EXTRACTS by Hugo Adan

August 7 2019

The Fed may have

launched its first easing cycle since 2007 and liquidity-sapping quantitative

tightening may finally be over, but Powell may have a much bigger problem on

his hands - one which has nothing to do with China, and everything to do with a

dramatic drain of liquidity in the market over the next two months.

The Fed may have no choice but to

resume Quantitative Easing and start expanding its balance sheet again -

potentially as early as 4Q - in order ease funding pressures expected during

the coming wave of Treasury supply.

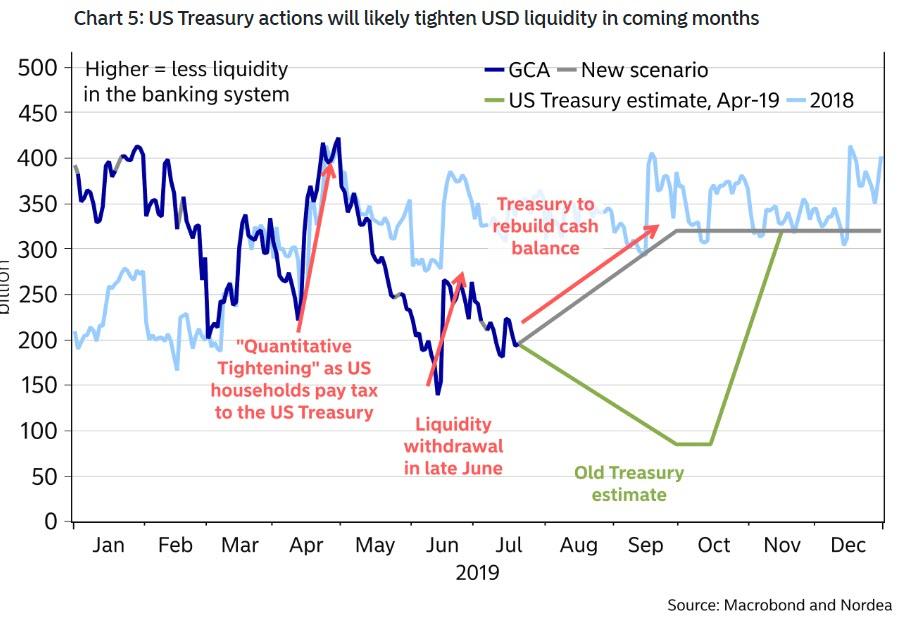

We first hinted at this last

week when we noted that as part of the recently completed debt ceiling

deal, instead of taking its time in replenishing the cash balance (green line

in the chart below), the US Treasury will scramble to rebuild its cash balance

up to $350 billion, from today's level of

$133 billion (gray line), a process which as we said

last Wednesday will "significantly tighten up liquidity in the

banking system and potentially result in turmoil in funding and money markets

as the world is flooded with an issuance of T-Bills" as the

Treasury seeks to fill the $217 billion cash hole, which will lead to a

substantial liquidity withdrawal from the broader financial system as shown in

the following Nordea chart.

See chart:

US

Treasury actions will likely tighten USD liquidity in coming months

{kind=link}

The problem, in a nutshell, is

that traditionally such a rapid liquidity withdrawal

leads to weaker risk appetite, a far stronger USD and lower treasury yields,

while widening the LIBOR/OIS spread and further depressing the already negative

EURUSD cross-currency basis.

While we cautioned about all

this last week (even before the FOMC announcement), it appears that our

appreciation of just how severe this problem may be for the Fed and capital

markets was overly optimistic, because according to a new analysis by Bank of

America's Mark Cabana, the

Fed may have no choice but to resume Quantitative Easing and start expanding

its balance sheet again - potentially as early as 4Q - in order ease funding

pressures expected during the coming wave of Treasury supply.

For those unfamiliar with the

funding problems the Treasury's cash rebuild entails, these are four-fold, as

BofA explains by using the poetic description that "it will keep on raining and funding levy

is likely to break", or said more

technically, USD funding market pressure will keep rising through year end due

to the following four factors:

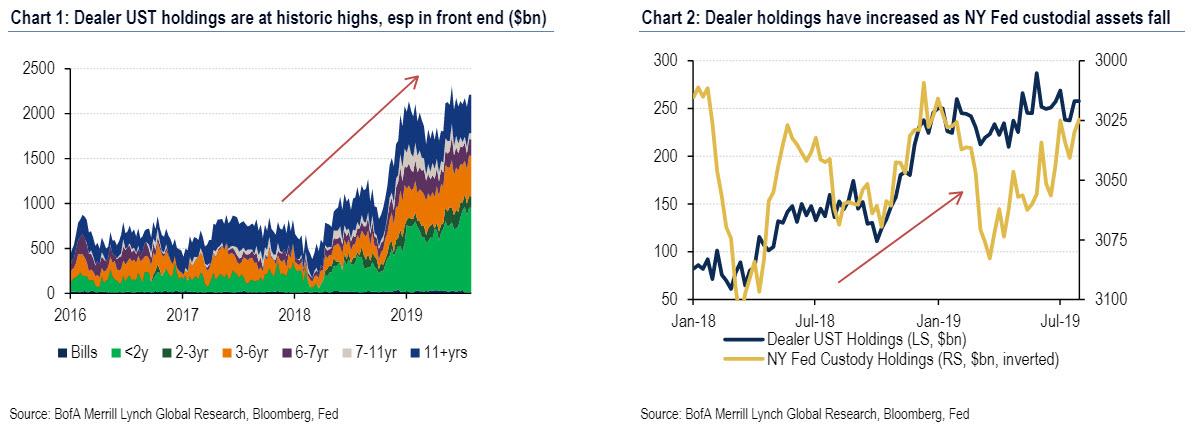

- 1. Treasury supply: Treasury supply will be elevated in the wake of the debt limit resolution. From now thru year end BofA expects net UST supply of ~$750bn (~$500bn coupons, ~$250bn bills). This supply will come to market rapidly: in August alone we expect $90bn net coupons and $160bn net bills. These estimates are close to Treasury; as we noted last week, the Treasury's financing estimatessuggested a net $814bn supply increase in 2H 19.

- 2. Dealer UST holdings: Primary dealer balance sheets are near historic highs and concentrated in short-dated holdings (bottom chart, left). The elevated dealer holdings are likely due to both voluntary and involuntary reasons: voluntary = dealers may view USTs cheap vs OIS and futures, involuntary = heavy UST supply and overseas reserve manager selling (bottom chart, right). Already bloated dealer balance sheets would likely pose intermediation challenges for UST supply, especially with year-end GSIB regulatory constraints.

See Charts

1:Dealer UST holding are at historic hights

2: Dealer holder increased while in NY FED assets

fall

{kind=link}

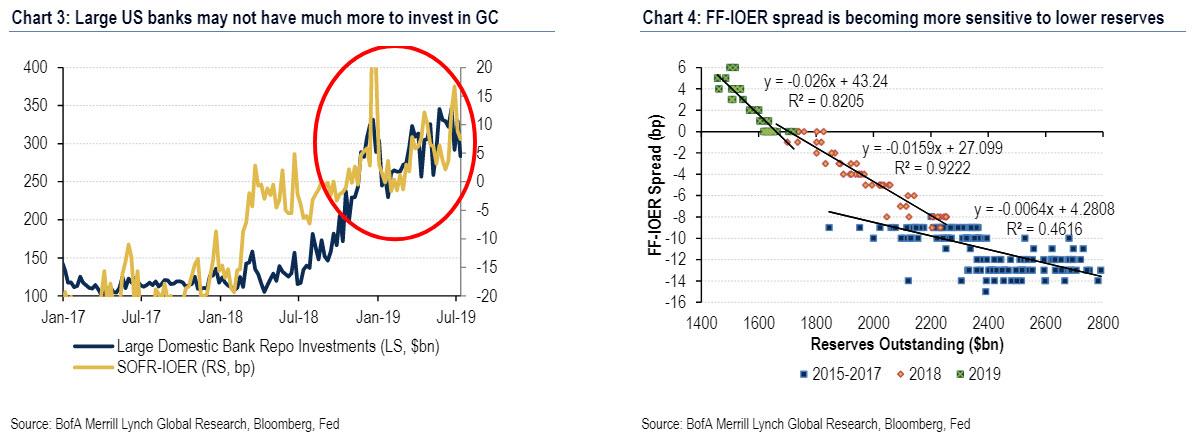

- 3. Banking system and reserve scarcity: Reverting to a topic which was especially dear during the QE ear, Bank of America notes that it is becoming increasingly concerned that the US banking system is nearing reserve scarcity. This can be seen via reluctance of large domestic banks to move out of reserves and into the closest HQLA level 1 substitute of O/N UST GC repo. Instead, large banks prefer to hold reserves as the most core component of their HQLA portfolios since reserves can be directly monetized and accessed intraday. Large domestic banks had previously been a key backstop to the O/N UST GC repo market as SOFR cheapened vs IOER; however, their GC investments have not been as sensitive to further UST cheapening (Chart 3). As such BofA is concerned that large domestic banks may not have as much ability or willingness to backstop the GC market as heavy UST supply arrives this month. This also coincides with increased sensitivity of FF to IOER at lower reserve levels (Chart 4).

- 4. Reserve manager selling: the recent sharp CNY depreciation should all else equal support Chinese UST purchases. However, the market is likely more concerned about trade tensions that slow China growth, support mainland capital outflows, and result in PBOC selling of USD to stem CNY depreciation pressures. This would result in a further decrease in Chinese UST holdings and additional Treasury cheapening.

See Charts 3 & 4:

3:

Large US Banks may no have much more to invest in GC

4: FF

IOER Spread is becaming more sensitive to lower reserves

{kind=link}

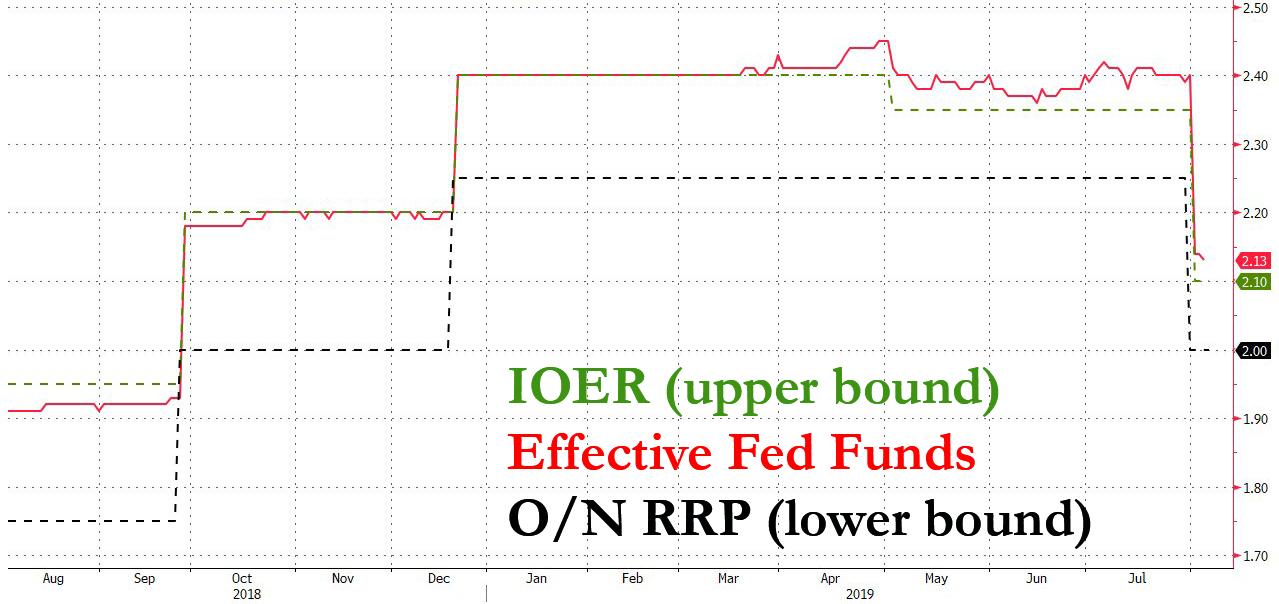

While

we hardly have to remind readers of the ongoing inversion in the Fed Funds vs

IOER rate, we can easily say that each of these factors has contributed to

heightened sensitivity of money markets in relation to changes in UST supply

and reserves, of which the FF-IOER "flip" is the most immediate

consequence.

See Chart:

{kind=link}

Of course, it will not come as

a surprise to any rates experts that there has been a clear relationship between UST supply, lower

reserve levels, and higher SOFR- and FF-IOER spreads (Chart

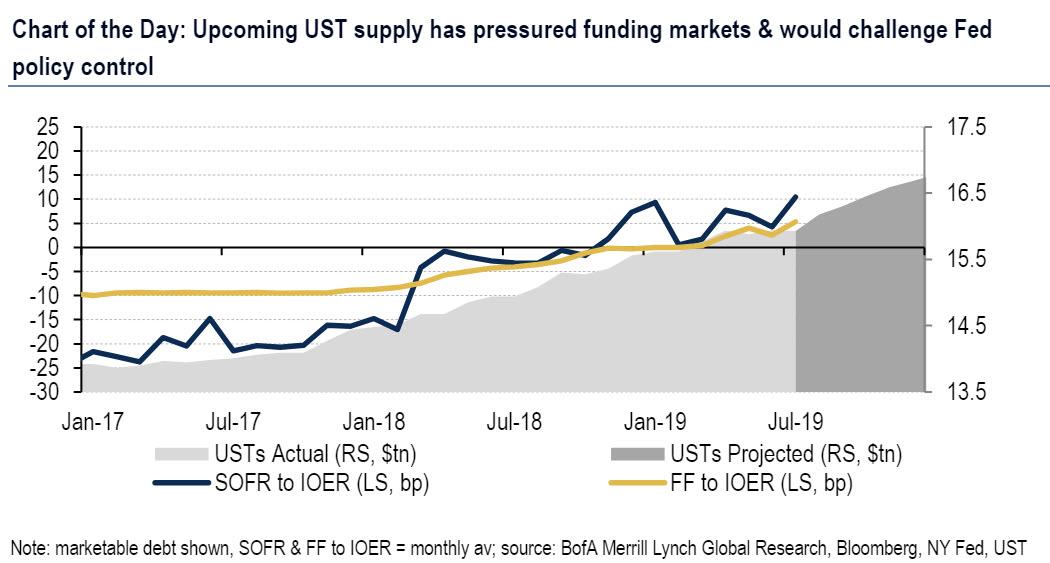

4, Chart 5, Chart 6). As a result, BofA expects even greater upward pressure on

SOFR- and FF-IOER spreads by year end. Specifically, Cabana's

best guess is that the net $750bn

of UST supply and $300bn of reserve drain by year end will place upward

pressure on SOFR-IOER of 10-15bp and FF-IOER of 5-10bp vs current levels,

substantially tightening liquidity conditions despite the end of QT.

See Chart of the day:

Upcoming

UST supply has preasur funding markets & would challeng Fed policy contrl

{kind=link}

It

could get worse: according to BofA, risks are skewed to the high side of these

estimates given the non-linearity we have recently observed in money markets.

What are the political implications?

Well, for one, doing QE while

still above the zero lower bound is guaranteed to raise concerns over Fed

independence. To wit, any Fed action that results in balance sheet expansion to

control front-end rates would likely receive the following criticisms:

- Fed indirect financing of UST fiscal deficits;

- independence of US monetary and fiscal policies; and

- US slipping toward MMT.

Of course, each of these

potential criticisms over Fed balance sheet expansion is rooted in the issue of

too much UST supply and constrained dealer balance sheets; of course, in

the case of MMT the "independent" Fed will be done away with entirely

as it starts monetizing all bond issuance, a la helicopter money. Here,

BofA struggles to see how the Fed avoids such criticisms without regulatory

changes for treatment of USTs (e.x. exempting them from SLR) or dealers (e.x.

broader FICC repo clearing across assets).

What the Fed will ultimately

choose is unclear, however in any case the upcoming wave of UST supply will

present challenges for the Fed to control its target FF rate. These challenges

largely stem from simply too much UST supply and the market's ability to

warehouse it - a challenge that will only grow in the coming years, which is why

we have been warning for much of the past year to watch out for market crashes

- these are a conveniently and easy scapegoat for the Fed returning to the old

QE regime.

For

what it's worth, Bank of America believes "the

Fed will need to step in to offset these funding market pressures through

outright balance-sheet expansion or QE, potentially in 4Q." And

while the Fed could get ahead of these issues by laying out a framework around

money market control before greater criticisms and questions emerge about the

independence of monetary/fiscal policies or the path to MMT, it won't do that,

and instead it will wait for another, even greater "Lehman-like"

crash to float the idea of imminent QE... which is precisely what Nomura

warned about earlier in the day..

….

Read the entire art at:

SOURCE: https://www.zerohedge.com/news/2019-08-06/forget-china-fed-has-much-bigger-problem-its-hands

----

----

No hay comentarios:

Publicar un comentario