RISK of COLLAPSE: DONDE ESTAMOS y

ADONDE VAMOS

By JP

Morgam

IF big

Corp & Bamkers said it, it means that is time to pay attention to middle clases

to deflect a chaotic transition or REV in the post-neoliberal agenda. Hugo

Adan

"We have consistently argued

that one should not expect the next US recession ahead of the presidential

elections, but the odds of one might go up significantly post the event, in our

view. "

JPMorgan repeats that it has

"consistently" argued that one should not expect the next US

recession ahead of the presidential elections, it then spoils the ending, and

in previewing what happens after next November, says that "the odds of a

recession might go up significantly."

We will spare readers the

cheerful side of JPM's year ahead forecast as it is a repeat of many themes

covered here previously by the "bullish" JPM and instead focus on the

gloomier aspects of the bank's year ahead predictions, as those are decidedly

new and represent a reversal to JPM's years of relentless optimism.

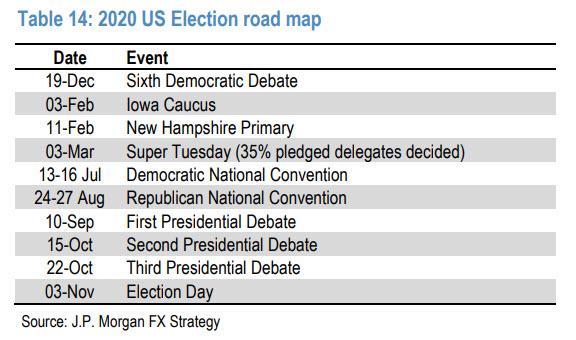

The first notable item is the US election road map

See Chart:

2020 US

Election road map

{kind=link}

This will be add to my report

on: “Middle Classes &

Rev in America”

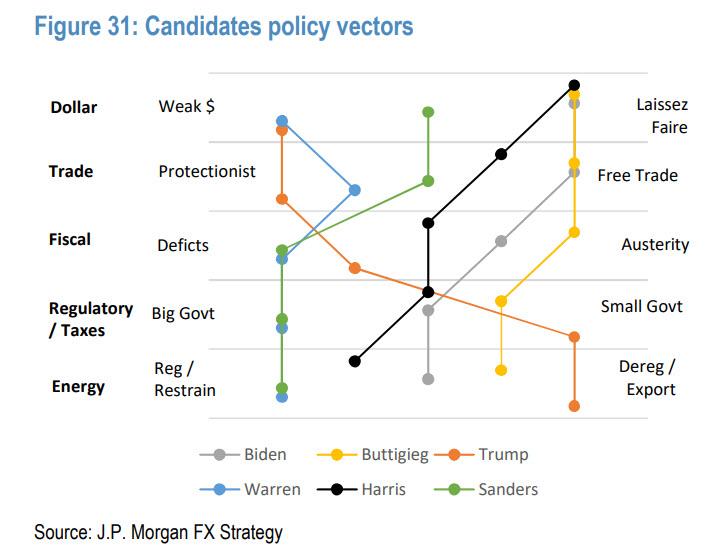

As JPM notes, "we might end up with two candidates who are potentially on

the extreme ends of the political spectrum. The exhibit above compares the

policies of a select number of Democratic candidates and president Trump, based

on our interpretation of published policies and public comments. The divergence

of policy proposals between the different Democratic candidates is

probably as extreme as the comparison between Trump’s policies and that of any

of his Democratic adversaries."

See Chart:

Candidates

Policy Vectors

{kind=link}

The risk of trade uncertainty escalating again, post

the current truce

JPM's base case over the past

months was that Trump will be compelled to move towards a truce with China,

given what were the rising risks to the economy, and in particular to the US

consumer. The risk is that the current improving

sentiment with respect to trade doesn’t hold for too long, and that potentially

re-elected Trump resumes his aggressive stance.

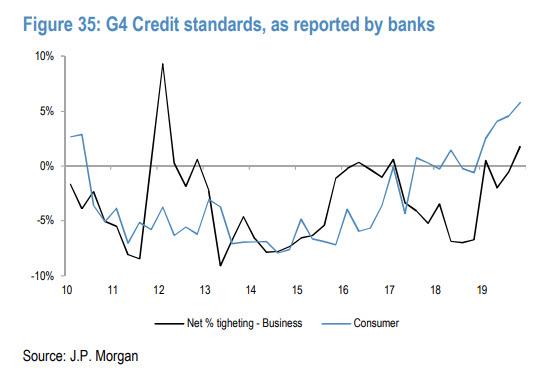

An inflecting credit cycle

See Chart:

G4

credit standards , as reported by Banks

{kind=link}

Notably, G4 credit standards

appear to be tightening for both the businesses and for the consumer of late.

One typically sees tightening standards ahead of the downturns.

Corporate leverage is surging

US

corporates have been levering up over the past years, with median US company

net debt-to-equity ratio at the record highs.

See Chart:

Median Net debt to –equity for

US

{kind=link}

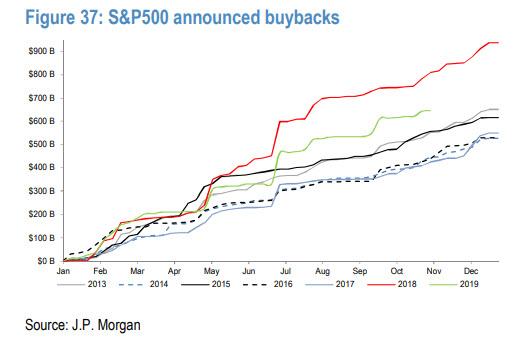

Why is this a risk? Because "if the

credit markets weaken, this could reduce the pace of corporate buybacks."

Because where would we be without buybacks...

See Chart:

S&

P 500 announced buybacks

{kind=link}

Economic indicators are looking decidedly late-cycle

The US

cycle is now officially the longest one since the WW2, and some of the cycle

indicators appear to be rolling over. One such indicator is that job opening

rate appears to have peaked. This is what usually happens ahead of the

downturns.

See Chart:

US job vacancies

rate

{kind=link}

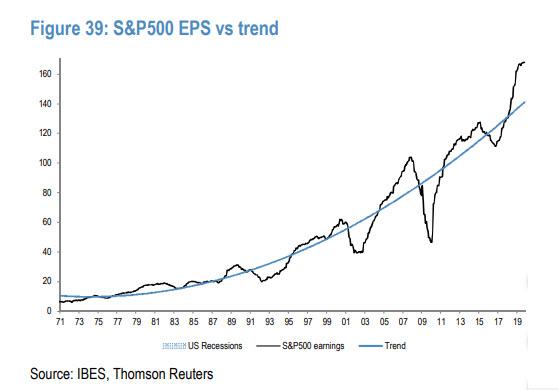

Earnings have significantly overshot the trendline

Another

key JPMorgan concern is that US profits are now starting to appear stretched vs

their long term trend-line.

See Chart:

S&P

500 vs trend

{kind=link}

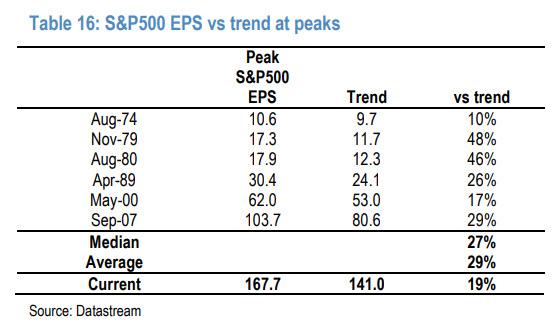

Here Matejka notes that one of the arguments that kept him bullish all this time was

the finding that US profits don’t tend to peak for the cycle before they

significantly overshoot their long term trend. The size of these overshoots was

on average of the order of 20-30%. The current overshoot is at 19%

See Chart:

S&P

500 EPS vs trend at peaks

{kind=link}

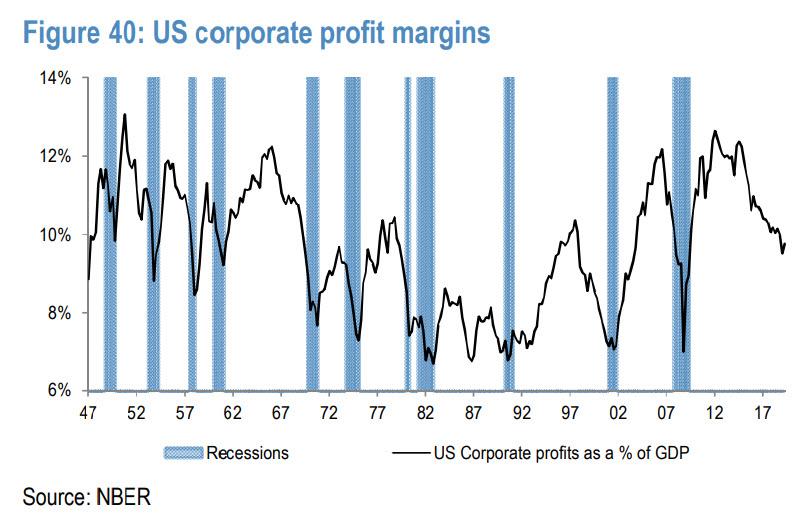

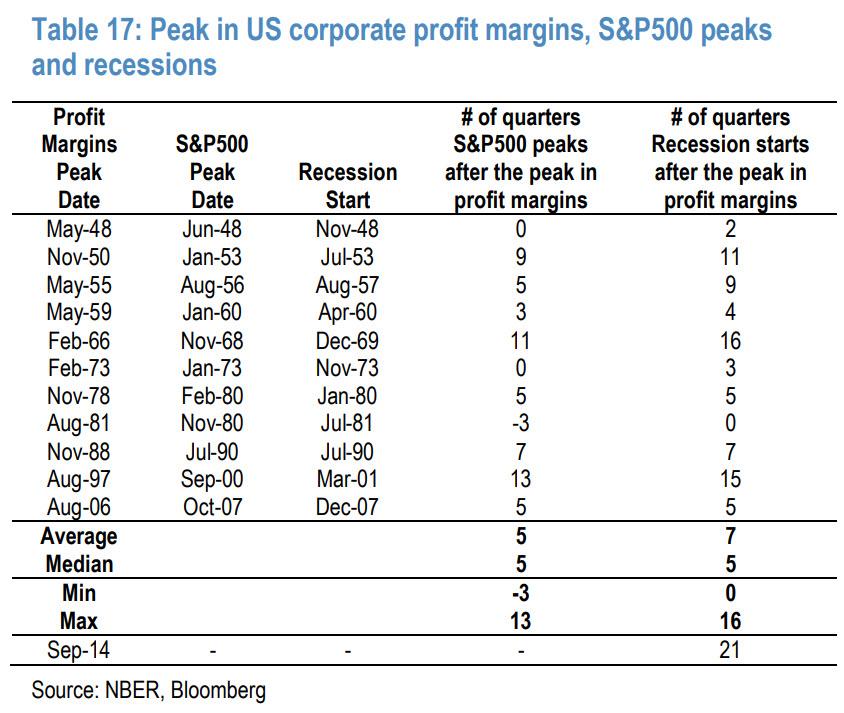

Profit margins have peaked, which typically bodes

negatively for the longevity of the expansion cycle

As we noted recently when

discussing real, operating profits, one doesn't usually have a recession before

US profit margins, as measured by NIPA, peaked. The

lead-lag between margins peak and the next recession was sometimes very

significant.

See Charft:

US

Corporate Profit margins

{kind=link}

However,

as of this moment, JPM finds that "we are now in unchartered

territory", with US

profit margins appearing to have peaked in Q3 ’14, leading to the longest

lead-lag on record, and counting...

See Chart:

{kind=link}

Putting

it together, JPM concedes that while "the

time is likely approaching when one should be contrarian again", this time

around through turning bearish vs presently growing consensus bullishness, the

bank still thinks that "one should not cut risk-on trades too

early, as the bear capitulation, which is currently

under way, could have legs." The only question is when does someone, or something, pull the rug from under the

market's melt-up, triggering what even JPMorgan now see as a coming, and long

overdue, day of reckoning for the markets

….

----

----

No hay comentarios:

Publicar un comentario