ND

APR 30 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

“Never gonna let you down?”

BTW - it's not just US markets that

entirely decoupled from fun-durr-mentals...

See Chart:

{kind=link}

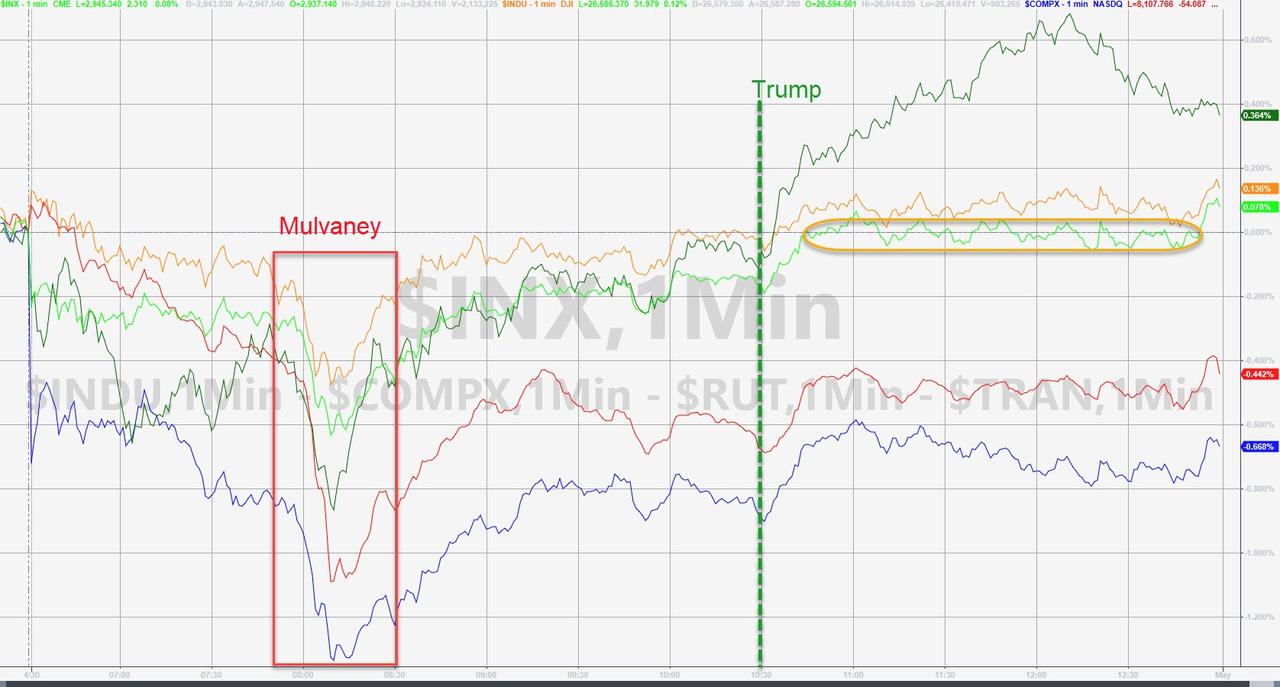

US Stocks lumped into the EU close

(after Mulvaney spooked stocks with China trade deal headlines) and then ripped

back, extending gains after Trump raised the idea of The Fed slashing rates and

QE... S&P was glued to unchanged all afternoon...

See Chart:

{kind=link}

GOOGL spooked Nasdaq futures (as did

weak China PMI and Mulvaney)...

See Chart:

{kind=link}

With investors having hugged their margin clerks for months,

hoping to chase outsized returns during what many have dubbed a melt up, today

they are hugging the toilet bowel instead as the year’s hottest trade in stocks is suffering a huge market-value loss over the

previously noted Google ad revenue meltdown.

See Chart:

{kind=link}

Led by an

earnings-driven sell-off at Alphabet, FAANGs are on

track to lose more than $100 billion in combined capitalization, and are set to suffer their second-biggest market cap drop of

this year.

See Chart:

{kind=link}

The culprit of course was Alphabet, which dropped 8.3% after

its its ad revenue growth posted a sharp slowdown, resulting in a $68.3 billion

market cap loss. The rest of the drop was due to Apple, whose 2.1% drop

resulted in nearly $20 billion wiped out, and came just ahead of Apple’s own

results, due after the market closes. When the FAANGs last saw $100 billion

erased from their valuations, it was after Apple cut its outlook in January, which wiped almost

$70 billion from the iPhone maker’s valuation.

See Chart:

{kind=link}

VIX and Stocks continue to decouple

- Call-buying or protection bid?

See Chart:

{kind=link}

Treasuries were bid, erasing

yesterday's losses...

See Chart:

{kind=link}

10Y Yield roundtripped 5bps

intraday, fading back to 2.50% by the close...

See Chart:

{kind=link}

The Dollar Index slipped for the 4th

day in a row ahead of the FOMC meeting..

See Chart:

DXY Dollar Index

{kind=link}

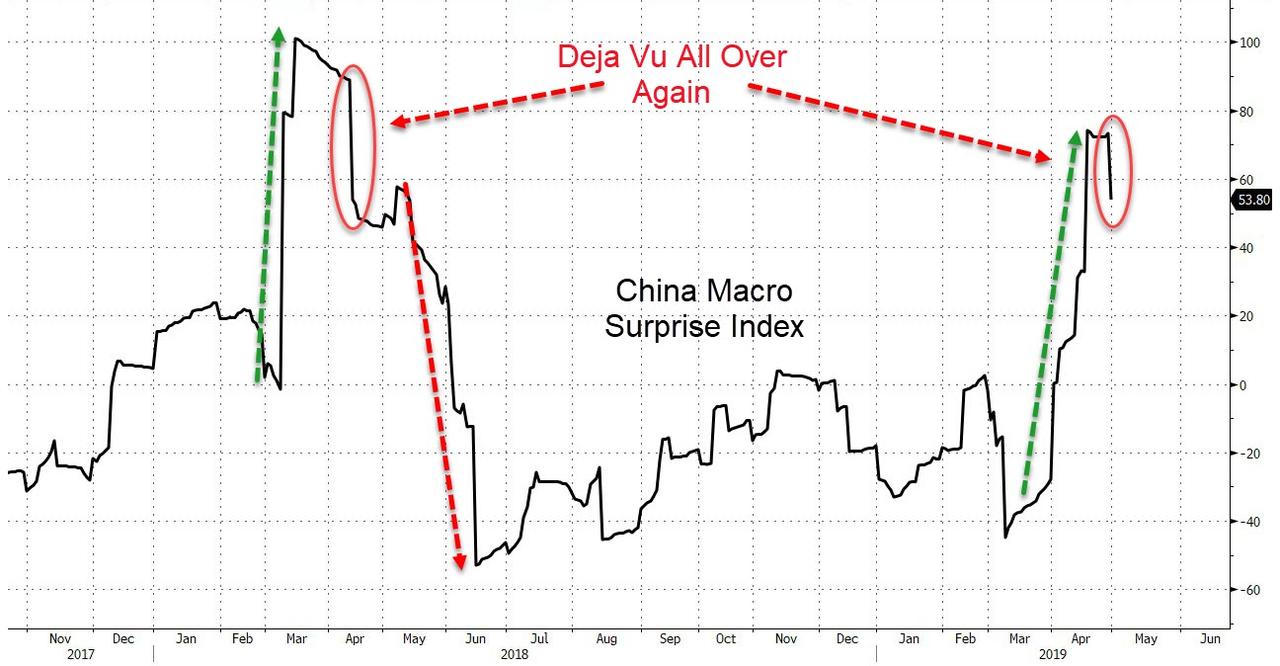

Green Shoots, shot?

See Chart:

China Macro Surprise Index

{kind=link}

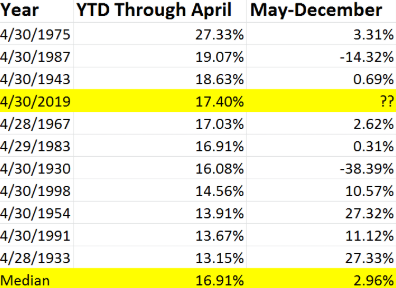

Finally, the S&P 500 is up 17.4%

in 2019, making it the fourth best

start to a year in history.

See Table:

{kind=link}

….

----

----

WTI slipped

back below $64 after API reported a much bigger than expected 6.81mm barrel

crude inventory build in the last week (the 5th in the last 6 weeks)...

Oil prices rallied on the day amid a sliding dollar and

increased protests in Venezuela adding to concerns about supply (despite a

slowdown in China PMI potentially questioning demand).

“The market is currently witnessing the

largest number of barrels subject to potential outage in many years, between

Venezuela, Iran, Nigeria, Algeria and Libya,” said Leo

Mariani, a KeyBanc Capital Markets Inc. analyst.

After a surprise crude build last week, expectations were

for another small stock rise and yet another gasoline drawdown and API did not

disappoint with a large 6.8mm crude build... This is the 11th weekly draw in gasoline (and 7th weekly draw in

distillates) in a row...

See Chart:

{kind=link}

“We have to keep in

mind that with more than 12 million barrels being produced, until we ramp back

those refineries up, we will probably see crude stocks build,” Gene

McGillian, manager of market research at Tradition Energy, says

WTI hovered around $64 ahead of the

API print and knee jerked lower after

See Chart:

{kind=link}

….

----

----

"The

problem for the Fed, is that if growth continues at anything like this pace,

the labor market will tighten much further this year, and the question of rate

hikes will be back on the agenda.”

Tomorrow, at 2pm, the FOMC will leave its rates unchanged.

FEDERAL

FUNDS RATE: Money markets

have assigned a 97.5% probability that the FOMC will keep rates at 2.25-2.50%

this week; there is no chance of a hike, and a very small (but not negligible)

probability of a rate cut.

GROWTH: “The problem for the Fed,” Pantheon says, “is that

if growth continues at anything like this pace, the labour market will tighten

much further this year, and the question of rate hikes will be back on the

agenda.”

INFLATION:

PCE data – the Fed’s preferred measure of inflation – this

week fell to 1.6% Y/Y in March (exp. 1.7%)…

“On a 12-month basis, overall inflation has declined, largely as a

result of lower energy prices; inflation for items other than food and energy

remains near 2 percent.

IOER:

Analysts note that the premium of the Effective Federal

Funds Rate (EFFR) over the Interest On Excess Reserves (IOER) has widened to a

record 4bps recently. Goldman Sachs observes that volume in Fed Funds trading

has slipped by as much as USD 20bln over the last fortnight, with the bank

suggesting it is likely a result of

Federal Home Loan Banks shifting some of its lending into repo markets. .. Goldman therefore assigns a one-in-three chance that

the Fed could cut the IOER rate from the current 2.40% if the EFFR remains at

2.44%, with the bank stating that the probability might increase if the rate

remained elevated into the FOMC meeting.

FINANCIAL

CONDITIONS:

USD is near its all-time highs. UBS says this 1) it

highlights that this cycle is different than 2008, 2001; 2) the USD strength

has a domestic effect, as it offsets the lower rates guidance for 2019; and if this is becoming an increasing

discussion within the Fed, it would most likely appear in the press conference,

and buzzword would be any focus on financial conditions.

ON THE HORIZON.

BofAML think the Fed will soon indicate that it is

comfortable with core PCE inflation in the 1.5-2.5% range. “This would allow a late-cycle overshoot, which is necessary

for inflation to average 2% in the long run. We think the Fed is also being

patient in order to assess downside risks to global growth and determine how

last year’s confidence shock and financial tightening will impact growth.”

PROPOSED MAY FOMC

STATEMENT READLINE, via Goldman Sachs

Information received since the

Federal Open Market Committee met in January March indicates that the labor market remains

strong but and that growth

of economic activity slowed

from its has been rising

at a solid rate in

the fourth quarter . Payroll

employment was little changed in February, but j Job gains have been solid, on

average, in recent months, and the unemployment rate has remained low. Recent

indicators point to slower growth

of suggest that household spending has picked up, while and business

fixed investment grew more

slowly in the first quarter. On a 12-month basis, both overall inflation has declined, largely as a result of lower energy prices; and inflation for items

other than food and energy remains

near have

declined and are running somewhat below 2 percent. On balance, market-based measures of inflation

compensation have remained low in recent months, and survey-based measures of

longer-term inflation expectations are little changed.

…

SOURCE: https://www.zerohedge.com/news/2019-04-30/fomc-preview-goldilocks-sets-stage-rate-hikes-or-cuts

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Advertising fraud online is being called the second largest organized crime scheme globally...

====

...attempting to destroy this with redistribution schemes will ultimately be harmful to the 99%.

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

Bring him home. It’s time...

====

Think tanks

backed by NATO and Saudi Arabia eligible to "investigate" on

behalf of US...

[[ Gatotes en la despensa ]]

====

“A mediocre coup d'etat attempt has failed,” declared Venezuela's defense

minister Vladimir Padrino.

====

"DirecTV,

Net Uno, Intercable, and Telefónica all received orders from Venezuela's

government regulator Conatel to block

CNN."

----

----

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

- 'Greed

of Foreign Investors': JILL STEIN Slams Bolton, Trump for Seeking Regime Change

in Venezuela

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

Áfric Caos permanen de Libia.

Indifer e inercia Robert Charvin

====

ALAI ORG

VEN Detalles d “Calle Sin Retorno” d fuerzas

terroristas JM

US reconoce autoría en intento de golpe de Est a Maduro LL

US reconoce autoría en intento de golpe de Est a Maduro LL

====

RT EN ESPAÑOL

- Un militar venezolano cuenta cómo fue engañado para participar en la intentona golpista

- Rusia: "Si Washington dejara de interferir en los asuntos de Ven, mejoraria la situación"

- ¿Qué países apoyan el golpe de Estado de Venezuela y cuáles se oponen?

- US prohíbe a pilotos d aviones USA volar a menos de 8 kilómetros de altura sobre espacio aéreo venezolano

- Trump amenaza con imponer "un embargo total" y sanciones a Cuba por el apoyo militar a Maduro

- Cómo luce Bs As durante la huelga contra el modelo económico de Macri

- Keiser Report " Implementar la tecnología 5G de Huawei se globalizará y a EE.UU. le gustaría dominar ese mundo"

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

-Venezuela: Military Uprising in Caracas By Venezuelanalysis

- Fanatic Running Trump’s Foreign Policy By Daniel Larison

- Clinton Foundn and ISIS were funded from the

same source By J P n J A

- Blame Palestinians for Gaza By Philip Giraldi

- The New Silk Roads reach the next level By Pepe Escobar

- Why Australians Should Fight To Bring Assange

Home By Caitlin Johnstone

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more business-wars

from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

----

----

PRESS TV

Resume of Global News described by Iranian observers..

====

No hay comentarios:

Publicar un comentario