ND APR 13 19

SIT EC y POL

ND denounce Global-neoliberal debacle y

propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over.

Financiers know it, they documented with graphics

Historic

levels of debt – check; Major recession

signal proven reliable for 50 years - check; Massive amounts of money being sucked out of the financial system - check!

Authored by Alt-Market's

Brandon Smith, originally published at Birch

Gold Group,

It’s been more than 10 years since the

last economic recession.

Since the U.S. economy generally operates in cycles, it looks like the time is drawing near for

another.

In fact, late last year the Dow Jones

took a dive,

but that was likely just an appetizer for the course to

come…

A recent piece from

Bloomberg reported the risk of

a recession has “more than doubled this year as leading economic indicators

deteriorate, the yield curve inverts and monetary policy tightens,” referencing a note by Guggenheim Partners.

[ INDICATORS of

recession at portas:]

-Debt, Yield

Curve Inversion & QE Signaling Recession Risk

This dangerous “debt

trifecta” has even gotten the attention of several billionaires.

Rising national debt currently tops $22 trillion.

Corporate debt topped $6 trillion at

the end of 2018. And the “ATM” of consumer debt has hit $4

trillion. Americans are tapped out. Combined together, this signal alone

should sound recession alarms.

But

this is just one of multiple major warning signs…

The yield curve is dangerously close to

inverting at only 16

basis points between 2- and 10-year treasuries. What’s even more

troubling is yield curve inversion has preceded every major recession over the

last 50 years.

The third big warning sign comes from the

Federal Reserve. They used Quantitative Easing (QE) to

help bring the economy out of the depths of the last recession. But

right now that process is going in reverse. In other words, they are sucking hundreds

of billions of dollars out of the banking system in a process

called Quantitative Tightening.

The Fed said they would stop

unwinding QE in September. But for now,

Wolf Richter reports this unwinding process is still on “autopilot”

at $535

billion and counting.

So let’s review our recession risk:

- Historic levels of debt — check

- Major recession signal proven reliable for 50 years — check

- Massive amounts of money being sucked out of the financial system — check

It’s pretty clear why Guggenheim is so

worried. In fact, would not surprise us if their

warnings are confirmed in the very near future.

….

SOURCE: https://www.zerohedge.com/news/2019-04-13/imminent-recession-risk-doubled-3-signals-sounding-alarm

----

----

[[

Neil Kearns is Interview by Goldman on BUYBACKS ]]

Meet

Neil Kearns, a name few have previously heard of. He may well be the most

powerful person on Wall Street today.

Amid a rising legislative chorus

demanding a halt to corporate buybacks (an activity

which was illegal until 1982), with Congress realizing that most of the

funds released by Trump's tax cut and offshore tax repatriation were used not

for capex or hiring but merely to levitate stock prices, last

week Goldman's chief equity strategist published the most

"inspired" defense of buybacks, in which he said that from a

portfolio strategy perspective:

"the

potential restriction on buybacks would likely have five implications for the

US equity market: (1) slow EPS growth; (2) boost cash spending on dividends,

M&A, and debt paydown; (3) widen trading ranges; (4) reduce demand for

shares; and (5) lower company valuations."

Or, as

we summarized it, if Congress were to ban buybacks, it would likely crash the market. Hence Goldman's increasingly

vocal defense of corporate buybacks, which

incidentally are the biggest source of stock demand in

the past decade..

Then, just a few days later, Goldman -

clearly worried that the anti-buyback push is gathering steam in Congress -

published yet another research report discussing the "Buyback

Realities", in which it paradoxically tried

to mitigate the role buybacks have on price formation and capital misallocation

just one week after it explained how banning buybacks would have disastrous

consequences for stocks.

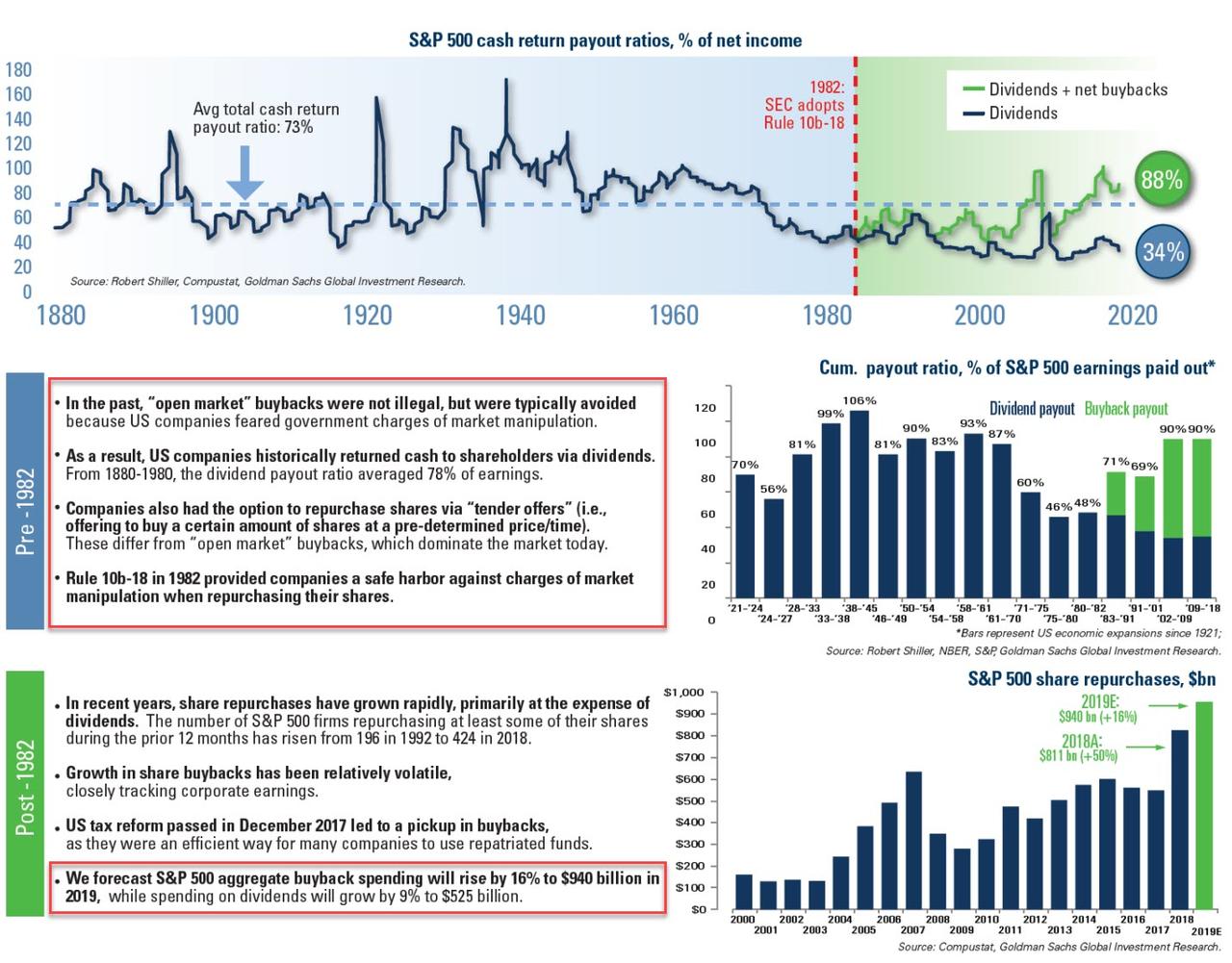

Goldman explained that "in the past buybacks were not illegal [ZH: they

were illegal prior to 1982] but were typically avoided because

US companies feared government charges of market

manipulation."

[[ Just what

we have now: Trump ‘ manipulation to keep his candidacy in election 2020 alive

]]

As a result, for decades US companies returned cash

to shareholders almost exclusively via dividends, and from 1880 to 1980,

the dividend payout ratio averaged 78% of earnings (companies

also had the option to repurchase shares via tender offers, in which they would buy a certain amount of shares at a pre-determined

price/time, however the price moving impact of such operations was

virtually nil).

Then, everything

changed in 1982 with the passage of Rule 10b-18,

which provided companies a safe harbor against charges

of market manipulation when repurchasing their shares.

In short, buybacks were illegal until 1982 for a reason - market

manipulation- and then they gradually became mainstream, with

stock buybacks and dividends rising to 90% of the cumulative payout ratio of

S&P 500 earnings in the 2002-2018 period. The

cherry on top: in 2019, Goldman forecasts companies will

spend a record $940 billion on buybacks (with $1.1 trillion in buyback

announcements) up 16% from the prior record hit in

2018. See Charts below.

[[ This billionaires gula is what we called Neoliberal Economics .. We will explain later the Economic damage it cost

to our nation.]]

See Charts:

{kind=link}

Some more staggering context: since the 2008 financial crisis, the S&P 500 companies

have repurchased about $5 trillion of their own shares, which represents

approximately 20% of the current market capitalization.

So while it remains to be seen if

Congress will ban buybacks, one thing is certain: as Goldman's David

Kostin cautioned last week, without company buybacks, demand for shares

would fall dramatically, for one simple reason: repurchases have consistently been the largest

source of US equity demand. Since

2010, corporate demand for shares has far exceeded demand from all other

investor categories combined. Net buybacks for all US equities averaged $420

billion annually during the past nine years. In

contrast, during this period, average

annual equity demand from households, mutual funds, pension funds, and foreign

investors was less than $10 billion for each category – despite the fact these

categories collectively own 83% of corporate equities.

Buybacks represented the largest source of equity demand in 2018. This is shown in

the table below.

See Table

Corporations are the largest

source of Equity Demand

{kind=link}

Then, overnight, Kostin reiterated this

point, saying that "buybacks remain the largest

source of net demand for US equities. Other ownership categories have been

generally reducing equity exposure, including mutual funds."

What this means is the following: with buybacks having become the most important marginal buyer

of stocks, the one trading desk that dominates the daily flow of

buybacks - which amount to just under $3 billion in

gross purchases each and every day - has more influence on the overall

market than even the NY Fed. And the person who

controls that trading desk will be the most powerful person on W St: Neil Kearns.

Meet Neil

Kearns.

Kearns, besides Stevie Cohen, Israel Englander, Larry Fink, Lloyd Blankfein,

Jamie Dimon, Bill Dudley and any other hedge fund billionaire, is part of the Wall Street folklore - is the head of Goldman Sachs’ corporate trading desk: the desk that executes hundreds of

billions in corporate buyback orders for clients all around the world. Neil is the most powerful man

on Wall Street right now.

In its latest "Top of Mind" publication,

Goldman sat down with Kearns, this "master of the buyback universe", to address the size, impact, and outlook for US share

repurchases. Since Neil is the man that sees more buyback dollars

executed in any year than anyone else, he is just the right man to answer all

buyback related questions.

[ Here the

questions ]

Q: How large is the corporate bid in the stock market?

Q: What is the major driver of volatility in share

repurchases?

Q: How much seasonality is there in share repurchases?

Q: We are in the midst of a blackout window for

share repurchases, which occurs four times a year around quarterly earnings.

Does that mean companies can’t buy stock?

Q: How do companies judge the success of their stock repurchase

programs?

Q: How would you judge investor focus on stock

buybacks today?

Q: Do you see any evidence that the corporate bid is diminishing,

especially given increased focus in Washington, DC?

To read all answers open the source below:

Regarding these answers I would like to know the opinion of Michael Hudson, Richard Wolff, James Petras, Atilio Boron,

Michael Snyder on this regard.

----

----

In

recent weeks, retail investors have become convinced that a market crash is

imminent while institutional investors have rarely been more complacent. Who

will be right?

Back in January 2018, just weeks ahead of

the infamous VIX termination event on Feb. 5 2018 that wiped out virtually all

inverse VIX ETPs in seconds, we

predicted that such an event was imminent as a result of a sharp spike

in the total outstanding Vega across the entire levered and inverse volatility

derivative space, which had reached an all time high. Since then, while the VIX

ETP market had been relatively quiet as a result of last year's fireworks which

wiped out countless retail investors and other vol sellers, another VIX "event" is coming, and it will be the

result of a silent war being waged between retail and institutional investors.

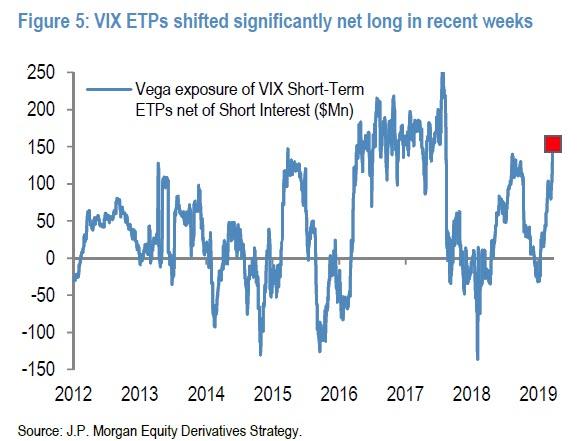

As we noted two

weeks ago, JPMorgan's Bram Kaplan recently pointed out that after a year of

relative quiet, the net exposure among VIX ETPs recently spiked to their

largest net long position in 1.5 years, tilted long by ~$150Mn vega, which is

just shy of the record vega exposure hit in early 2018 and which precipitated

the VIX ETP implosion. However, unlike

2018, this time the

trade is in the other direction as

investors piled into long and levered VIX ETPs beginning in February, as

soon as the VIX index fell below 16, to as JPM

suggests. "position for/speculate on the next volatility spike."

See Chart:

VIX ETPs shift significantly

net long in recent weeks

{kind=link}

However, when it comes to asset flows in 2019

- which has seen the S&P rise back to all time

highs even as equity investors have been pulling money from equity funds week

after week - here too the situation is not nearly as simple.

Commenting on the latest VIX flows,

Deutsche Bank's Parag Thatte reiterates JPMorgan's point, observing that long VIX ETPs have seen significant inflows totaling $2bn

YTD, as retail investors hedge equity gains. This

record inflow into VIX ETPs, amounting to $2 billion in notional, is shown on

the chart below.

See Chart:

{kind=link}

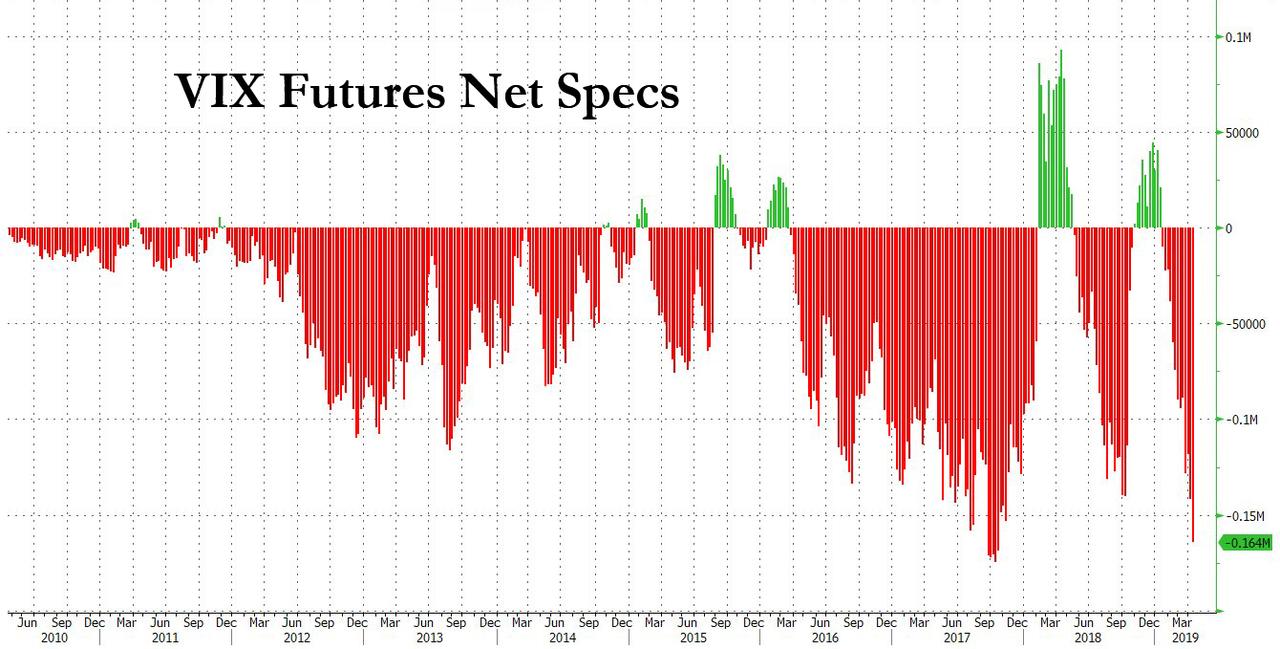

Yet while retail investors,

which traditionally prefer ETPs to hedge exposure, have been loading up on crash bets, institutional

investors which traditionally prefer the greater liquidity of the futures

market, are taking the other side of the volatility

trade and as the latest CFTC commitment of traders report shows, THE

SPECULATIVE NET SHORT POSITION IN VIX FUTURES IS APPROACHING A RECORD,

See Chart:

VIX Futures NET Specs

{kind=link}

If one believes institutions, one look at

the chart above confirms that not only is market complacency greater than its

was either ahead of the Q4 mini bear market and February 2018 Volmageddon, but

it is just shy of a record.

And so the question emerges: who is right - retail investors, who are not only pulling

billions from equity funds but have pushed their crash bets to all time highs

via VIX ETPs, or institutions, who oddly are on the other end of the spectrum,

and not are complacent to an almost record degree, but

in their pursuit of yield and carry trades have pushed the net VIX futs short

position to unprecedented levels. And while conventional wisdom would

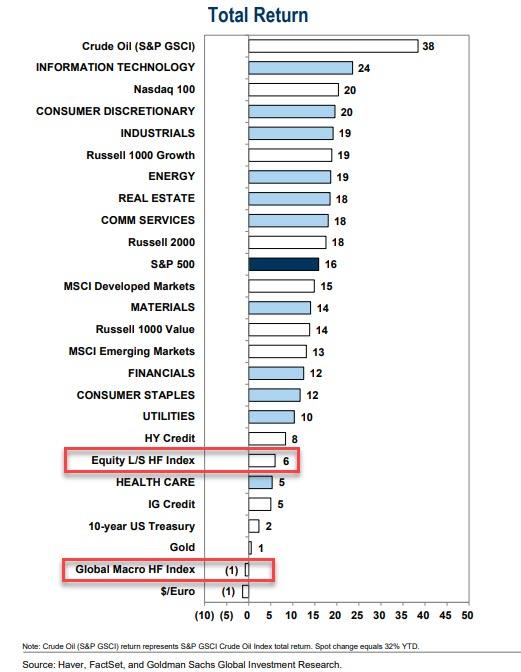

say that institutions, i.e., the smart money is always right, for the 9th year

in a row, hedge funds and their peers are

underperforming the market (with macro funds getting demolished once again).

See Chart:

Total Return

{kind=link}

So who will be right - retail

or institutions. Since both positions are at or near record levels, the answer

should emerge in the very near future.

….

----

----

Make time to read this one:

“If you understand valuations and market history, you know we’re not joking.”

There are three principal

phases of a bull market: the first is represented by reviving confidence in the future of

business; the second is the response of stock prices to the known improvement

in corporate earnings, and the third is the period when speculation is rampant

– a period when stocks are advanced on hopes and expectations.

There are three principal

phases of a bear market: the first represents the abandonment of the hopes upon which stocks

were purchased at inflated prices; the second reflects selling due to decreased

business and earnings, and the third is caused by distress selling of sound

securities, regardless of their value, by those who must find a cash market for

at least a portion of their assets.

– Robert Rhea, The Dow Theory, 1932

– Robert Rhea, The Dow Theory, 1932

The recent bull

market clocked in as the longest in history. Even if the September 20, 2018 peak in the S&P 500 was the final

high, the preceding advance outlived the 1990-2000 bull market by nearly 8

weeks.

Meanwhile, based on the valuation measures we find

best-correlated with actual subsequent market returns across history, the

current market extreme already matches or exceeds those of the 1929 and 2000

peaks.

There’s little question that the market

is long into what Rhea described as the final phase of the bull market; “the

period when speculation is rampant – a period when stocks are advanced on hopes

and expectations.”

As I’ll detail below, the economic expansion we’ve

observed since the 2009 economic low has been a rather standard mean-reverting

recovery, with a trajectory no different than could have been projected on the

basis of wholly non-monetary variables. The primary effect of extraordinary monetary policy wasn’t to drive real

economic gains, but instead to amplify speculation and contribute to wealth and

income disparities. Wages and salaries as a share of GDP are clawing higher

from the historic low set in 2011, but have only begun to erode the elevated

profit margins on which Wall Street is basing its permanent hopes and

expectations.

Continue reading at the source

below:

…

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete;

it’s full of frauds & corruption. Urge cambio

Take away that punch bowl, good man...

====

US Politics degrade you more

than porns.. It would be fine if LAS VEGAS

brothel is closed, but top politician,

very top ones, invested in this type of business

as they do in wars. If they don’t invest, they are the whores of politics ready

to sell their soul to Saudis & other royalties of the world. That degrade

our nation more than porns. Regarding taxing our Nation already victimized with

exclusion, racism, class exploitation and many injustices, better cut their taxes

and/or return their money.

The only way that those living in our fair state

could have uncensored Internet access would be to prove they are at least 18 years old and pay a $20 unblocking fee to the

state...

====

Forget

debt and deflation: the biggest threat to the global economy and the future of

modern civilization as we know it, may be demographics.

====

San

Francisco judges have been a persistent thorn in the side of the administration

as it seeks to implement its immigration agenda.

====

The

migrants were attacking local

police in the Mexican village of Metapa...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran

search for State socialis+K-, D rest in limbo

Killing innocent people in Syria.. what a

nasty way of celebrating Election victory

Syria's

newly installed Russian S-300 system reportedly not used.

====

ARE we really a FASCIST regime?

...you can’t

just go around imprisoning journalists willy-nilly simply for telling the truthabout

your government. That’s something other

countries do, bad countries, the kind of country the US routinely

invades...

====

Belmarsh

Prison holds terrorists and some of Britain's "most notorious

inmates"

====

We

must "stand with victims of sexual violence."

====

Japan

recorded a record net inflow of more than 161,000 migrants, but the overall

pace of decline still hit a new high of minus 0.21%.

====

"The

Western liberal model of development, which particularly stipulates

a partial loss of national sovereignty...is losing its attractiveness and is no more viewed as a perfect model for

all..."

====

"Looks

like at least one Ecuadorian government subdomain has been

hijacked."

====

"But to

hell with that. Let the thugs go in. Directed by the quasi-fascists

in Trump’s Washington..."

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

Blase

Bonpane, ¡presente! Amy Goodman y Denis Moynihan

Políticas

culturales: ¿El futuro ya pasó? Angel Marqués

De 10 de abril en 10 de abril Luis

Toledo

====

ALAI ORG

====

RT EN ESPAÑOL

- "Historias demenciales": WikiLeaks responde a sugerencia de Ecuador de que Assange usó su gato para espiar

- USA promete al "nuevo gobierno" de Ven financiación del comercio por un total de 10.000 millones de dólares

- Maduro solicita otorgar rango constituc a la Milicia Nacional Bolivariana

- El avión más grande del mundo realiza su primer vuelo

- Netflix pierde 8.000 mill de USD tras el anuncio del lanzamiento de Disney+

- 'Hackean' tres servidores del FBI y "más de 1.000 sitios" y afirman haber recogido "más de un millón de datos" Roban huevos al águila asesina

- WikiLeaks distrib imág del gato de Assange mirando la detenc de su dueño

- Presid de Cuba presenta medidas contra los ataques económicos de EE.UU.

- Pompeo viaja al Sur para reforzar rechazo contra Maduro

- Keiser Report ¿Fracaso del capitalismo... o del monetarismo?

- El Zoom Assange: preso de la verdad

----

----

PARA MAÑANA:

INFORMATION CLEARING HOUSE

Deep on the US political crisis:

neofascism & internal conflicts that favor WW3

====

COUNTER PUNCH

Analysis on US Politics & Geopolitics

====

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that

leads to more business-wars from US-NATO

allies

====

DEMOCRACY NOW

Amy Goodman’ team

====

PRESS TV

Resume of Global News described by

Iranian observers..

----

===

No hay comentarios:

Publicar un comentario