0CT 18 20 ND SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they documented with graphics

AN EMERGING MARKETS "DOOM LOOP" TIME BOMB EMERGES, AND INFLATION COULD SET IT OFF

by Tyler Durden

"If you’re looking for future potential crises this is another sovereign-bank nexus similar to that grappled with in the Euro sovereign crisis."

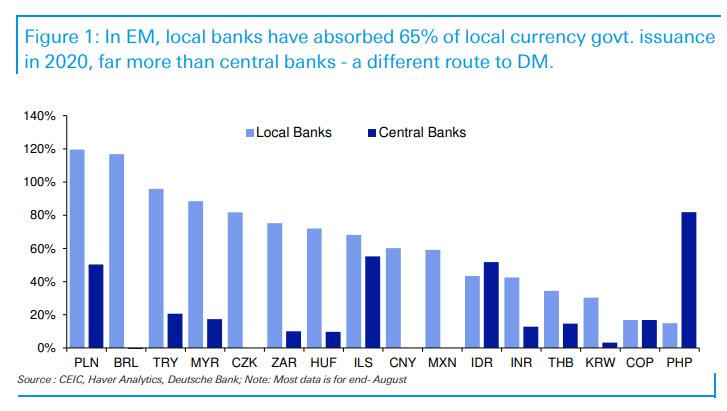

While both we have been focusing on soaring debt and QE since the covid pandemic, DB's Jim Reid correctly points out that this has been mostly in the context Developed Markets. But how have Emerging Markets funded themselves in the pandemic? The answer, as Reid writes in his Friday "Chart of the Day" note, is "via leveraging its banking system by a combination of moral suasion, liquidity provision from central banks, steep yield curves (encouraging carry trades), regulatory policies (reserve requirement cuts and easier accounting rules), and falling loan-to-deposit ratios (higher savings/weak demand) freeing up balance sheets."

This, according to some other analysts, is called "shadow" QE.

It's also a major problem: as the DB strategist explains, "if you’re looking for future potential crises this is another sovereign-bank nexus similar to that grappled with in the Euro sovereign crisis."

In other words, a Doom Loop for emerging markets.

See Chart:

Local Banks vs Centrasl Banks: In EM local Banks has absorbed 65% of local currency Govt issuance in 2020. Far more than Central Banks. A different route to DM

https://www.zerohedge.com/s3/files/inline-images/EM%20doom%20loop.jpg?itok=RNma8ouL

{kind=link}

Of course, an EM doom loop is just the start, as they are many more serious problems for emerging markets, with inflation the most likely one. As Reid explains, "a return [of inflation] could force central banks to sharply raise front-end rates, or to withdraw cheap liquidity. This would change the incentives for shadow QE which is inherently price sensitive, unlike the central bank QE mostly used in DM countries."

While CE3, Brazil & Mexico in Latam, and Malaysia in Asia stand out as countries where banks have played a particularly large role in absorbing issuance, a key condition of "shadow" QE has been muted inflation trends.

"If this changes, so could the calm in EM debt", Reid concludes adding that "increases in debt usually bring future crises so this is an interesting development to watch."

….

----

----

NOT THE ONION: FED CALLS FOR TOUGHER REGULATION TO "PREVENT ASSET BUBBLES"

After inflating the biggest bubble in history, the Fed suddenly realizes that it lacks sufficient tools to "stop firms and households" from taking on “excessive leverage” and has called for a “rethink” on “financial stability” issues in the US.

Boston Fed president Eric Rosengren, told the Financial Times that the Fed lacked sufficient tools to "stop firms and households" from taking on “excessive leverage” and called for a “rethink” on “financial stability” issues in the US.

“If you want to follow a monetary policy . . . that applies low interest rates for a long time, you want robust financial supervisory authority in order to be able to restrict the amount of excessive risk-taking occurring at the same time,” he said. “[Otherwise] you’re much more likely to get into a situation where the interest rates can be low for long but be counterproductive.”

Why thank you Eric, perhaps you should have chimed in oh... a few years ago when you and your Fed pals were injecting tens of billions of dollars daily into the market - not the economy as we explained earlier, and to do what - create the biggest asset bubble ever. The same bubble you are now warning about. So truly insightful.

See Chart

Aggregate Deposits vs. Aggregate Loans

{kind=link}

Hoover Institute, Quarles said that "the Treasury market being so much larger than it was even a few years ago, much larger than it was a decade ago and now really much larger than it was even a few years ago, that the sheer volume there may have outpaced the ability of the private market infrastructure to support stress of any sort there."

Translation: the Fed can never again step away and stop manipulating the bond market, which by extension and through the risk premium, is the market which defines every other market, including stocks, commodities, FX and so on.

The best comment, however, and by best we mean most idiotic, came from who else, but former PIMCO and Goldman banker, Neel Kashkari, who told the FT that stricter regulation was needed to stave off repeated market interventions by the central bank.

So for all those Fed officials "worried" about bubbles, here is DB's Aleksandar Kocic explaining just how to reduce the risk of bubbles bursting:

In a debt driven economy, the art of central banking is a technology of decelerating breakdown. By raising and lowering the primary interest rates, a central bank pursues the task of minimizing the endemic risks of a crash by adjusting to an acceptable level the stress incurred by the interest rate. Jumpstarting the economy becomes synonymous with decreasing the risk of insolvency for the units that are in debt.

And there you have it: IF YOU WANT TO REDUCE THE RISK OF ASSET BUBBLES, JUST END QE AND HIKE RATES. So which Fed staffer will be the first to float this particular idea?

Yeah, that's what we thought.

,,,,

SOURCE: https://www.zerohedge.com/markets/not-onion-fed-calls-tougher-regulation-prevent-asset-bubbles

----

----

Again the story-tell from Billonanaires that RECESION is good.. To whom is the QT

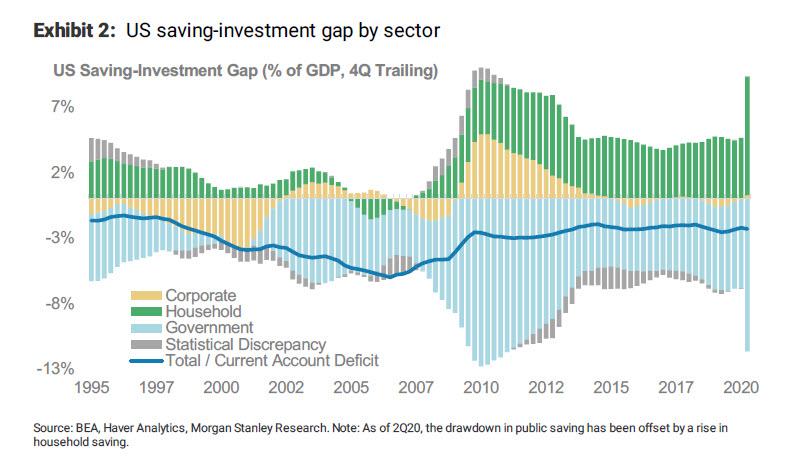

MORGAN STANLEY: THE SOARING US CURRENT ACCOUNT DEFICIT WILL ACT AS A GLOBAL REFLATIONARY IMPULSE

"This set-up of continued low real rates and a widening current account deficit in the US will act as a reflationary impulse for the rest of the world, especially EMs, setting the global economy on a path towards a synchronous recovery in 2021."

Mind the Gap [ como no se puede probar los que viene en el Fut: especulat=science ]

The extraordinary policy response to the exogenous COVID-19 shock is one of the key reasons why we expect a V-shaped recovery and a return of inflation in this cycle. BUT that is not all. This policy response will also bring about a remarkable shift in the trend in the US saving-investment gap (or the current account deficit), widening beyond the stable range of 2-3% of GDP that it has been in over the past nine years. The US policy response and its transmission to the rest of the world via the current account deficit plays an important role in global reflation and supports our call for a synchronous recovery in 2021. [ Tan fácil esta ‘ciencia’.. mas fácil que fabricar USD from thin air ]

With this V-shaped recovery, we expect a very different inflation outcome in this cycle too, which we peg as core PCE inflation moving through 2%Y on a sustained basis starting in 2022.

But we view things differently. We have consistently argued that the state of the private sector balance sheets were healthier coming into the recession. Private debt/GDP levels had remained stable for some time and US households had completed their deleveraging cycle. A FED that is committed to its average inflation goal will keep real rates lower for longer too in this cycle, which will provide greater incentives for the private sector to dis-save. We think that the trend of broad-based declines in saving has been set in motion, but how far it will go depends on how expansionary fiscal policy will be. [ Does this ‘expansionary F-P’ include bombing of CH & start WW3? ]

See Chart

US saving –investment gap by sector

https://www.zerohedge.com/s3/files/inline-images/savings%20gap%20by%20sector.jpg?itok=friPzgQW

{kind=link}

Additional fiscal stimulus post the elections, which our US public policy analyst highlighted in last week’s Sunday Start, is a possibility in three of the four post-election party configurations. COVID-19 has exacerbated the pre-existing income inequality trends in the US. Policy-makers will continue to focus their efforts on helping low-income households, suggesting that they will err on the side of running expansionary fiscal policy for longer.

If more fiscal stimulus arrives, it will impart upside risks to the growth and inflation outlook and consequently lead to a further and more rapid widening in the current account deficit, particularly if the fiscal policy mix remains tilted towards transfers to households.

[ Mas claro no cantan los gallinazos neo-nazis que lucran con la economía USA ]

See Chart:

US current account balance

https://www.zerohedge.com/s3/files/inline-images/US%20current%20account%20balance.jpg?itok=-cZFJlkB

{kind=link}

The widening current account deficit will be another factor in driving USD weaker, as our global macro strategy team forecasts. We believe that this set-up of continued low real rates and a widening current account deficit in the US will act as a reflationary impulse for the rest of the world, especially EMs, setting the global economy on a path towards a synchronous recovery in 2021.

….

----

----

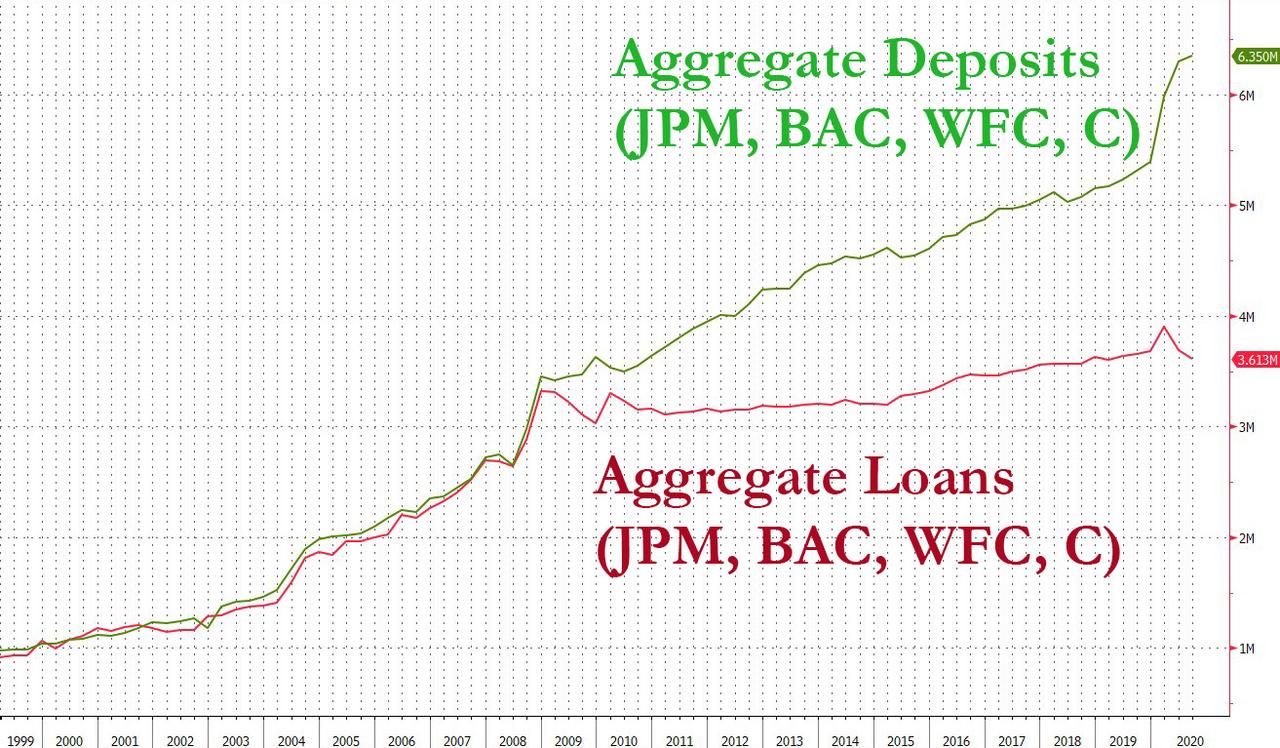

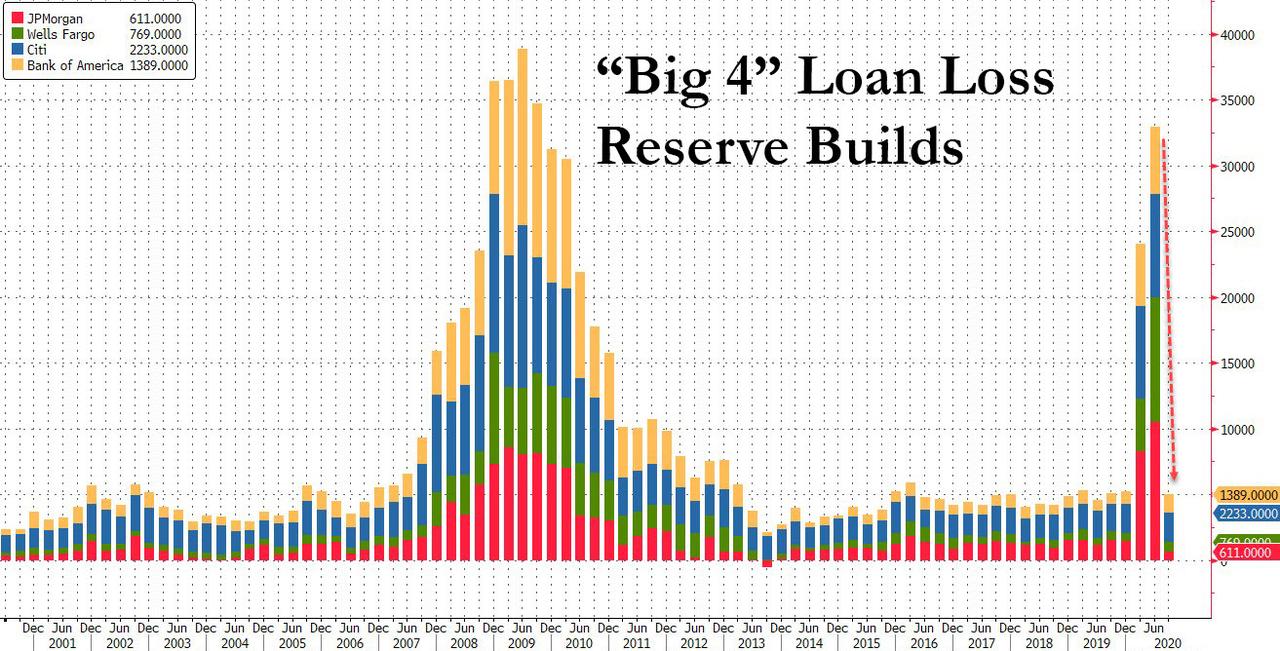

THE ONE-CHART SUMMARY OF ALL THAT IS WRONG WITH THE US FINANCIAL SYSTEM: DEPOSITS OVER LOANS

by Tyler Durden

So much for "loans create deposits."

Now that the big banks have concluded their earnings season, with the top highlight being the collapse in loan loss reserve builds from $33 billion in Q2 to just $5 billion in the quarter ended Sept 30...

See Chart:

Big 4: Loan Loss Reserve Builds

https://www.zerohedge.com/s3/files/inline-images/big%204%20reserves.jpg?itok=M_2R_za-

{kind=link}

.. in what some have taken as a vote of confidence for the economy as bank risk managers clearly don't anticipate another sharp leg lower in the economy (that may change if a second wave of covid forces new shutdowns), we can take a closer look at some of the other, just as notable observations within the US financial sector.

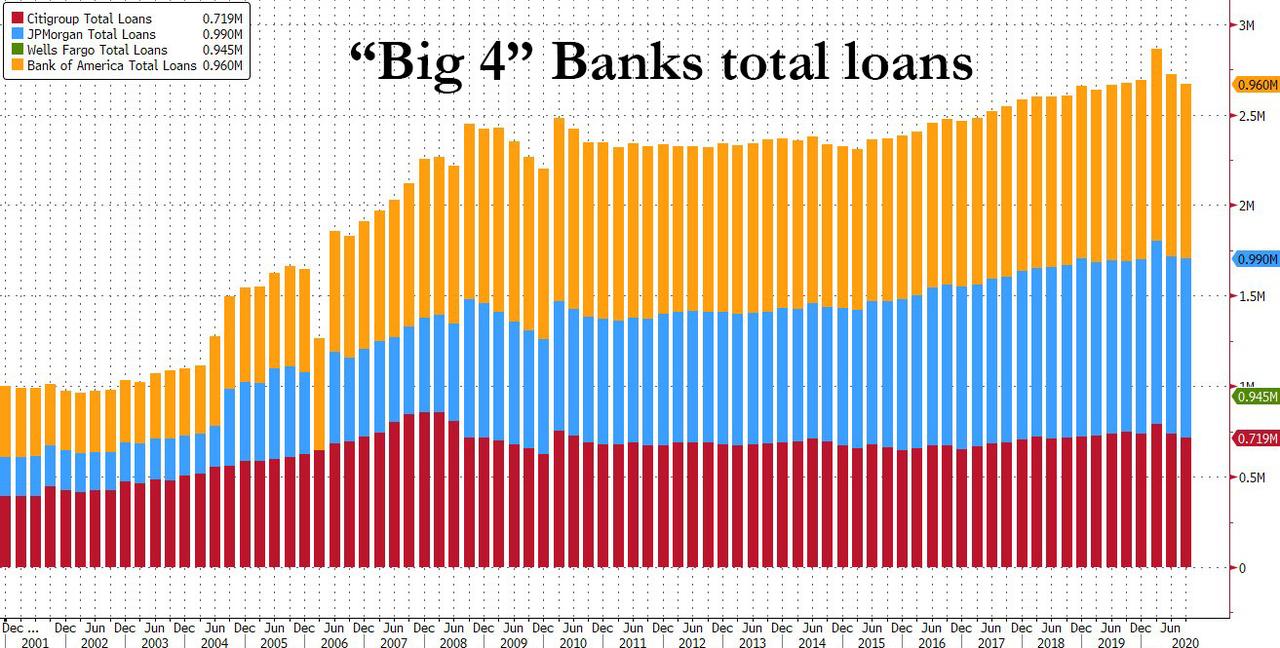

First, we looked at the amount of total loans across the 4 megabanks, where for the second consecutive quarter aggregate loans declined after the Q1 surge (which as a reminder was driven almost entirely by revolver drawdowns, which have since been refinanced by bonds and other debt instruments).

See Chart:

‘BIG 4’ Banks total loans

https://www.zerohedge.com/s3/files/inline-images/big%204%20banks%20total%20loans.jpg?itok=80702l1S

{kind=link}

Those who have followed our reporting on the surge in bank lending standards, which recently spiked to levels not seen since the financial crisis, will not be surprised by the ongoing freeze in loan issuance: after all, banks remain terrified about lending across most verticals, including C&I, consumer (credit card and auto loans) and residential and commercial real estate.

See Chart:

https://www.zerohedge.com/s3/files/inline-images/tighter%20loan%20standards%203_3.jpg?itok=e-En9LFy

{kind=link}

Yet while the continued flatlining in US bank loans - which haven't budged in the past two years and have barely increased since the financial crisis - is explainable, it is nonetheless quite troubling: after all, if there is neither supply nor demand for loans, the economy simply won't grow, period. It's also why the velocity of money will be catastrophic and is approaching that monetary "singularity" of 1 for the first time ever

See Chart:

Velocity of Money (M2)

https://www.zerohedge.com/s3/files/inline-images/velocity%20of%20M2.jpg?itok=PuiaKj_7

{kind=link}

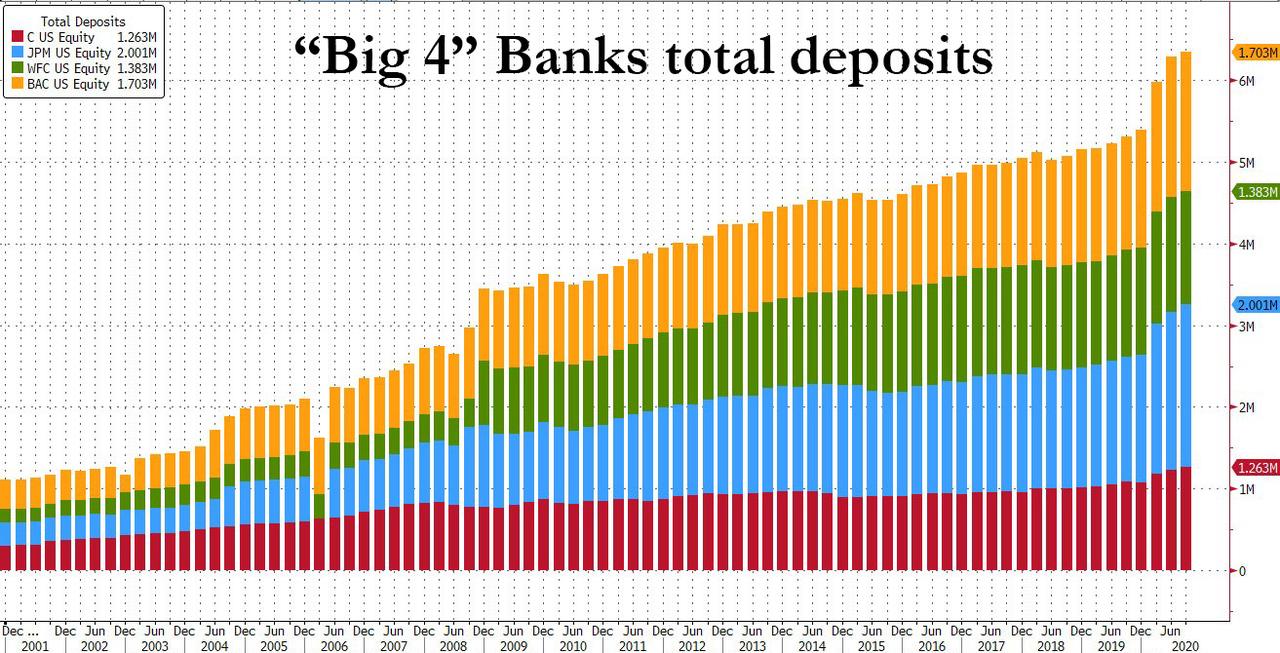

However, while it is hardly surprising that loan growth has refused to pick up during the worst economic depression since the "Great" one, what is certainly remarkable is when one looks at the corresponding bank liability: deposits. Here, there is no such problem, and in fact, in recent quarter (and years), deposits have exploded higher and continued to do so last quarter too.

See Chart:

‘BIG 4’ Banks Total Deposits

{kind=link}

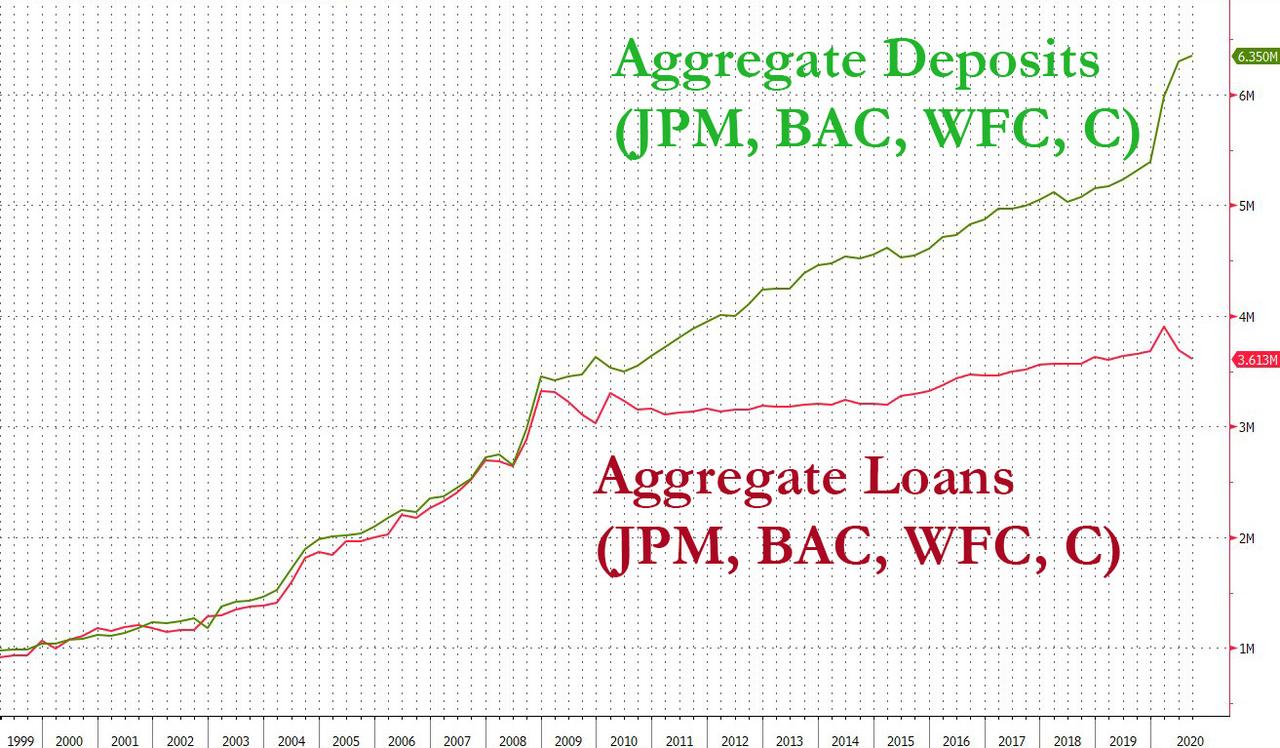

Why is this notable? Well, for one, it crushes the socialism-enabling "theory" known as MMT, or Modern Money Theory, also known as Helicopter Money. Recall that according to the hodgepodge of confused concerts that were thrown at the wall in hopes of coming up with some comprehensive monetary theory, from the perspective of Modern Monetary Theory private bank lending is unconstrained by the quantity of reserves the bank holds at any point in time. In other words, according to MMT loans create deposits ((see here,here, and here)). Only... clearly in reality that's not the case.

Which then brings us to what may be the best one-chart summary of all that is wrong with the US financial system. It is a very simple chart - it shows consolidated deposits and loans within the US financial system (which consists of both US and foreign banks).

See Chart:

Agregate deposits (JPM,BAC, WFC, C) vs Agregate Loans (same banks)

https://www.zerohedge.com/s3/files/inline-images/aggregate%20loans%20vs%20deposits.jpg?itok=UNqZh__G

{kind=link}

CONCLUSION

Risk assets continue to be bid up to record highs on the back of QE, even as the actual flow through of the Fed's "wealth effect" to the economy is halted precisely due to the complete collapse in new loan creation - the primary "transmission mechanism" of economic growth.

In other words, by keeping the pedal to the metal on QE, the Fed is giving the banks all the benefits of money creation (soaring deposits), without any of the risks (loan creation in a record low Net Interest Margin environment).

And that is precisely the crux of all that is broken in the US financial system, and why the Fed's QE is making things worse, not better, and is progressively destroying the wealth of the middle class, stunting any growth opportunities the US may have, and all the residual wealth is pumped into the hands of those benefiting solely from rising asset prices.

OPEN THE SOURCE BELOW TO SEE MISING COMMENTS & CHARTS

….

----

----

AMERICA'S STIMULUS & DEBT-DEFERRAL ECONOMY EXPOSES THE SURREALITY BEHIND THE RISE IN RETAIL SALES

...money not spent...

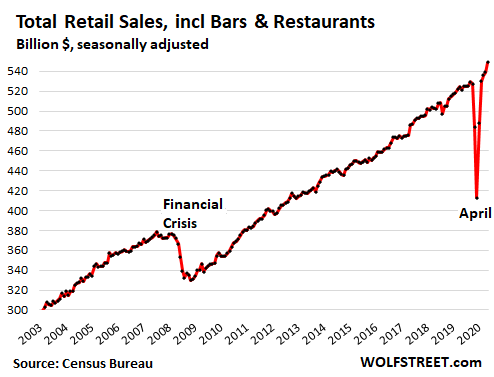

Total retail sales – sales of goods in stores and online, but not including services such as doctor’s visits, insurance, airline tickets, hotel bookings, rent, etc. – in September jumped by 1.9% from August, to a record of $549 billion (seasonally adjusted), according to the Census Bureau. Compared to September 2019, retail sales were up 5.4%.

But as we’ll see in a moment, there were huge differences between categories, from sales at clothing stores and restaurants which, though they bounced a lot, were still below where they’d been years ago; to sales at stores for building materials and garden supplies, which jumped from record to record during the crisis:

See Chart:

Total Retail sales, incl Bars & Restaurants

{kind=link}

The stimulus money & things consumers no longer pay for.

There were a lot of things consumers didn’t do, such as flying – passenger traffic in the US was down 65% from a year ago – staying at hotels, going to the movies, and the like. And the money not-spent on these services got spent on other stuff. About 7% of households with a home mortgage got their mortgage moved into forbearance, and they no longer have to make mortgage payments for the forbearance period, and that money of those not-made mortgage payments got spent elsewhere.

Then there were the stimulus payments, starting in April, some of which are still going out to people the IRS had trouble locating. And the extra $600 a week in unemployment benefits, and the federal program for gig workers (PUA) that states had trouble processing, were sent out often way behind and in lump-sums.

The extra $600 a week was replaced in August by the extra $300 a week, which states started sending out in late August and September, also in lump-sums.

Then there were all the folks that fraudulently obtained unemployment coverage, under one or several programs, and that money too got spent.

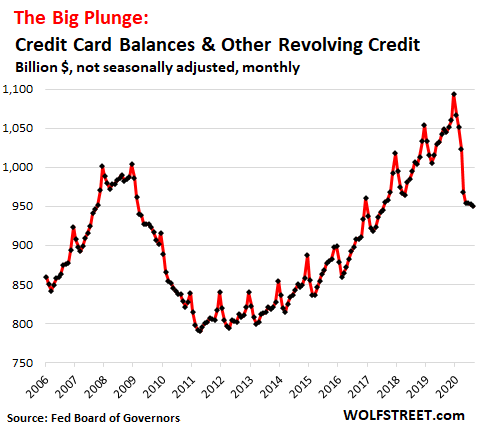

But not all these funds got spent. The pay down of credit cards essentially came to a halt in June, July, and August with the slowdown of the stimulus and extra unemployment money:

See Chart:

The BIG PLUNGE: credit card balances and other revolving Credit

{kind=link}

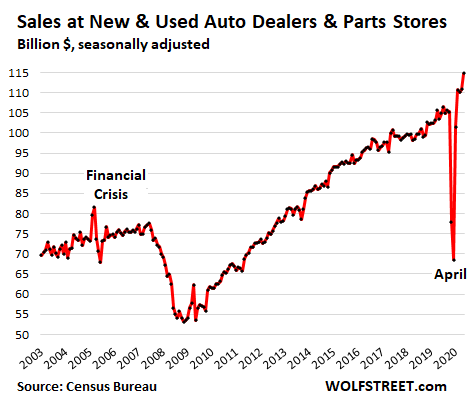

Sales at auto dealers and parts stores form the largest retail category, accounting for 21% of total retail sales:

See Chart:

Sales at New & Used auto dealer & parts stores

{kind=link}

Continue reading & see more charts at

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge cambio

Hallowing the whole year?

Authored by Roger Koops via The American Institute for Economic Research

"I understand the psychological crutch that people feel with something covering their mouth/nose. I am sorry, but that is a false sense of security..."

2020 is a year of disguises. Some examples include computer models/modelers disguised as “science/scientists,” Tyrants/Dictators/Totalitarians disguised as “elected officials,” propaganda machines disguised as “news sources,” brainwashing disguised as “information,” censorship disguised as “public health safeguard,” panic and fear disguised as “social responsibility.”

Even the virus itself has been disguised by humans as an “apocalypse.” And if you look at the totality of events in 2020, it is clear that the average citizen has been treated generally less than human, certainly not as adults in any case.

I believe we are in as great a crisis as a species as we have ever been. The crisis is not from some seasonal virus (which is a health issue), but it is from ourselves and what we have devolved into as a species (social, cultural, ideological issues).

HUMAN PERCEPTION

The natural perceptive abilities, i.e. the physical senses, of human beings are quite poor. For example, we can see only a very, very small part of the electromagnetic spectrum, illustrated as follows:

See Chart:

The Electromagnetic Spectrum

https://www.zerohedge.com/s3/files/inline-images/electromagneticspectrum-768x421.png?itok=pv4FN2Lq

{kind=link}

Consequently, humans have difficulty understanding that which is not directly observable by their senses. Size and mass we do okay at, providing we can see it. We tend to have better abilities with larger things that we can observe. But, even size perception has its limits. For example, many people cannot grasp the scope of our universe.

We have bacteria and fungi in our bodies constantly. Our immune system usually keeps them at bay, or more accurately, keeps them in balance. However, if our immune system weakens, or if a balance is shifted towards the bacteria/fungi, the balance can tip in their favor and we can experience disease. We tend to have more difficulty with control of bacterial/fungal infections than viral infections. In fact, the most common cause of a fatal outcome due to viral infection, including coronavirus, is a bacterial infection.

THE VIRUS IN DISEASE TRANSMISSION

The “rationale” for lockdowns, masks, distancing, etc. all rest on the assumption that human direct transmission is the greatest risk for disease.

But, is this really the case? In short, “No” and here is why.

CONTINUE READING AT:

SOURCE: https://www.zerohedge.com/medical/year-disguises

----

----

Biden is a 'national security crisis...'

====

'YOU HAVE UNTIL TUESDAY': PELOSI ISSUES ULTIMATUM OVER RELIEF FUNDS

Or what?

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

More ultra-xenophobia:

"The foundation for investing so much money in China is unstable... One must invest very carefully in China and be skeptical of all the numbers that are presented."

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars & danger of WW3

-Joe Biden 'Bad' for India as he Could be Soft on China, Predicts Donald Trump Jr

- France to Expel 231 Radicalised Foreigners After Beheading of Teacher in ‘Islamist Terrorist Attack'

- Iran Plans to Sell More Arms Than Import as Embargo Lifted

- Trump Slams Final Debate Moderator Kristen Welker as 'Extremely Unfair'

- Sudan Might Be Lured By Israel's Tech and US Cash But Peace Still Not an Option

- MAS Candidate Arce Winning in First Round of Bolivia’s Presidential Vote

- Azerbaijani Forces Take Control of Several Settlements in Nagorno-Karabakh

- Navalny Says Trump Should Condemn His Alleged Poisoning

- Trump Will Be Back in 2024 If He Loses November Vote

- China’s GDP Grew Nearly 5 Percent in Third Quarter of 2020, Stat-Bureau Rep

====

====

No hay comentarios:

Publicar un comentario