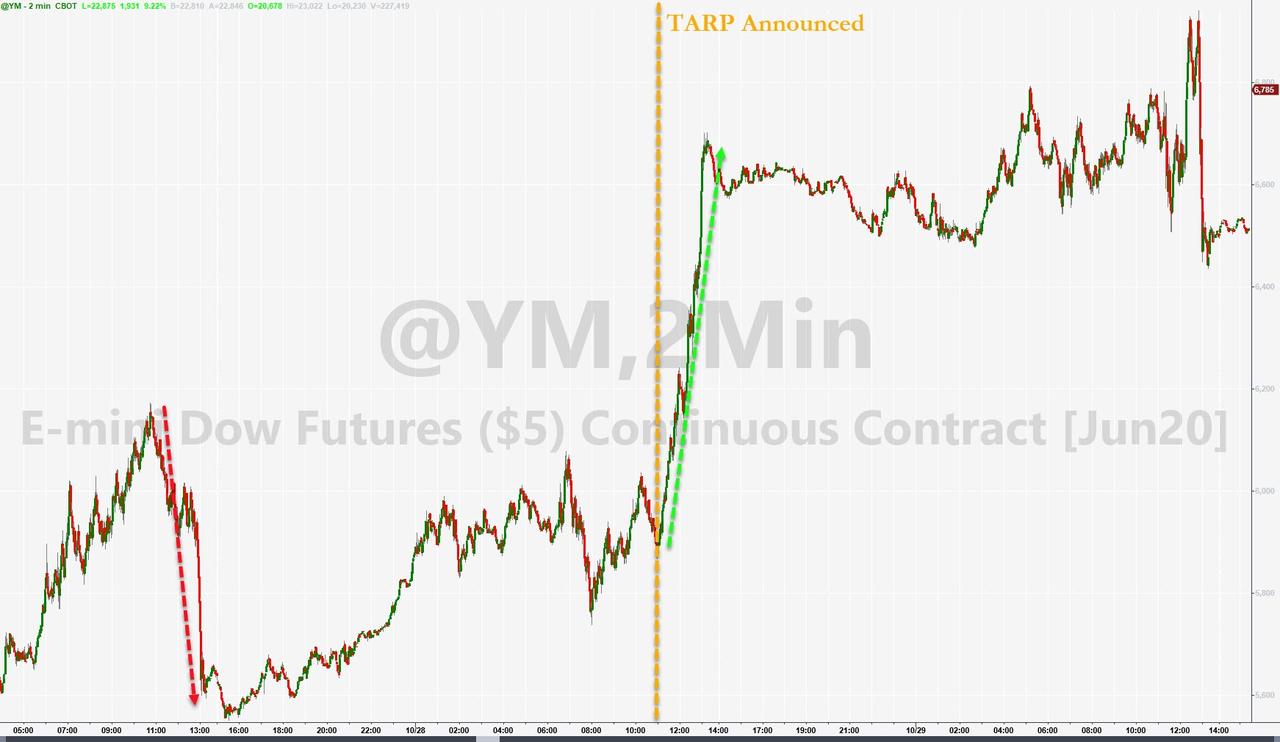

Today saw the biggest spike in US equities since

October 2008 after an avalanche of

intervention in the last 24 hours across the world and

extended by 1600 Dow points as Trump unveiled his stimulus/testing plan...

See Chart:

{kind=link}

The last time the market rallied this much was

10/28/2008 - the day TARP was announced...

See Chart:

{kind=link}

HOWEVER, THE S&P FELL 35% FURTHER AFTER THAT

TARP BOUNCE...

See Chart:

S&P 500

Last day the Market rallied as much as today

{kind=link}

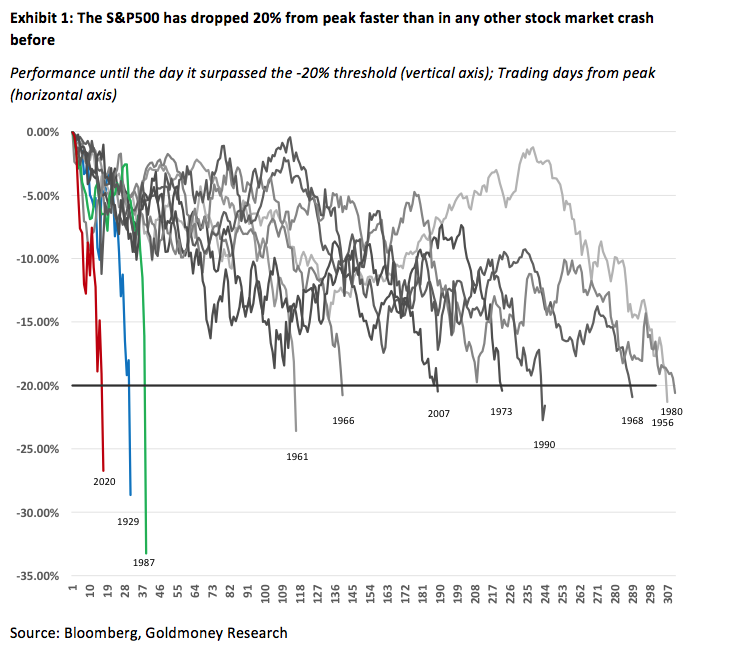

But, overall, the market just suffered its fastest,

most aggressive collapse into a bear market... ever...

See Chart:

{kind=link}

But even more ominously, the

broadest measure of the US equity market - The NYSE Composite Index - has collapsed below the

2007 highs (despite trillions in added liquidity)...

See Chart:

{kind=link}

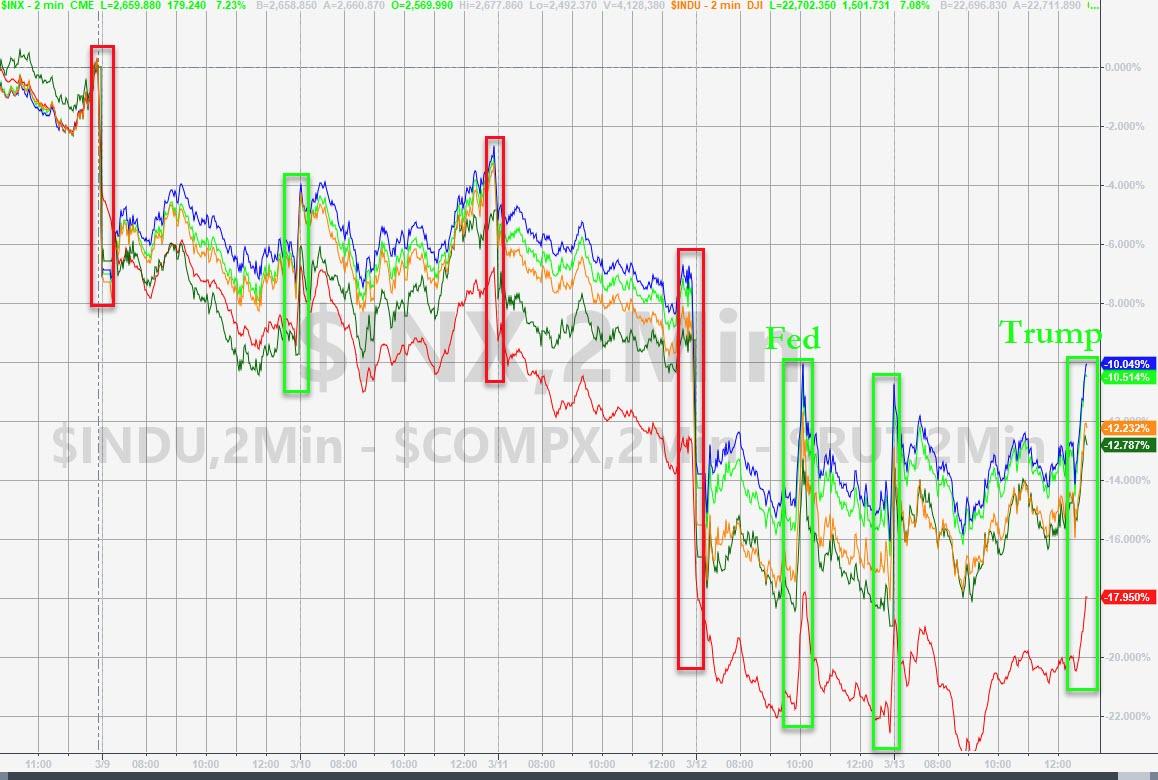

US equity markets ended the

week on a stronger note, big gains overnight (limit up in futures), a plunge at

the cash open, only to rebound when rumors hit that the President would declare

a National Emergency (implicitly some fiscal largesse) and when he announced

his plans, the market went vertical... this was the best day for stocks since 10/28/08...

See Chart:

{kind=link}

This

was the market's worst week since Oct 2008, but Small Caps' 20% crash this week

is the worst since 1987 (Small Caps' 3-week plunge of 30% is the worst ever)

See Chart:

{kind=link}

Banks

were battered (but bounced today)...

See Chart:

{kind=link}

VIX

surged higher this week at an unprecedented pace, closing near record highs...

See Chart:

{kind=link}

Investment

Grade credit crashed this week - by our record this is the biggest weekly spread

decompression in history...

See Chart:

{kind=link}

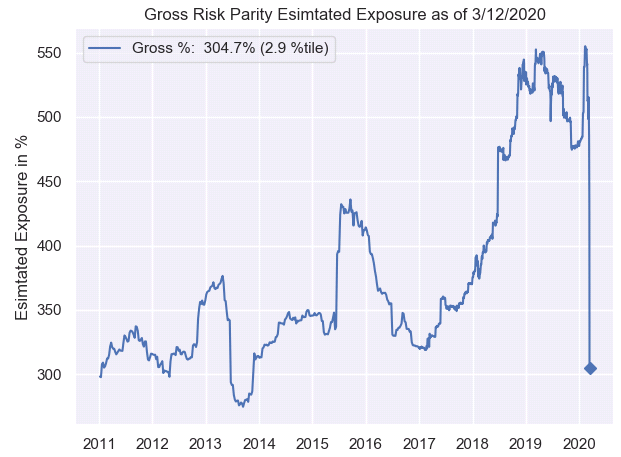

As

Risk-Parity Funds saw the biggest deleveraging losses in history...

See Chart:

{kind=link}

Bonds

suffered a total bloodbath this week - despite the collapse in stocks, with the

end of day seeing a melt-up in rates...

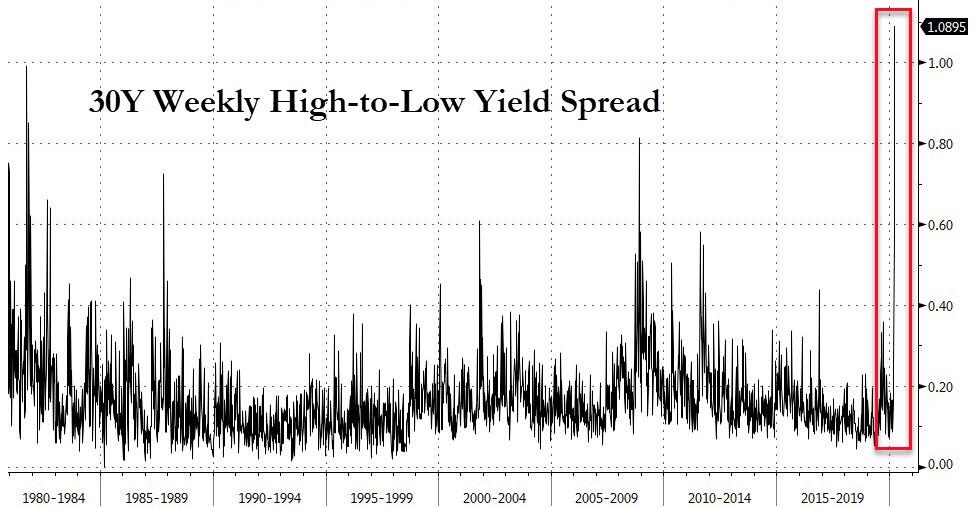

30Y yields exploded higher this

week after Sunday night's crash to record lows. Today saw 30Y spike to 1.79%

intraday before tumbling back to 1.39% on the Fed's

emergency QE today...

After

collapsing to 69bps on Sunday night/Monday morning, this week's blowout on

yields is the biggest ever...

{kind=link}

But most worryingly, the Bond ETF world really

started to break as massive, unprecedented

discounts occurred in Treasury, Muni, and HY Credit ETFs exposing the

illiquidity of the underlying assets...

See Chart:

Before

we leave bond land, we note that CMBX

crashed back towards its lows

See Chart:

{kind=link}

And the

market is now demanding practically 1 full percentage point cut in rates next

week by The Fed...

See Chart:

{kind=link}

The B-Dollar

was massively bid this week as it appears key safe-haven flows - and liquidity

demands - sparked a 'sell-everything-else' trade worldwide... (3 days this week

were the biggest daily gains in the dollar since Nov 2016)

See Chart:

{kind=link}

The

surge in the dollar this week did not help but commodities were clubbed like baby

seals as it seemed someone was mass liquidating everything in a scramble for

cash...

See Chart:

{kind=link}

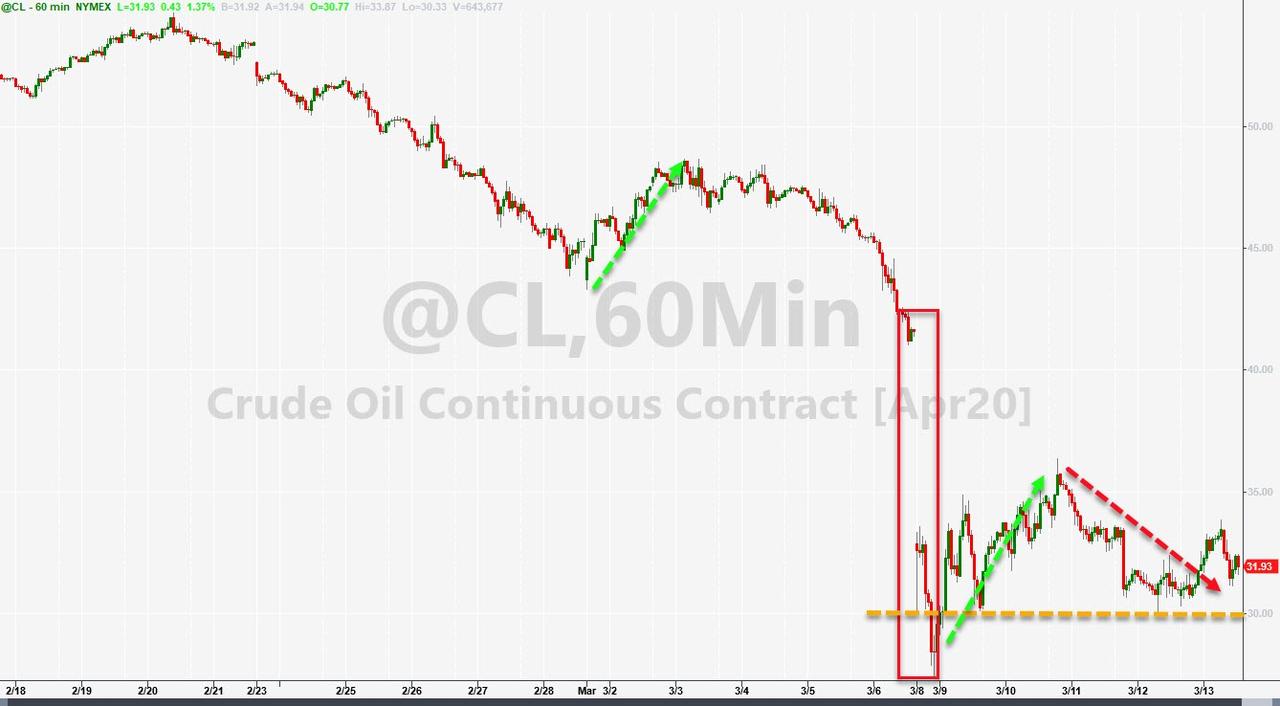

This

was WTI's worst week since Dec 2008 (and biggest 3-week drop ever)...

See Chart:

{kind=link}

Finally,

this was the worst weekly loss for a 'diversified' book of bonds and stocks

since Lehman...

See Chart:

{kind=link}

And, if you're wondering where this ends, it's

simple - below 2,000 for the S&P 500... as the last five years of equity

market gains have been total delusion...

See Chart:

{kind=link}

And if

you thought The Fed's Trillion-dollar-plus care-package helped... it didn't!

FRA-OIS spreads continued to blow out, strongly suggesting massive dollar

shortages and/or fear of systemic bank credit risks

See Chart:

{kind=link}

….

----

----

"I’ve never seen that before,

the inability to trade a U.S. Treasury."

On the first day of this week,

which would soon mutate into the worst week for capital markets since the 2008

financial crisis, we warned that markets are about to go full tilt for the

simple reason that "there

is no liquidity", something we first highlighted at the start of the

month when we pointed out "Two

More Problems For The Bulls: Market Liquidity And Short Interest Are At All

Time Lows."

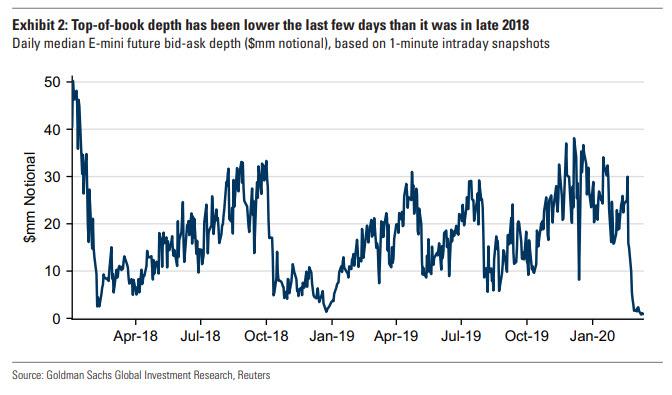

Why our constant focus on

liquidity? Because as Goldman explained on Thursday, "liquidity and

volatility are interconnected, creating a self-reinforcing loop, and as a

result liquidity conditions have been an important contributor to the velocity

of recent S&P 500 moves." Typically the conventional metric of

liquidity representing the dollar-amount of SPX E-mini futures available to

trade electronically on the typically 25-cent wide market, has - as Goldman put

it - "started to

lose meaning as fewer and fewer market participants are quoting one-tick-wide

markets for the futures at all."

See Chart:

{kind=link}

As Goldman further explained,

as volatility spiked, electronic futures liquidity has fallen to the point

where there has been a median of just 10 contracts, representing $1.5mm

notional, on the bid and ask of E-mini futures screens over the past week

(compared with a median of 120 contracts, representing $18mm notional, in 2019)…

The key takeaway of diminished liquidity, however

measured, is that individual

trades can move markets more than they otherwise would have, leading to higher

volatility.

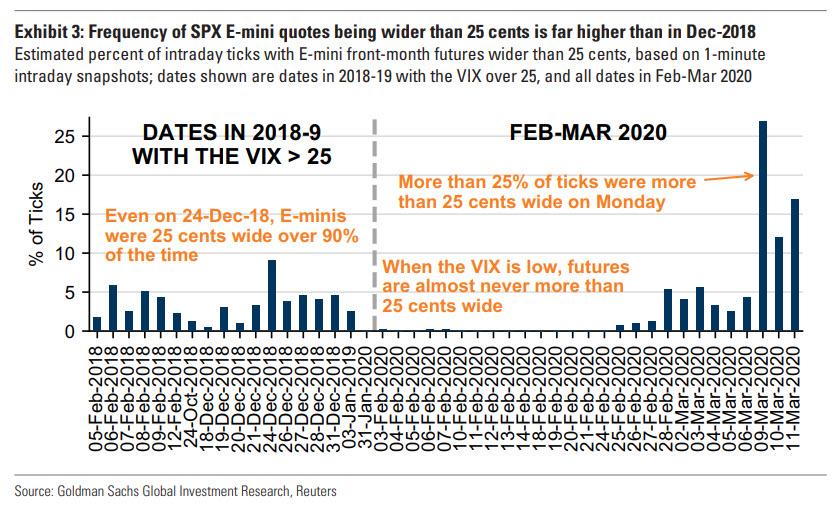

See Chart:

Frequency

of SPX E-mini quotes being widen than 25cents I higher than in Dec2018

{kind=link}

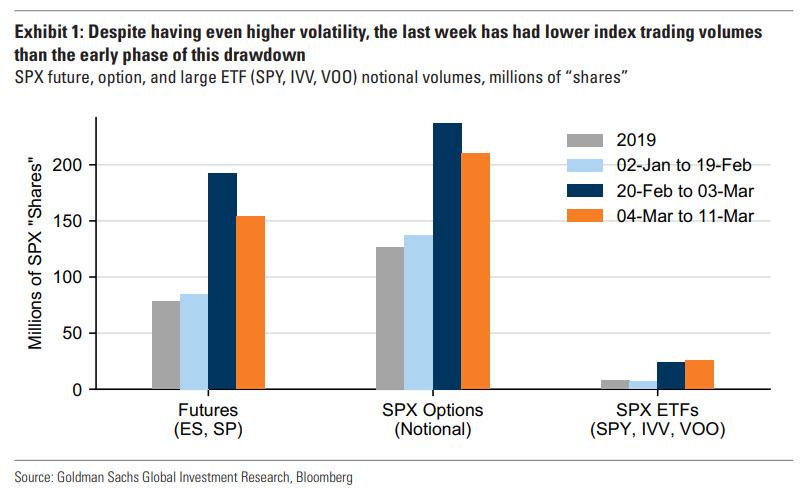

A key

reason for the latest drop in liquidity has, curiously, been the concurrent

drop in trading volumes: SPX future and option volumes were materially lower

over the past week than they had been in the initial days of this market

downturn (although they were still high relative to normal periods).

See Chart:

Despite

having even higher volatility the last week has had lower index trading volume

{kind=link}

Continue reading up to you get

this conclusion:

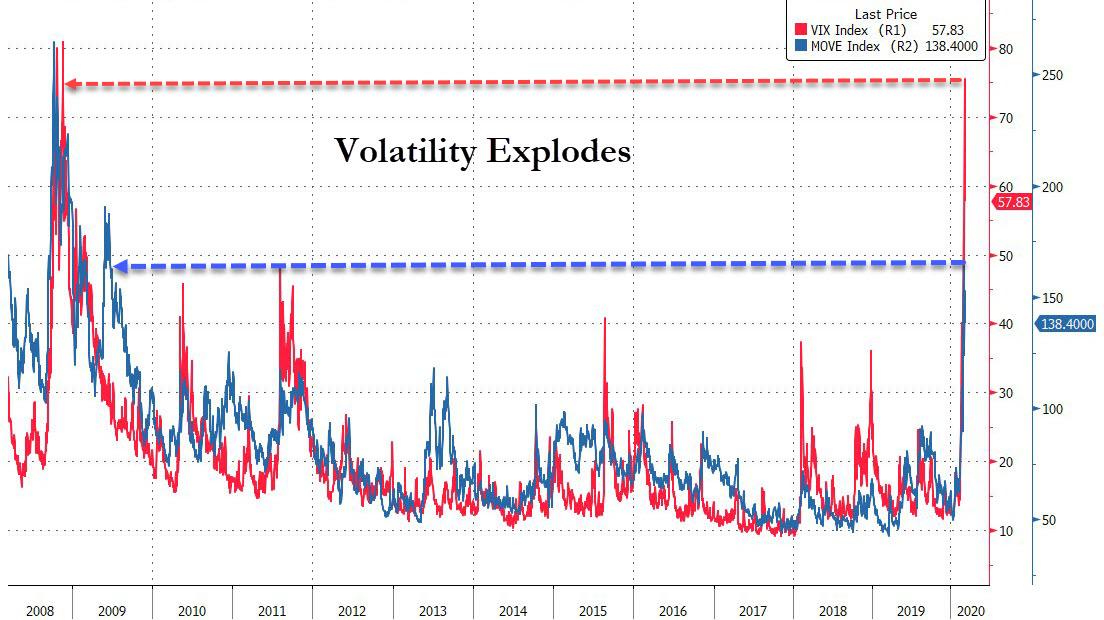

Finally,

adding insult to injury, volatility - both for stocks and bonds - continues to

surge. The Bank of America Merrill Lynch MOVE Index, which measures price

swings in Treasuries, and the VIX both jumped to the highest levels since the

financial crisis.

See Chart:

{kind=link}

"We are at the stage where central banks need

to provide exceptional liquidity into the market to make sure that basic

markets can function."

“The Fed just cutting rates

again at this stage is really not the right medicine,” Li said."'The Treasury

market is broken -- with it being very illiquid. There’s very wide spreads between on- and off-the-run

spreads," and other signs of dislocation.

Let's

just hope Jerome Powell, who first diagnosed the real problem with the US

capital markets back

in 2012, knows how to fix them.

….

----

----

"The plunge in US equities

pushed weekly returns down to 7.7 standard deviations below the norm.... we can

say with confidence that we are witnessing a history-making market disaster in

real-time."

See CHART:

DJIA

WEEKLY RETURNS SINCE 1900 (Z SCORES)

{kind=link}

Setting aside legitimate

quibbles over the statistical significance of this, we can say with confidence

that we are witnessing a history-making market disaster in real-time.

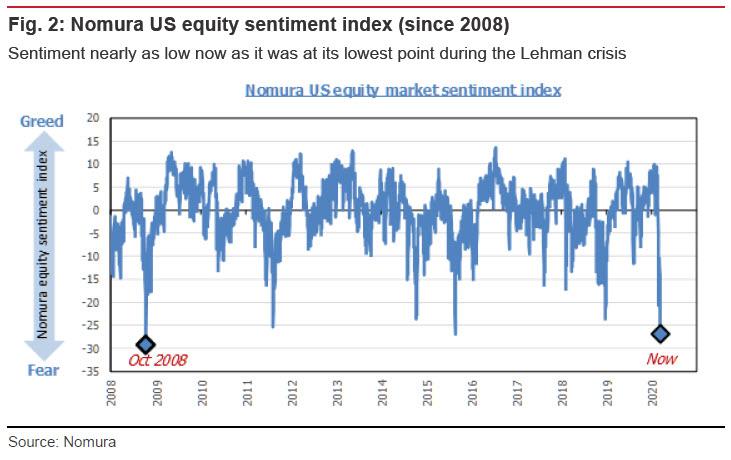

US stock market sentiment has also seen a jarringly swift collapse, as

equity sentiment has now gone beyond the low point marked during the 2015

renminbi shock. In

little more than the blink of an eye, the situation has come to look like the

2008 Lehman Brothers crisis all over again.

See Chart:

Nomura US Equitty

sentiment index (since 2008)

https://www.zerohedge.com/s3/files/inline-images/nomura%20sentiment%20index%203.13.jpg?itok=HPeEQ8i8

{kind=link}

Continue reading the best

description of our Economic collapse before arriving to this conclusion:

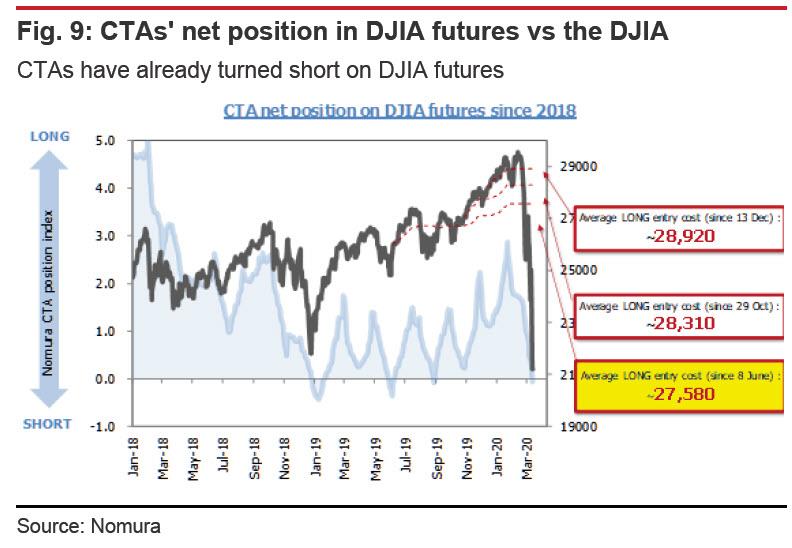

CTAs have turned short on DJIA futures. Because of the rapid pace of

the Dow's drop, CTAs have been able to build sufficient short positions. As

they had already preferred short positions with the DJIA below 28,000, CTAs look likely to build short positions rapidly at current

share price levels.

See Chart

CTAs

have already tuned short on DJIA Futures

{kind=link}

It may be, then, that

the market has only just begun staring into the abyss.

….

SOURCE: https://www.zerohedge.com/markets/77-sigma-move-nomura-says-market-has-only-just-begun-staring-abyss

----

----

SHORT NEWS on ECONOMICS:

Never

forget that there’s a fool on

every corner and a sucker born

every minute.Avoid being one of them

when at all possible...

====

====

Even as stocks surge, the interbank

funding market is approaching a state of total paralysis. Unless this is fixed,

and soon, total systemic collapse may follow.

====

This week’s unprecedented moves are

more about investors responding to the biggest VaR shock since the Lehman

crisis.

See Chart:

====

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

Legislation would allow carriers to arrive in

US unimpeded...

====

US-World

ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

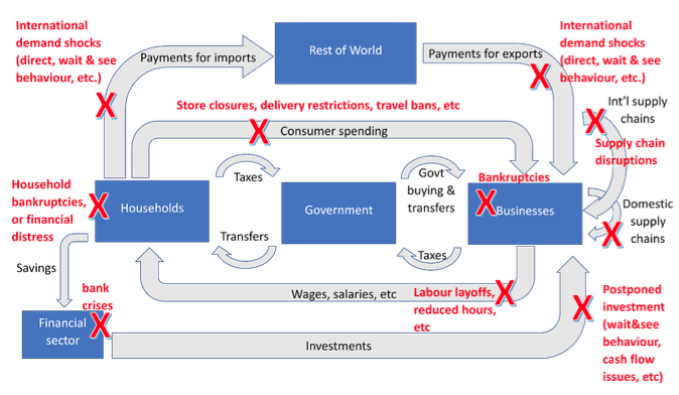

The

COVID-19 crisis has struck the

economic ‘machine’ in several placesat the same time...

See Chart:

{kind=link}

====

Siding with CCP propaganda?

====

Iraqi officials outraged over

Thursday airstrikes on Iran-backed militias, citingnational troops killed and wounded.

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

====

ALAI ORG

----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

Craig Collins Civilizations Won’t Decline: They Collapse

Michèle Brand Class

Conflict is Stronger than Clan Conflict

Marshall Auerback Coronavirus

Reveal Cracks in Globalization

Joseph Natoli A

Machine to Beat President Trump

Nomi Prins The

Fed, the Virus, and Inequality

Alice Slater The

Virus of Nuclear Proliferation

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

===

No hay comentarios:

Publicar un comentario