EASY TO UNDERTAND US ECON ISSUES

LA

ECON USA ES FACIL DE ENTENDERSE

Con

paciencia y saliva un elefante de comió una hormiga. Aqui es al revés.

Si

te quieres comer el elefante Econ-US,

don’t worry about the 1st chart.

Interesting truth at the end…& beautiful lessons at all

….

"...now, because the outcomes are already

bad, they’re wanting to drive interest rates even lower to deal with the

bad outcomes that these low interest rates have already caused..."

Trump & Powell

Square Off

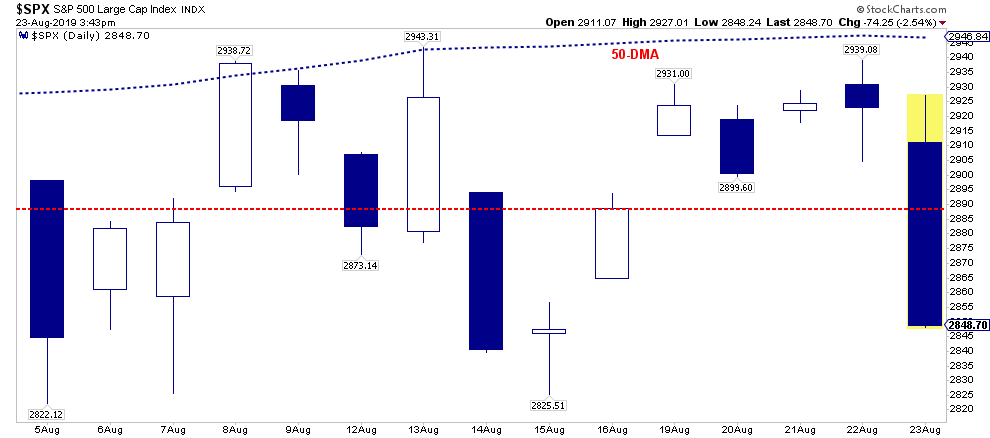

Let’s start with a simple chart:

$SPX S&P 500

Large Cap Index vs. 50 DMA

{kind=link}

This has been an impossible market

to effectively trade as rhetoric between the White House, the Fed, and China,

has reached a fevered pitch.

[ If you are new in Econ start your Reading here:]

On Friday, several things happened which have at least

temporarily significantly heightened market risk.

Jerome Powell disappointed the markets, and the White House,

by sticking with their previous guidance concerning monetary policy actions. To wit:

- We Will Act As Appropriate To Sustain The Expansion (Will cut rates if needed)

- Says Events Since The July Fomc Have Been `Eventful’ (Trade War/Tariffs)

- Carefully Watching Development For Impact On U.S. (China/US Trade)

- Monetary Policy Has No Rulebook For International Trade

- We’ve Seen Further Evidence Of A Global Slowdown (Germany in recession)

- Fitting Trade Policy Into Risk-Management Framework Is a New Challenge

- Fed Faces Heightened Risk of Difficult-to-Escape Periods of Near-Zero Rates (Neg. rates)

- U.S. Economy Has Continued to Perform Well Overall (No rush to cut rates)

- Sees Financial Stability Risks as Moderate, but Will Remain Vigilant

However, this commentary was not a surprise to us. We

have suggested

for several months the Fed should be slow to use what little ammo they

currently have.

“With the markets pushing record highs, recent employment and regional

manufacturing surveys showing improvement, and retail sales rebounding, it certainly

suggests the Fed should remain patient on cutting rates for now at least until more data becomes available. Patience would also seem logical given the

limited room to lower rates before returning to the ‘zero bound.’”

Not surprisingly, Chairman Powell’s comments did not sit

well with President Trump who has frequently pressed the Fed to cut rates

aggressively.

“After Powell’s closely

watched speech in Jackson Hole, Trump tweeted, ‘As After China announced more

import tariffs on U.S. goods early Friday, Trump said he would respond Friday

afternoon. The president

also asked ‘who is our bigger enemy,’ Powell or Chinese President Xi Jinping.” – MarketWatch

By the end of the day on Friday both the U.S. and China had

hiked tariffs on one another.

“China said it would increase

existing tariffs by 5% to 10% on more than

5,000 U.S. products, including soybeans, oil, and aircraft. A 25% duty on

American-made cars would also be reinstituted. The value of these products is

estimated by the Chinese Commerce Ministry to total around $75 billion.

Trump responded after financial markets closed by saying he would raise

current U.S. tariffs. A 10% duty on $300 billion in

Chinese goods will be raised to 15% in September while a 25% tariff on $250

billion in imports would be increased to 30% in October.” – MarketWatch

The

Investing Conundrum

The problem with managing money is that markets are now

trading on “tweets,” and “headlines,” more

than fundamentals. This makes being either long, or short, particularly

difficult.

This is

where we are currently.

Over the past few months we have reiterated the importance

of holding higher levels of cash, being long fixed income, and shifting risk

exposures to more defensive positions. That strategy has continued to work

well.

- With the trade war ramping up, there is little reason to take on additional risk at the current time as our holdings in bonds, precious metals, utilities, staples, and real estate continue to do the heavy lifting.

See Chart:

IVV Shares Core S&P500 ETF NYSE

{kind=link}

If you are

being advised to hold all these asset classes for “diversification” reasons,

you should be asking yourself, “why?”

Trade wars, and tariffs, are not friendly to these markets.

With those “taxes” being ramped up by both parties, things will

get worse, before they get better.

Risk management is critically

important to long-term returns, and risk is becoming more elevated

daily. So, if you are

paying for a “buy and hold” portfolio, you may want to

reconsider what you are paying for?

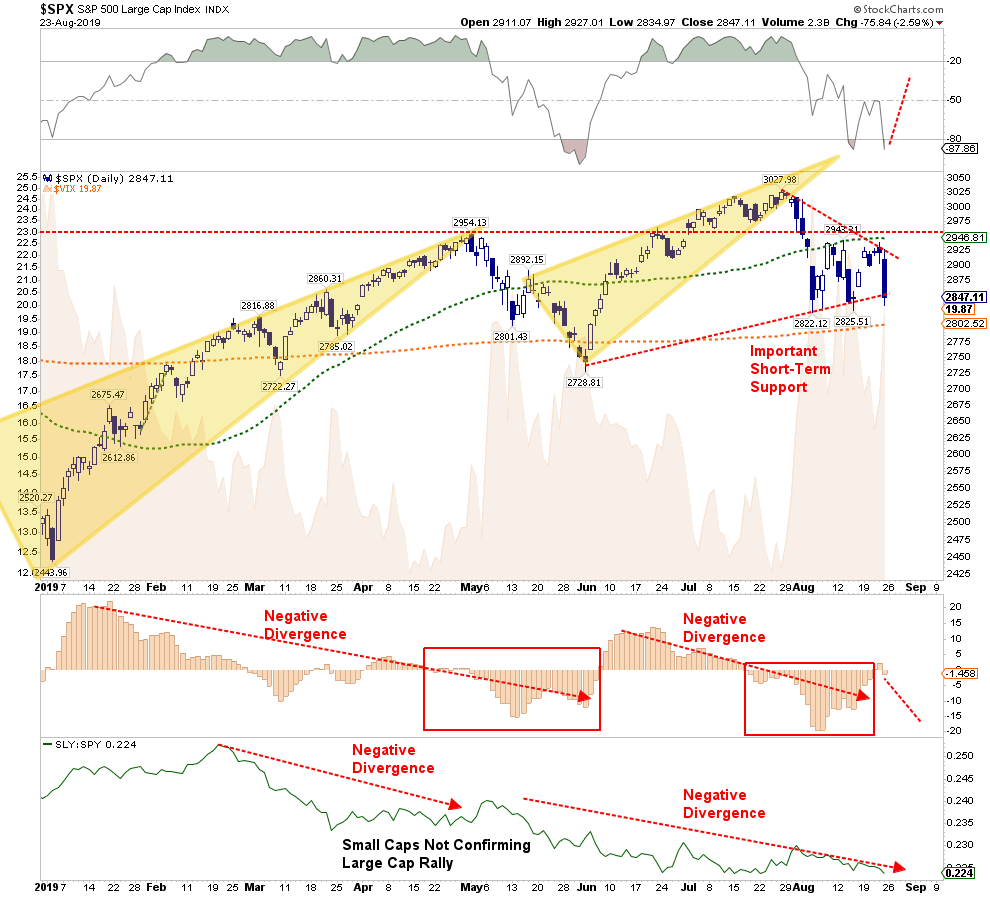

From a technical perspective, the market is back to

oversold, so a bounce next week is possible, but as noted last week, this is “still

a sellable rally.” However, if the

market breaks the current consolidation to the downside, a test of the 200-dma

will be critically important. Any failure at that support will bring the

December lows back into focus.

See Charts:

{kind=link}

As we have continued to note over the last few weeks, the

ongoing deterioration of small and mid-capitalization companies continues to

suggest the overall backdrop of the markets is not healthy.

Negative

Yields Everywhere

As I noted last week in “Pavlov’s

Dogs & The Ringing Of The Bell:”

“The ‘ringing of the bell’ over the last decade has trained

investors to rush into equity-related risk.”

With Powell disappointing traders, and Trump retaliating

with additional tariffs, the initial response was to flee to “safety,” or

rather should I say ”

bonds.”

While retail investors continue to cling onto stocks hoping

for a resurgence of the “bull

market,” institutions are piling into bonds

as the tidal wave of data continues to warn something is “broken.”

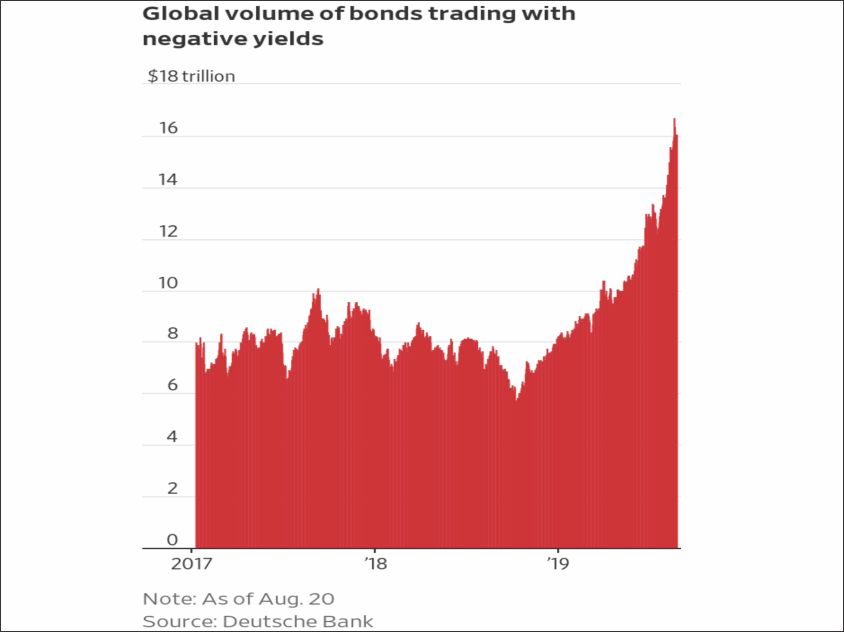

(You

don’t have $17 Trillion in negative-yielding sovereign debt if there is

economic and fiscal stability.)

See Chart

Global

Volume of Bonds Trading with Negative Yields

{kind=link}

The message that negative yields are sending coincides with

weaker growth rates in:

- Corporate profits

- Employment

- CapEx

- Personal Consumption Expenditures

- Real Retail Sales

- GDP

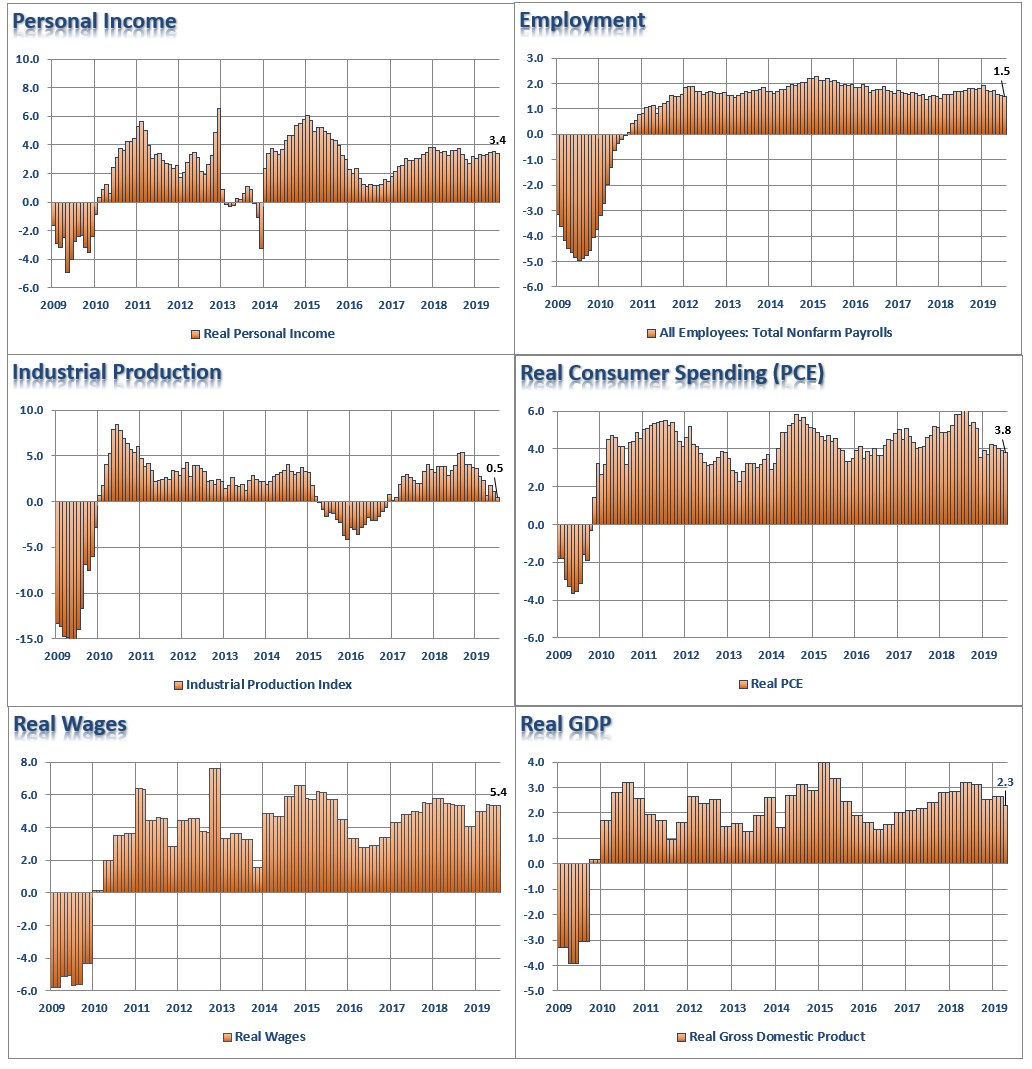

You can see this visually in the

6-panel chart from last

week’s missive

See Charts:

Personal Income, Employmt, Industrial Produc., Real Consumer Expend, Real

Wages, Real GDP

{kind=link}

Yes, the

data is not negative which is why we aren’t in a recession…yet, (However, the data is subject to substantial

negative revisions, and as we showed last week, the month before

the last recession started all the data was positive as well.)

This is

also the reason the Fed stopped hiking rates.

Since that is a lot of “Fed speak,” let me translate:

“Listen, as a member of the Fed, I can’t tell you the economy has weakened significantly, and

the threat of a recession has risen markedly. If I did say that, the

market would crash, consumer confidence would crash, and we would immediately

be in a recession.

The reality is that we needed to get rates off

of zero percent, and we were hoping to get rates closer to 4%, to give us some

room to support the economy during the next recession. Unfortunately, we actually ‘over tightened’

which led to the market disruption last year. The rate

cut in July was to be supportive of the economy short-term, but we need to hold as much ‘ammo’ as

possible in reserve for when the recession hits.”

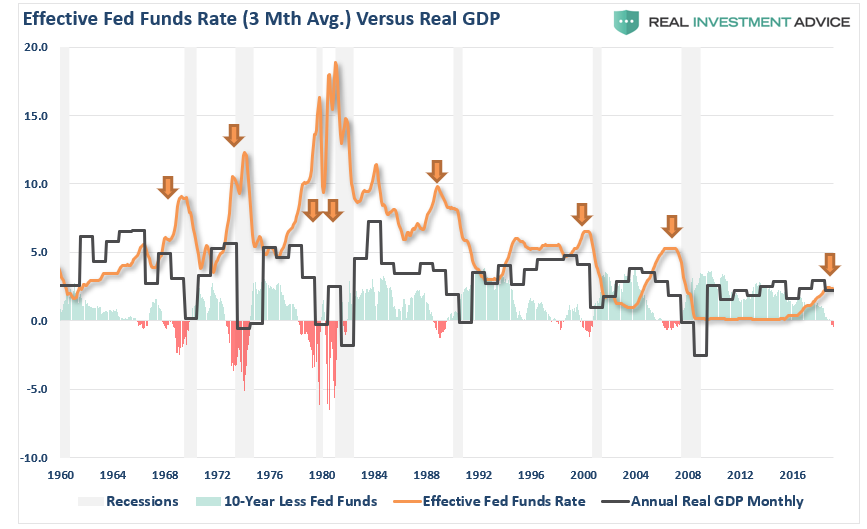

Here is a chart of the Effective Fed

Funds Rate versus the Neutral Rate (Real

GDP):

See Chart:

{kind=link}

Why The

Fed Won’t Go Negative?

They won’t go “negative” on rates.

Daniel

LaCalle summed

it up well:

“The paper ignores the collapse in net income

margin and ROE and even dismisses ROTE (return on tangible equity) to try to defend the idea that banks earnings have not

suffered from negative rates.

The worrying part is that these statements

ignore the fact that one of the main reasons why banks’ bottom line has not

fallen more is they have almost stopped making provisions on bad loans.“

His point is

critically important.

Negative rates have irreparably damaged

European banks, which only can be resolved through a massive debt revulsion.

Wolf

Richter also had some

excellent points in this regard:

“Negative interest rates drive banks to chase

yield to make some kind of profit. So they do things that are way too risky and

come with inadequate returns. For example, to get some return, banks buy

Collateralized Loan Obligations backed by corporate junk-rated leveraged loans.

In other words, they load up on speculative financial risks. And as this drags

on, banks get more precarious and unstable.

This is not a secret. The ECB and the Bank of

Japan and even the Swiss National Bank have admitted that negative interest

rates weaken banks. The ECB has even been talking about a strategy to

‘mitigate’ the destructive effects its policies have on the banks.

So that’s the issue with negative interest

rates and banks. They crush banks.”

Don’t forget.

Why did

the Fed launch Q.E., and cut rates to zero, to begin with?

To bail out the member banks of the Federal Reserve, or should I just say, “Wall Street.”

Interest rates are a function of economic growth. Globally, despite massive levels of QE, and low interest

rates, economic growth is

faltering, not strengthening.

The Fed does understand this.

Unfortunately, the Fed is still misdiagnosing what ails the

economy, and monetary policy is unlikely to change the outcome in the U.S.,

just as it failed in Japan. The reason is simple. You can’t cure a debt problem with more debt.

Therefore, monetary interventions, and government spending, does not create

organic, sustainable, economic growth.

If rates

ever do rise, it’s game over as borrowing costs surge, deficits balloon,

housing falls, revenues weaken, and consumer demand wanes. It is the worst thing that can happen to an slow

growing economy that is dependent of further debt expansion just to sustain

current growth.

As Wolf noted, lower rates are

not the solution, they are the problem.

“So far, the outcomes are already bad, and

now, because the outcomes are already bad, they’re wanting to drive interest

rates even lower to deal with the bad outcomes that these low interest rates

have already caused.”

….

Read the full article at:

----

----

No hay comentarios:

Publicar un comentario