ND

NOV 25 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

Is everything going great?

Stocks decoupled from bonds, gold,

and the dollar today, melting up aggressively at the US cash market open and

close...

See Chart:

{kind=link}

Thanks to the continuation of the

biggest short-squeeze since early October...

See Chart:

{kind=link}

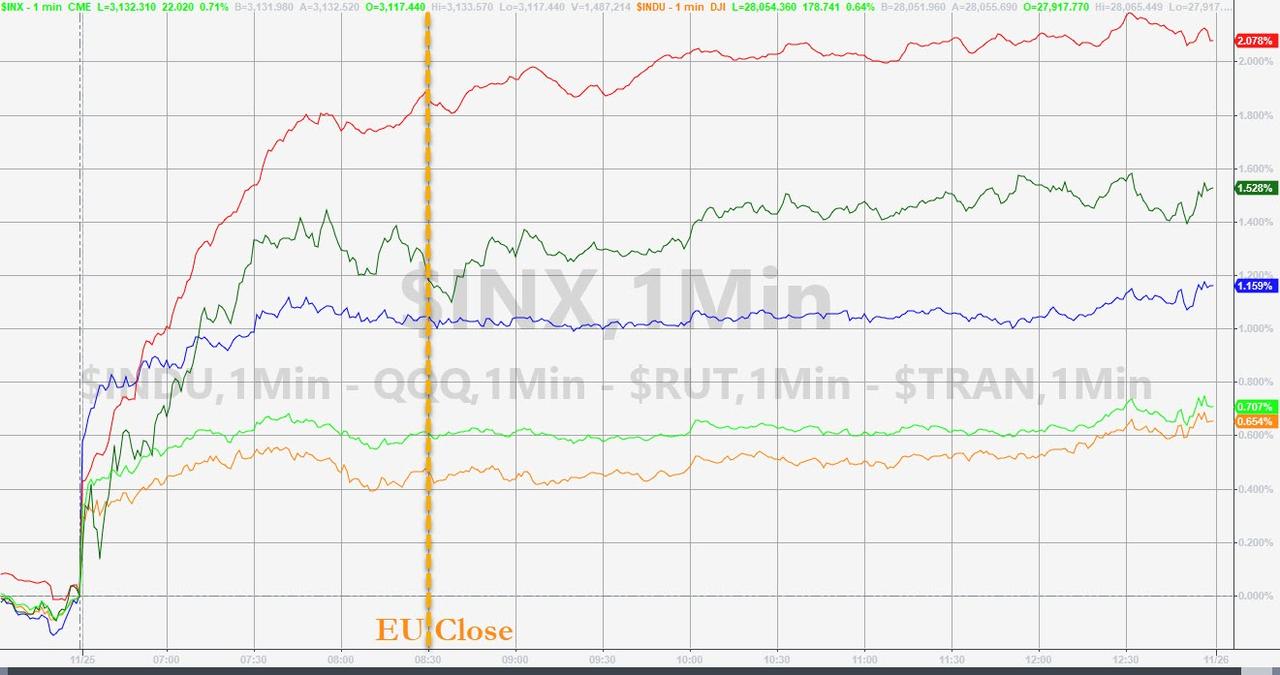

Which sent Small Cap stocks exploding higher...NOTE - markets really went nowhere after Europe

closed...

See Chart:

{kind=link}

As Morgan Stanley warned - Smaller-capitalization

companies could see a second full year of negative EPS growth.

Additionally, the Russell 2000

massively outperformed S&P SmallCap 600 massively today...

See Chart:

S&P SmallCAP 600/ Russell 2000

{kind=link}

Dow futures Algos were entirely

focused on 28,000 today

While VIX was clubbed like a baby seal to the lowest since Oct 2018...

See Chart:

{kind=link}

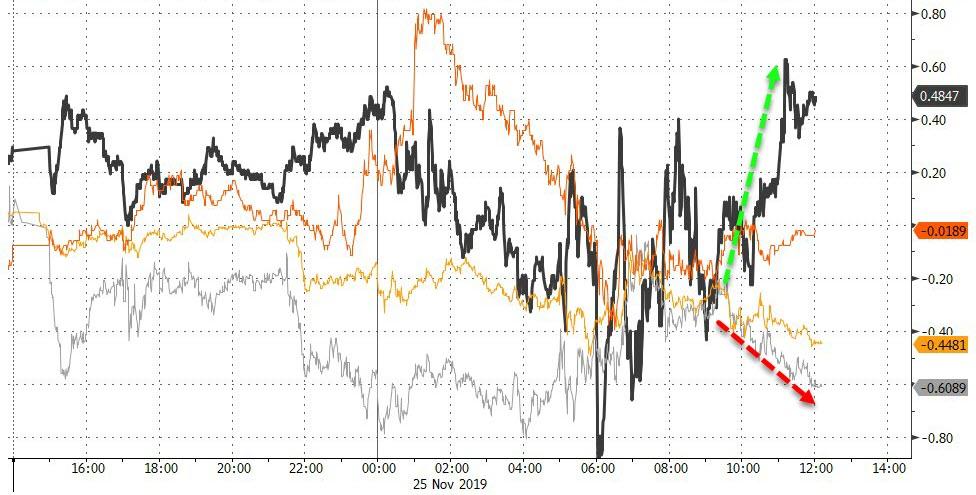

Treasury yields tumbled early and

held the gains on the day...

See Chart:

{kind=link}

The Dollar extended its rebound

today, taking out last week's highs...

See Chart:

{kind=link}

Commodities were chaotic today with oil

higher and PMs lower...

See Chart:

{kind=link}

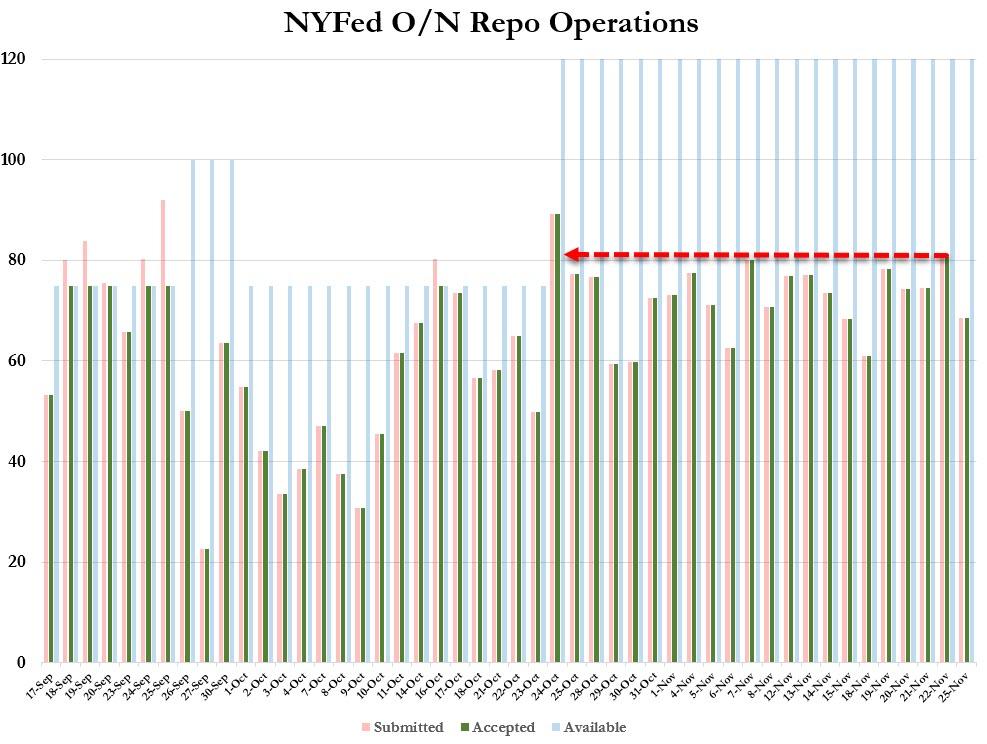

Finally, as Bloomberg

reports, market

participants submitted $49.05 billion in bids for the Fed’s 42-day term repo

operation, which matures Jan. 6, 2020. That was more than the $25 billion on

offer. This was the

first of three term operations to provide funding past the year-end period. The

others will be held in the coming weeks. Meanwhile,

overnight repo demands remain anything but transitory...

See Chart:

{kind=link}

All of which is a huge deal as global liquidity is starting to decelerate

(just as it did in April)...

See Chart:

{kind=link}

….

SOURCE: https://www.zerohedge.com/markets/vixtermination-sends-stocks-surging-amid-massive-short-squeeze

----

----

OPIUM DREAMS?

Maxims in

politics such as "United we stand, divided we fall" do not

necessarily hold in investing.

Overnight, in his 2020 US Equity Outlook, Goldman's chief US

equity strategist David Kostin shared some other

key considerations how he sees the way forward in the equity market, as well as

his year end forecast, which for the first time bifurcates into two explicit

targets, depending on key variable.

Curiously, Kostin's forecast bifurcates not only from an

"event-risk" standpoint, but also chronologically and as the

strategist writes, the "durable profit cycle and continued economic

expansion" will lift the S&P 500 by 5% to 3250 in the early part of

2020. However, the rising political and policy

uncertainty will keep the index range-bound for most of next year.

"Goldman also reveals the bank's baseline forecast for

2020, which he expects to rise by 6% to $174 in 2020 and by 5% to $183 in 2021.

Yet here too Goldman reveals that things may change

depending on whether or not Trump's tax cut is reversed - in which case the

bank's baseline 2021 EPS estimate of $183 would be reduced by 11% to $162.

Assuming the bill is applied retroactively to the start of the year, S&P

500 earnings growth in 2021 would equal -7%, compared with the baseline

estimate of +5%.

See Chart:

S&P 500 earning

{kind=link}

However, this time the risk

exists of a sharp multiple re-rating lower as the election result will affect

equity valuations through changes in policy uncertainty and consumer

confidence. here, Goldman uses its macro model of the yield gap between the

S&P 500 earnings yield and 10-year US Treasury yield to estimate the impact

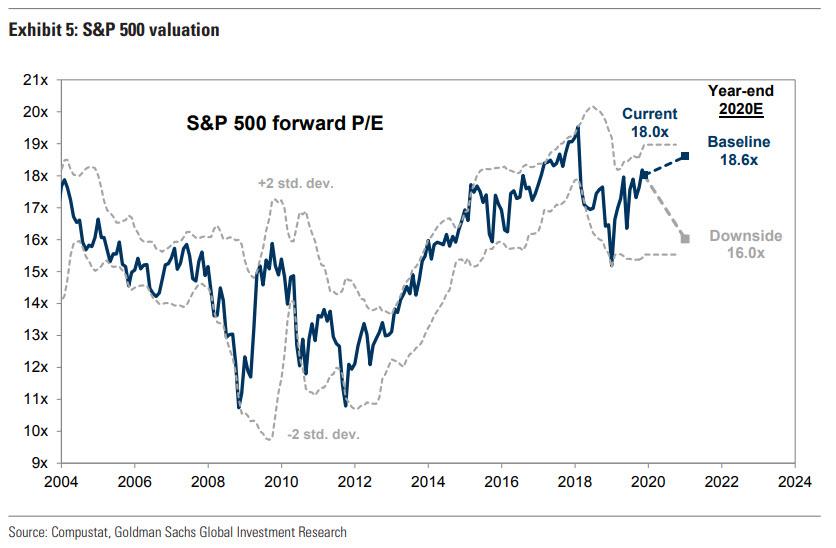

of uncertainty and confidence on equity valuations. And

while the bank's baseline forecast assumes that following the election the

S&P 500 forward P/E multiple expands slightly to 18.6x, if US policy

uncertainty post-election rises rather than falls - read if a Democrat wins the

election - or consumer sentiment declines, the equity risk premium would

increase and the P/E multiple would compress by approximately 2 points to 16x.

See Chart:

S&P 500 valuation

{kind=link}

What does this mean from a simple

price perspective? Well, one can multiple one by the other and get the answer.

For those who can't, Goldman writes that the election

outcome "could magnify risks or the economic growth outlook could

deteriorate", by which it means Trump may not be re-elected. But more importantly

should Democrats also regain sole control over Congress, "a unified

federal government post-election could prompt investors to assume the tax cut

is reversed and lower projected 2020 EPS to $162 (-7% year/year growth),

compressing the P/E multiple to 16x consistent with an index level of 2600."

See Chart:

Path of the S&P 500 in 2020

{kind=link}

And while Goldman's price target "range" is indeed

quite broad, the bank's confusion appears to be prevalent because as Kostin

notes, as investors consider the outcome of the election, the distribution of

S&P 500 levels implied by the options market at year-end is wide: "The options

market currently implies a 22% probability the S&P 500 ends next year above

3400 and a 28% probability the index ends 2020 below 2600."

In other words, much like the Fed, Goldman appears to have

taken its price target based on what the market is already discounting.

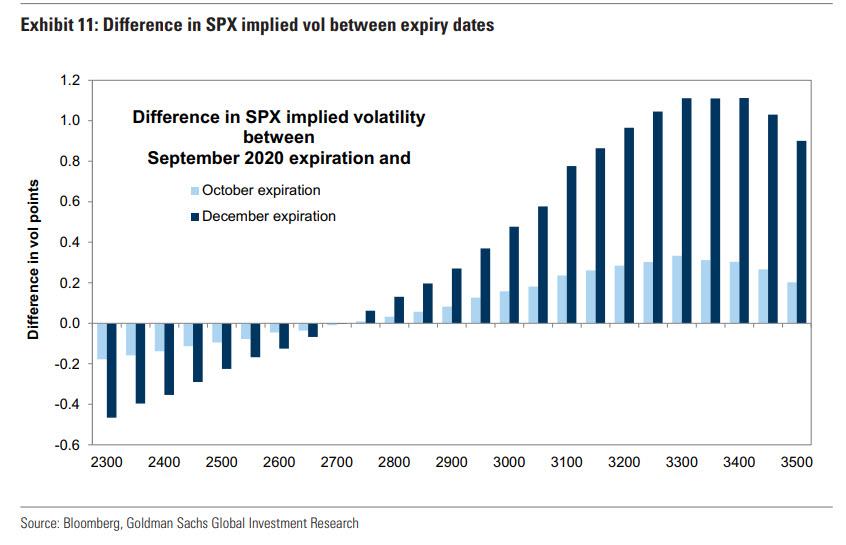

Here, Kostin points out something we noted last week when

analyzing the latest report by Goldman's derivatives strategist Rocky Fishman,

according to whom the options market was indicating "different distributions of risk before and after Election Day."

Skew is higher for the September and October 2020 maturities than for the

November and December 2020 maturities. This can be seen

from the spike in upside implied volatility from October to December and little

gap in downside implied volatility.

See Chart:

Difference in SPX implied volatility between expire dates

{kind=link}

Which brings us to the key issue at the heart of Goldman's

schizophrenic forecast: whether government will be united or divided. This is

how Kostin frames it:

Maxims in politics such as “United we stand,

divided we fall” do not necessarily hold in investing. In the United States, equity returns during periods of divided federal government

have typically exceeded returns achieved when one political party controls the

White House, Senate, and House of Representatives. Since 1928, excluding

recessions, when the federal

government was controlled by a single party, the S&P 500 median 12-month

return equaled 9%. However, the median return under a divided government was 12%. Prediction markets currently suggest the most probable 2020

election outcome is a divided government.

See Chart:

S&P 500 returns based on the control of FED Gvt since 1928

{kind=link}

As Kostin further

adds, "investors focused on equity market implications of policies

discussed on the campaign trail need to take into account the probability that

these outcomes will be realized." What this means is that a candidate

would need to win the presidency, have the support of both chambers of

Congress, and actually pass legislation.

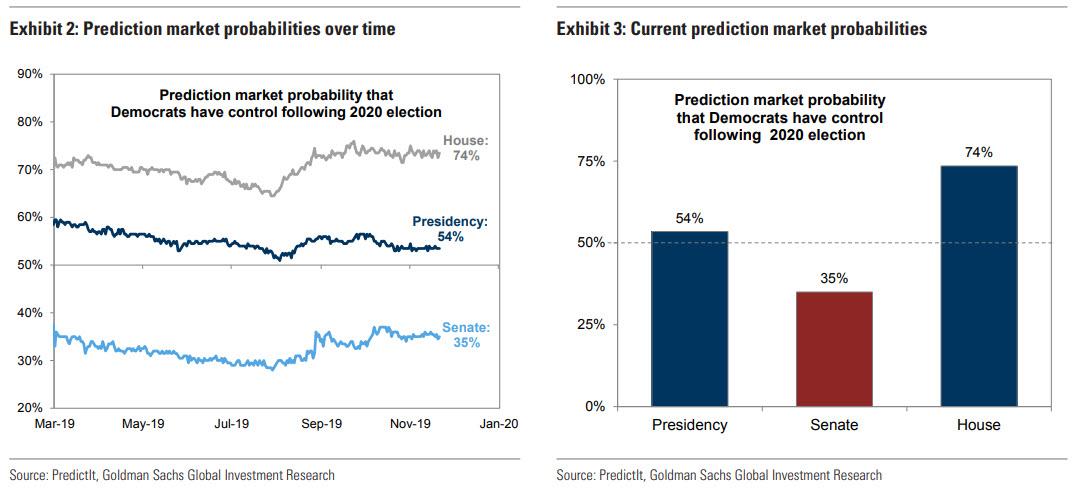

Indicatively,

online prediction markets such as PredictIt- which are notoriously illiquid and

can be easily gamed with one modestly sized wager - currently

assign a 74% probability that Democrats control the House, a 54% likelihood

that they win the presidency, but only a 35% probability that they control the

Senate.

See Charts:

Prediction

Market probabilities over time

{kind=link}

And if the

composition of US government is the dependent variable, the emerging two key

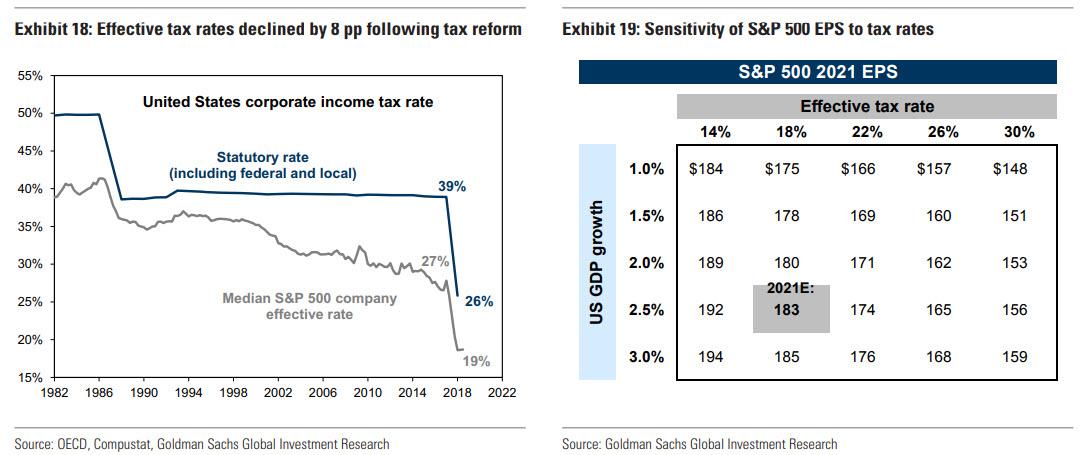

risks to Goldman's baseline forecast are tax rates and tariffs. Kostin

explains:

The S&P 500 YTD effective tax rate has equaled 19%, well below

consensus expectations for 21%. Analyst estimates currently imply a 21% tax

rate in 4Q and in 2020. If the 2019 YTD pattern continues, it could mitigate

likely negative revisions to consensus EPS estimates. However, several

presidential candidates have proposed raising corporate tax rates,and we estimate

every 1 pp change in the effective tax rate would lead to a roughly 1% change

in S&P 500 EPS. Our model suggests a complete

reversal of the tax cut would translate into 2021 EPS of $162 rather than our

current estimate of $183. The impact of tariffs on profits remains highly

uncertain. Recent reports suggest that pending tariffs may be delayed or rolled

back. Currently, tariffs have been levied on roughly $370 billion of imports

from China.

See Charts:

Effective tax rates declined

by 8 pp following tax reforms

And

Sensitivity of S&P 500 EPX to tax rates

{kind=link}

There are also a bunch of secondary variables, or macro

drivers, which will be less dependent on the election outcome yet which will

directly shape the path of the S&P 500: for example, higher interest rates and oil prices provide a boost to

Financials and Energy EPS, respectively, but weigh on the profitability of

companies outside of these sectors. Higher inflation boosts nominal sales

growth but pressure margins, resulting in a modest impact on EPS.

See Table

Sensitivity of our top-down EPS Forecast

{kind=link}

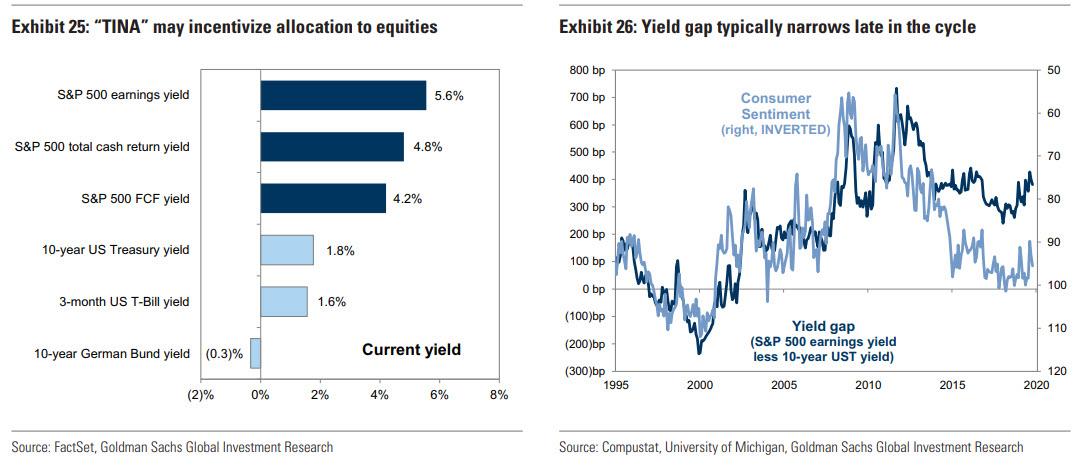

Continue reading and see two more

charts here:

TINA may incentivize allocation of equities

And

Yield Gap typically narrows late in the cycle

{kind=link}

To summarize Goldman's

multi-modal model, no pun intended, the bank expects that as we approach the

2020 election, clarification of policy will expand the P/E multiple to 18.6x

and - assuming a divided government - push the index to 3400 by year-end 2020.

However, should the US end up with a unified government after the election, it

will likely result in lowering 2021 EPS to $162 and compress P/Es to 16x, "resulting in

the index closing next year at 2600."

----

----

----

Strip-mining the planet to maximize profits isn't progressive or

renewable - it's just exploitive

and destructive.

….

It is Trump who will destroy the planet with WW3

to maximize the profits from the 1% & his own profits

====

"Higher stock prices will boost consumer wealth and help increase

confidence, which can also spur spending." -

Ben Bernanke

====

“If you run out of chips,

you are out of the game.”

====

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

...most shocking thing to come out of the hearings thus far is confirmation that no matter who is elected President

of the US, the permanent

government will not allow a change in our aggressive interventionist foreign

policy...

====

Scattered around the nation, there are parts of the

country in which millions of Americans are living without the basic amenities that most of us take for granted...

====

And it has

not Russia, nor China, nor any other enemy, foreign or domestic, to blame...

except for one: the Federal

Reserve Bank of the United States.

In some ways, we sympathize with Neel Kashkari's concern

about the unprecedented wealth inequality that has emerged in the US

in recent years and which has resulted in a slow, methodical

and relentless destruction of the US middle class ... or rather make

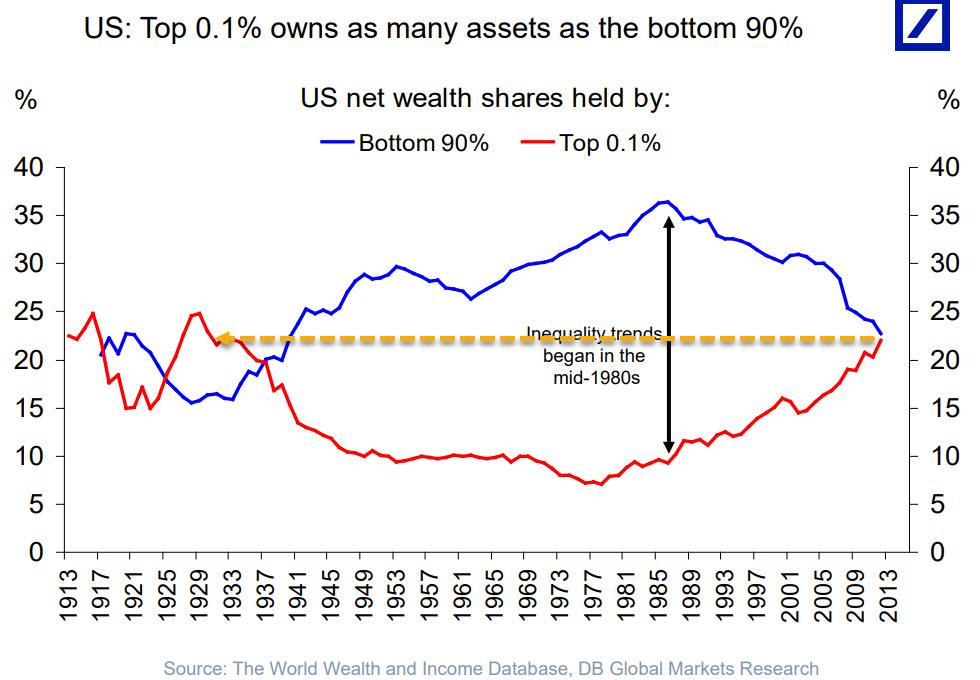

that precedented because

there was another time when the top 0.1% had amassed as

much wealth and it was just before the Great Depression.

See Chart:

US top 1% owns as many assets as the

bottom 90%

{kind=link}

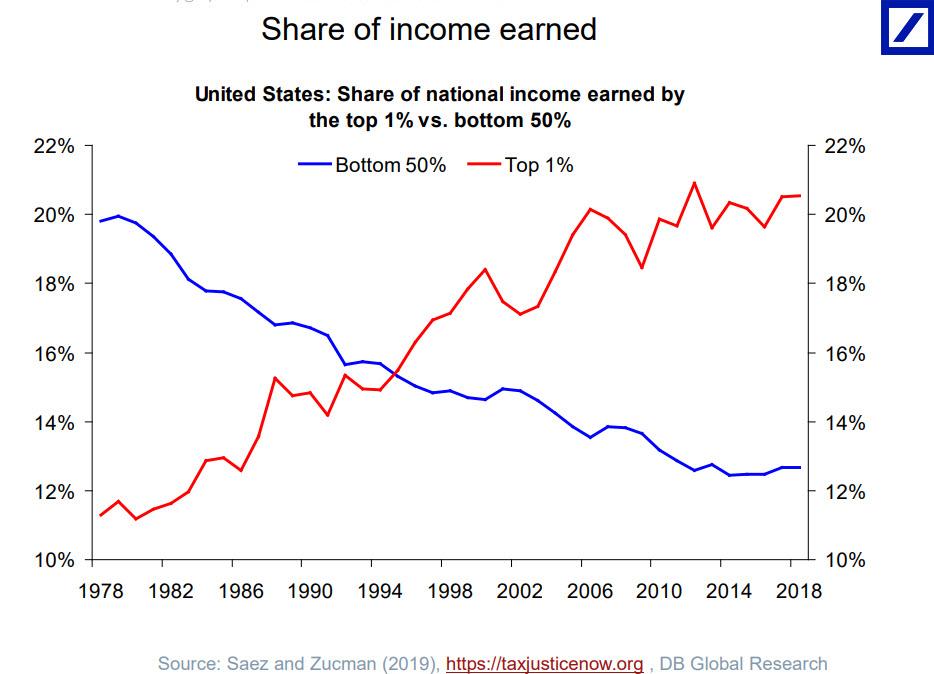

After all, who hasn't seen charts

such as these showing the tremendous divergence in income earned by America's

Top 1% at the expense of the middle and lower classes:

See Chart:

Share of income earned

{kind=link}

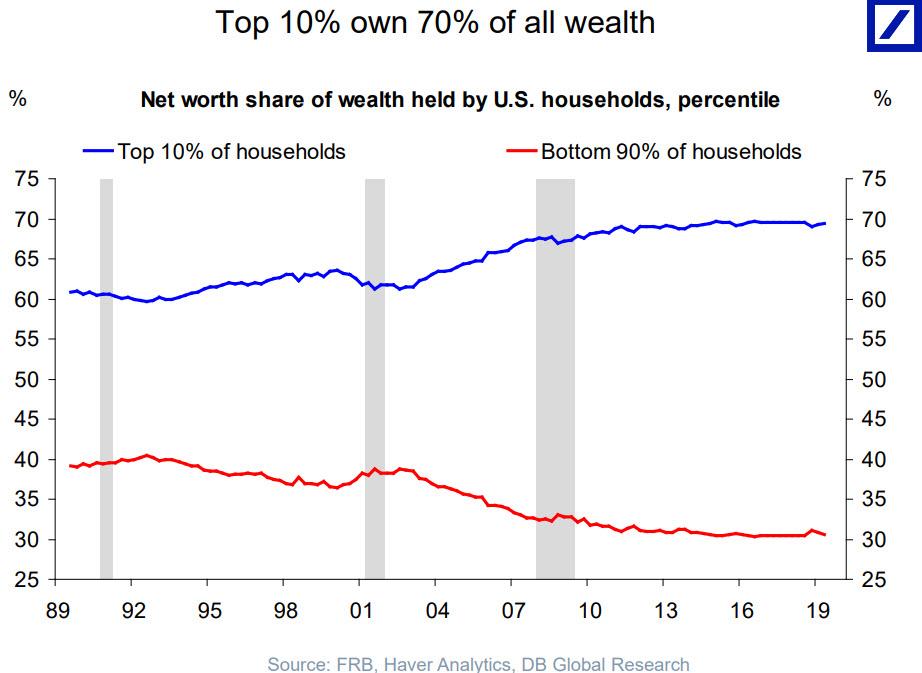

Or that the top 10% now own 70% of

all the US wealth, the same as the middle

and lower classes combined...

See Chart:

Top ten owns 70% of

the wealth

{kind=link}

Yet we find Kashkari's "jaw-dropping" virtue

signalling proposal to grant the Fed wealth redistribution power not only

laughable but absolutely terrifying: after all it was

the Fed's ZIRP and QE that was behind the greatest wealth redistribution in the

past decade...

See Chart:

Growth in Household Wealth ,

1950-2016

{kind=link}

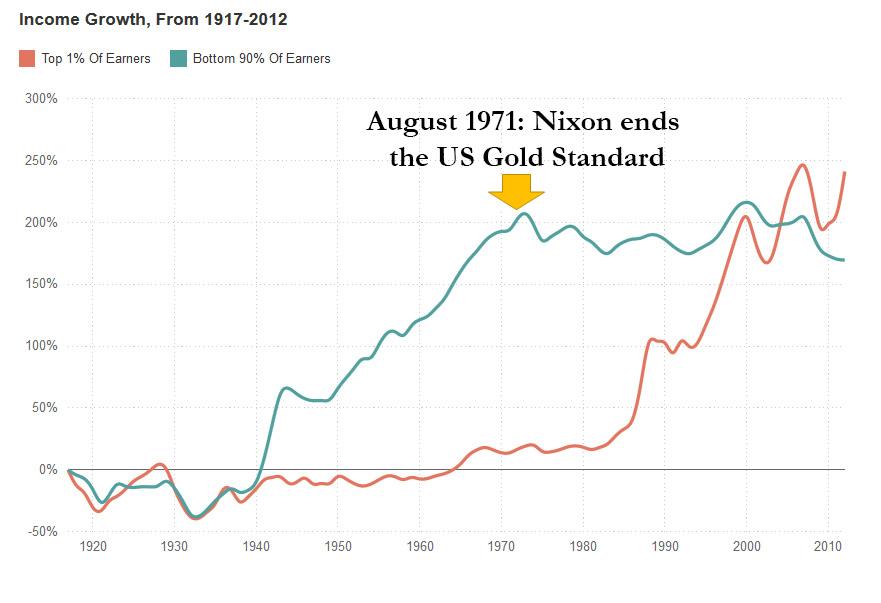

.. a redistribution that started almost 50 years ago,

when Nixon

decided to end the Fed's biggest nemesis - the

US gold standard - launching an unprecedented increase in income growth

for the "Top 1%", even as the income of the

"Bottom 90%" has remained unchanged ever since 1971

See Chart:

August 1971Nixon Ends US ends the US

Gold Standard: start the explosive inequality

{kind=link}

For those confused, Rabobank's Michael Every put it best: of

course the Fed can redistribute wealth but "that redistribution has been from the poor and

middle-class to the rich, not the other way round."

And so, over a decade after the start of the biggest

monetary and wealth redistribution experiment in history intermediated by the

world's central banks, we find ourselves in a place where Deutsche Bank writes

that at the very top of its Top 20 risks for 2020 is none other than the "continued increase in wealth

inequality, income inequality and healthcare inequality."

See Table:

20 Risks to markets in 2020

{kind=link}

To be sure, the issue of wealth and

income inequality is shaping up as the most sensitive topic not only during the

Democratic primary race, but the entire 2020 presidential race, with one

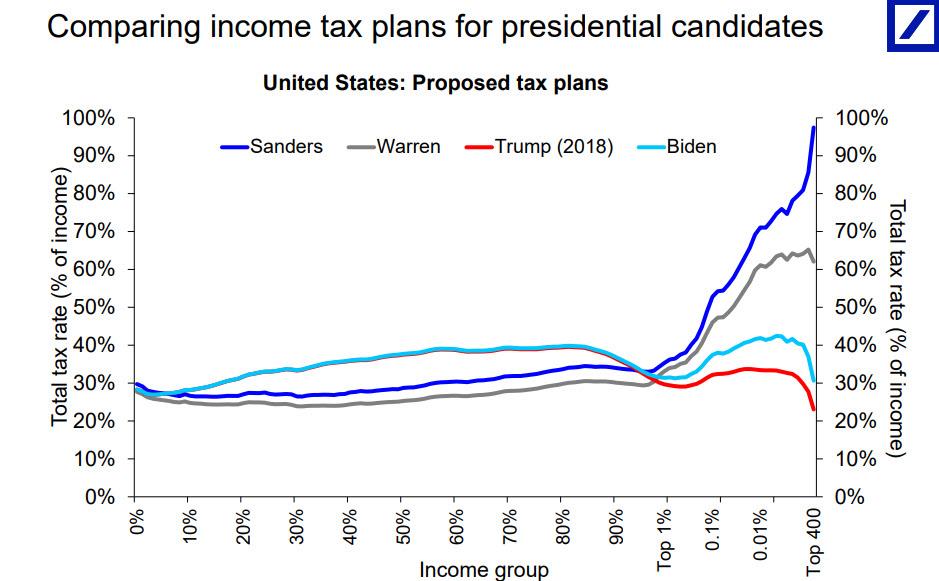

of the most salient questions emerging who can tax the richest the most.

See Chart:

BUT

CONSIDER THIS FIRST:

Al comparar ‘income tax plans for Presid Candidate’ se

incurre en 2 falacias lógicas:

Slippery slow+ Cir-Arg . En Econ el GDP (gasto vs ahorro & deuda

vs inflatio-deflation) depende de 3 actores: el

consumidor, el estado, el inversor, y de ellos depende el rate d import-export en el Mdo mundial. La Politica solo depende solo de 2 actores: el votante y el

Gbo electo. Y en esto los indicadores de Gobernabiliad

lo deciden todo. Se incurre en Slippery Slow cuando se asume un futuro evento sin

probar causación ni su probabalidad causal. Se incurre

en Circular Arg cuando se asume que si A is true, B is true & y a la

inversa. Aquí la causa no es ‘real causa’ ni precede el efecto. ‘A’ es cierto

porque lo dijo el pope o la biblia, u otra autoridad asumida como tal (aqui se

asume que un grafico Stad valida el argumeno).Estas

son FALACIAS LÓGICAS que invalidan un arg como el que se propone arriba: la Econ (taxes) depende de quién es el candidato. Si es Sanders –se asume aqui- los taxes van a subir

y si es Trump, van a bajar. Este razonamiento

ridículo es conocido en el análisis político como “manipulación

pre-fraude-electoral” . El

grafico Stad de abajo ha sido inventado de la

nada: NO se menciona la muestra estudiada: no tiene validez el

argumento: Véanlo:

See Chart:

Comparing Income Tax plans for

Presidential Candidates

{kind=link}

….

----

----

Como darle

vida a la farsa?

...what is being

desperately defended on Capitol Hill is not the rule of law,

national security or fidelity to the Constitution of the United States., but a giant Neocon Lie that is needed to

keep the Empire in business...

====

The great mistake foreign

observers make observing the latest impeachment farce in Washington is assuming that there must be some order,

rationality and linear logic behind it. There is none...

====

Never with Trump in power:

A

surprising number have already made their peace with that...

====

Why do so many American Progressives wish to put even larger swathes of our lives under

political control given their belief that politics is so very easily corrupted by oligarchs and

big-money donors?

====

“No, you don’t understand. It

was the Russians, I tell you, the Russians!”

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

...the world has started to witness an incremental de-dollarization push by a handful of nations.

====

From a big picture perspective, the largest rift in American politics is between

those willing to admit reality and

those clinging to a dishonest

perception of a past that never actually existed...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

Or

Pr: Turquía, ¿aliado o

adversario estadounidense? A

Al-Khaled

México: A contracorriente de Latinoamérica? Óscar García

====

ALAI NET ORG

COL: Habló la diversidad social.

¿La escucharon? Alejo Vargas

====

RT EN ESPAÑOL

Toques de queda y militares en las calles: Colombia

se suma a las protestas contra el neoliberalismo https://actualidad.rt.com/opinion/luis-gonzalo-segura/334794-protestas-colombia-neoliberalismo-ejercito-policia

- La importancia geopolítica del 'Triángulo del

litio' en Sudamérica (y su conexión con el golpe en Bolivia) https://actualidad.rt.com/actualidad/334451-importancia-geopolitica-triangulo-litio-sudamerica

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

-The Lies About Assange Must Stop Now By

John Pilger

- Netanyahu’s Get-out-of-Jail Card... War With

Iran By Finian Cunningham

- Israeli Settlements :Not Only Illegal. They

Are Immoral By Peter Beinart

- Ukrainian Peddling Rings—How Imperial Wash Rolls By David Stockman

- Why the Hell Did Democrats Just Extend the

Patriot Act? By Sam Adler-Bell

- Land of the free? Voter surpression in the US By Molly McCracken

- Eroding Exceptionalism - America In Decline By Mark Hannah

- Deep State Coup D’Etat: from JFK to Trump By Michael Welch et-al

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

----

----

PRESS TV

Middle East n world news

----

====

No hay comentarios:

Publicar un comentario