ND AUG 7

19 SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

A manic day in stocks and bonds

today with an early collapse panic-bid back to unchanged as precious metals soar

and commodities crash.

The extreme vol prompted a

warning from Guy Haselmann, chief executive officer of FETI Group LLC and

Scotia-bank’s former head of capital market strategy, who

said global markets are moving

closer to a Minsky moment,

or a sudden collapse of asset prices. FETI is a Summit, New Jersey-based company that

works with portfolio managers.

“An extended period

of low volatility like we have seen in recent

years significantly increases leverage and risk-seeking

behavior,” he said in an interview.

“When volatility turns like it has, people often need to sell

assets to meet margin calls. That’s what makes this so combustible”

"Just one more waffer-thin quantitative easing...?" What

could go wrong?

A

weaker than expected (though fractionally stronger than 7) Fix by the PBOC

unleashed hell globally once again overnight...

See Chart:

CNY Fix

vs. Offshore Yuan

{kind=link}

But,

thanks to rate-cuts from New

Zealand, Thailand, and India combined with Chicago Fed President Evans comments

suggesting more easing and QE4EVA prompted some

PPT-sponsored panic-bids in US equities.

"...you

could take the view that the risks now have gone up, and as we think we’re

going to get closer to the zero lower bound with higher probability, that would

also call for more accommodation."

Nevertheless, investor sentiment has

collapsed from euphoric greed just a month ago to "extreme fear" ...

See Chart:

FED and

Greed Index

What

emotion is driving the market now? [The market doesn’t exist, we’ve

speculat +]

{kind=link}

In the

US, markets were mixed with Nasdaq best as desperate panic bids appeared to

lift stocks back to unch (and to top the farce off a super-spike at the close)...

See Chart:

{kind=link}

VIX was

smashed back to a 19 handle...

See Chart:

{kind=link}

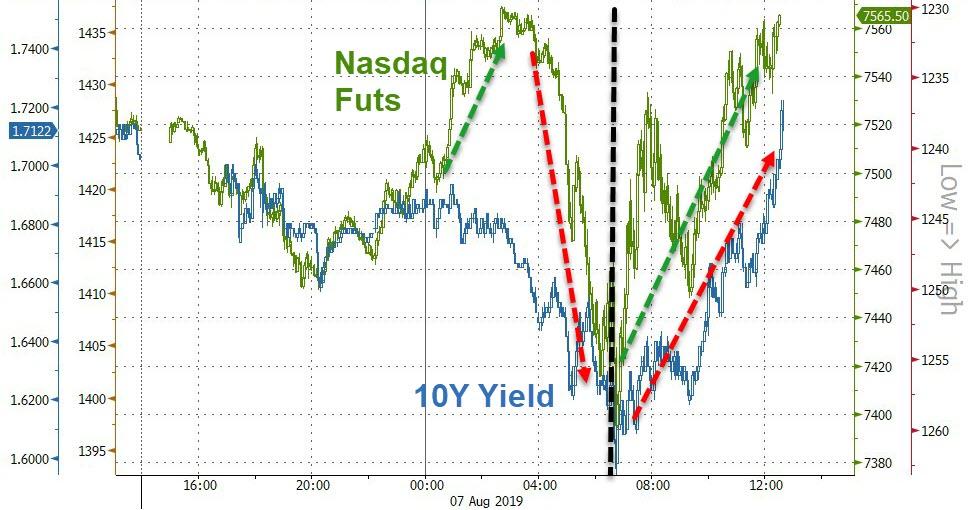

Stocks

and bonds decoupled overnight, with stocks tumbling back to bonds reality, but

then the US cash open sparked stock-buying, bond-selling all day...

See Chart:

Nasdaq

Futs vs. 10Y Yield

{kind=link}

Treasury

yields tumbled again overnight but ramped back higher after Europe

closed...ending the day practically unchanged

See Chart:

{kind=link}

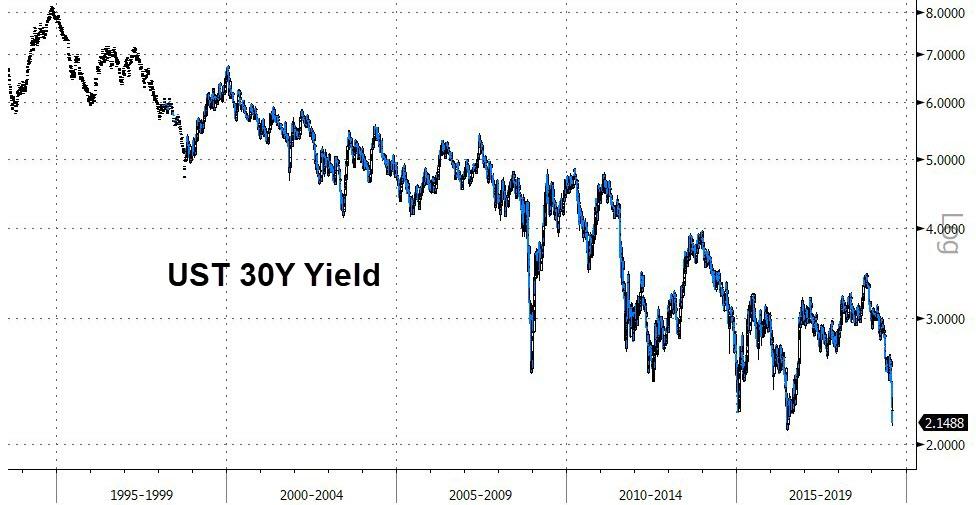

30Y

Yield plunged to near record lows...

See Chart:

{kind=link}

The

Dollar roundtripped like everything else to end unch...

{kind=link}

Gold

surged to new six-year highs...

See Chart:

{kind=link}

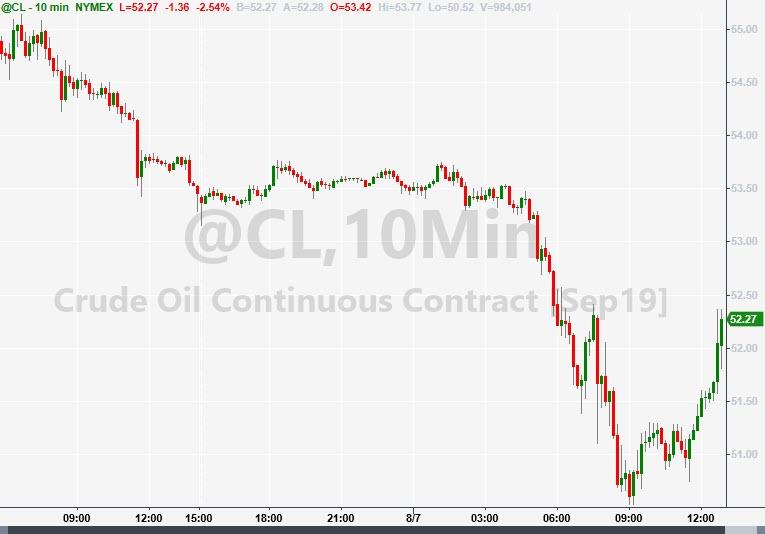

Oil prices collapsed, crude

build sent WTI prices back to a $51 handle...BUT then late in the day, Saudis

takes to halt oil price drop back above $52..

See Chart:

{kind=link}

Finally,

with $15 trillion (and rising tonight) in negative-vielding debt, bullion and

bitcoin appear the preferred safe haven against policy-maker panic...

See Chart:

{kind=link}

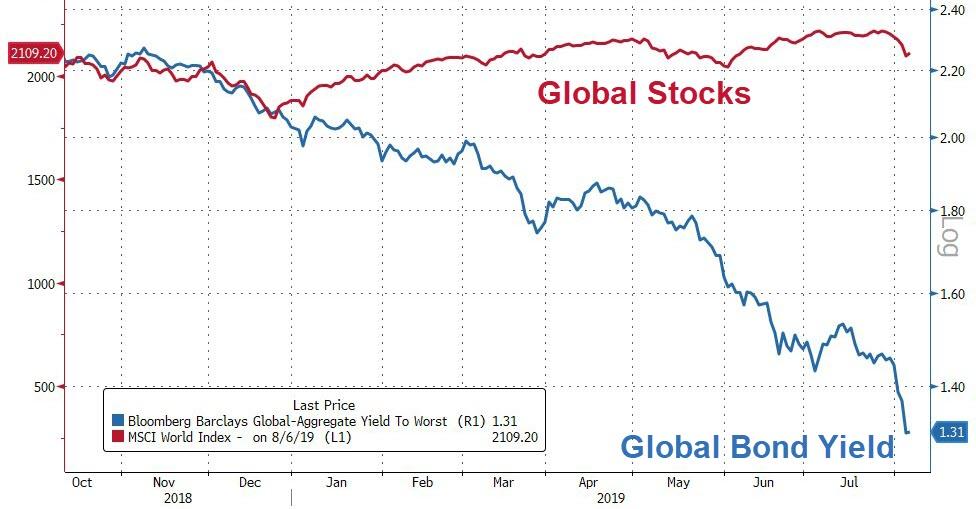

Still,

global bonds and stocks remain massively decoupled...

See Chart:

{kind=link}

So can

you guess who will be right in the end?

….

SOURCE:

https://www.zerohedge.com/news/2019-08-07/bonds-gold-surge-stocks-purge-fear-reaches-2019-extremes

----

----

Even speculators wants to avoid

the funeral of US Econ..But rethorically

Financial markets are raising risks

of recession. Equities continue to slide and volatility has spiked, but the

alarm bell is loudest in rates markets, where the yield curve inverted the most

since just before the start of the financial crisis.

Financial

markets are raising risks of recession. Equities continue to slide and

volatility has spiked, but the alarm bell is loudest in rates markets, where

the yield curve inverted the most since just before the start of the financial

crisis.

Not all

indicators are as bearish as the yield curve, however. While equities

have sold off rapidly since last week, the sell-off late last year was much

larger only to recover just as rapidly.

Within the economic data, the

near-term indicators are even less downbeat than the lower

frequency signals coming from the low unemployment rate and recent decline in

the profit margin.

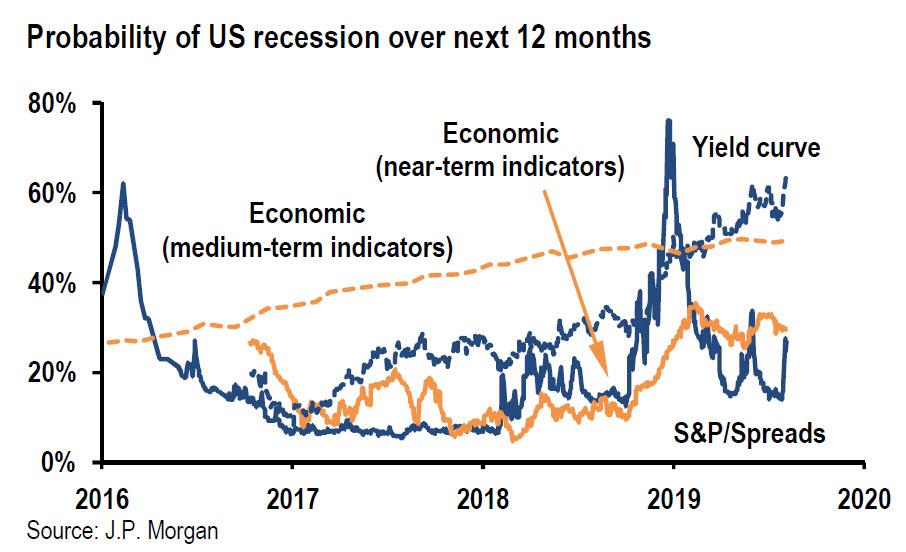

Bottom

line, we stick with our macro

indicators and see the odds of US (and global) recession in the coming 12

months closer to 40% (the average of our near-term and medium-term

indicators).

See

Chart:

Probability of US recession

over next 12 months

{kind=link}

At the same time, we continue

to flag downside risk to our modal growth outlook as the latest data and likely

hit to sentiment from the recent trade war escalation and financial market

moves suggest global growth running below our forecast

of 2.5% in 2H19.

….

----

----

More and more Americans are getting themselves into so much

debt that it becomes impossible to

pay back their loans. In the month of July,

there was a 5% increase in the

number of bankruptcies filed in the United States.

In a “booming” economy, this is

worrisome. Far too many Americans are spending way too much more than they make. There

were 452,797 filings in the first seven months of 2019, up from 450,568 during

the same period last year. There were roughly 1,000

more consumer bankruptcies at this point this year, compared to the same point

last year, the organization added. This rise in bankruptcies is coming

off a ten year low.

Southern states seem to be affected the most as well, according

to Market Watch. Alabama had the highest per capita rate, with

5.61 filings per 1,000 people, followed by Tennessee (5.39) and Georgia (4.31),

Mississippi (4.25) and Nevada (3.79).

Samuel Gerdano, ABI’s executive

director, said:

According to a

new survey

from Bankrate of about 3,000 Americans, 23% of people who were

adults when the recession started in December 2007 say they are now financially worse off than

they were before the recession hit. That

percentage amounts to just under 50 million Americans. Another 25% say they are

doing the “same.” In all, just over half believe their “overall finances” are

better than before.

“Americans were and continue to be in a degree

of denial of the financial crisis and Great Recession,” said Mark Hamrick, Bankrate’s senior

economic analyst according

to a report by Yahoo Finance. “One of the constant themes

that presents itself

in the data is that Americans are still digging out in many ways from that

experience.”

“While some have

managed to prosper in the decade since, there are still tens of millions who are struggling to

even get back to where they were before the economy took a turn for the worse,”

added Hamrick. Could that mean that the economy is not all that robust? We

certainly think so. But speaking

the truth is a revolutionary act in times of deceit.

Not only are 25% of Americans worse off than they

were before the Great Recession, but many others are also using credit to

buy essentials,

such as food. Millions more

people are buying essential goods and services on credit. Consumers had $14

trillion in household debt (and rising) in the first quarter of

2019, according to the Federal Reserve Bank of New York data. That is up from

approximately $13 trillion in debt consumers held back in 2008.

….

----

----

"If the US escalates the tariff fight further (i.e. 25% tariffs on

the remaining $300bn of Chinese imports) or takes other additional measures

against China, it would not be inconceivable for USD-CNY to rise to 7.50

or 7.70."

The French bank's EM strategist

Jason Daw, is correct there is much more pain to come for the emergers, and

especially the yuan, which after sliding below 7.00 for the first time ever

this week, is now expected to plummet as low as 7.70, a level which would

certainly prompt currency war retaliation from the Trump administration.

As Daw writes overnight, the US

and China are increasingly engaged in an entrenched tit-for-tat escalation

phase, and as he correctly predicts "one of the two sides probably need to reach their pain limit before there

is a chance of a de-escalation phase."

Meanwhile, "the Chinese

authorities can deploy their formidable defenses to stop or slow the

depreciation", as they may want to see the impact

on capital flows before permitting another leg higher. However, as the

SocGen strategist cautions, the upside risks to USD-CNY have intensified and he

now forecasts USD-CNY modestly higher than our previous forecasts (to 7.10, 7.15, 7.20, 7.25) over the next four

quarters.

Worse, if the US escalates the

tariff fight further (i.e.

25% tariffs on the remaining $300bn of Chinese imports) or takes

other additional measures against China, "it would not be inconceivable for USD-CNY to

rise to 7.50 or 7.70."

If Daw is right, the trade is

simple: buy either the USDCNH or the USDCNH +12 month forward outright, which

as of today is pricing in that the Offshore Yuan will

only drop to just 7.1335 in 12 months time.

See Chart

CNH 12

Months forward Outright

{kind=link}

That said, even the bearish FX

strategist concedes that it is important to remember that the Chinese authorities have strong policy tools and it is

likely that CNY will only weaken as much and as quickly as they want it

to. In other words, if China really wants

to devalue its currency, it can, and will do so with relish. The

question is what Trump will do to provoke such a devaluation.

….

----

----

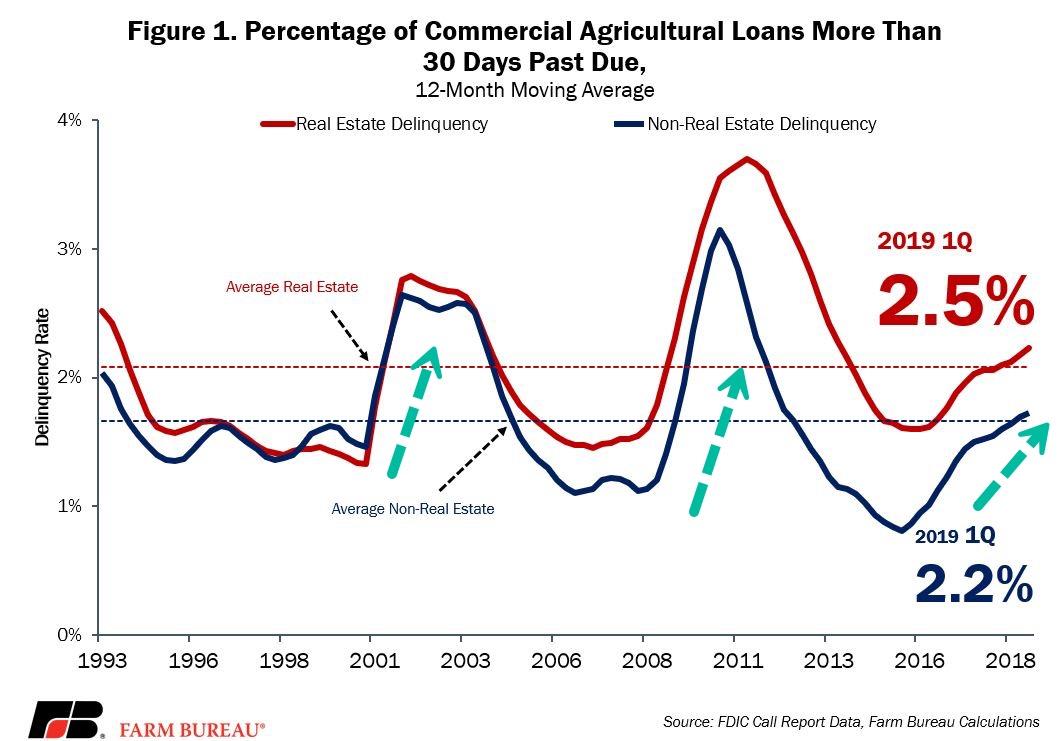

Government is preparing for a farm

crisis; this

time, it could be worse than the 1980s.

President Trump on Tuesday

morning hinted at

what appears to be yet another farm bailout (the third one must be the charm), as farm bankruptcies soar

and agricultural debt loads become unbearable.

A farm crisis on par to what

was observed in the early 1980s could be coming, especially since the US Senate

passed a bill late last week that makes it more accessible for farmers with larger debt loads to file for bankruptcy

protection, reported

Reuters.

See Chart:

% of

Commercial Agricultural Loans more than 30 days past due

{kind=link}

Republicans

and the Trump administration are preparing for Farmageddon with

new interventionist measures that will hopefully cushion farmers from

retaliatory tariffs by China.

See Chart:

Shrinking

Soy

{kind=link}

Reuters

notes that not everyone is excited about the change. The American

Bankers Association told lawmakers to oppose the bill and warned "credit

terms would tighten considerably for many family farms, with a disproportionate

impact on the most distressed farms most in need of credit," according to

a memo sent to House lawmakers on July 25.

A Reuters investigation of the

Federal Deposit Insurance Corporation showed that major

Wall Street banks are now winding down risky lending to farmers as farm incomes

decline and delinquency rates soar.

Government is preparing for a farm crisis; this time, it could be worse

than the 1980s.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

Why not? It’s not yours.

….

Are Banks free to do

whatever they want? IF so, take out your

USD now. Put it in safer inside your house or family house. Or by gold coins or kriptos

====

The

significance of the spike is difficult to overstate...

There are moments of inflection in the market when the phrase 'prices

have changed more than the facts' becomes particularly apropos and today's

Treasury rally ostensibly qualifies. We'll caution here

however that the devolving macro narrative is very consistent with with

such a repricing.

The overnight round of Asian central bank cuts combined with the weakest

yearly change in German industrial production since 2009 are symptoms of

changing expectations rather than the root cause of the move. Nonetheless,

10-year German yields dipped as low as -0.613% to a fresh record low. The selloff in domestic equities offers echoes of Q4 2018,

with the primary difference being the Fed just cut rates versus the December

hike-too-far.

Our primary concern linked to the sharp selloff in

stocks is a spike in equity vol that tightens financial conditions to rapidly

price in the Fed's series of three quarter-point-eases…

See Chart:

Financial conditions vs. Market- implied Fed rate

change

{kind=link}

An inter-meeting ease isn't on our radar; although

the futures market shows the August contract trading with an implied rate of

2.115% -- 1.5 bp of easing (or a 6% chance of a quarter-point emergency move).

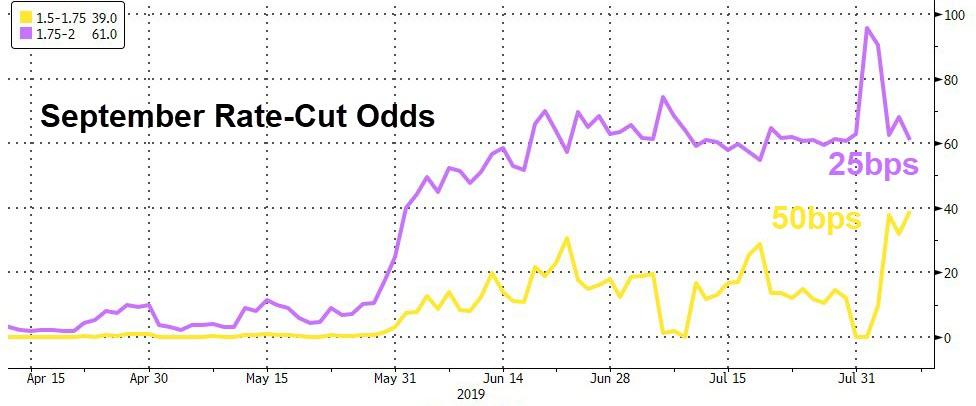

What is even more compelling are the odds of a 50 bp cut in September

jumped >50% -- 54% depending on how one slices it or 38.5 bp net easing. To say the Fed's fine tuning ambitions just became a lot more

complicated would be an understatement.

See Chart:

Sept Rate- Cut Odds

{kind=link}

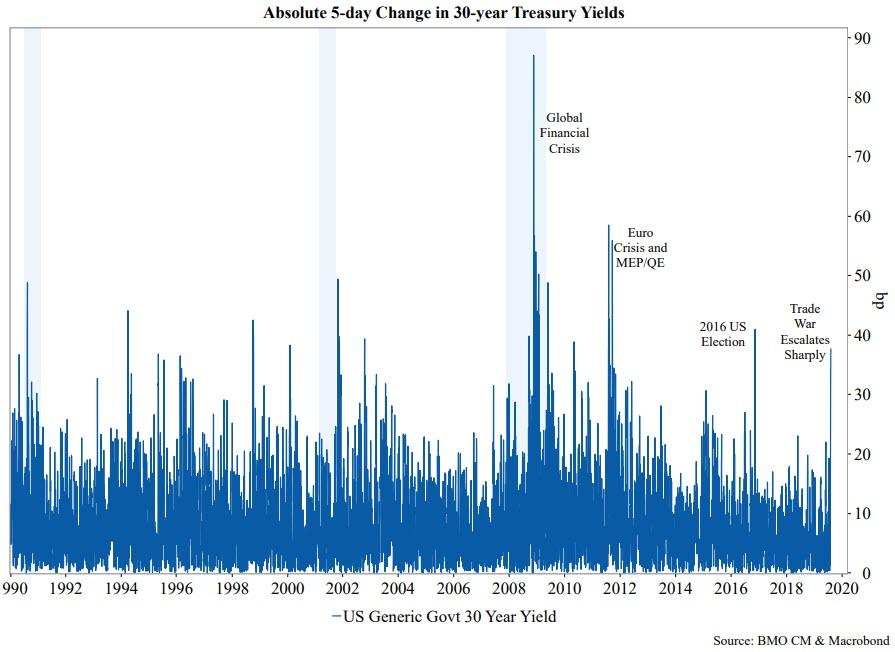

We've included a chart of the absolute 5-day change in 30-year yields

dating back to 1990 to illustrate just how dramatic the

recent 40 bp rally in the long bond has been. Every time the market

moved in a comparable fashion, 'something has changed'

was invariably the takeaway.

See Chart:

{kind=link}

If there was ever any question whether or not there

is a significant shift in investor expectations afoot, the performance of the

long bond should make it abundantly clear -- particularly in light of the proximity to the August refunding

auctions.

Remember when supply events warranted a concession? So pre-crisis.

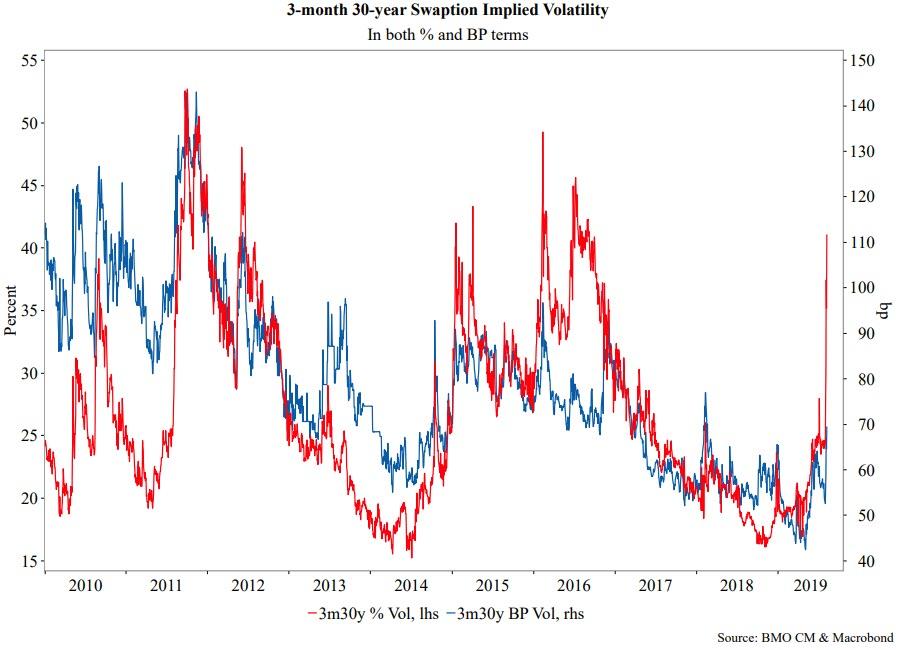

In keeping with our efforts to demonstrate the

relevance of the magnitude of the recent move, we offer a chart of 3-month 30-year swapt implied volatility -- in both percentage and basis point terms.

See Chart:

3 months 30 years swaption implied volatility

{kind=link}

The significance of the spike is difficult to

overstate.

….

SOURCE: https://www.zerohedge.com/news/2019-08-07/why-today-echoes-great-recession-euro-crisis-2016-election

----

----

The ruling

is just one element of the infighting that has gripped former Gov. Rosselló's

New Progressive Party...

====

... present voters are willing to steal from

future generations, many of whom do not yet get to vote, or are poorly

informed or involved in the political process.

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

Is it true that the US is arming

both sides? Or only Paks?

PM Khan

said he would take "all

possible options" in support of Kashmir's Muslim-majority

population.

====

For

the first time since March 2008,

PBOC fixed the yuan weaker than 7 per USD.

See Chart:

{kind=link}

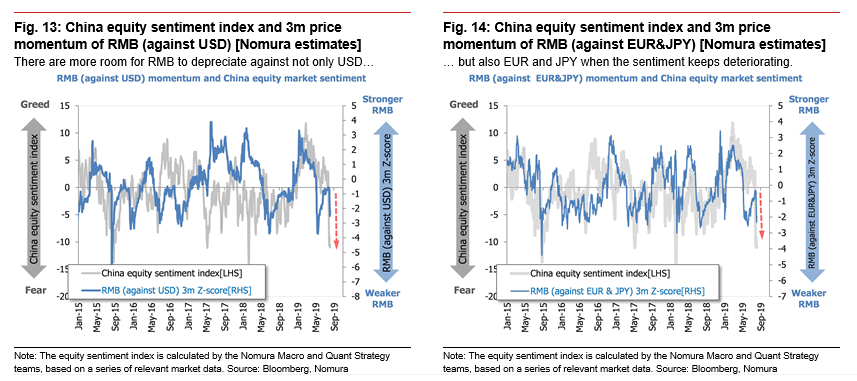

But, as Nomura notes, it could be set to get worse. [ To whom?

China plays Chess ]

If it turns out that actual economic momentum in China has flagged to

the extent suggested by the deterioration in Chinese equity sentiment, past patterns suggest that there is still scope for RMB to weaken further.

See Charts

{kind=link}

[ What variables include his sample? Fixing values

to an index is not real research.. I guess Nomura is becoming too

sentimental, or subjectivist. So: lack

of objectivism ]

The possibility remains that the yuan could depreciate even more

against JPY and EUR than against USD, judging by the relative shift lower in

the RMB Basket versus USDCNH, it seems that pressure is

starting.

See Chart:

{kind=link}

The PBOC decision comes as trend-following CTAs are chasing downside in

Hang Seng futures and H-share futures at an increasing pace. They have restored their existing net short

positions in Hang Seng futures to 48% of the YTD peak (June), and to 67% for

H-share futures, which suggests room to build these positions further.

[

The fact is that Nomura & US pressure doesn’t affect China, but to US

mainly. Check the recent moves in US Economy. US got desperate &

incoherent: Zombie Empire? ]

….

SOURCE: https://www.zerohedge.com/news/2019-08-07/china-fixes-yuan-weaker-7-first-time-over-11-years

----

----

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

====

RT EN ESPAÑOL

- Venezuela denuncia retención de barco con 25.000 toneladas de soja en el Canal de Panamá por bloqueo de EE.UU.

- ¿Otro conflicto por energía? Las posibles consecuencias de las nuevas sanciones de EE.UU. contra Venezuela

- Los vaivenes del comercio entre México y China

- Gob VEN no asistirá a reuniones de diálogo con la oposi en Barbados

- Maduro acusa a Trump de promov racismo blanco tras masacres en US

- Puerto Rico: La secretaria de Justicia Wanda Vázquez se juramenta como gobernadora de la isla

- Arrestan a 680 inmigrant en plantas procesadoras de alimentos en Misisipi

- Pakistán reducirá relaci diplomát y suspendel comercio con la India

- Analista político: "Trump ha buscado los caminos inciertos en Venezuela"

- Keiser Report llego el "fin de neoliber y globalización y el inicio de la desdolarización"

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political

crisis: neofascism & internal conflicts that favor WW3

-

Mass Shootings and Political Misuse of Them

Have Unintended Consequences

By Paul Craig Roberts

By Paul Craig Roberts

-

Feeding the Israel Lobby: Congress Gives the

Jewish State Whatever it Wants

By Philip Giraldi

By Philip Giraldi

-

Inside the Submissive Void: Propaganda,

Censorship, Power and Control

By Greg Maybury

By Greg Maybury

-

An Open Invitation to Tyranny By Paul Craig Roberts

----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

John G.

Russell The

“Feel Better” Presid: Making Racism Fashionable Again

J W.

Whitehead The

Rise of the American Gestapo

Nia

Harris et.al: the

Stubborn Truth About Employment and the Defense Industry

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

----

PRESS

TV

Resume of Global News described

by Iranian observers..

- A tale of two Dominics

- India, Pakistan ‘clash in Kashmir’ at delicate moment

- Abbas to congressmen: Palestine won’t take US ‘dictates’

- Caracas cancels talks with opp. to protest US asset freeze

- Pentagon chief in Mongolia to up pressure on Russia, China

- Tehran-Ankara train resumes after 4 years

- China urges US to stop bullying other countries

- Israeli forces use tear gas to kill Palestinians

- Maduro supporters rally against US blockade

- PROGRAMS

- The African Free Trade Zone: Winners and Losers

- Women’s no go zone

- Zarif slams UK roll in US economic terrorism

- Turkey's dubious role in Syria

- Israel pollution

----

===

No hay comentarios:

Publicar un comentario