ND

AUG 18 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

Economists don’t understand bonds. But they know just enough of

them to understand that they had

better change the subject...

Should anyone ask

if QE was effective, Bernanke (and Yellen) would always answer with “TERM PREMIUMS.” Not recovery, accelerating growth, or

robust inflation. Just Term

premiums!

Why?

Because these are just complicated enough so that no one really

understands what anyone referring to them might be talking about. ..SO, ‘Term premiums’ was “The perfect

getaway setup”.

The thing about

term premiums is really two things; first, forgetting

the fact that they are a ridiculous made up idea so that Economists can try

(and fail) to plug interest rates into econometric

models (in the few cases they do), simulations

already suggest term premiums have fallen more without QE than with it. Even

on its own terms, term premiums fail to live up.

Bernanke

in 2015 conceded

that point:

What about the decline in longer-term yields since early 2014? In the

US at least, that decline is somewhat surprising, as economic fundamentals have

recently seemed more consistent with rising, not falling, longer-term

yields… By the process

of elimination, with fundamentals stable

or improving, much of the decline in yields over the

past year must reflect a sharp drop in term premiums. [emphasis added]

What did he blame solely term premiums?

The reason it has to be term premiums is because Bernanke, Janet Yellen, or Jay Powell ALL SAY

INFLATION IS GOING TO RISE AND SO WILL SHORT-TERM INTEREST

RATES. GUARANTEED. TAKE IT TO THE BANK. The Fed will therefore be hiking short-term

rates and since they don’t believe the bond market would ever, ever disagree

with them, process of elimination, it therefore must be term premiums that

are causing yields to fall (when these same people say they should be rising).

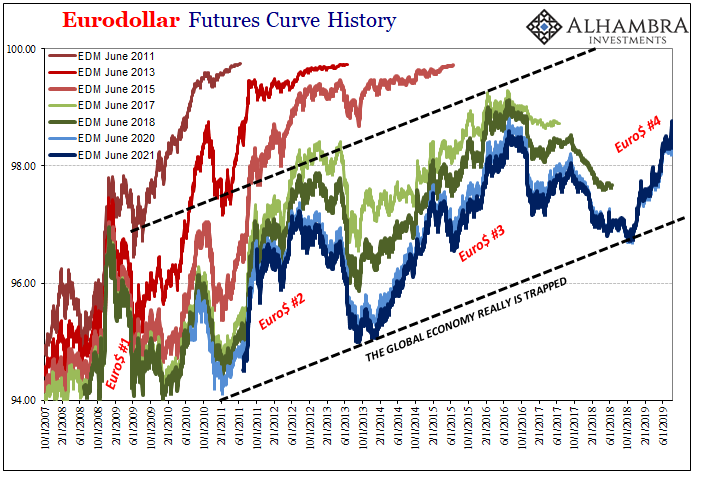

See Chart:

Eurodollar:

Futures Curve history

{kind=link}

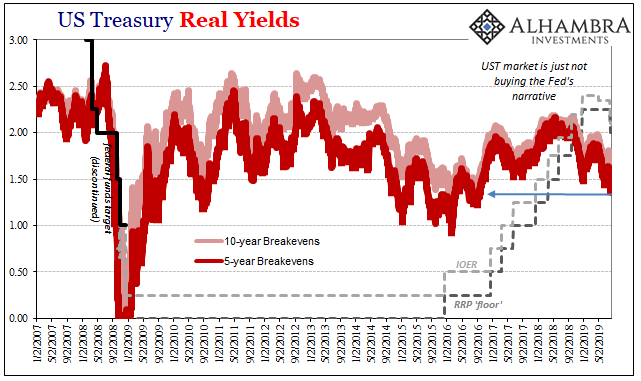

US

Treasyry; Real Yields:

She chart

https://www.zerohedge.com/s3/files/inline-images/SABOOK-Aug-2019-Swaps-TIPS-Longer.png?itok=jh-t5c-Q

{kind=link}

Whether in 2015 or

more recently, the market evidence for the other two pieces of the yield

picture are pretty unequivocal. The market is obviously

expecting a very different set of circumstances than policymakers, an

increasingly dangerous scenario OF LOWER INFLATION, not higher, at the same time it is thinking lower

short-term rates, not rate hikes.

It actually isn’t

all that difficult to challenge the assertion, especially with market prices in

hand. And it’s becoming even more of a necessity now

that people are (finally) paying attention to the yield curve.

This week Janet Yellen said:

I would be relying on the yield curve as the

best signal of that risk given the yield curve has obviously not got the same

sort of structure that it’s had historically.

Term

premiums are not science nor really math. They

are made up and more than that they are rationalizations, truly Orwellian,

intended to deny the obvious and straightforward signals coming from the

very fundamental building blocks of all finance and economy. The entire notion

is purposefully shrouded in unnecessarily complex concepts whose only true use

is to attempt to answer for the otherwise inexcusable.

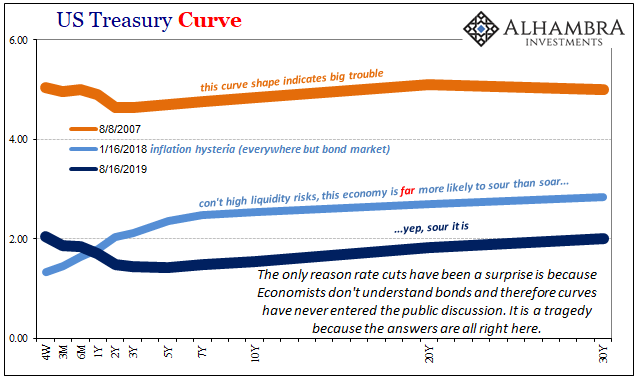

SEE Charts:

US TREASURY CURVE 1

{kind=link}

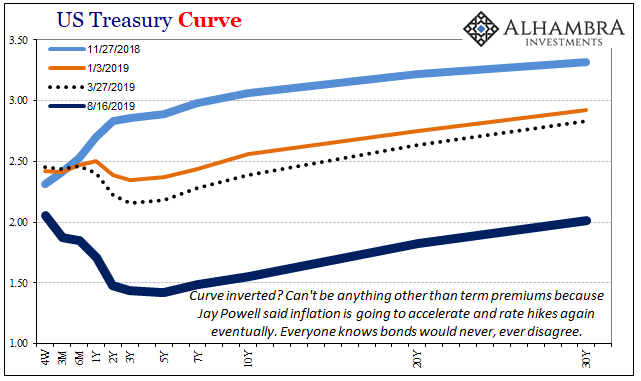

And chart:

US TREASYRY CURVE 2

{kind=link}

As I often write, Economists don’t understand bonds. But they

know just enough to understand that they had better change the subject.

….

----

----

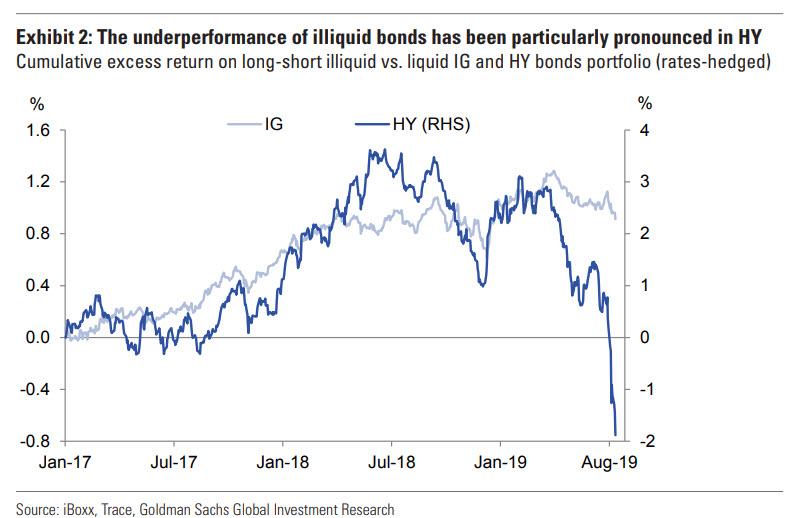

The spread

differential between illiquid and liquid bonds, has been drifting wider in both

the IG and HY markets, reaching its highest level in two years

See Chart:

The underperformance of illiquid

bonds has been pronounced in NY

{kind=link}

The liquid bonds outperformed by 2%

over the past two weeks.

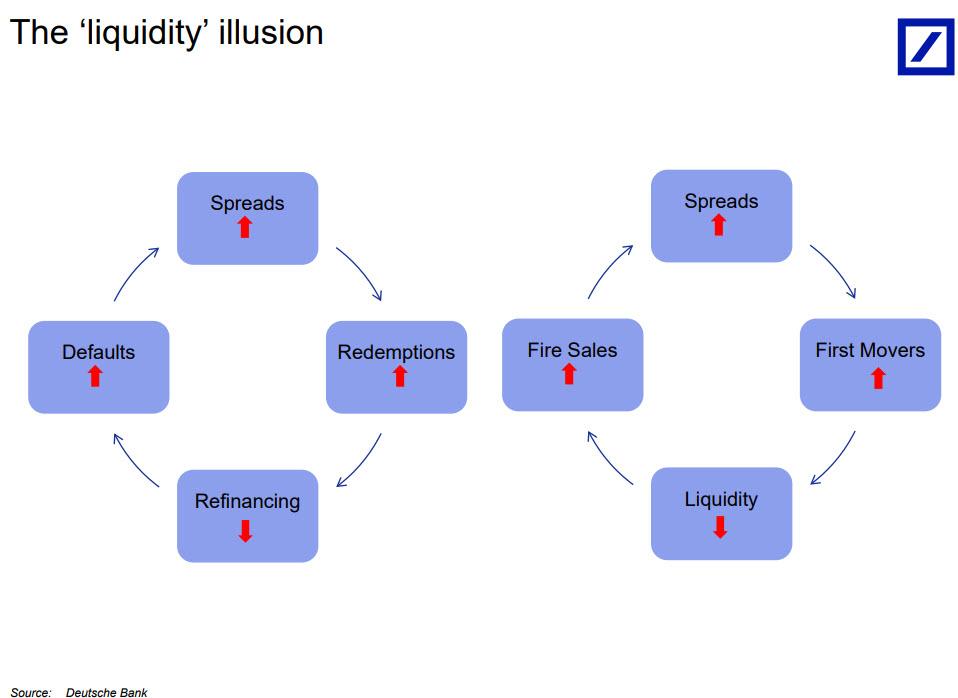

As with the relative value of high

vs. low price bonds, Goldman thinks the risk-reward in being long

illiquid bonds remains poor despite the new highs made by the illiquidity

premium, especially when considering

recent market repricing events of illiquid securities such as those of

Woodford, H2) Asset Management, GAM and so on.

See Graphic:

The Liquidity Illusion

{kind=link}

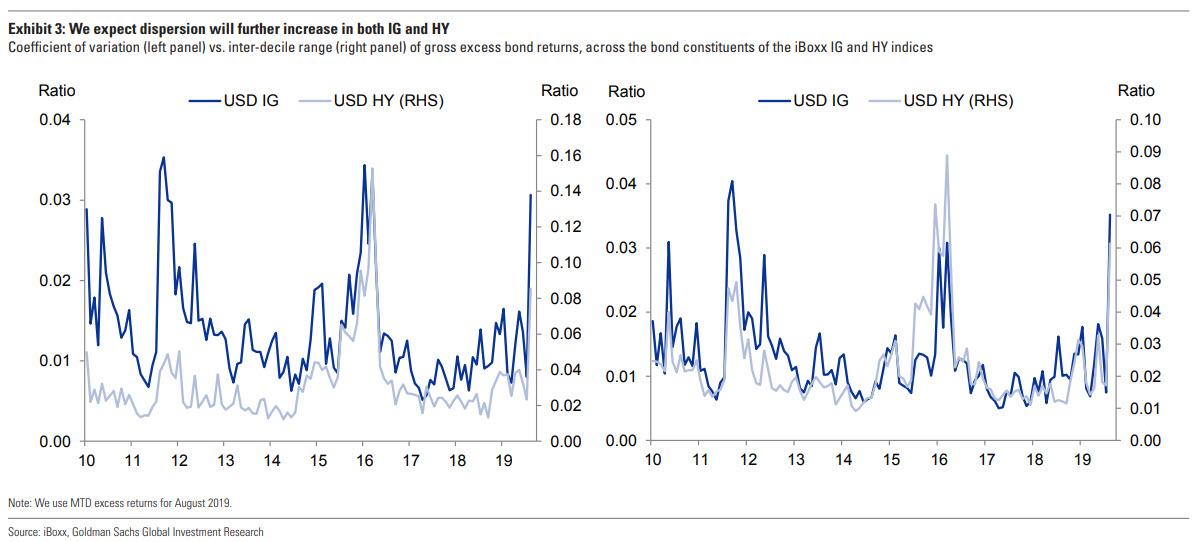

Of course, if the market is finally starting to correctly

account for an illiquidity premium, one will expect a violent bond dispersion

in both IG and HY, and that is precisely what is happening because as the chart below shows,

dispersion is surging from rock-bottom levels, with Goldman warning to

"brace for a new regime."

See Charts:

We expect dispersion will further increase in

both IG and HY

{kind=link}

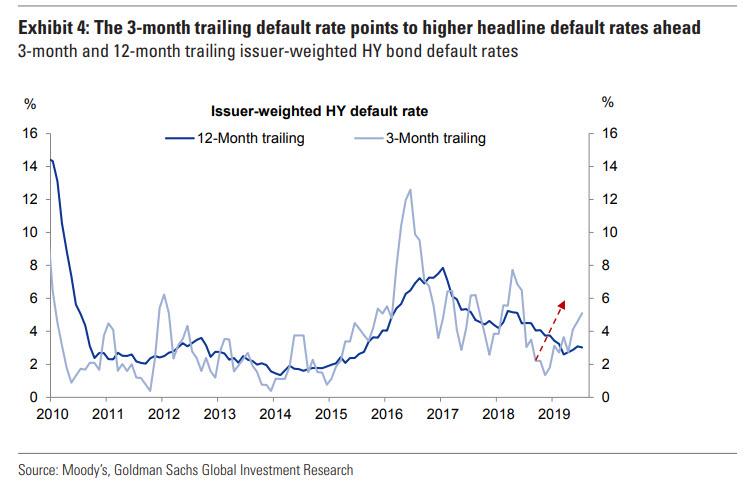

Goldman writes, "headlines

about bankruptcies and restructuring plans have recently intensified. And while

the 12-month trailing issuer-weighted default rate remains at a benign level,

higher frequency indicators show a notable acceleration in the pace of

defaults. This is illustrated in Exhibit 4,

which shows that the 12-month issuer-weighted default rate stands at 3%. The

3-month trailing HY default rate (annualized) now stands above 5% and has been

steadily rising since bottoming out at 1.3% in November 2018."

See Exhibit 4

The 3-month trailing default rate

points to higher point headline default rate ahead

{kind=link}

What may come as a surprise to most is that on a dollar

basis, 2019 has been a banner year

for default volumes with over $36 billion notional of defaulted bonds year to

date, which is on

track to surpass the $43 billion in 2016 as the highest year for notional

default volumes in the post-crisis era (Exhibit

5).

See Chart:

On

a dollar basis, 2019 is on track to surpass the 2016 post crisis default

peak

{kind=link}

In short a default tide has already

appeared, however thus far, defaults have been highly concentrated among

Energy issuers, a trend that reflects structural

as opposed to cyclical challenges. The lingering

weakness in oil prices coupled with weak growth sentiment may push issuers

in other structurally-challenged sectors towards

defaults.

….

----

----

RELATED

"For these producers, the

game clock has run out of time to keep playing 'kick the can' with

their creditors and other stakeholders."

====

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

La

violencia de los pedofilos va de la mano con las guerras del terrorism imperial

Bombing

Serbia was a family affair in the Clinton White House: “I urged him to bomb,” Hillary told an interviewer.

====

Ahora reconocen que el chantaje ‘tarifas’ agrava la Ec USA y las

pastergan: Ridículo

"The

inventory glut reflects a continued cooling of the US auto market."

----

La real historia es que se publicó esto “China

prepares its nuclear option in Trade-war” Lealo: https://rt.com/business/4667-china-nuc

. Un tit for tat destinado a agravar la crisis interna del US.. una

respuesta económica a la ingerencia política del US en Hong Kong. China es la

horma del zapato US.

====

In addition to being money for thousands of years, the price of gold is primarily a measure of

faith in central banks. If you believe central banks have everything

under control, don't buy gold...

….

Si los billonarios no creen en central Banks,

por que tendrían que creer en ellos los inversores medios del sector

productivo. El empresario pequeño que maneja la economía de la ciudad tampoco

cree en central Banks y cuando llegue la REV se aliaran con el mediano

empresario para crean Banco Propio.

….

See

Chart:

Gold vs. Fe

en Central Banks

{kind=link}

….

----

----

...automation is going to accelerate and jobs in Walmart nation are going to continue to disappear at

an exponential rate...

====

"They

pointed to three key advantages for Trump: He’s the incumbent, the U.S. economy

is strong and the Democrats have no definitive front-runner to challenge

him."

----

Point 1:

many incumbents have been defeated. P.2: it is totally false that the Economy is strong. P.3: Elizabeth Warren is ahead in electoral polls

today. In short:

A. foreign diplomats are paid to support

trump. B. One thing is right today more than

ever: 'PEOPLE DON'T WANT TO BE STUPID TWICE'

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

This reckoning with

Beijing’s authority was baked into

the cake 22 years ago when the Union Jack came down over Government

House...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

RT EN ESPAÑOL

- El petrolero iraní Grace 1 zarpa desde Gibraltar pese a la demanda de incautación de EE.UU.

- España ofrece "el puerto más cercano" al barco de rescate Open Arms tras su negativa a desembarcar en Algeciras

- Trump reconoce estar "estratégicamente" interesado en Groenlandia

- Comandante de la Guardia Revolucionaria: "EE.UU. ha acumulado todo su poder en el campo de batalla con Irán"

- Una estadounidense pierde la custodia de su hija en Arabia Saudita por ser demasiado occidental

- US: Una gasolinera desata un caos vehicular luego de ofrecer el litro de combustible a 10 centavos de dólar

- Rusia y Venezuela consolidan sus vínculos militares durante una visita de Padrino López a Moscú

- Keiser Report "Hoy tenemos un sistema global de regresión infinita"

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

PRESS TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario