RECESSIONS ARE A GOOD THING, LET THEM HAPPEN

That is a Big lie: Recession only bring huge money to big Corp & billonaires.

Hugo Adan

10/17/2020

But we must read them to know how they create the big monster & how it works

This is the best art I read on the neoliberal system that is collapsing now

It is a defense of big Corp & Billionaires: an insult to the labor or working classes

Pero no hay nada mejor que conocer bien al enemigo de clase y saber dónde golpear

Pronto enviaré mis notas criticas al respecto. Por lo pronto lo comparto con Uds.

….

….

RECESSIONS ARE A GOOD THING, LET THEM HAPPEN

Authored by Lance Roberts via RealInvestmentAdvice.com,

https://www.zerohedge.com/markets/recessions-are-good-thing-let-them-happen

Trying to delay the inevitable

only makes the inevitable be much worse in the end...

Wildfires, like recessions, are a natural part of the environment. They are nature’s way of clearing out the dead litter on forest floors, allowing essential nutrients to return to the soil. As the soil enrichens, it enables a new healthy beginning for plants and animals. Fires also play an essential role in the reproduction of some plants.

No Tolerance For Recessions

Following the century’s turn, the Fed’s constant growth mentality exacerbated rising inequality and financial instability. Rather than allowing the economy to perform its Darwinian function of “weeding out the weak,” the Fed chose to “mismanage the forest.” The consequence is that “forest fires” are more frequent.

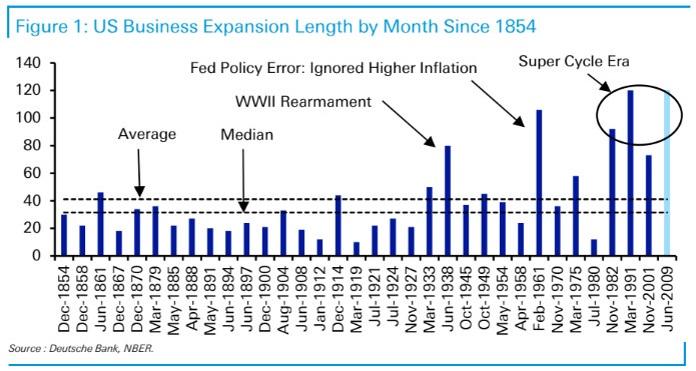

Deutsche Bank strategists Jim Reid and Craig Nicol previously wrote a report that echos what other Austrian School economists and I have been saying.

“Actions are taken by governments and central banks to extend business cycles and prevent recessions lead to more severe recessions in the end.”

See Chart:

US Business expansion length by Months since 1854

https://www.zerohedge.com/s3/files/inline-images/DeutscheBankReidChart-1_0.jpg?itok=9-5T7XNw

{kind=link}

Prolonged expansions had become the norm since the early 1970s, when President Nixon broke the tight link between the dollar and gold. The last four expansions are among the six longest in U.S. history .

Why so? Freed from the constraints of a gold-backed currency, governments and central banks have grown far more aggressive in combating downturns. They’ve boosted spending, slashed interest rates or taken other unorthodox steps to stimulate the economy.” – MarketWatch

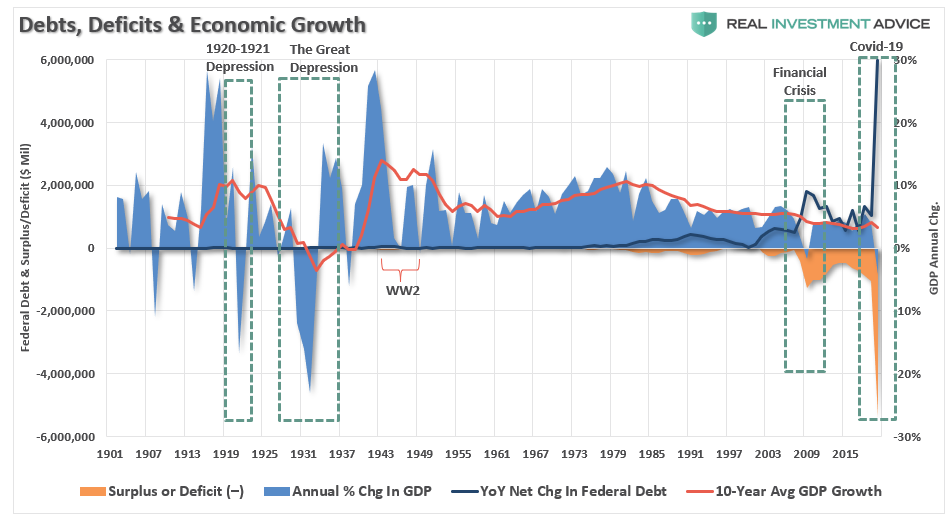

See Chart

Debts, Deficits & Economic Growth

{kind=link}

But therein also lies the problem.

MORE DEBT LEADS TO LESS OF EVERYTHING ELSE

The massive indulgence in debt, what the Austrians refer to as a “credit induced boom,” has now reached its inevitable conclusion. The unsustainable credit-sourced boom leads to artificially stimulated borrowing, seeking out diminishing investment opportunities.

Ultimately, diminished investment opportunities lead to widespread malinvestments. Not surprisingly, we saw it play out “real-time” in everything from subprime mortgages to derivative instruments previously.

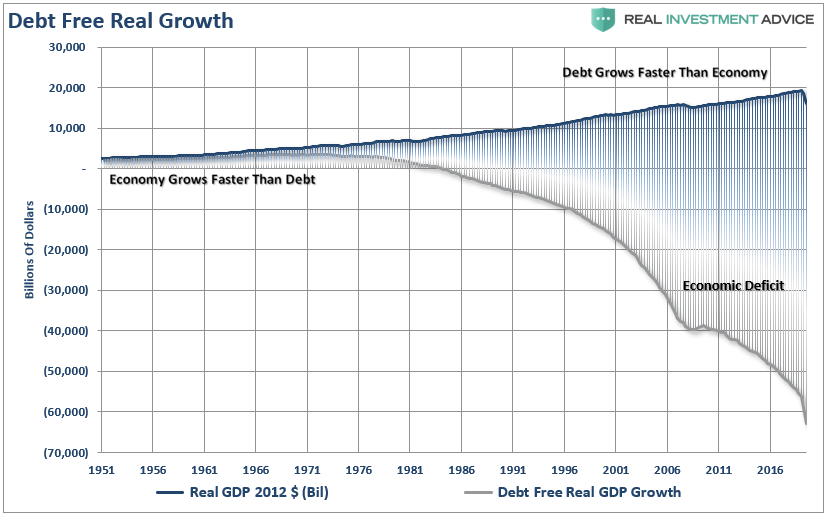

See Chart:

Debt Free Real Growth

{kind=link}

When credit creation can is no longer sustainable, the markets must clear the excesses before the cycle can restart. Only then, and must be allowed to happen, can resources be allocated towards more efficient uses.

Such is why all the efforts of Keynesian policies to stimulate growth in the economy have ultimately failed. The ongoing fiscal and monetary policies, from TARP and QE to tax cuts, only delayed the clearing process allowing it to grow larger. That delay worsens the current impact and the eventual reversion.

The economy currently requires roughly $5 of total credit market debt to create $1 of economic growth. A reversion to a structurally manageable debt level would require a reduction of nearly $40 trillion. The last time such a clearing process occurred, it was called the “Great Depression.”

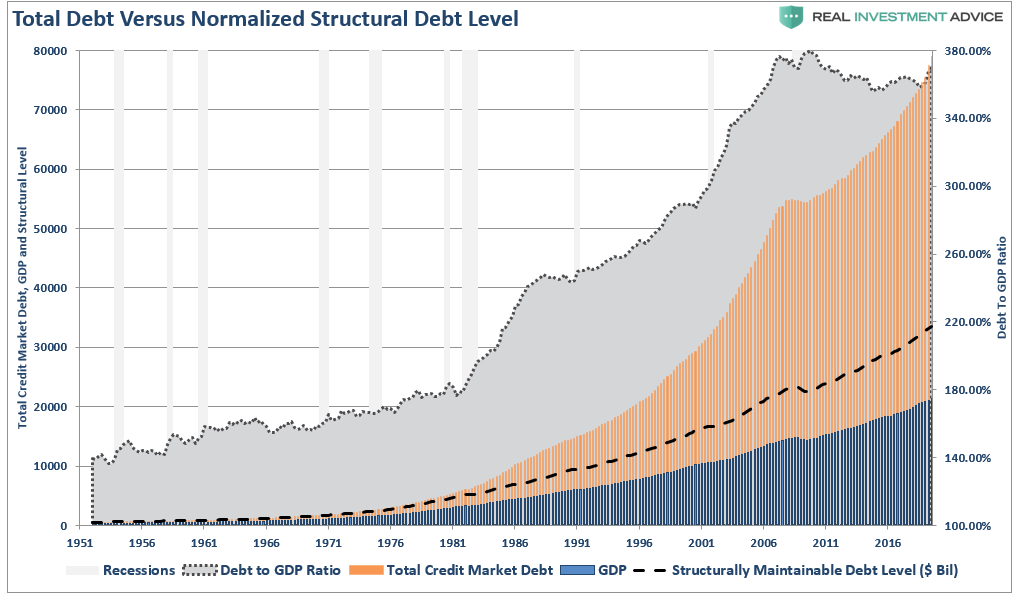

See Chart:

Total Debt versus normalized structural debt level

{kind=link}

The chart shows why “demands for socialism” is now “ a good thing.”

Austrian Theory Of Business Cycles

“As the inevitable consequence of excessive growth in bank credit, exacerbated by inherently damaging and ineffective central bank policies, which cause interest rates to remain too low for too long, resulting in excessive credit creation, speculative economic bubbles, and lowered savings.”

In other words, the proponents of Austrian economics believe that a sustained period of low rates and excessive credit creation results in a volatile and unstable imbalance between saving and investment. In other words, low rates tend to stimulate borrowing from the banking system that, in turn, leads, as one would expect, to the expansion of credit. This expansion of credit then, in turn, creates an expansion of the supply of money.

See Chart:

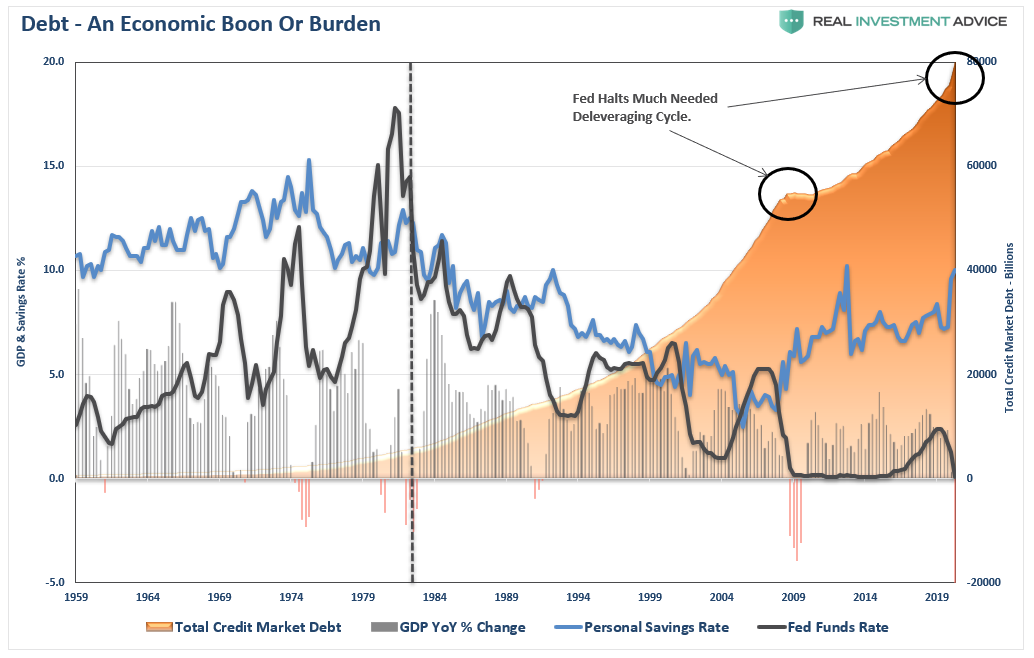

Debt: An Economic Boon Or Burden

{kind=link}

Therefore, as one would ultimately expect, the credit-sourced boom becomes unsustainable as artificially stimulated borrowing seeks out diminishing investment opportunities, ultimately resulting in widespread malinvestments.

When the exponential credit creation is longer sustainable, a “credit contraction” occurs. Such ultimately shrinks the money supply and the markets finally “clear.” The clearing process allows resources to be allocated back towards more efficient and productive uses.

As shown in the chart above, the Federal Reserve’s actions halted the much needed deleveraging of the household balance sheet. With incomes stagnant and debt levels still high, it is worth little wonder why 80% of Americans currently have little or no “savings” to meet an everyday emergency.

Furthermore, the velocity of money has plunged as overall aggregate demand has waned.

Monetary Velocity

What the Federal Reserve has failed to grasp is that monetary policy is “deflationary” when “debt” is required to fund it.

What is “monetary velocity?”

How do we know this? Monetary velocity tells the story.

“The velocity of money is important for measuring the rate at which money in circulation converts into purchasing of goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

With each monetary policy intervention, money velocity has slowed along with the breadth and economic activity strength.

See Chart:

Fed Balance Sheet vs Monetary Velocity

{kind=link}

However, it isn’t just the Fed’s balance sheet expansion, which undermines the economy’s strength. It is also the ongoing suppression of interest rates to try and stimulate economic activity.

In 2000, the Fed “crossed the Rubicon,” whereby lowering interest rates did not stimulate economic activity. Instead, the “debt burden” detracted from it.

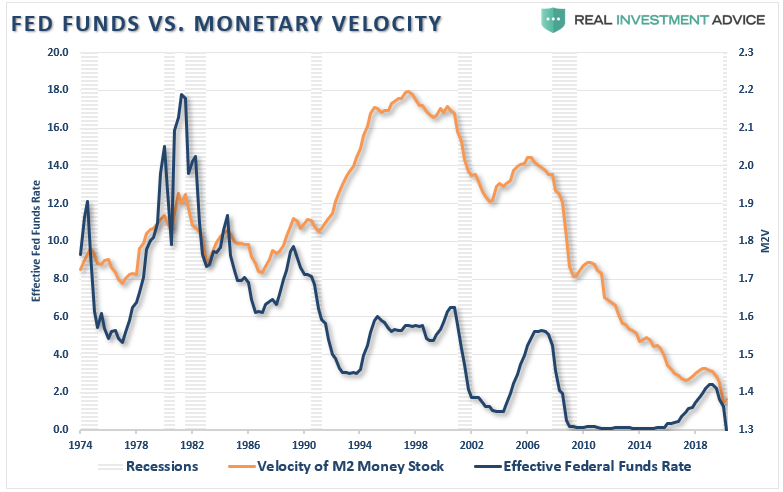

See Chart:

FED Funds vs Monetary Velocity

https://www.zerohedge.com/s3/files/inline-images/Fed-Funds-M2V-052020%20%281%29_0.png?itok=TkPRm0RC

{kind=link}

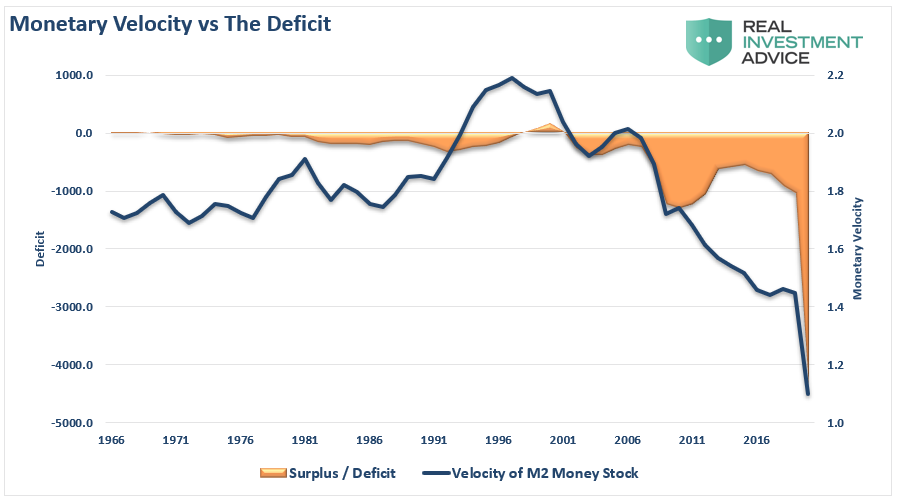

To illustrate the last point, we can compare monetary velocity to the deficit.

See Chart:

Monetary Velocity vs The Deficit

https://www.zerohedge.com/s3/files/inline-images/Defict-M2v-080520%20%282%29_0.png?itok=7TJq7Oox

{kind=link}

To no surprise, monetary velocity increases when the deficit reverses to a surplus. Such allows revenues to move into productive investments rather than debt service.

The problem for the Fed is the misunderstanding of the derivation of organic economic inflation.

The Fed’s Mistake

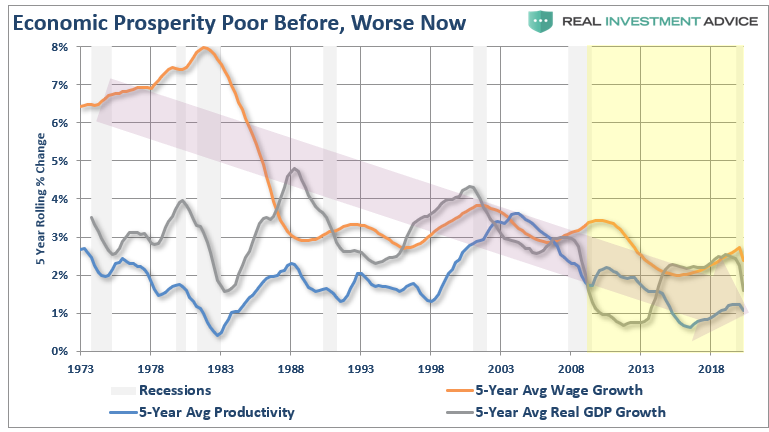

The Fed continues to follow the Keynesian logic, mistaking recessions as periods of falling aggregate demand. They believe lower rates and asset price inflation will stimulate demand and increase the rate of consumption.

However, these policies have all but failed to this point. From “cash for clunkers” to “Quantitative Easing,” economic prosperity worsened. Pulling forward future consumption, or inflating asset markets, exacerbated an artificial wealth effect. Such led to decreased savings rather than productive investments.

See Chart:

Economic Propensity Poor Before Worse Now

{kind=link}

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the result, is wrong. It has not happened in 30 years. Despite the short-term benefit of policies like tax cuts, or monetary injections, they do not create economic growth. Debt-driven policies merely reschedule future growth into the present. The average American may fall for a near-term increase in their take-home pay. However, any increased consumption in the present will be matched by a decrease later when the tax cut is revoked.

Of course, such assumes the balance sheet at home is not a complete disaster. As we saw during the “Great Depression,” most economists thought that the simple solution was just more stimulus. Work programs, lower interest rates, and government spending didn’t work to stem the depression era’s tide.

There Has Been A Cost

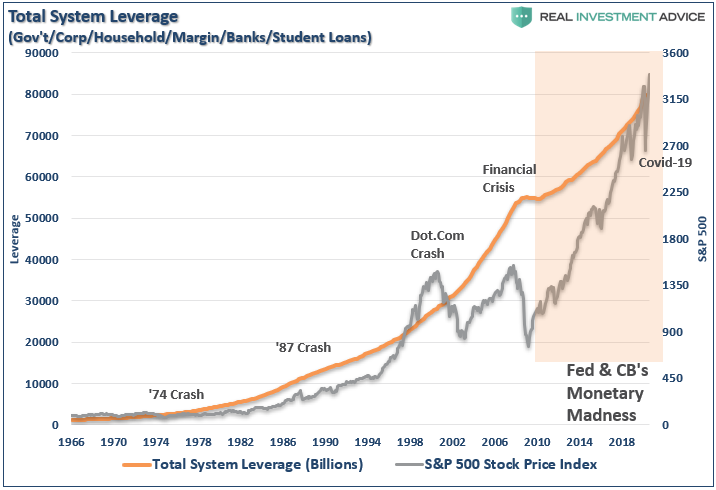

The Fed’s foray into “policy flexibility” did extend the business cycle longer than normal. Those extensions led to higher structural budget deficits, increased private and public debt, lower interest rates, negative real yields, and inflated financial asset valuations.

See Chart:

{kind=link}

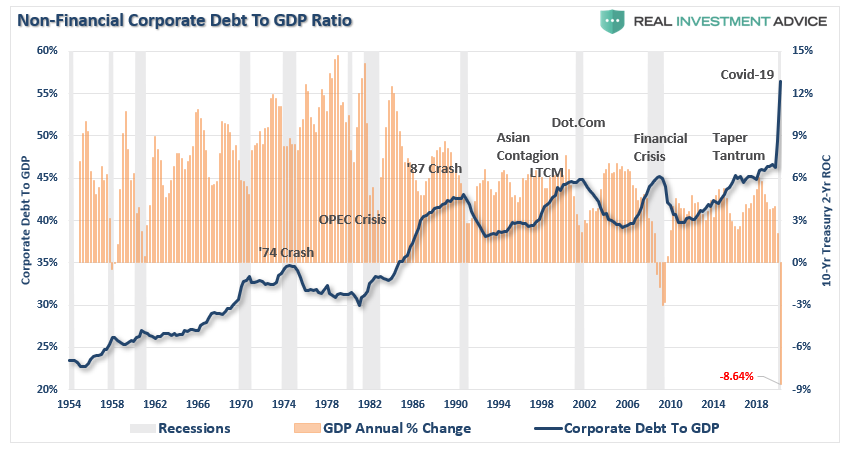

The Fed’s interventions have also led to a massive leveraging of U.S. corporations, which has led to lower defaults via cheap corporate debt.

See Charft:

Non Financial Corporate Debt to GDP Ratio

https://www.zerohedge.com/s3/files/inline-images/Corporate-Debt-GDP-Ratio-100820-1.png?itok=q5W3MgXU

{kind=link}

Unfortunately, it has also created an economy with a record level of “zombie companies.”

“‘Zombies’ are firms whose debt servicing costs are higher than their profits but are kept alive by relentless borrowing.

Such is a macroeconomic problem because zombie firms are less productive, and their existence lowers investment in and employment at more productive firms. In short, one side effect of central banks keeping rates low for a long time is that it keeps more unproductive firms alive, which ultimately lowers the long-run growth rate of the economy.” – Axios

See Chart:

Percentage of US ‘zombie’ Firms

https://www.zerohedge.com/s3/files/inline-images/Zombie-Companies.png?itok=spgZqNVZ

{kind=link}

Just as poor forest management leads to more wildfires, not allowing “creative destruction” to occur in the economy leads to a financial system that is more prone to crises.

As such, the “boom and bust” cycles will continue to occur more frequently at the cost of increasing debt, more money printing, and increasing financial market instability.

Welcome Recessions

The problem currently is that the Fed’s actions halted the “balance sheet” deleveraging process keeping consumers indebted and forcing more income to pay off the debt, which detracts from their ability to consume.

Such is the one facet that Keynesian economics does not take into account. Most importantly, it also impacts the equation’s production side since no act of saving ever detracts from demand.

Consumption delayed is merely a shift of consumptive ability to other individuals. Even better, money saved is often capital supplied to entrepreneurs and businesses that will use it to expand and hire new workers.

The continued misuse of capital and erroneous monetary policies are responsible for 30-years of an insidious slow-moving infection that destroyed the American legacy.

We should embrace “Recessions.” Allow recessions to clear the “excesses” accrued during the first half of the economic growth cycle.

Trying to delay the inevitable only makes the inevitable bemuch worse in the end.

….

SOURCE: https://www.zerohedge.com/markets/recessions-are-good-thing-let-them-happen

----

----

No hay comentarios:

Publicar un comentario