ND APR 14 19

SIT EC y POL

ND denounce Global-neoliberal debacle y

propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

The gaps

in narratives and in price action are becoming ever more plentiful

and they will have to be

reconciled...

Bears

are rapidly losing the will to live, underinvested bulls are desperately

waiting for a dip, any dip, to emerge to buy and the most complacent are

rewarded with handsome gains. Welcome to every bubble.

Lowest unemployment claims in 50 years,

3.8% unemployment and $JPM reports record earnings with Jamie Dimon, $JPM’s CEO, declaring everything is wonderful but

$SPX closed Friday a mere 1.1% off of the all time human history highs.

No wonder the Fed caved

All joking aside there’s

a widening gap between sentiment and reality.

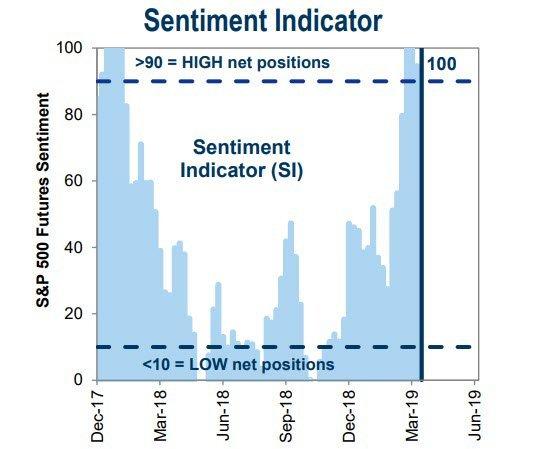

Here’s sentiment:

See Chart:

Sentiment Indic: <10= LOW

net position

{kind=link}

Yet here’s the Citi economic

surprise index:

See Chart:

-62.30 … -6.60

… -11.85%

{kind=link}

Not

even a hint of improvement, yet buyers assume all negatives already to be a

thing of the past. After all $JPM just reported record earnings and $DIS will offer

streaming services at $6.99 that won’t be profitable for 5 years, but that’s

apparently worth adding over $23B market cap to the stock in one day.

The economy is not the stock market, the

stock market is not the economy. The stock market of 2019 is dovish central

banks, buybacks and China trade deal jawboning.

“By one measure, the amount of investment-grade bonds has doubled to $52 trillion since

the financial crisis. And yields have, on average, fallen to

roughly 1.8 percent, less than half the level in 2007. If they were to rise by a mere

half-percentage point, investors could be looking at almost $2 trillion in

losses.

“This is an element of

hidden leverage that is not appreciated,” says Jeffrey Snider, global head of research at Alhambra

Investments. “We are eventually going to have a shock.”

The current situation is a legacy of the easy-money polices enacted by

central banks following the financial crisis. With interest rates at or near zero, governments and

corporations went on a historic borrowing binge — and investors gorged on debt

that yielded little in return.

These worries aren’t new, of course, but they’ve attracted fresh

attention as the amount of negative-yielding debt has climbed past $10

trillion. To some, it’s a sign investors have gotten a little too complacent

and could easily get blindsided once growth and inflation start to pick up.

“The debt

load in the world is so high now that it can’t withstand any

historically-normal size of interest rate increases anymore,” says Stephen Jen, chief executive

officer of Eurizon SLJ Capital”.

The world is trapped in debt. Central bankers are trapped by the very construct

they helped enable. And now, after a torrent 16% rally in the first 3.5

months of 2019 investors are finally turning bullish. The chase

is on.

See

any signs of unidirectional chasing?

Look no further than high

yield:

See Chart:

{kind=link}

Speaking of unidirectional

chasing: Stocks go up forever now, don’t you know?

As outlined in Icarus Warning, it is precisely at these points of historic disconnects, courtesy

forever dovish central banks, that investors are

embracing complacency once again with the $VIX back at 12. The $VIX on

Friday filling the open gap left on the heels of the October swoon when people

were saying a low $VIX is bullish:

See Chart:

NormanTrader.com

{kind=link}

..while markets are running

from open gap to open gap:

See Chart:

{kind=link}

While markets are ignoring these gaps now

they represent target zones for when volatility reawakens from its compressed

slumber. It is precisely these open gaps that represent the achilles heel of

this levitating market as they will become magnets for a future market seeking

to find balance.

But as long as momentum drives price

investor psychology will seek to dismiss all negatives and warning signs.

Case in point: The yield curve

“scare” a few weeks ago? Already long forgotten:

See Chart:

{kind=link}

The “scare” was barely worth a dip in

markets. With all negatives ignored it is precisely the type of environment

that could lead to the blowing off top scenario I described in Combustion.

But because memories are short it may be

worth keeping an eye on the lessons of history. That short yield curve

inversion that is being dismissed as a false positive?

That has happened before as

well:

See Chart:

Recession Start

{kind=link}

Note that little “false signal” in April

2000? Dismissed as a false positive for 3 months. The yield curve then

inverted again and the recession hit a mere 11 months following the original

signal.

The gaps in narratives and in price

action are becoming ever more plentiful and they will have to be reconciled.

Mind

the gaps.

Some of these charts and many others

discussed in more depth in the video below:

….

----

----

...even the upper-middle-class is starting to feel the pain of income

stagnation...

THE ISSUE : being "left behind"

has now spread to all Americans aside from the top 10%, according to Bloomberg.

This means that even the upper middle class is starting

to feel the pain of income stagnation. The growth of upper middle class income continues to lag behind that

of those both lower and higher than them on the socioeconomic ladder, according

to the data.

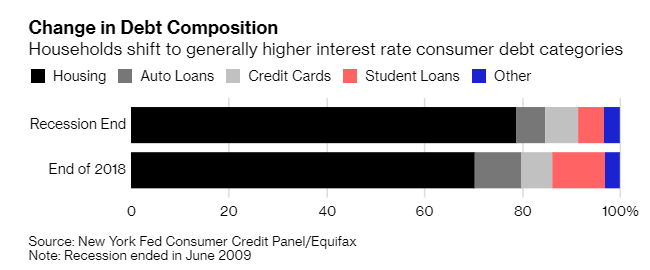

The cost of many items purchased by the

upper middle class, including things like college education and cars, is

outpacing inflation. That is causing upper middle class households to tap into

more expensive forms of debt. The debt these households

is taking on is shifting from mortgages to credit with higher financing

costs.

See Chart:

Change in Debt composition

{kind=link}

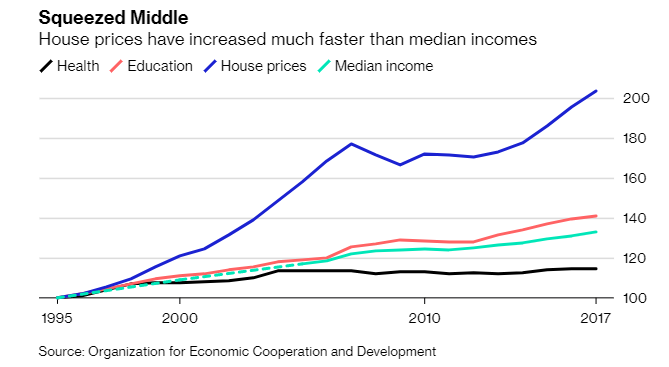

In addition, the overall middle class'

share of total income is falling while home prices have

increased faster than median incomes.

The Organization for Economic Cooperation

and Development said: “The middle class is increasingly only a dream for many. This bedrock of our democracies and economic growth is not as

stable as in the past.”

See Chart:

Squeezed Middle

{kind=link}

Credit card rates recently hit a

"generational high" despite the low prime rate. The spread between the prime rate and credit card interest

rates is at its highest point in almost 10 years.

See Chart:

Debt Service Costs

{kind=link}

2018 property taxes rose by 4% annually,

on average, according to an analysis of more than 87 million U.S. single

family homes by ATTOM Data Solutions.

Todd Teta, chief product officer for

ATTOM Data Solutions said:

“Property

taxes levied on homeowners rose again in 2018 across most of the country. While

many states across the country have imposed caps on how much taxes can go up,

which probably contributed to a slower increase in 2018 versus 2017. There are

still many factors at play that can contribute to local property tax hikes, and

without major changes in the way a community runs public services, tax rates

must rise to pay for them.”

Only incomes in the top 25% were able to

outpace this rate on an annual basis, according to the Atlanta Fed. For everyone else, a greater share of income must be

allocated to property taxes, leaving less to spend on everything else.

See Chart:

Luckluster Gains:

Median 12 Months Wage Grows for

those in the 2nd tier flat-lines

{kind=link}

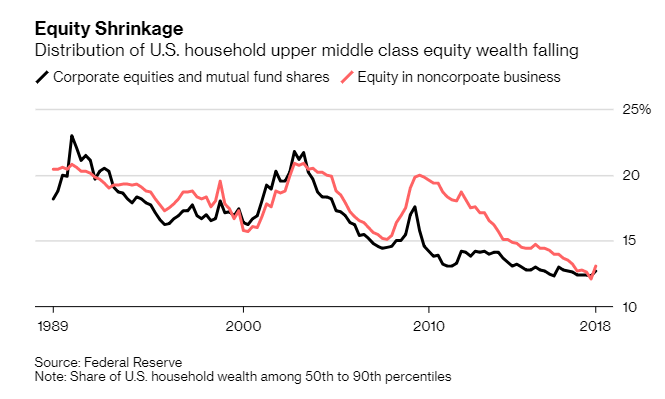

Equity ownership in companies, both

public and private, is also sliding for the upper middle class. The share of equity ownership for citizens in the 50th to

90th percentile of net worth has fallen and the top 1% of Americans still own

the majority of shares.

See Chart:

Equity Shrinkage

{kind=link}

By the end of 2018, net worth

as a share of the U.S. total had shrunk considerably for the upper middle

class. During the course of just one generation, U.S. wealth held by households

from the 50th to the 90th percentile fell from 35.2% of the total to 29.1%.

Most of this wealth has been transferred to the top 1% of U.S.

households.

See Chart:

Smaller slice of the pie

{kind=link}

The OECD defines middle class as households with incomes between 75% and and 200% of the

national median. Over the last 3 decades, incomes have increased 33%

less than the average of the richest 10%, according to the OECD. Real

income of the middle class has grown only 0.3% a year since the financial

crisis.

Stefano Scarpetta, OECD director of

employment, labor and social affairs said: "There

is a risk of a spiral to the extent that the middle class is the one main

sources of political and economic stability."

See Chart:

Middling Millennials

{kind=link}

Rising to the middle class is also

getting tougher. More skills are needed, as more than 50% of middle income

workers are now in high skilled occupations, up from about 33% two decades

ago.

“It’s a wake up call. Overall

there is a need to really focus on targeted policy intervention for those with

specific problems. General policies may not work very well,” Scarpetta concluded.

….

----

----

... the Fed’s

present interest rate policy is nearly 50 basis points too high and

getting wider by the day... too tight for too long, slower growth, lower rates.

In the

Hoisington First Quarter Review, Lacy Hunt blasts MMT as "self-perpetuating" inflation.

See Chart:

{kind=link}

…

SOURCE: https://www.zerohedge.com/news/2019-04-14/lacy-hunt-blasts-mmt-fears-hyperinflation-if-implemented

----

----

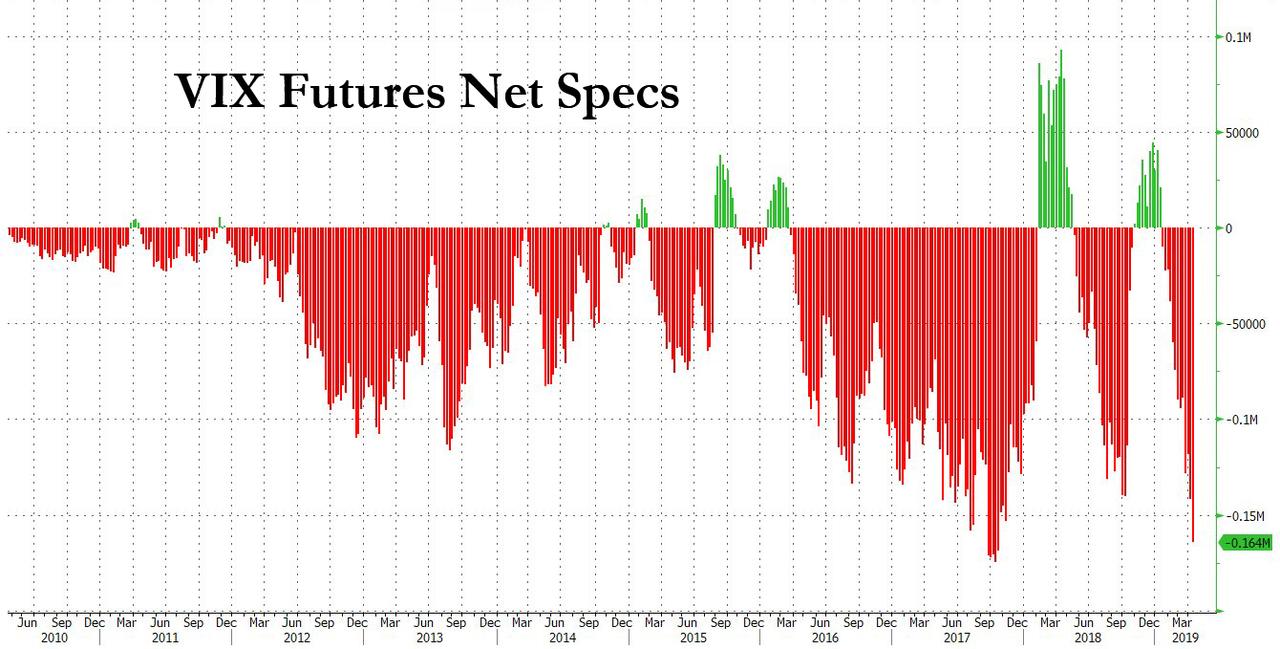

In recent weeks, retail investors have become

convinced that a market crash is imminent while institutional investors have

rarely been more complacent. Who will be right?

See Chart:

VIX Futures Net Specs

{kind=link}

…

----

----

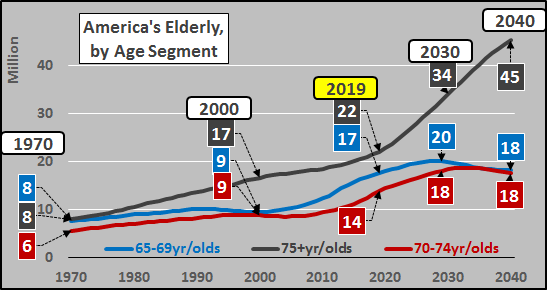

Population growth in America has shifted to the

elderly, that have very low labor force participation rates. Presently,

and for at least the next decade,

there is no clear impetus for further growth in employment...

See Chart:

America’s

elderly by age segment

{kind=link}

See many more RELATED

charts at the source below:

…

----

----

...the message

from lumbershould be paid attention to.

See Chart:

Lumber vs Cooper

{kind=link}

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete;

it’s full of frauds & corruption. Urge cambio

"Buybacks were

illegal throughout most of the 20th century because they were considered

a form of stock market manipulation. But in 1982, the Securities and

Exchange Commission passed rule 10b-18..."

====

"There are all sorts of crazy stuff.The craziest, of course, is that

around 20% or $11 trillion worth of bonds worldwide are priced to yield less

than zero...This is thegreatest non

sequitur in finance..."

====

But

never has China been such a big part of the global economy. Its influence

dwarfs all else. Which renders history mostly meaningless. China is all that

matters.

====

RELATED:

The controversial claim stems from capital gains treatment

of options...

====

"The difference

is solely legal and one of scale. Private counterfeiters are

punished, and rightly so, whereas the Fed is lauded for its actions..."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran

search for State socialis+K-, D rest in limbo

Assange's

arrest represents anabuse of power, highlighting

not only how true journalism has

now been banished in the West, but also how politicians,

journalists, news agencies and think-tanks collude with each other to silence people...

====

Trade war is becoming ugly.. Tit for Tat

expected.. Tax only affect output..Finan: In-D

Chen

Mailin’s son, Ding Chen, posted a message on Instagram complaining about

US$680,000 in taxes on the new supercar, saying they made his ‘heart feel

tired’

[[

We arrived to the end of neoliberal

globalization: USD will collapse soon ]]

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

VIENTO SUR

Demo Claudio

Katz: “Conquistas democráticas van a estar

en gran peligro”

Niklas

Olsen : Cómo el neoliberalismo reinventó la democracia

RT EN ESPAÑOL

- Periodista destapa una reunión secreta en EE.UU. sobre el "uso de la fuerza militar en Venezuela" y publica la lista de participantes

- Irán critica a Europa por "retrasarse" en lanzamiento del canal de pagos que permita sortear las sanciones de EE.UU.

- VIDEO: Israel creará otra sonda Beresheet tras estrellarse la primera en la Luna

- Kim Jong-un advierte sobre un futuro "sombrío y muy peligroso" a menos que EE.UU. adopte la "postura correcta"

- Sistemas S-300 rusos repelen un "ataque masivo con misiles" de un enemigo durante simulacros militares

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis:

neofascism & internal conflicts that favor WW3

- The US Charge Against Assange Is Fraudulent By Caitlin Johnstone

- The Killing of Journalism By Pepe Escobar

- Pardoning Assange: First Step Back Toward

Rule of Law By Thomas Knapp

- Rogue State? – Britain railing against

internat norms and laws By TruePublica:

- Time for Russia to Prepare for War By Paul Craig Roberts

- U.S. Just Declared War on Iran and Nobody

Blinked By Scott Ritter

- Libya: Fruits of US-NATO Regime Change By Tony Cartalucci

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that

leads to more business-wars from US-NATO

allies

- Major

Revelation: Assange

Was Bought for $4.2 Billion – Former Ecuadorian President Confirms IMF Loan In

Exchange For Assange By Paul Antonopoulos,

- Mairead

Maguire Requests Permission to Visit Assange, Nominated for Nobel Prize

By Mairead Maguire,

- Solidarity

with Venezuela: 60 Countries Create Group for the Defense of Peace and the

Principles of the UN Charter By Simon Garcia

----

----

PRESS TV

Resume of Global News described by

Iranian observers..

----

===

No hay comentarios:

Publicar un comentario