ND AUG 14

19 SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

Is every thing awesome?

Since

Powell cut rates, Bonds and Bullion are up 6%, Stocks are down 6%, and the

dollar is unchanged...

See Chart:

{kind=link}

The duration of the bond is set

to be around 44 years, making it the bond with the highest duration in the euro

zone government debt market.

Ugly

day for US stocks (down broadly 3%) as stops were run yesterday and dismal data

from China and Germany sparked a big de-risking...

See Chart:

{kind=link}

And

stocks on the week...

See Chart:

{kind=link}

Today's dump occurred after a 3rd failed test of the

Fib 61.8% retrace of the July tumble.

See Chart:

{kind=link}

The Dow

closed below its 200DMA

See Chart:

{kind=link}

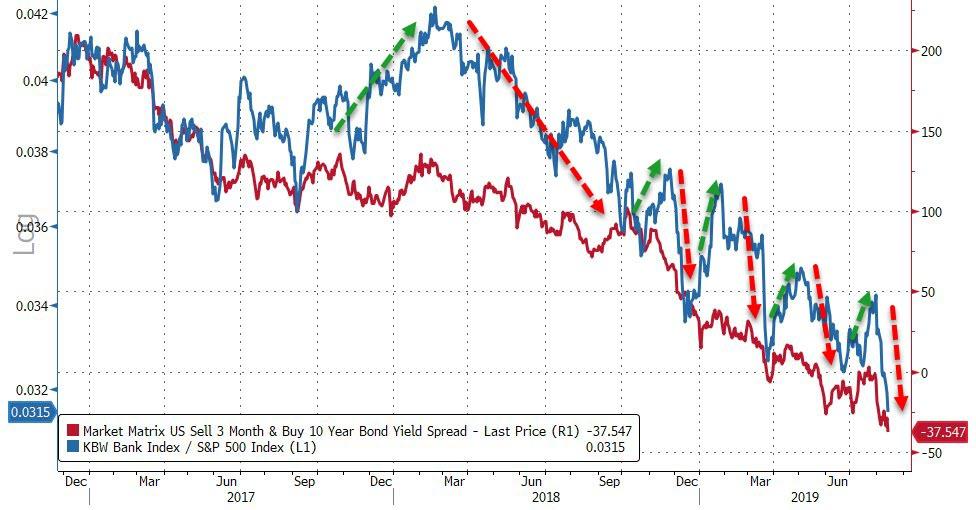

Bank stocks were battered, once

again catching down (relative to the broad market) to

the collapsing yield curve (how many more false starts in financials will

traders willing bid for)

See Chart:

{kind=link}

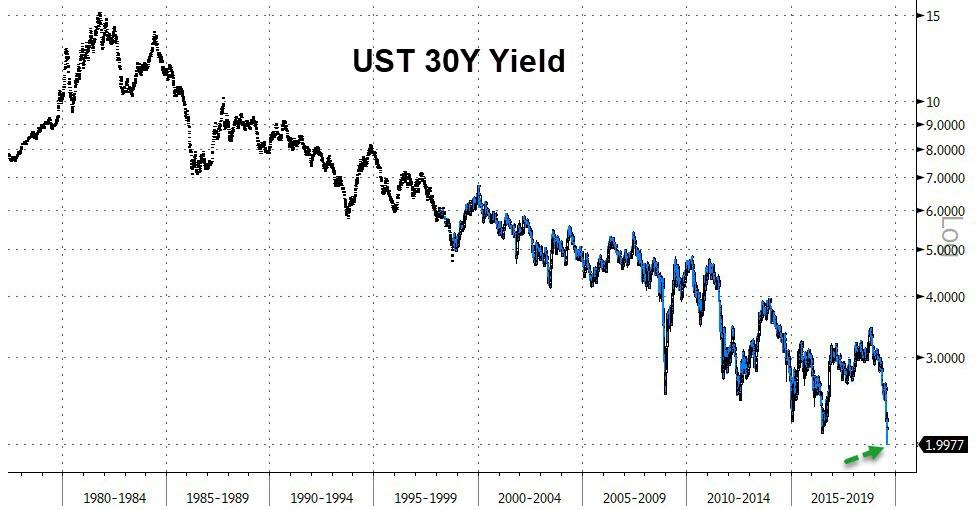

Treasury

yields collapsed today, led by the long-end (30Y -13bps, 2Y -8bps)...

See Chart:

{kind=link}

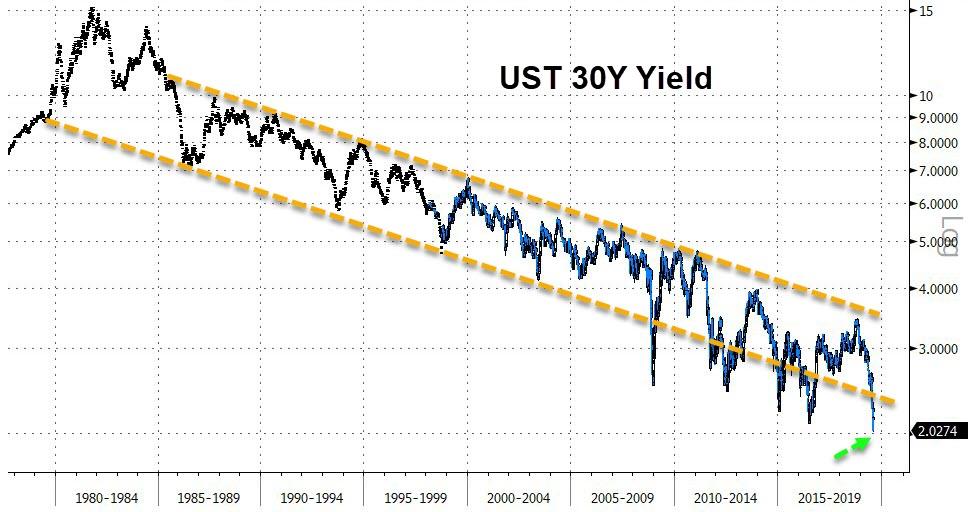

The 30Y Treasury yield tumbled to an all-time record

low today, trading as low as 2.01%...

See Chart:

{kind=link}

And the

10Y term premium tumbled to a record low...

See Chart:

{kind=link}

The

yield curve completed its inversions today with 2s10s finally crossing the zero

line...

See Chart:

{kind=link}

Negative-yielding

debt continues to soar...

See Chart:

{kind=link}

Finally, as Albert Edwards

warns:

"The

answer seems pretty obvious to me. The

bond markets are telling us that the cycle is ending with the central banks

having failed to drive core CPI inflation higher.

So Japanese-style outright deflation lies ahead

at a time when western economies have piled debt sky high."

Who could have seen that

coming?

Gold

tops stocks YTD and bonds are about to overtake the S&P too...

See Chart:

{kind=link}

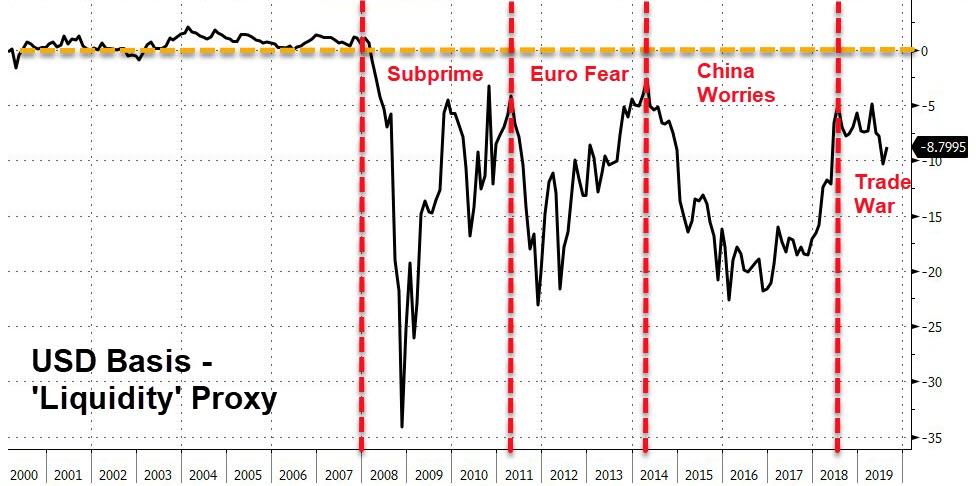

The

dollar shortage continues...

See Chart:

{kind=link}

Tremendous amounts of money pouring into

the United States. People want safety!

— Donald J. Trump

(@realDonaldTrump) August

14, 2019

….

----

----

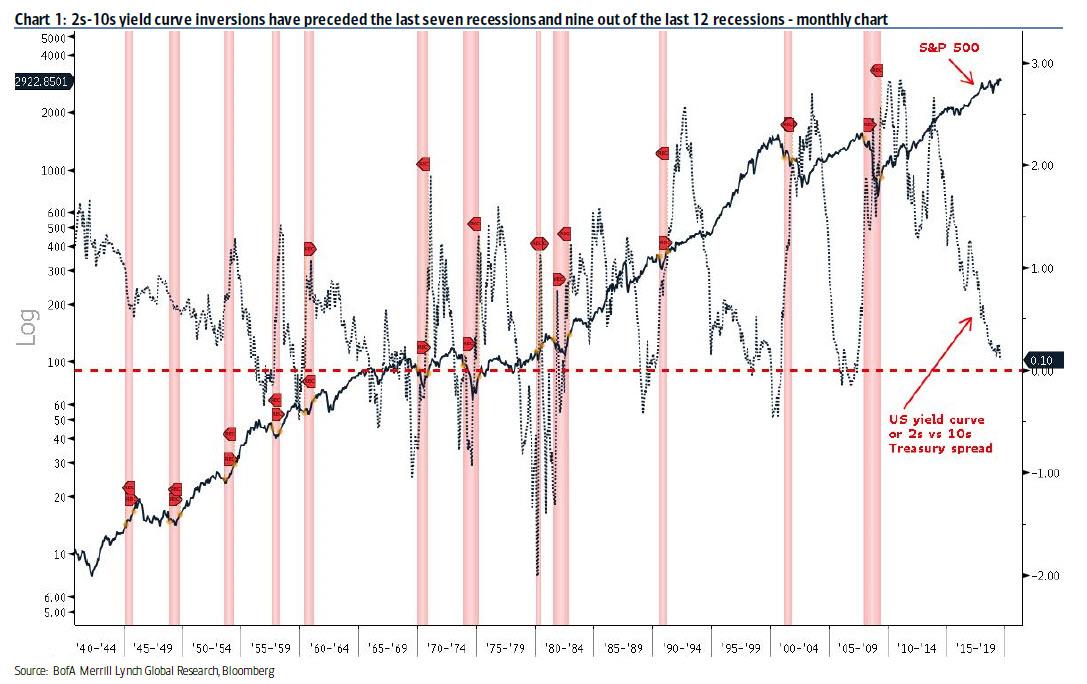

The typical

pattern is the yield curve inverts, the S&P 500 tops sometime after the

curve inverts and the US economy goes into recession six to seven months after

the S&P 500 peaks.

Because of all economic indicators, this one is without doubt the most

foreboding and ominous. Consider that 2s-10s yield curve inversions have

preceded the last seven recessions and nine out of the last 12 recessions. In

fact, as Bank of America points out, there was one yield curve inversion in the

mid 1960s that did not precede a recession and the yield curve did not invert

ahead of the three recessions between the mid 1940s and early 1950s. However, in the past 5 decades, a 2s10s inversion has been a

guaranteed signal that a recession is imminent.

See Chart:

{kind=link}

See more charts at:

….

----

----

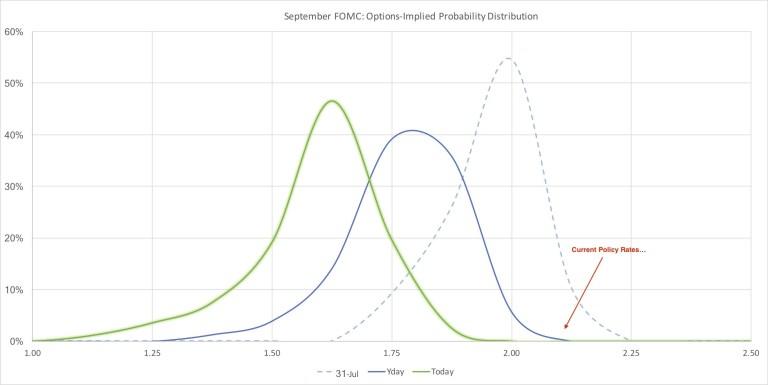

5 Things Every Trader Needs To Know About Rates

5. What’s Priced In

-50bps is now the base case for September.

{kind=link}

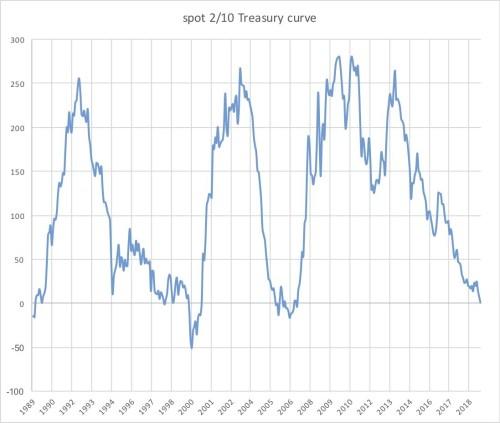

4. Curve Inversion

Read any sell-side literature & you’ll quickly find that the shape of

the curve is one of the most widely followed “recession predictors” available,

where a flat curve indicates a higher likelihood of recession. When this

flattening becomes so pronounced that the yield on the longer tenor falls below

the yield on the shorter tenor, it’s referred to as inversion – something

that’s happened only a handful of times. We’re now

sitting at the most inverted levels in the last 30 years for the spot 2s/10s

swaps curve. But, caution against extrapolating that into the meaningful

“recession predictor” that the street seems to love.

See Chart:

{kind=link}

Here’s the same curve, but in Treasury space (not swaps). This is the

curve that you’ll hear pundits hyperventilating over whenever it dips below 0

(which it did, ever so briefly, this morning).

See Charts

{kind=link}

3. Funding

The Dec 19 future associated with this spread is now

at its widest levels since early February 2018.

See Chart:

{kind=link}

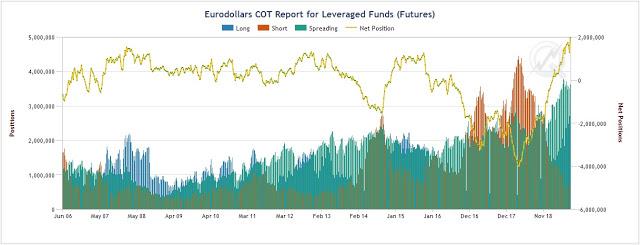

2. Positioning

Hedge funds are more long the front-end of the interest rates market

right now than at any historical point on record. Yes, rates are low – and

the largest positions in the hedge fund community are

setup to profit if they go even lower (yellow line shows net

position).

See Chart:

{kind=link}

1. Negative Rates

Negative Rates are to 2019 what Beanie Babies were to the 90s. They might

be great for price appreciation during times like these, but if you’re

expecting them to return your love in the way, say, a “positive” yielding

investment will – you’re sadly mistaken.

That all being said. Consider this for a moment. The 0% coupon German

10yr note currently yields about negative 0.70%. It hasn’t yielded more than

positive 1% since 2014. But if you’d invested a

million dollars in German 10yr bonds 6 months ago, you’d have made more in 6

months than you would make in interest on the US 10yr Treasury – from now until

2025.

Currently, we’re at -1.21%. That’s easily the lowest

since the Fed started tracking this in 1960.

See Chart:

{kind=link}

….

----

----

With

little else in place for shelter, the

US dollar served as a safe haven. It remains to be seen if this will

also be the case when the next

financial disaster happens...

President Donald Trump wants a lower US dollar. He complains

about the over-valuation of the American currency. Yet, is he right to accuse other countries of a “currency

manipulation”?

Trump is right. The American dollar is overvalued. According to the latest version of the Economist’s

“ Big

Mac Index,” for example, only three currencies rank higher than the US

dollar. Yet the main reason for this is not currency

manipulation but the fact that the US dollar serves as the main international

reserve currency.

Yet the international reserve status comes also with

the curse that the persistent trade deficits weaken the country’s industrial

base.Instead of paying

for the import of foreign goods with the export of domestic production, the

United States can simply export money.

American Supremacy

After each of the two world wars in the 20th

century, the United States emerged as the largest creditor country, while the

war had ruined the economies of the war-time enemies along with that of the

major allies. After the end of the Cold War, this pattern would experience a

repetition. The United States, so it seems, has been, since then, the only

remaining superpower.

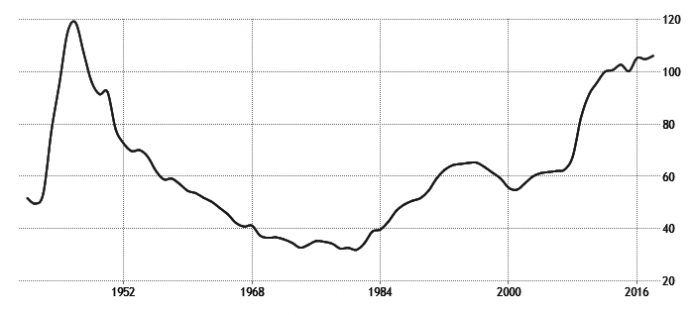

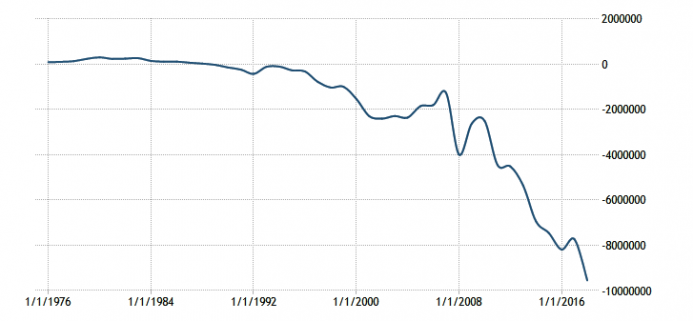

The

public debt ratio, which had been falling since the end of the war began to

turn-around in 1982 and has been rising ever since (Figure 1).

See Chart:

{kind=link}

With this debt creation came a new phase of global

expansion of the dollar. The

spread of the dollar provided the basis for the economic performance and the

military position of the United States. Yet this time, the new structure that

has emerged is outwardly powerful but inherently fragile. It is not economic

strength that provides the foundation of the role of the US dollar in the

international monetary system, but it is the US dollar's financial role that

provides the basis for the United States to maintain and extend its global

activities

While

the parallels fit insofar as the current system provides similar benefits to

the participants, the present

structure is even more flawed than the older scheme, which broke down due to

its inner contradictions.

Bretton Woods

The decoupling of the European currencies from the

dollar progressed step by step and finally led to the introduction of the euro in 1999. As of now, the euro is equal to the US dollar in the

size of its internal use, yet as a global currency, and particularly as an

international reserve currency, the US dollar still dominates majestically

(Figure 2).

See Chart:

{kind=link}

The Bretton Woods System as it was established by

the end of World War II bestowed an “exorbitant

privilege” to the United States when the dollar

became the point of reference for the international currency system following

the Bretton Woods

Accord. With the other member countries fixing their currencies

to the US dollar, and the US dollar officially fixed to gold at $35 per troy

fine ounce, it seemed as if an ideal construction was found in order to avoid

international monetary disruptions and to provide the framework for global

economic expansion.

he gold

anchor was aimed at preventing an excessive production of US dollars

by the US government. When foreign countries had a trade surplus,

they were formally allowed, according to the Bretton Woods Accord, to exchange

the excess dollars for gold from the American Treasury. With a stable parity

between dollar and gold, this would have restricted dollar creation. France took the agreement literally and demanded gold from

the United States instead of accumulating dollars as international

reserves.

Originally in the BW1 treaty, it was stipulated that

the modification of currency parities should be an exception rather than a

rule. But in the course of the 1960s, the international monetary system entered

into a phase of high instability when fixing and re-fixing of foreign

currencies to the dollar became a huge concern. The

perverse monetary system that emerged created a bonanza for currency

speculators. The candidates for exchange rate revaluation — such as Germany or Japan — were easy to identify.

In 1971, with the so-called "Smithsonian

agreement," a final attempt was made to save the old system when the

United States devalued its currency against gold and a series of other

currencies. However soon thereafter, it became obvious that there was no chance

of revival for the old regime. In 1973, with the adoption of the new rule that

each country could choose its own currency arrangement, the Bretton Woods

System was officially declared as dead.

In the 1990s, the triad of global dominance seemed

well in place for the United States: unrivalled military might, a booming and

innovative economy, and the status of undisputed issuer of the global currency. The US dollar experienced

another period of strength. Since 2002, however, the long-term trend toward a

weaker dollar is back in place, interrupted by lower

peaks of the waves of strength (see Figure 3).

SEE

Chart:

{kind=link}

The Dollar and US Foreign Policy

In the 1990s, the monetary policy of the United

States became an instrument of a grand geostrategic enterprise. The

neoconservative movement took this constellation as it emerged in the 1990s for

granted and implemented a policy that was based on a philosophy that assumed

with almost religious confidence that it was the duty and right of the United

States to be the hegemon in the 21st century. In contrast to the time after the two world wars,

however, the rest of the world outside of the United States did not lay in

ruins.

Changing of the Guard

The easy monetary policy of the United States has

accelerated the de-industrialization at home and has fostered industrialization

abroad (predominantly in China and in the rest of Southeast Asia); it has

produced a situation that stands in sharp contrast to the end of World War I

and World War II. Under the new BW2

system, the United States is no longer the largest creditor with the largest

industrial base, but instead has become the largest international debtor.

Imperial politics requires expansive monetary policy, and

the consequence of it shows up in persistently high trade deficits and a

deteriorating external investment position (Figure 4).

See Chart:

{kind=link}

Being the issuer of a global currency provides huge

benefits that come with a curse. Increased

private and public consumption possibilities come from the privilege of getting

goods from abroad without the necessity of producing an equivalent amount of

tradable export goods. While other countries have to export in order to pay for

their imports, the sovereign who emits a global

currency is exempt from adhering to the most fundamental law of economic

exchange.

History,

and in particular economic history, always shows both: common features and

differences, and indeed, the American Empire is different from some of the

former empires. Yet what the United States has in common with the former

imperial states is that at some point the military extension becomes too

complex to be handled efficiently and thus becomes too costly.

Different from the factors that justified the

expectation of a coming demise of the dollar in 2007, the American currency has

experienced a new spring due to the financial crisis of 2008. With little else in place for shelter, the US dollar served

as a safe haven. It remains to be seen if this will also be the case when the

next financial disaster happens.

….

SOURCE: https://www.zerohedge.com/news/2019-08-13/why-dollar-rules-world-and-why-its-reign-could-end

----

----

And for the first time ever, the entire UST curve is below 2.00%...

See Chart:

{kind=link}

….

See

more charts at:

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

As

attitudes toward war grow dangerously worshipful in the US, quitting our endless wars becomes all the

more difficult...

====

So far, Big Pharma has watched the

cannabis industry from the sidelines, deterred by regulatory concerns. But the

sleeping giant’s takeover is slowly intensifying as more patents, partnerships,

and sponsored clinical trials come to fruition.

====

"THANK YOU to clueless Jay Powell and the Federal

Reserve. "

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

Wishful thinking :

The new “Cold War” is here. Get used to it.

====

Throughout the history of the world, many civilizations have risen and fallen.

VIDEO:

….

----

----

“It

is important for the country to

diversify away from the US dollar. Over the long run, even

relatively small-scale gold purchases add up and help to meet this objective.”

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

- Bolton

Accuses Russia of Stealing US Tech, Gets Tough on China, Gives Flaccid Support

to Venezuela

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

Ecua: 40

años entre "democracia" y desengaños JJ. Paz-y-Miño Cepeda

Huawei: América

Látina y trumpismo (II) Carlos

Jenkins

====

ALAI ORG:

====

RT EN ESPAÑOL

- "Que primero trabajen humanamente con Hong Kong": Trump afirma que China quiere llegar a un acuerdo comercial

- Economía argentina en pausa electoral: entre el 'terrorismo financiero' y el afán de calmar a los mercados

- Maduro acusa al expresidente colombiano Álvaro Uribe de orquestar un plan para asesinarlo

- El primer ministro pakistaní promete dar "una lección a la India"

- "Un paso en falso causaría una explosión": Bolton insta a China a tener cuidado con sus acciones respecto a Hong Kong

- China podría lanzar criptomoneda y serviría como impulso para otras

- México insiste en que la matanza de El Paso es un acto terrorista

- Keiser Report "La línea de resistencia oro-dólar caerá al igual que la Linea Maginot durante la Segunda Guerra Mundial"

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political

crisis: neofascism & internal conflicts that favor WW3

-US, UK Hong Kong Hypocrisy By Finian Cunningham

-China And the Zombies Of The Past By Christopher Black

-How Tehran fits into Russia-China strategy By Pepe Escobar

-The Epstein Mystery By Paul Craig Robert

-Epstein, Faction, and Neopatrimonialism By Dan Corjescu

----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

John W.

Whitehead We’re

All Enemies of the State

Kollibri

t-S The

Case Against Voting for President

Elliot

Sperber The

New Mayor of New York

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

----

PRESS

TV

Resume of Global News described

by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario