ND

AUG 3 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

The trade

war hinders economic growth, therefore prompting additional Fed easing, which

in turn allows for greater trade war escalation, rinse, repeat until the world

slides into a depression.

See Chart:

{kind=link}

….

SOURCE: https://www.zerohedge.com/news/2019-08-03/how-fed-now-underwriting-trumps-trade-war-one-chart

----

----

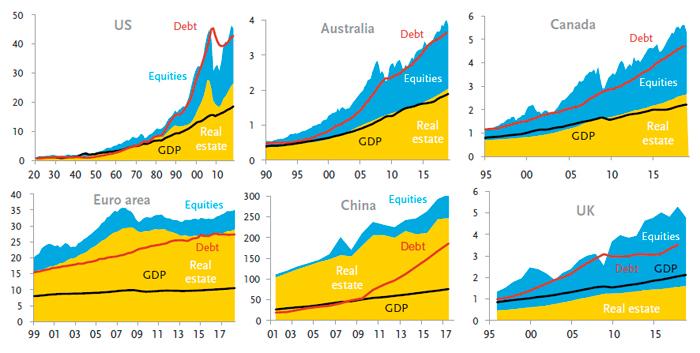

More and more stimulus – leverage – is ultimately a bridge to nowhere. Investors would do well to recall the down on the farm

wisdom of Stein’s law: if it can’t

go on forever, it won’t.

Do we have any way

to assess what the fruits of “stimulus” have been thus far? Perhaps the following charts provide some help:

See Charts:

{kind=link}

Let’s ask

ourselves: has the credit this cycle been used to drill productive wells, metaphorically

speaking? Measured by

income generated, it doesn’t look that way to me! Evidently, too much credit

has been employed in “stimulating” asset prices. Alas, if asset prices

“correct”, lots of debt will be written down, and what

was understood as “stimulus” will be re-classified as mal-investments.

No household nor

business can stay on a path of forever rising debt to income, nor can any

society in aggregate. More and more stimulus –

leverage – is ultimately a bridge to nowhere. Investors would do well to recall

the down on the farm wisdom of Stein’s law: if it can’t go on forever, it

won’t.

….

----

----

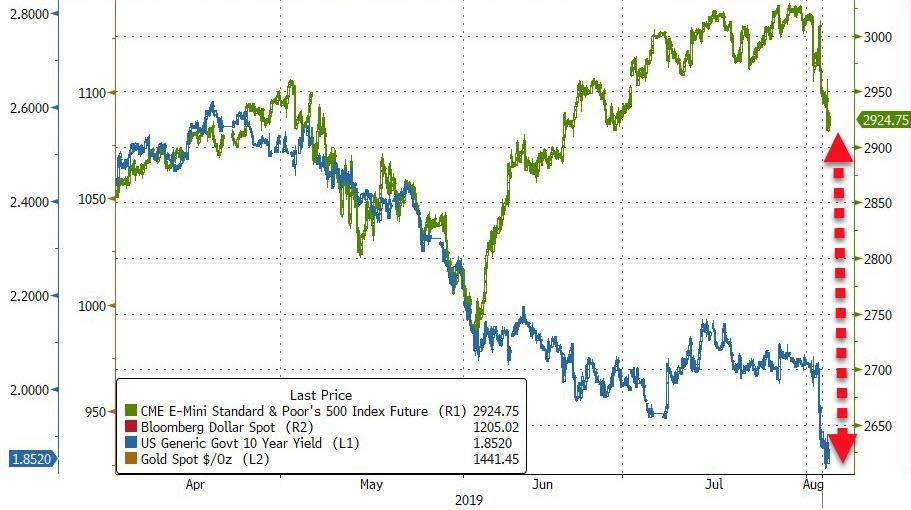

The front end is currently implying that even if the Fed cuts rates three

more times over the next year, the curve would still be inverted at the front

end!

As is traditional,

Panigirtzoglou starts off by focusing on the most important recent macro event,

in this case the unexpected re-escalation in the US-China trade war, which

similar to May, is creating recession-like/risk-off market dynamics with

government bonds rallying and equities and risky assets selling off, resulting in the infamous "alligator jaws" chart.

See Chart:

{kind=link}

The re-steepening

that the Fed had managed to engineer at the time is shown in Figure 1 which shows that the very front end of the US

curve stopped being inverted and re-steepened sharply following 75bp of rate

cuts (unlike now).

See Fig 1

{kind=link}

During both 1995 and

1998 episodes the forward spread i.e. the 1-month rate

2-years forward minus 1-year forward, entered negative territory only very

briefly.

See Fig 2:1

{kind=link}

However, as the JPM

strategist shows, the persistent negativity of

this forward spread at the moment is reminiscent more of the 2001/2007

recession episodes rather than the 1995/1998 mid-cycle Fed policy adjustment

episodes.

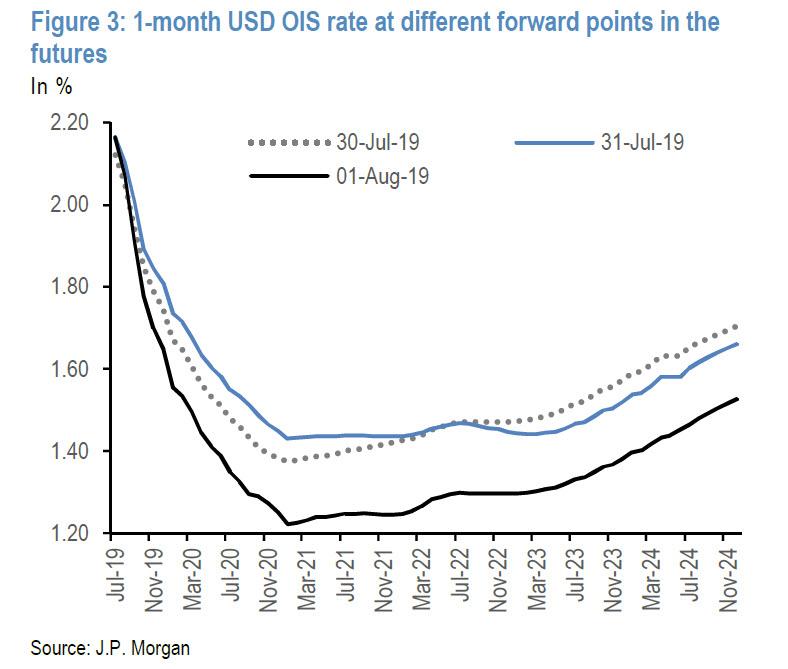

The flattening at

the front end of the US curve following this week’s FOMC meeting is also depicted in Figure 3 which shows the 1-month US OIS

rate at different forward points in the future, pre-FOMC (July 30th) and post-

FOMC (July 31st).

See Chart:

{kind=link}

Which brings us to

the $64 trillion question: will the Fed keep cutting rates by another

100bp by the beginning of 2021 to only provide insurance in a good growth

environment to satisfy both equity and bond markets at the same time. In other

words - and here we urge readers to once

again look at the alligator jaws chart above - the only way the divergence

between bonds and stocks is sustainable, is if the Fed cuts at least another 4

times.

See Chart:

Will the

Fed do this? According to

JPMorgan, "most likely not" unless of course Trump manages to

transform World Trade War III into something even more dire, so as Panigirtzoglou concludes, "one of the two markets is

likely to prove wrong." It was so obvious which one, that the JPM

strategist didn't even both to point out which.

….

----

----

At this point in the business cycle, corporations have loaded

themselves up with so much debt

that they are extremely fragile. Should the economy slow ever so

slightly, it will be game over for

countless over-leveraged companies.

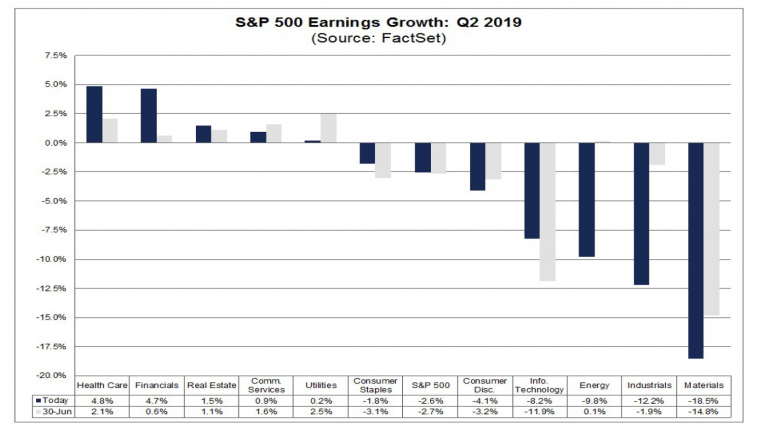

The

economy, after 10 years of growth, appears to be heading for a respite too. Second quarter earnings, currently being

reported by S&P 500 companies, have been a mixed bag thus far. But in

sectors that actually make stuff, like materials and

industrials, earnings are suffering double

digit declines.

See Chart:

{kind=link}

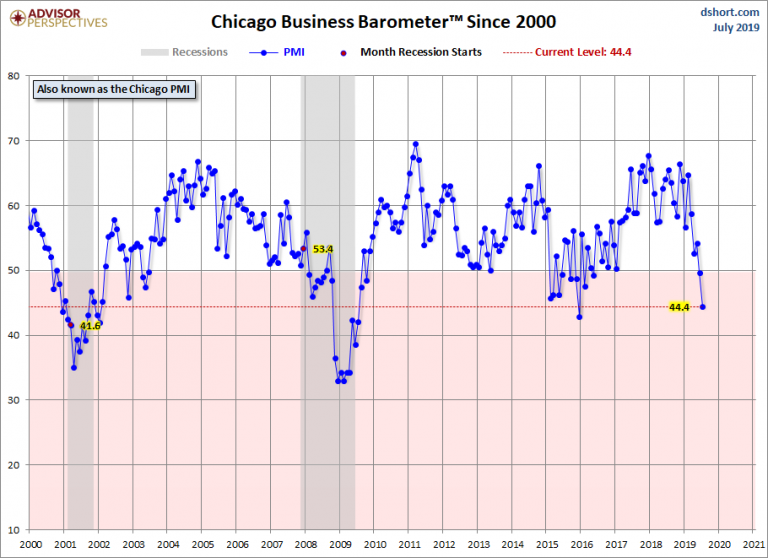

For context, a Chicago

PMI reading below 50 indicates a contraction of the manufacturing sector in the

Chicago region. So far this year, the Chicago PMI has been

down five out of seven months. On top of that,

weaker demand and production pushed the employment indicator into contraction

for the first time since October 2017.

See Chart:

{kind=link}

Unfortunately, the

weakness in manufacturing extends beyond the Chicago

region. On Thursday it was reported that the U.S.

Manufacturing PMI dropped in July to its lowest level since September

2009. Employment also fell for the first time

since June 2013. What is going on?

See Chart:

{kind=link}

Making lemonade from

these economic lemons is generally impossible. Still, that

doesn’t mean companies don’t try by taking on

greater and greater levels of debt. And the big

banks, which are backstopped by the Fed, continue

extending credit to keep the sham going.

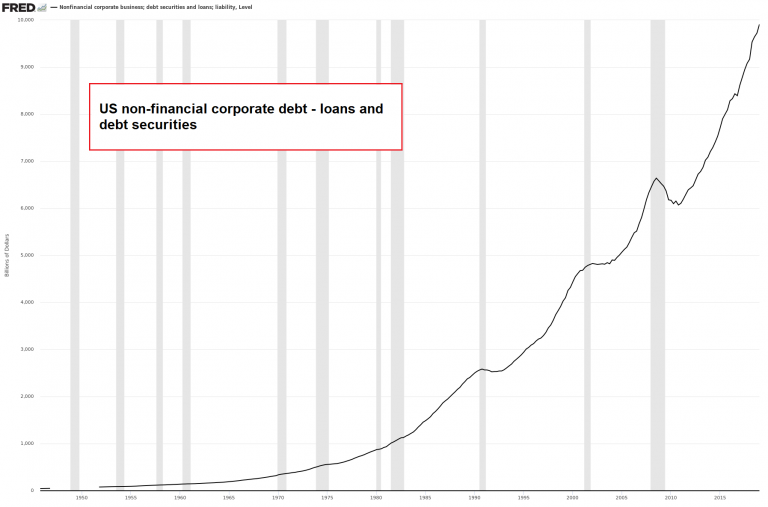

U.S. non-financial corporate debt is

about $10

trillion, or roughly 48 percent of gross domestic product (GDP). That is up about 52 percent from its last peak in the third

quarter of 2008, when corporate debt was about $6.6 trillion, roughly 44

percent of 2008 GDP. In short, corporate debt is

at record levels and is rising much faster than economic output.

See chart:

{kind=link}

Do You Hear a

Bell Ringing?

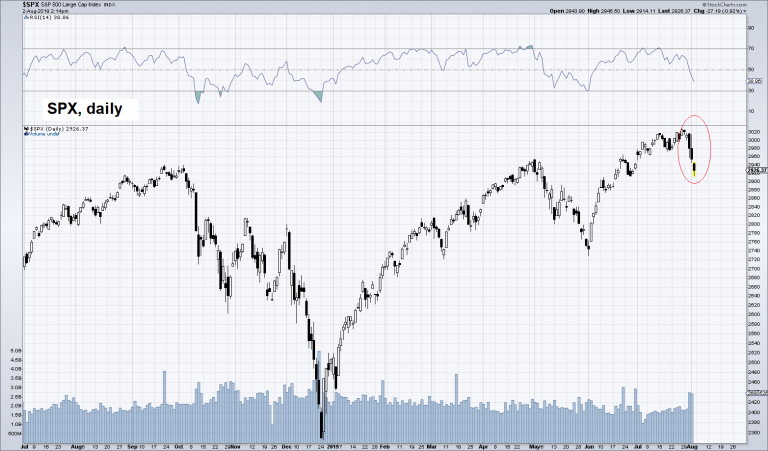

Promises of more cheap credit from the Fed have propelled

stocks to record highs. Year-to-date, stocks, as measured by the S&P

500, are up over 17 percent.

On Wednesday, however, some

uncertainty was added to the market. At the conclusion of the July Federal Open

Market Committee (FOMC) meeting, Fed Chair Powell cut

the federal funds rate 25 basis points. But instead of telegraphing that

additional rate cuts would follow like Wall Street expected, Powell said it was

merely a mid-cycle adjustment. In other words, he’s winging it.

See Chart:

{kind=link}

Yesterday, after sleeping on the Fed’s ambivalence, traders

showed up to work with focus and intent. They bought the dip with

confidence. And everything was great until about mid-day. The

S&P 500 was up 33 points – and then something unexpected happened.

President Trump, via

Twitter, dropped a turd in a crowded swimming pool:

“…the U.S. will start, on September 1st, putting a small additional

tariff of 10% on the remaining 300 billion dollars of goods and products coming

from China into our country. This does not include the 250 billion

dollars already tariffed at 25%.”

The

market gets whacked by the God Emperor… [PT]

Following Trump’s tweet, Wall Street

freaked out. The S&P 500 dropped 68 points, ending the day at 2,953.

“No one rings a bell at the top of the market,” says the old Wall Street adage. Make of this

week’s manifestations what you will. We hear a bell ringing. Do

you?

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

US Wars everywhere create environment for any crazy person

to shoot everywhere

According to a police scanner the shooter was armed with an automatic weapon, possibly an AK-47,and

that they began shooting in the car park before entering the business...

====

The big

billonaires tambien devinieron crazy.. en contradic internas se destruirán

"Some of the other stuff

we’ve encouraged, such as The EU, ETFs, Hi-Frequency Trading, Neil

Woodford and Deutsche Bank look likely to be highly effective vectors of short-term economic destruction and

destabilisation..."

….

Querran destruir el centralism y acelerar la

div y autonomia Reg.. y la alianza del Inversor medio con el labor se encargara

de expropiarlos.. adiós al especul

====

Mexico is diving deeper into a murder crisis

as cartels and narcos overrun the country, leading to more than 17,000

people killed in the first half of this year.

….

Militaristic malady turns into pandemia= if

they shoot, we shoot too. No difer

====

A 'routine

website redesign'...

….

CA fue el fuerte del Viejo Pdo Dem y Kamala hizo temblar a los Reps.. Su

error fue no aliarse a los socialistas.. aun puede hacerlo y demandar: 1- “best educat & Health

for all” lo que implica pedir “zero-debt para los estud-Univ y egresados

y “one single payer” (El Estado Central) para garantizar la buena salud de

todos. Seria el adiós a la Pharma: los parasitos que engordan con el neliberal

health system we have. Como financiar esto? . 2- Exigir

el recorte del Presupuesto Militar. El Penta - Nato y su WW3 son

una amenaza no solo para nuestra Nacion, lo son para todo el Universo. Esto supone

un PACIFISMO tan agresivo como lo es el militarismo

actual. Y ello implica denunciar

y encausar a las empresas del Milit-Industrial Complex y exigir inmediato

impeachement de Trump. K-H debe unirse a los candidatos socialistas para

llamar Movilizac-popular en Washington a favor de la PAZ

MUNDIAL. Pero ya debe empezar con

un manifiesto claro en favor del punto 1 y 2. Si no lo

hace, solo le queda unirse a Joe

Biden y los de la vieja guardia Dems. Si lo hace,

Kamala Harris reactiva

este Pdo en CA y CA vuelve a ser el fuerte del Pdo Dem y ella real candidata a

la Presidencia, no mera aliada de un bufón de la vieja guardia.

….

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in

limbo

No es la

politica “garrote vs. zanahoria” lo que usa Trump contra Zarif. Da 1ro el

garrotazo como hampon de esquina y luego dice ‘dialogo’. Eso es vulgar coaccion

y chantaje. Zariff debe exigir el retiro público de

la sanción para asistir a dial-honesto

After

rejecting the surprise overture for direct negotiations, Zarif was sanctioned this week by

US Treasury.

====

Maduro

retorted Venezuela's seas will remain "free and independent"...

….

Trump puede enviar

a VEN todos los terroristas Saudis que no pudo enviar a Europa.. Igual da: las

brigadas civil-militares están listas para responder y los misiles listos para

mandar abajo aviones y barcos con comandos USA y sus saudis. La ‘bienvenida’ a

estos miserables esta lista. Brazil acaba de enviar brigadas Rev bien armadas

para defender VEN, la patria latina hermana. Lo demás lo harán las brigadas rev

de cada país de sur contra las embajadas USA y los empresarios del US. Asi

están las cosas, sin duda veremos otra V de Ven

….

====

La

mejor sirvienta del Imperio y el USD se va .. quiera o no.. será cambiada

If new institutional reform is to come to the Eurozone, it will entail a major paradigmatic shift...

….

Si se va pronto,

mejor para ella y el IMF. Posible una Rusa tome su puesto.

====

SPUTNIK

and RT SHOWS

GEO-POL n

GEO-ECO ..Focus on neoliberal expansion

via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

====

RT EN

ESPAÑOL

- Todo lo que se sabe sobre el tiroteo en El Paso que ha dejado 20 muertos y al menos 26 heridos

- VIDEOS: Publican las primeras imágenes del tiroteo mortal cerca de un centro comercial en Texas

- FOTOS: Qué se sabe hasta ahora del tirador de Texas

- El nuevo buque de asalto anfibio de la Marina de EE.UU. llegará con retraso debido a problemas técnicos

- Trump empuja a Guatemala a la catástrofe humanitaria y al conflicto internacional Luis Gonzalo Segura

- Nuestro presidente racista: Trump y la política de crueldad Eva Golinger

- Keiser Report Capital Pirata y Recorte de tasas: "Las corporaciones zombis le dan dos tiros en la nuca a la economía estadounidense"

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

- Why The End Of The INF Treaty Will Not Start

A New Arms Race By Moon Of A

- Tainted Meat Market By Paul Edwards

- A Blockade of Venezuela Must Be Opposed By Daniel Larison

- CBP agents interrog US citizen and seize his

phone after Ven solidarity trip By MB

- More Fake Happy News About Jobs By Paul Craig Roberts

- More Fake Happy News About Jobs By Paul Craig Roberts

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

PRESS TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario