ND

AUG 22 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

"The

most concerning aspect of the latest data is a slowdown in new business growth

to its weakest in a decade, driven by a sharp loss of momentum across the

service sector."

See Chart:

{kind=link}

….

----

----

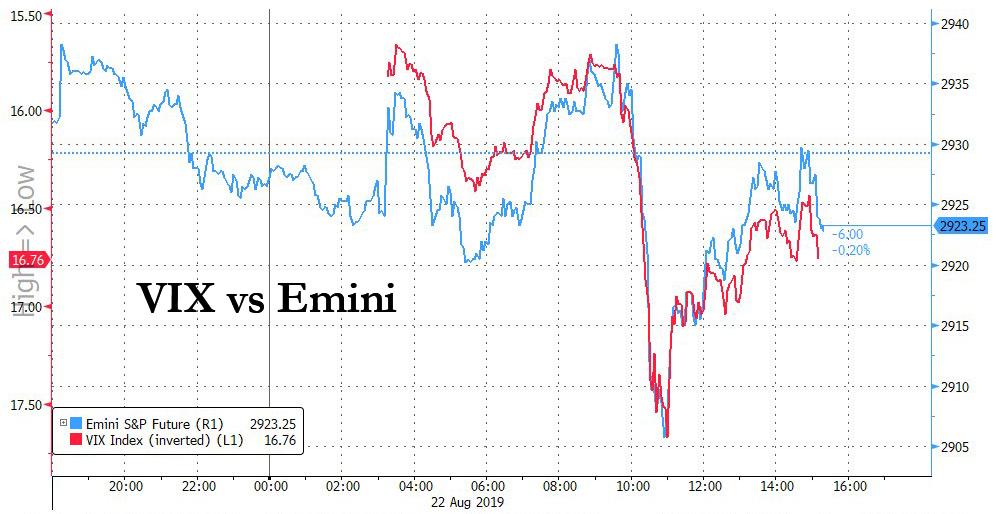

In what was mostly a very quiet day, with traders refusing

to trade in size ahead of tomorrow's main event, J-Powell's J-Hole speech, we

got a glimpse of what will happen if the Fed chair disappoints the market's

expectations for committing to further rate cuts.

After spiking in early trading,

stocks slumped to session lows and the VIX jumped back over the key 16

threshold, after Philly Fed's Harker joined other regional Fed presidents

in pouring cold water on hopes for more rate cuts, and instead saying that he

expects not to vote for more easing.

See Chart:

VIX

vs. Emini

{kind=link}

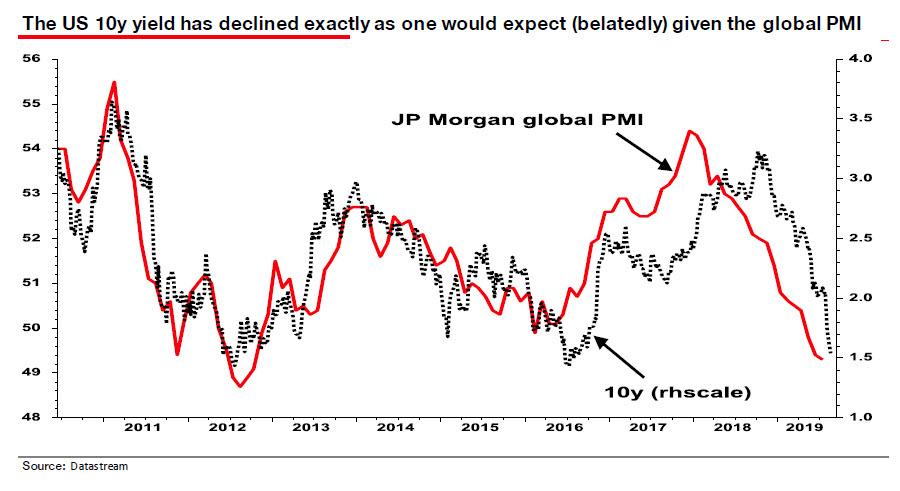

The drift higher in short-term

yields came even as Markit reported the first contractionary manufacturing PMI

in ten years, at 49.9, while the services PMI stumbled as well, making the case

for a recession that much more likely.

See Chart:

In any case, the surprising

hawkishness out of Fed presidents, and the spike in 2Y yields, meant that the

2s10s yield curve inverted again - yet another recessionary indicator - and was

flipping between negative and positive for much of the day.

See Chart:

{kind=link}

And so with the S&P closing flat, Chris Zaccarelli, CIO

for Independent Advisor Alliance, summarized it best: "The big question mark is just going to be Jackson Hole --

what’s Powell going to say You’re seeing the market going higher and lower this

week heading into tomorrow, where we could get some market-moving commentary

out of Powell’s speech."

For those curious what Powell may say, and why he will

likely disappoint, read

our preview of tomorrow's J-Hole main event here.

….

----

----

"A

global deflationary bust will wreak havoc with financial markets. Does anyone

seriously believe that in the next global recession equity markets will not

collapse?"

Earlier this week we

wrote that after decades of waiting, for Albert Edwards vindication

was finally here - if only outside the US for now - because as per BofA

calculations, average

non-USD sovereign yields on $19 trillion in global debt had, as of Monday, turned

negative for the first time ever at -3bps.

See Fig 1

Globsl IG

fixed income

{kind=link}

What does he mean?

As Albert explains, "when you see the creeping advance

of negative bond yields throughout the investment universe, you really start to

doubt your sanity. For me it is not so much that 10y+

government bond yields are increasingly negative, but when European junk bonds go negative I really start to scratch my

head." And as we wrote in "Redefining

"High" Yield: There Are Now 14 Junk Bonds With Negative Yields",

there certainly is a lot of scratching to do.

One thing Edwards isn't scratching his head over is whether

this is a bond bubble: as he explains, his "own view is that this government bond

rally is not a bubble but an appropriate reaction to the market discounting the

next recession hitting the global economy from all overleveraged corners of the

world (including China), with close to zero core inflation

and precious few working tools left at policymakers’ disposal."

This means that "the bubbles are not in the government bond

market in my view. They are in corporate equities and corporate bonds."

If Edwards is correct about the locus of the next

mega-bubble, it is very bad news for risk assets as the "global

deflationary bust will wreak havoc with financial markets", prompting

Edwards to ask a rhetorical question:

Does anyone seriously believe that in the next

global recession equity markets will not collapse? Do market participants

really believe fiscal stimulus and helicopter money will save us from a

gutwrenching global bust that will make 2008 look like a picnic? Has the longest US economic cycle in history beguiled investors into

soporific complacency? I hope not.

So to validate his point that the

rates market is not a bubble, Edwards goes on to show that "US and even eurozone government bond yields are not in

fact overextended – certainly not on a technical level – but also that

fundamentals should carry government bond yields still lower."

See Chart:

{kind=link}

In his note, Edwards launches into an extended analysis of the declining workweek for both manufacturing and total

workers, and explains why sharply higher recession odds (which we recently

discussed here), are far higher than consensus

expected.

See Chart:

{kind=link}

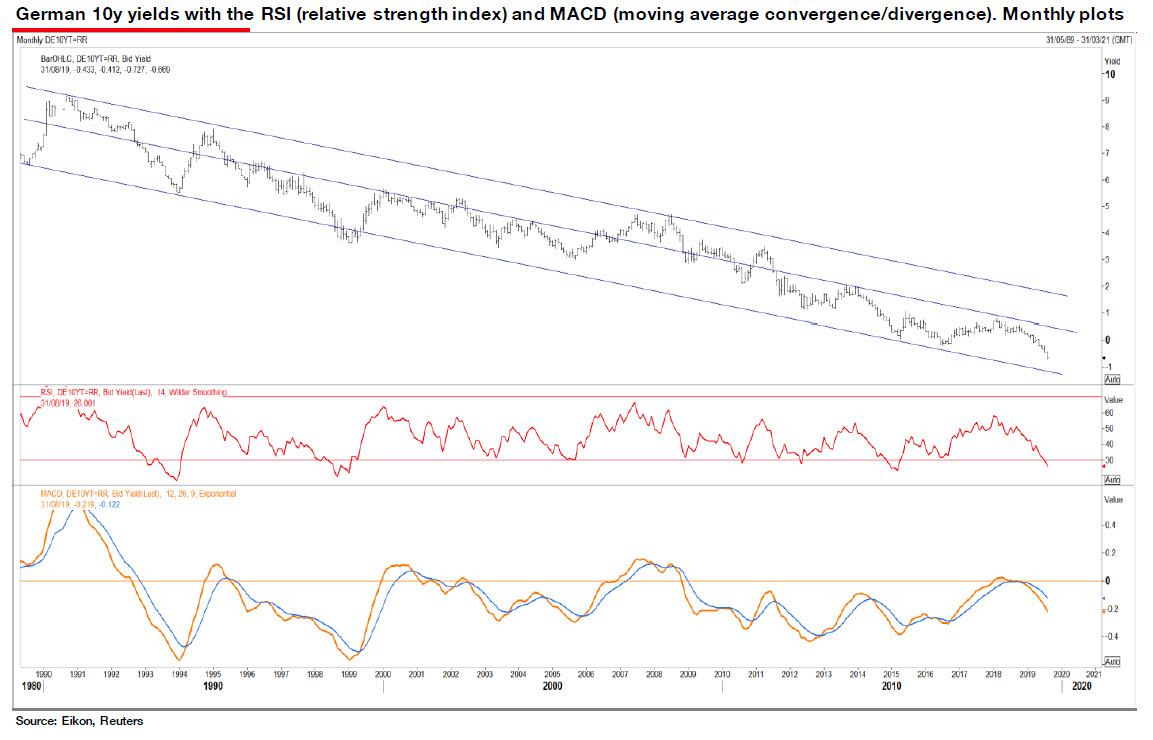

But what we found most notable was his

technical analysis of the ongoing collapse in 10Y Bund yields. As

Edwards writes, "looking at the chart for German 10y yields (monthly plot)

their decline to close to minus 0.7% does not seem so extraordinary – merely the continuation of a downtrend within very clearly

defined upper and lower bounds”

See chart below

{kind=link}

As Edwards explains referring to the chart above, "the

bund yield has remained in the lower half of that band since 2011, but there is

good reason for that as the ECB has struggled with a moribund eurozone economy

and core inflation consistently undershooting its 2% target."

His conclusion: "This market certainly doesn’t look like a

bubble to me."

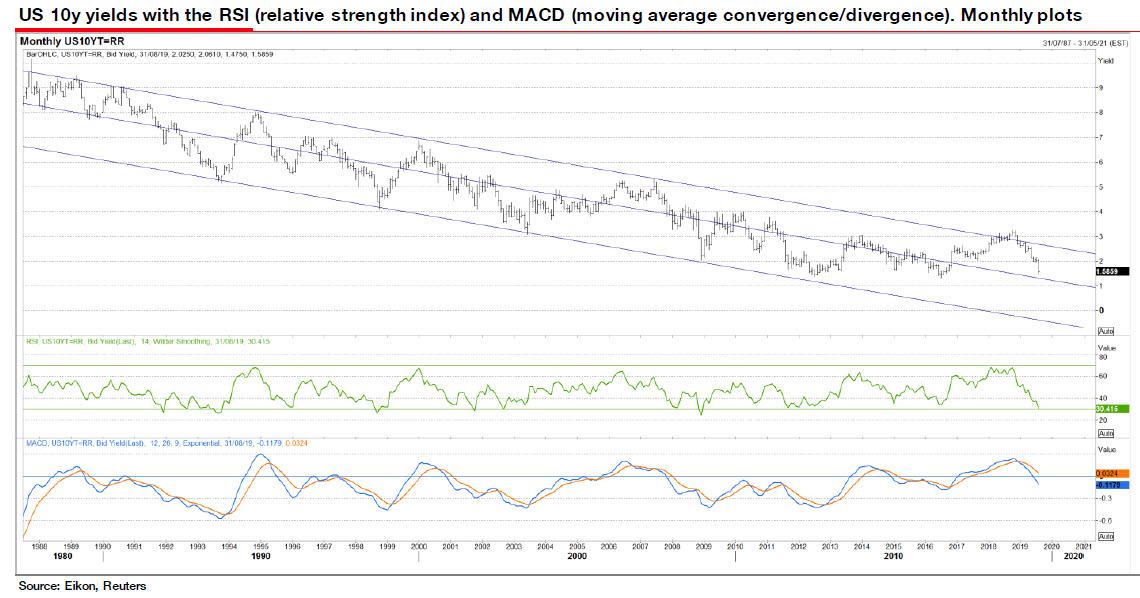

Shifting attention from Germany to the US, Edwards writes

that unlike the 10y German bund yield, "the US 10y

has mostly occupied the top half of its wide downtrend band since 2013."

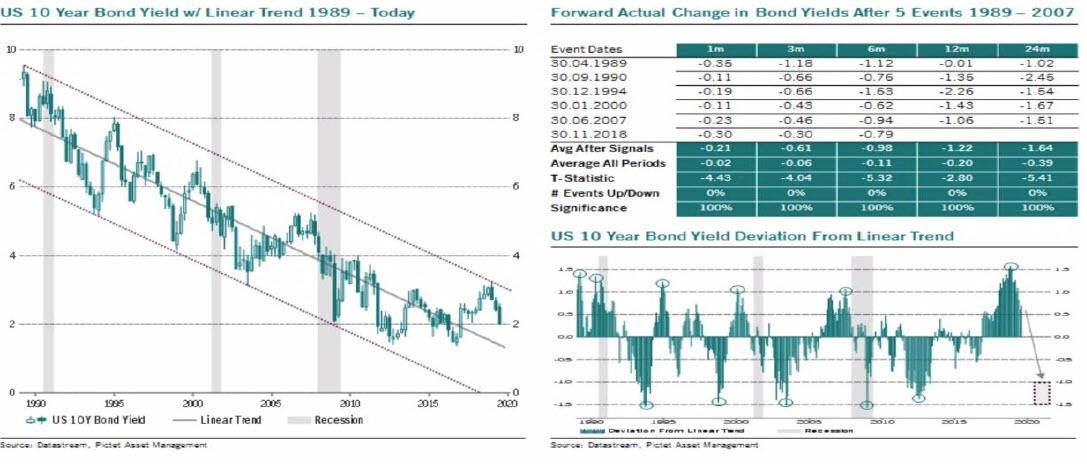

See Chart:

{kind=link}

It is Edwards' opinion that "we

are on autopilot until we get" to 0.5%.

But wait, there's more, because in

referring to the charting of Pictet's Julien Bittle (shown below), Edwards

points out the right-hand panel which demonstrates how far US 10y yields might

fall over various time periods after hitting a cyclical peak. "He shows that on average we should expect a decline of 1-1½ pp from the trendline, which takes us

pretty much to zero (see slide)." Personally, Edwards says, he

is even "more bullish than that!"

See Chart:

{kind=link}

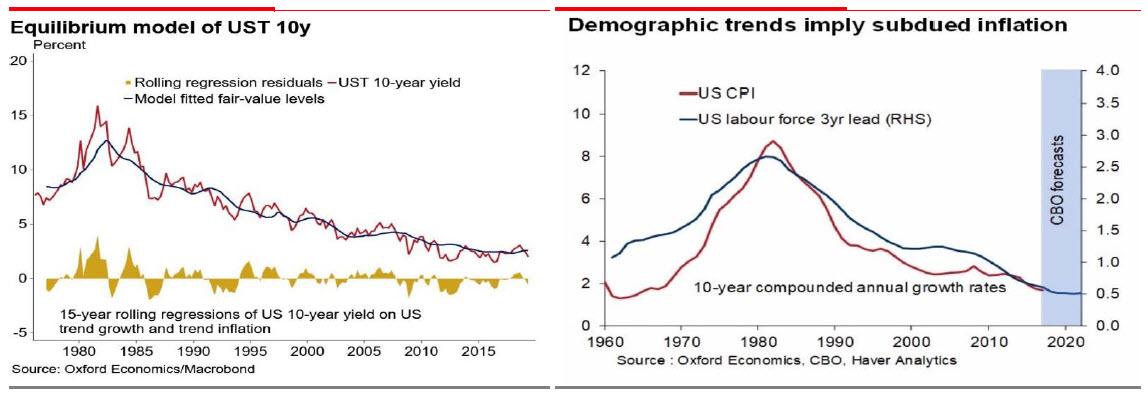

Edwards then points us to the work of Gaurav Saroliya,

Director of Macro Strategy at Oxford Economics who "certainly doesn’t

think that QE is depressing bond yields." In this particular case,

Saroliya uses a simple model which fits US 10y bond yields with trend growth

and inflation reasonably accurately (see left hand chart below). As Edwards

notes, "given the demographic situation, inflation

is likely to remain subdued."

See Charts:

{kind=link}

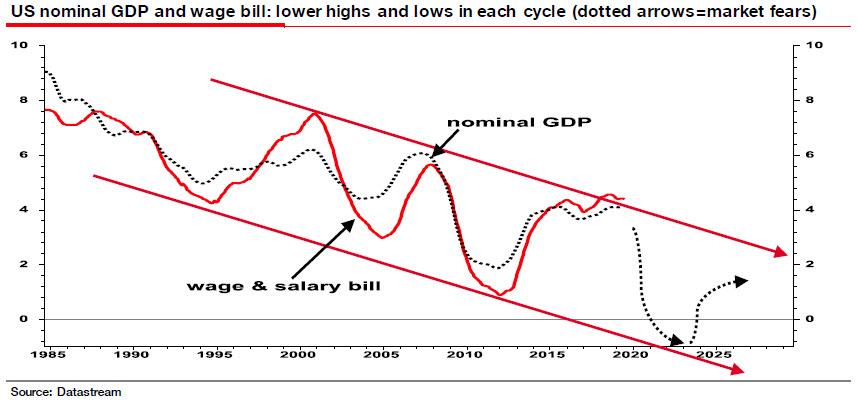

In conclusion Edwards presents one final and classic Ice Age chart to finish off.

As the bearish - or is that bullish... for bonds -

strategist notes, "the last few cycles have seen a sequence of lower lows

and highs for nominal quantities (along with bond yield and Fed Funds). I have used a 4-year moving average and have added where I

think we may be heading in the next downturn and rebound - and more importantly

where I think the market is now thinking where we are heading."

See Chart:

US Nominal GDP and wage Bill

{kind=link}

[ Be nice with your patient, please ]

Referring to the implied upcoming plunge in nominal GDP,

Edwards explains that "that

is why this is not a bond bubble. It is the next phase of The Ice Age. And it

is here."

[ Come on,

be nice.. say a lie please ]

One last note: is it possible that

Edwards' apocalyptic view is wrong? As he admits, "of course" he could be wrong: "And given my

dystopian vision for the global economy, equity and corporate bond investors, I sincerely hope I am."

[ Bravo!

Better than Trump’ team lies: “You sincerely

hope” so. ]

….

----

----

Sorry baby: If there is not milk in my breast is not your

fault. You have the right to cry

The latest

deal to get pulled was a loan by Vewd Software, which joined peers such as

Golden Hippo, Glass Mountain Pipeline Holdings, Chief Power Finance and

fitness-center builder Life Time, all of whom failed to raise money in the loan

market.

See Chart:

Fund Outflows

{kind=link}

What happens next? Well, there are two options: either the market freeze continues as the December 2018

"Ice-Nine" of the loan market indefinitely postpones the entire

pipeline, OR the more optimistic investors end

up being right: they are merely waiting to approach the market after

Labor Day on Sept. 2, when the liquidity - they hope - will return to the

market. That's when we will also see just how easy it

will be for a consortium of banks to sell a whopping $7 billion loan to help

finance the merger of T-Mobile US and Sprint.

[[ These dreams are better

than OPIUM DREAMS ]]

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Billionaires censoring freedom of informat with support of

FED Sys like in nazi German

What counts

as 'online hate'?

…..

Hate on migra, Ame-blacks &

other minorities? Are they saints? Saint Kosos?

====

====

It is not enough to support ISR expropriation of land from

PAL: you must be “semite” .. So, get a piece of condom on your head with the

logo ‘Trump 2020’: Semites = happy

"There

is no ambiguity..."

….

Not at all in declaring Jerusalem

capit of ISR, What if Vatican declar cap of IT?

Impossible!:

there is not troglodytes like BN in

Italy, though they try in XIV Ct

====

One more teen-Slippery

Slope & false similarity: the pedo-monster Epstein & Bill Gates the

greatest scientist of Apple who wanted to be indep from CIA info-staff.

And why was

his former science adviser named an executor of Epstein's will?

….

If you can’t compare good with best

and bad with worse, move t stink fantasy

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

Iraq has

sought to close its airspace even to US military flights "not

authorized"

====

Worse than OPIUM DREAMS:

The U.S.

could “drown the world in oil” over the next decade, which, according to Global

Witness, would “spell disaster” for the world’s attempts to address climate

change.

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

Mexico: presa

del terrorismo blanco del US

Marco I. Dávila C.

====

ALAI ORG

====

RT EN

ESPAÑOL

- Rusia: "Por las ambiciones geopolíticas de EE.UU., el mundo está al borde de una carrera armamentista descontrolada"

- VIDEO: Así avanza el fuego durante los devastadores incendios forestales de la Amazonia y Bolivia

- China prueba el avión que plantará cara a Boeing y Airbus

- Qué es la CICIG y por qué tiene los días contados en Guatemala

- VIDEO: Las primeras imágenes del Titanic en 14 años

- VIDEO: una indígena brasileña anticipó los incendios en la Amazonia

- El "mayor caso de pedofilia" en Francia: un cirujano violó a cientos de menores bajo anestesia y lo registró en un diario

- Corea-N afirma estar listo para el diálogo o la confrontación con US.

- Las posibles efectos que pueden dejar los incendios de la Amazonía

- Perú vive una jornada nacional de protestas y reclamos de nuevas elecciones generales

- López Obrador rechaza la existencia de grupos de autodefensa en México

- Keiser Report "Se está tratando de ocultar a toda costa una tragedia humana en San Francisco"

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

-U.S. No Longer Dominant Power in the Pacific By Paul D. Shinkman

- John Pilger: We are in a WAR SITUATION with

China! By Going U

- Suddenly West is Failing to Overthrow

“Regimes” By Andre Vltchek

- Omar, Tlaib, and the United States of Israel By Kurt Nimmo

- Trump’s White nationalist (Supremacy) Agenda By Bischara Ali EGAL

- What Globalism Did Was To Transfer The US

Economy To China By Paul Craig R

- American Apocalypse: Govt’s Plot to

Destabilize the Nation Works By J W.W

----

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

George Ochenski Breaking

the Web of Life

Steve Early A

GI Rebellion: When Soldiers Said No to War

Dan Corjescu The

Metaphysics of Revolution

Mark Weisbrot Who

is to Blame for Argentina’s Economic Crisis?

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

- 2020

Candidates Address Historical Trauma, Missing Indigenous Women & More at

Native American Forum

----

----

PRESS TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario