HICKMAN UNCOVER TRUMP’ MYTH ‘THE ECONOMY IS STRONG’

THE US ECONOMY IS IN THE PATH TO RECESSION

Hugo Adan 08/19/19

Here only extracts. Read

the full article :

WRITTEN BY ERIC HICKMAN,

president of Kessler

Investment Advisors

Published by Tyler Durden at:

…

The bull market in U.S. Treasury bonds is in full swing and there is plenty more return to be made...

…..

Why? Simply because we don’t have control on our destiny.. much less on

World Economics & Politics.. Our nuke power made it worse: Imp vs. colonias

The bull market in U.S. Treasury bonds is in full swing and there is

plenty more return to be made. Yields have fallen

dramatically, generating significant capital

gains for Treasury bond holders. The chart below shows when those articles were published and the path of U.S.

Treasury yields before and after:

See Chart:

US Treasury Yields

{kind=link}

A refresh

of the “recession era 4” concept

Three recessions have occurred in the U.S. over the last 30

years – the longest period in which there is rich financial and economic data.

Each of these periods show a similar pattern of interest rates (see chart

below).

Look at the approach to the

orange-boxed recession eras. Then if you look at the left-side of the

orange-boxed areas, all three rates converge to roughly the same place (the

yield curve gets flat or inverted), the Fed then stops raising and term rates

(the 2-year and 30-year) begin to fall in anticipation of a slowdown in the

economy. The Fed then starts cutting rates and the 2-year falls more than the

30-year (i.e., the yield curve steepens). The recession

then starts a little after the Fed starts cutting rates. The recession ends and

term rates continue to fall for years after. With minor variations, this is

what happens each time.

See Chart:

{kind=link}

We are going through “recession era

4.” The housing market peaked in December 2017, the yield curve (10-year

yield minus 3-month bill) inverted in March of this year, industrial production

peaked in December 2018, the expansion in the U.S. is now the longest in U.S.

history and the Fed has now begun to cut rates. The Fed will talk about how its

July 31 cut was a “mid-cycle adjustment,” but that mention was a nod to the two

“no-cut” dissenters (George and Rosengren) to not make a

determination about the future (i.e. retain a neutral bias).

In fact, be prepared for the

“risk-on” community and national policy-makers (read the Trump

administration and Federal Reserve) to present reasons why a recession isn’t coming.

PEOPLE OFTEN PREDICT WHAT THEY NEED TO

HAPPEN, NOT WHAT WILL HAPPEN.

To those who ask me, “Is the U.S.

going to go through a recession in the near term?” I say OF COURSE IT IS…..the

arguments against it are just from those desperate for it not to happen, not from careful analysis. Some are waiting to spot

the primary driver that will define this recession (like the S&L crisis in

the early 1990s, the dot-com crash in 2000-01 or the subprime crisis in 2008),

but this will be defined in arrears. Don’t make the

mistake of waiting to see a tidy .. ”why” before accepting that

a recession is coming. Consider some of the common protests against a

recession:

COMMON PROTESTS AGAINST A RECESSION:

- An eventual trade deal with China will remove the problem. The global economy was slowing well before the trade war started. It is certainly an exacerbating factor, but it going away will not avoid a recession.

- The economy looks good. The parts of the economy that are still good – the labor market and consumer spending – are expected to still be strong at this point in the cycle. Leading indicators are still in the process of making cyclical peaks. This suggests that labor will only weaken after that process has occurred. Counter-intuitively, the unemployment rate is always the lowest at the start of recessions. Waiting to see full “proof” of the recession will be too late.

- The Fed will lower rates and prevent a recession. It is often misperceived, but the Fed mitigates a business cycle, it doesn’t prevent one. The economic forces in a recession (the actions of hundreds of millions of people, even billions) are so much larger than what the Fed can respond with.

- The stock market has remained near its high. In the last recession era (2007-2011), the stock market (S&P 500) peaked after the first rate cut. Don’t wait for confirmation from the stock market. It will fall dramatically but marches to the beat of its own drummer.

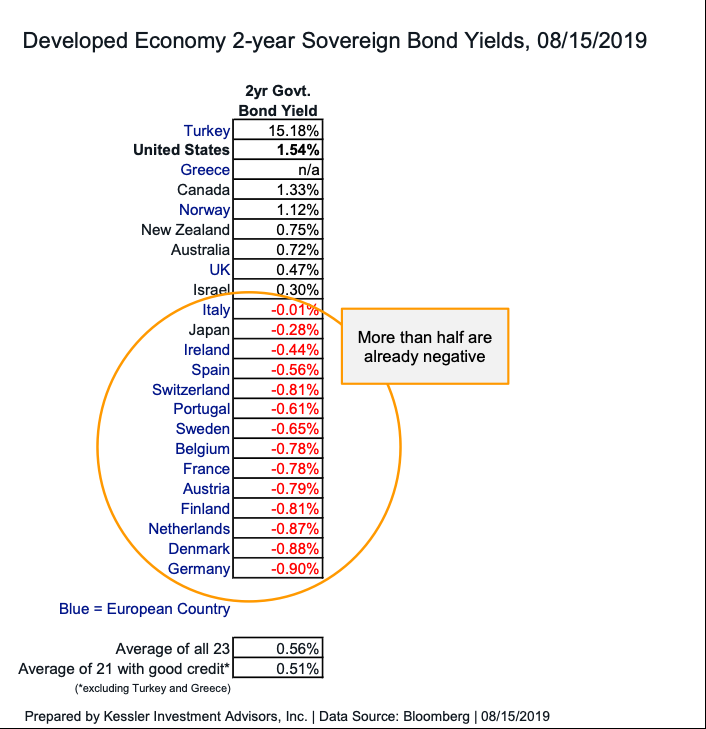

The Fed will cut rates to 0%-0.25%,

just like in 2008. The 2-year yield will fall to its 2011 low of 0.16%

or below and the 10-year yield will fall below 1%. Also,

a globally synchronized recession could easily push the 2-year yield into

negative territory, providing additional capital appreciation. More than half (56%) of global developed economy 2-year sovereign

bonds are already trading with a negative yield (see below).

See Table:

Developed Economy 2-year Sovereign Bond Yields, 08/15/19

{kind=link}

RECESSION

ERAS DISSECTED

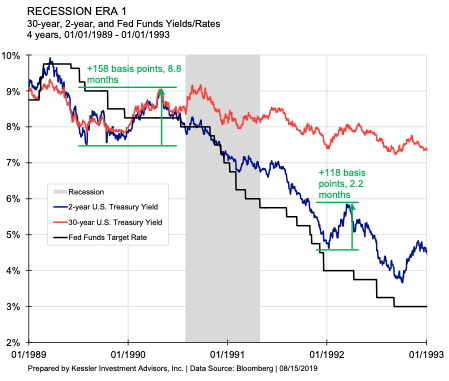

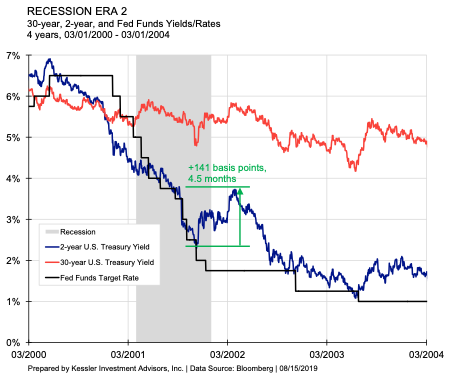

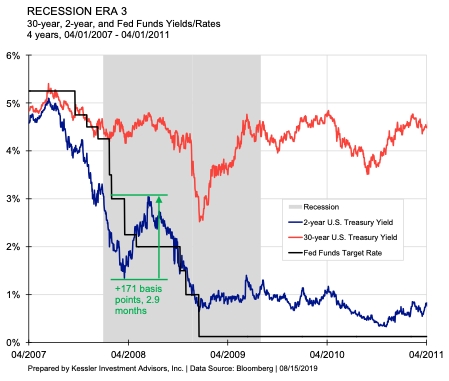

It is useful to deconstruct the long-term chart of yields

above into individual charts for each recession era. Each chart has a four-year

span. There are several things to notice about them:

- The 2-year yield drops much more than the 30-year (this is why we use leverage at Kessler; explained here).

- The recession occurs in the middle of 2-year yields falling (not at the beginning or the end.)

- Each recession-era takes three to four years.

- The 2-year yield has one or two major backups (> 2 months) during the process.

See Charts:

RECESSION ERA 1:

{kind=link}

RECESSION

ERA 2:

{kind=link}

RECESSION

ERA 3:

{kind=link}

RECESSION

ERA 4:

{kind=link}

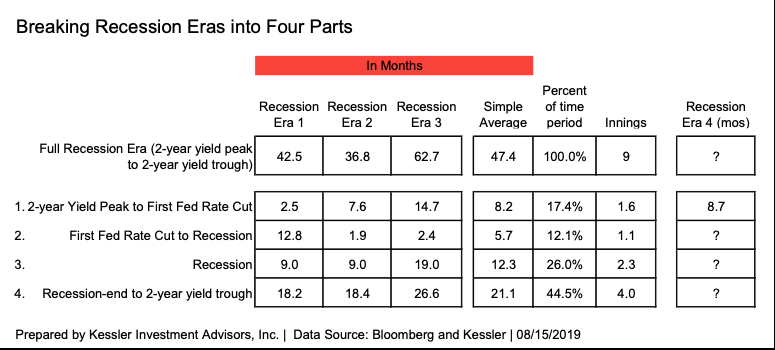

Taking the statistics from these past recession eras, similarities emerge. And because it is baseball season, why

not break it down into nine innings (see below):

See Table:

Breaking Recession Eras into 4 parts

{kind=link}

These averages can be generalized into a rough expectation

of how this cycle will evolve (see below.) The averages have dispersion – it isn’t that they hold

the answer to exactly how this cycle will evolve; THEY SHOULD SERVE AS A BASELINE FROM WHERE

NEW THINKING/MODIFICATIONS SHOULD START – not from scratch, as

if everything is new.

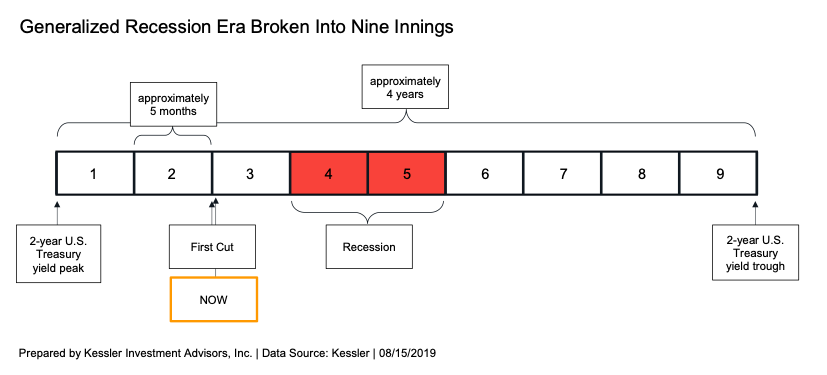

See Table:

Generalized Recession Era broken

into Nine Innings

{kind=link}

The first Fed rate cut (three weeks ago) indicates the start

of the third inning. This concept rings true in the sense that recession

conditions are not present yet. The recession will likely arrive sometime this fall/winter, not to be

officially confirmed until a year or so later by the National Bureau of

Economic Research (NBER).

U.S. Treasury yields have a strong historical basis that is

often missed. It is tempting to think that everything is new and unique every

time. But it is more challenging to accept that there are historical norms that

explain the medium-term Treasury yield trend. “Recession

era 4” is following this playbook quite well. As more and more pieces of the

puzzle fit into the mold, it gives increasing assurance that this is the right

model to use in this economic climate.

….

----

----

No hay comentarios:

Publicar un comentario