JUL 10 20 ND SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

====

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

On the

week, Nasdaq has soared higher once again, notably divergent from the rest of

the markets with Small Caps actually down on the week...

See Chart:

{kind=link}

Which

has sent the ratio of Megacap-Tech to Small Caps back near a record high...

See Chart:

Nasdaq

100 / Russell 2000

{kind=link}

Nasdaq is up 8 of the last 9 days and 17 of the last

20 days - this is easy!!!

Median

US stocks continue to diverge significantly from the handful of megatech stocks

driving the Nasdaq ever higher...

See Chart:

Nasdaq vs Median US stocks

{kind=link}

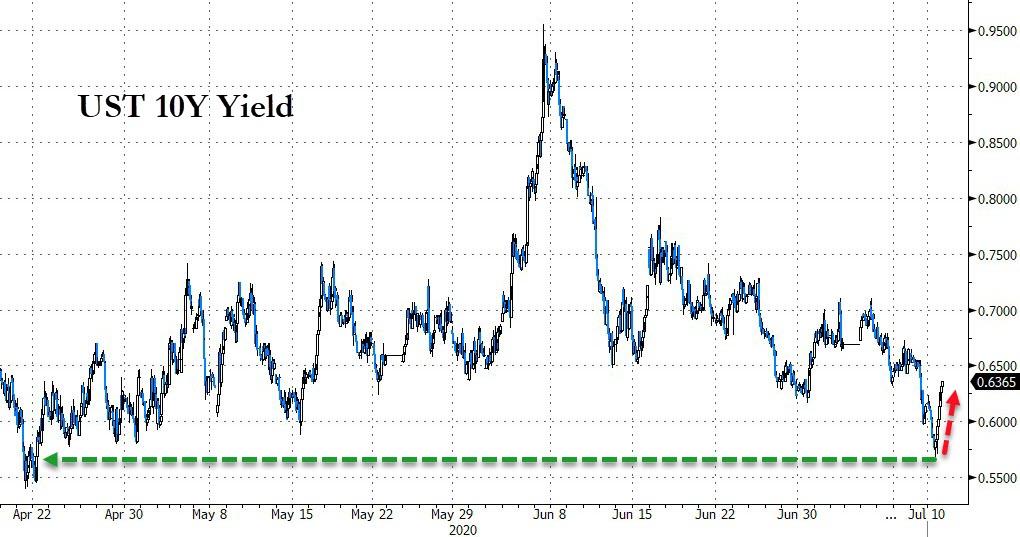

Treasury

yields touched a two month lows today...

See Chart:

UST 10

Y Yield

{kind=link}

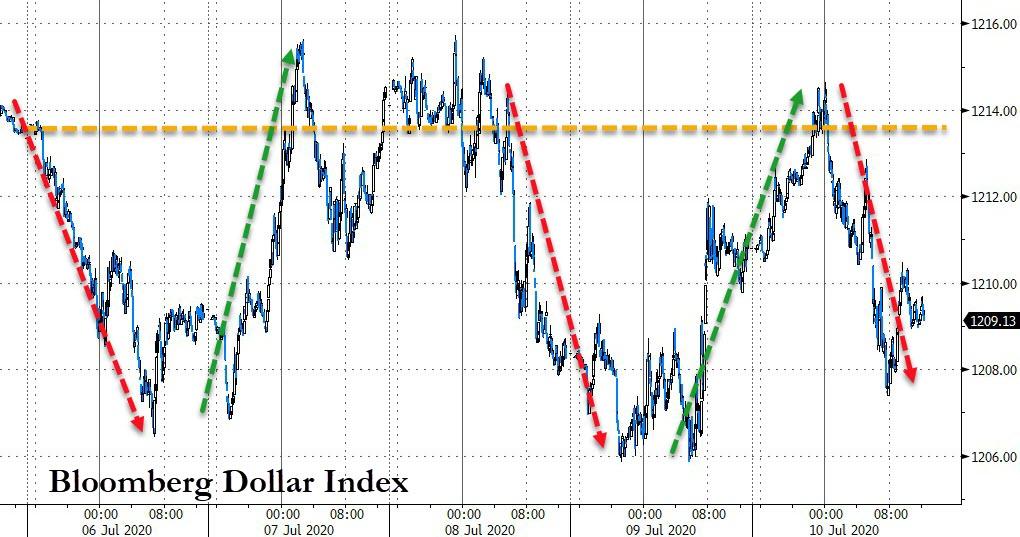

The B-Dollar

Index ended lower on the week, chopping around in a tight range...

See Chart;

{kind=link}

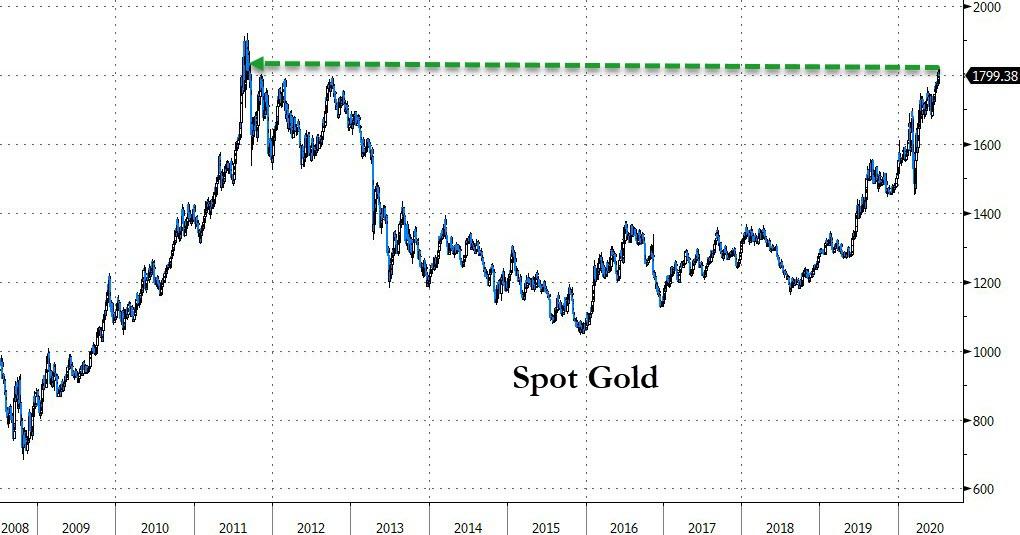

Spot

Gold reached back to its highest since 2011...

See Chart:

{kind=link}

Bonds

ain't buying it...

See Chart:

Nasdaq

vs 10Y Yield

{kind=link}

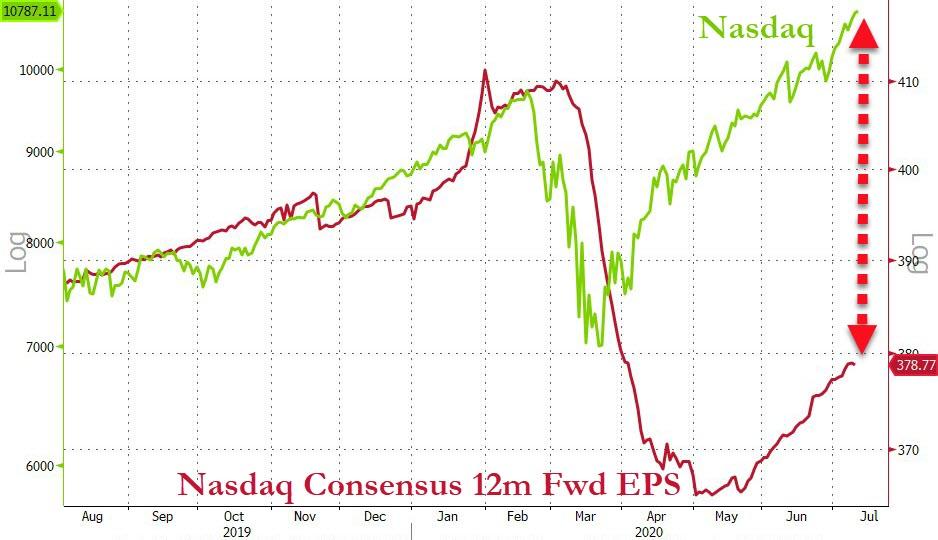

Because

fun-durr-mentals...

See Chart:

Nasdaq

vs Nasdaq Conssensu 12m Fwd EPS

{kind=link}

….

----

----

With every passing day, the bizarre

freakshow that was once known as the "market" gets even more bizarre.

And we use the term "market" only in its loosest,

legacy sense, one where it represented more than just the centrally-planned

intentions of a few central bankers and politicians. Why? Because as BofA's CIO

Michael Hartnett reminds us in his latest Flow Show report, the disconnect

between macro and markets has never been greater - i.e., they have never been

more broken - but that is to be expected for the following three reasons:

- Markets rationally being "irrational": government and corporate bonds have been fixed ("nationalized") by central banks, so why would anyone expect markets to connect with macro, why should credit & stocks price rationally.

- Markets leading macro: policy makers (see China this week) know higher asset prices necessary condition for macro recovery (Wall St assets are 5.6x size of US GDP)...

See Chart:

US Financial Assets now 5.6 times GDP

..V-shape recovery on Wall St leading V-shape recovery on

Main St (see PMI's & housing activity); gasoline demand good US mobility

signal, up sharply to 9mn barrel/day from spring lows, watch to see if virus

again negatively impacts economy.

3.

Markets rationally pricing-in Max Liquidity, Minimal Growth backdrop, as

they have done for 10 years; of 3042 stocks in

MSCI ACWI currently 2141 >20% below their all-time highs, i.e. in a bear

market.

Also consider this: if the S&P500 (3230 on Jan 1st) was

just "tech, health care, Amazon, Google" it would now be 4173 , and

if the S&P were "everything else" it would be 2924. No secret

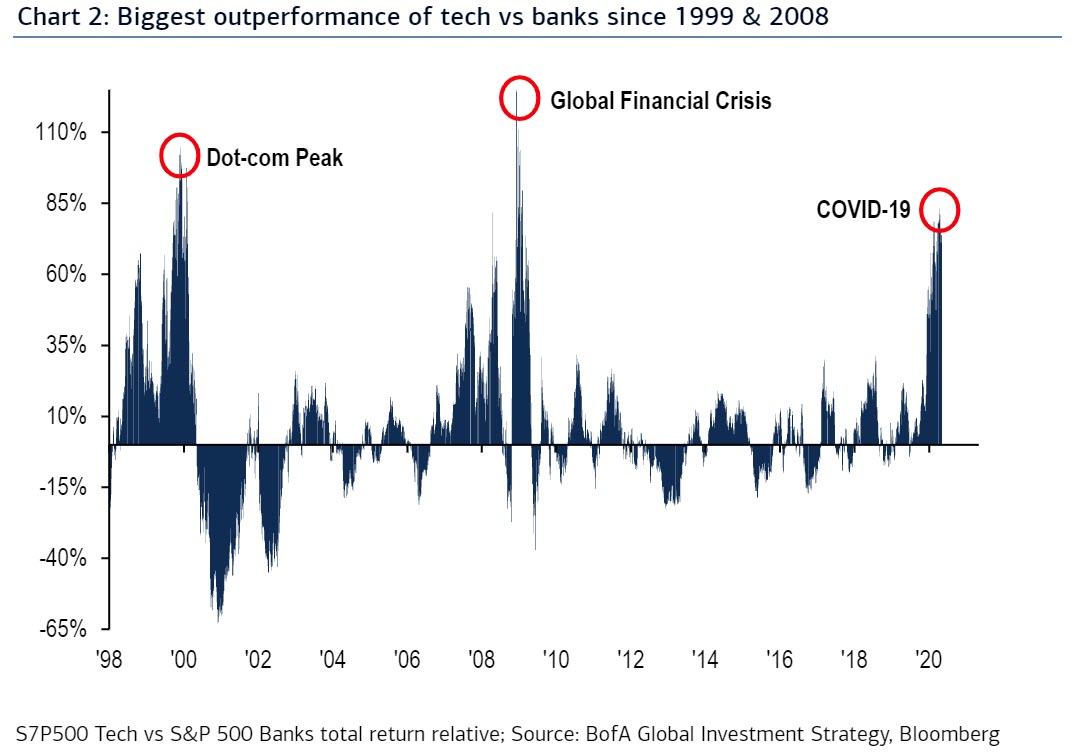

here, but US

tech outperformance over US banks past 6 months biggest since 1999 tech bubble

& 2008 GFC.

See Chart:

Biggest outperformance of Techs vs Banks since 1999 & 2008

{kind=link}

So while markets may be broken - as one would expect in a

world where central banks have taken over all price discovery - three key

trends remain and are totally unchanged for 2020. Per BofA:

- Central bank liquidity drives asset prices;

- Credit prices drive equities;

- Sellers' strike in credit & tech mirrored by buyers' strike in value stocks & banks.

Some other observations from BofA's CIO on what was once a

"market":

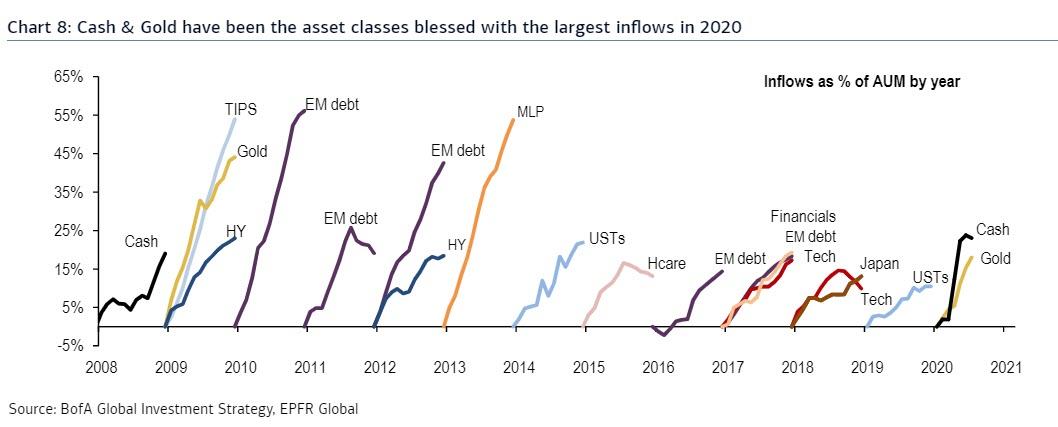

Cash & gold the big inflow

winners in 2020;

See Chart:

Cash & gold been blessed with largest

inflows in 2020

{kind=link}

Gold inflows on cumulative basis at

all-time high:

See Chart:

Cumulative Gold inflows at all time

high

{kind=link}

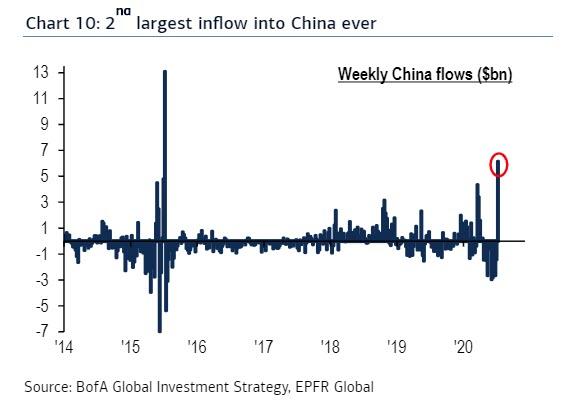

Discounting all-time high in price;

largest inflow to China funds ($6.1bn) since Jul'15 (and 2nd inflow largest

ever):

See Chart:

Largest inflow into China ever

{kind=link}

So with stocks now fully mandated and no longer discount the

future or respond to fundamentals or news, does this mean that stocks will rise

indefinitely until eventually the population burns down the Marriner Eccles

building? According to Hartnett the answer is now, and while stocks see bullish

drivers of Positioning & Policy into the summer, these will peak just as

the autumn begins, at which point bulls will require profits to surprise to

upside allowing rally in risk assets to broaden into HY, value stocks, small

cap and so on; At the same time, bears will argue that big 2020

underperformance of banks a signal of no economic hope & sinister repeat of

1999 & 2008; According to Hartnett, these are the catalysts

required to boost banks:

1. Vaccine: most

likely catalyst for big GDP & EPS upward revisions H2 and flip from growth

to value.

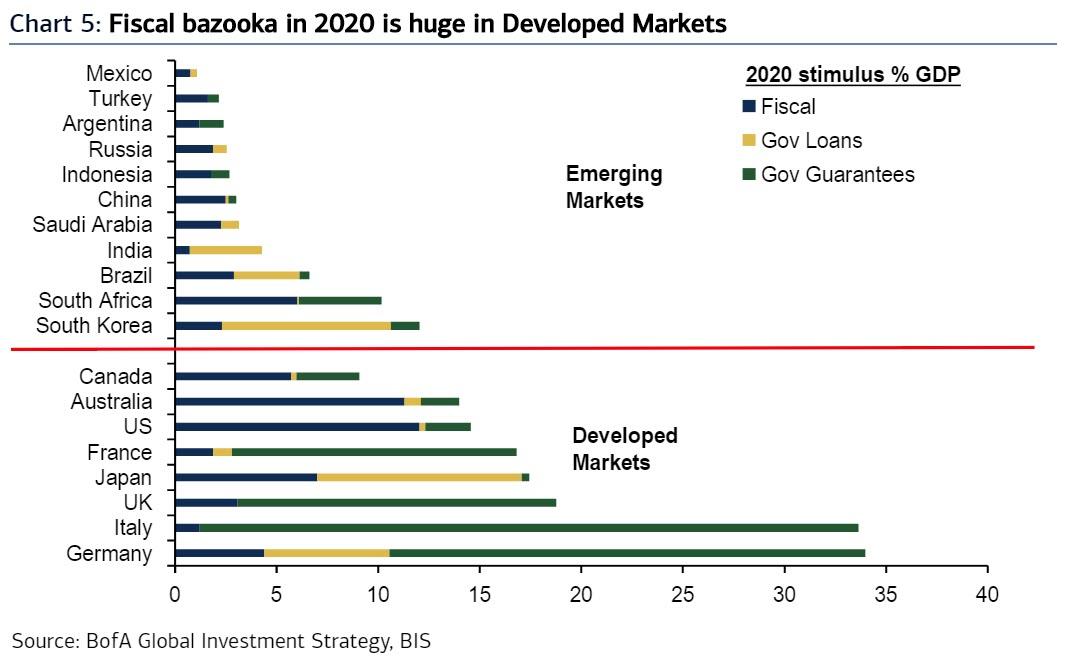

2. Fiscal: 2020

policy stimulus has been massive ($18.5tn of which $10.5tn in fiscal &

$8.0tn in monetary = 21% global GDP) (Chart 5) and coordinated (1st time in

years monetary & fiscal, like two wheels of a bicycle, moving quickly in

same direction working together); banks the natural

hedge for fiscal success (key barometer to watch = small business confidence

surveys, e.g. NFIB) in stimulating animal spirits.

See Chart:

Fiscal bazooka in 2020 is huge in

developing markets

{kind=link}

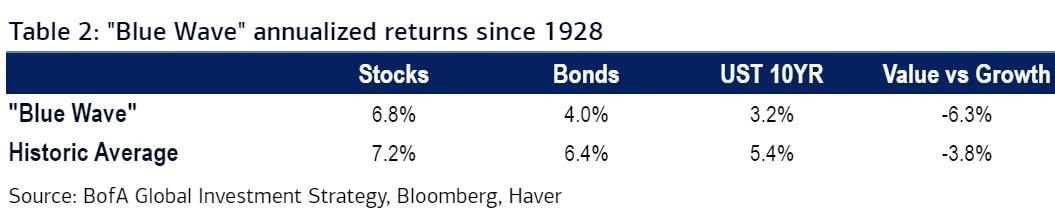

3-Politics: rising

probability of political "blue wave" i.e. Democrats winning White

House, Senate, Congress (latest Oddschecker.com probabilities…Biden win 57%,

Real Clear Politics probability…Dem Senate 62%); Table 2 shows annualized

returns following 7 out of 21 "blue waves" since 1928...returns, more

obviously in bonds, below historic averages after Dem

"clean sweep" but outperformance of value over growth more

pronounced; "Blue Deal" fiscal stimulus in 2021 via infrastructure,

student debt forgiveness, health care spending positive value & banks.

See Table:

“Blue Wave” Historical Average

{kind=link}

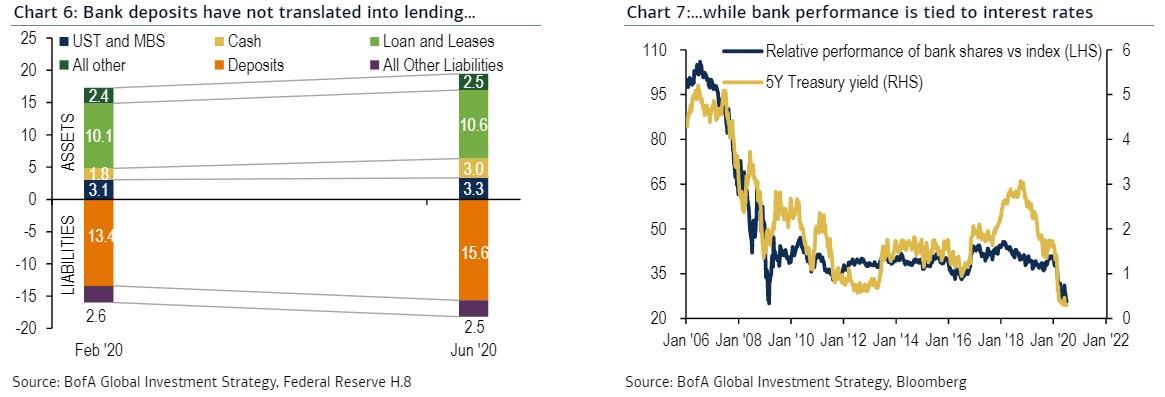

4. Risk-taking: bank deposits up $2.2tn since end-Feb but bank loans up only $0.5tn vs cash/reserves

up $1.3tn and UST+MBS holdings up $0.3tn (Chart 6); bank stocks tied-at-the-hip

to interest rates (Chart 7).

See Charts:

1: Bank deposits have not translated into lending

2: while banks performance is tied to interest rates

{kind=link}

If and when Fed/ECB/BoJ can ever raise interest

rates global banks will become the instant leadership; ironically introduction

by Fed of Yield Curve Control in Sept may in typical contrarian fashion trigger

a rally in banks; but the other irony is that sustained bank performance first

requires risk-taking to boost economic growth & interest rate expectations

in 2021 & 2022; until then bank stock bulls will focus on China (has led

virus, market & macro recovery) & Europe (start of fiscal stimulus).

----

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

"This is a historic

moment of change. We have to respect that..."

====

Meanwhile the Fed's buying of

corporate bonds and ETFs has shrunk by about 50% to around $150MM per day.

See Chart:

FED Balance Sheet vs S&P500

{kind=link}

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

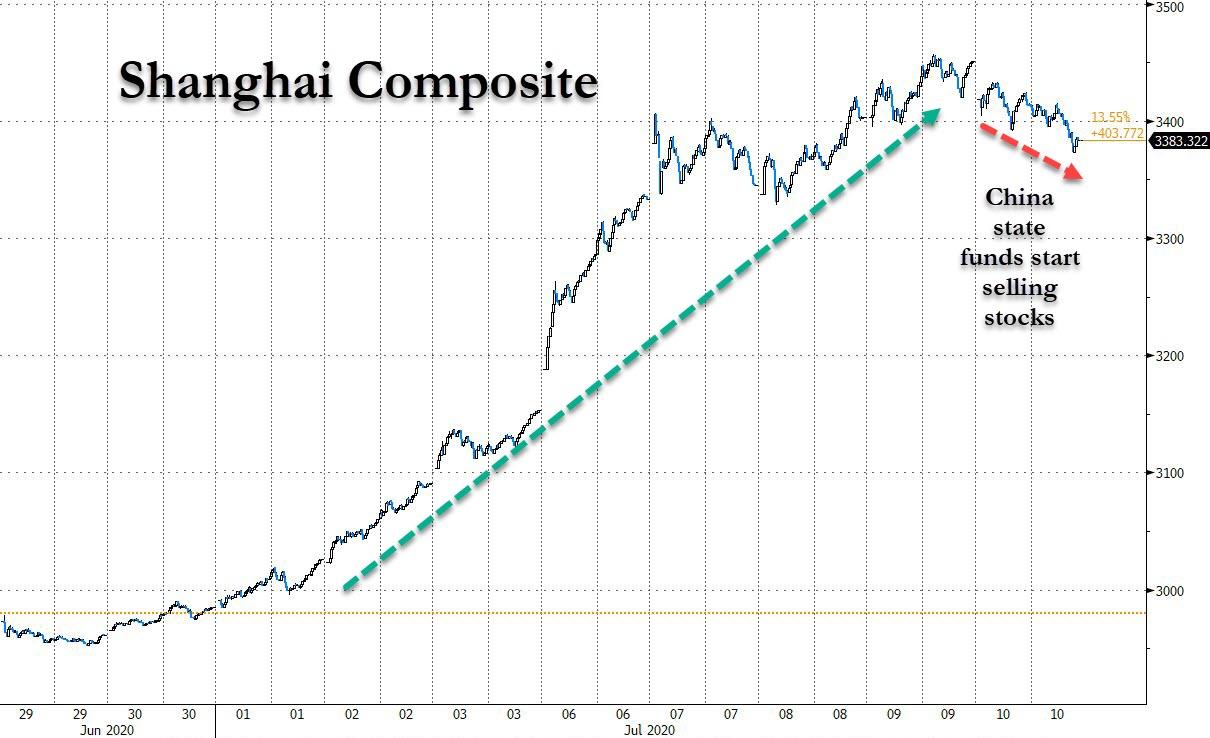

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

"The signal could not be clearer

-- stocks have just become too hot for the regulators’ liking."

The Shanghai Composite closed down 2% and the SSE 50 Index of

Shanghai’s largest stocks ended the day 2.6% lower. The

index had closed Thursday within 2% of its intraday peak in 2015.

See Chart:

{kind=link}

====

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

====

====

No hay comentarios:

Publicar un comentario