ND DEC 21 19

SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

“Predictions Are Difficult...

Especially When They Are About The Future”

….

Ni modo de predecir el pasado. Quiza se quiso

decir “The Future

of neoliberal economics & politics”

When it comes to trying to

predict what will happen in the financial markets over the next year, which is

an annual event, it is essentially an act of futility. Given the markets are

affected by a broad spectrum of inputs from economics, to geopolitics, monetary

policy, rates, and financial events, any prediction should be taken with a very

high degree of skepticism.

So, with that said, here is how we are preparing for 2020.

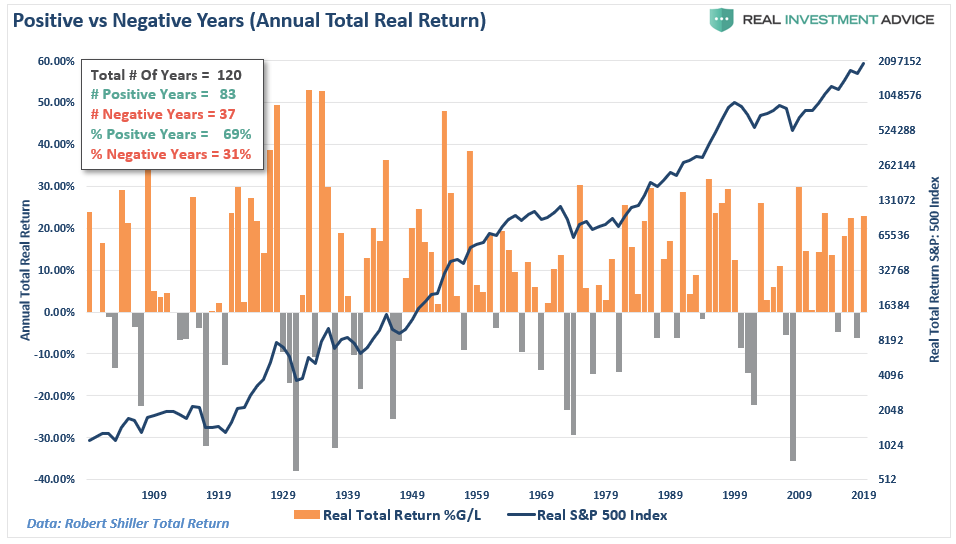

Odds Have It

In our portfolio management

practice, we begin with the basic assumption there is a 69% chance the market

will finish the coming year at a level greater than where it started. That 69%

probability comes from the fact that over the last

120-years, the market has (on a total real return basis) finished the year in positive territory 83 times, and

negative only 37 times.

See Chart:

Positive vs Negative Years ( Annual Total Real Return)

{kind=link}

The reality is that we can’t

control outcomes. The

most we can do is influence the probability of certain outcomes through the

management of risks, and investing based on probabilities, rather than

possibilities, which is important to capital preservation and investment

success over time.

So, as we head into 2020, here

is a short-list of the things we are either currently hedging portfolios

against, or will potentially need to:

- China fails to comply with the terms of the “Phase One” trade deal which reignites the trade war.

- Earnings growth fails to recover, and valuations finally become a concern for the markets.

- Corporate profits, which have been essentially flat since 2014, deteriorate due to slower economic growth both domestically and globally.

- Excessively high consumer confidence converges with low levels of CEO Confidence as employment begins to weaken.

- Interest rates rise which trips up heavily leveraged consumers and corporations.

- Investors become concerned about excess valuations.

- A credit-related event causes a market liquidity crunch. (Convent-Lite, Leveraged Loans, BBB-rated downgrades all pose a potential threat)

- The Fed’s “repo-crisis” continues to grow and turns out to be something much more significant.

- Similar to 2016, a shocking election result.

While I am not going to address

all of these concerns, I do want to touch a few that we feel are significant

risks heading into the first half of the decade.

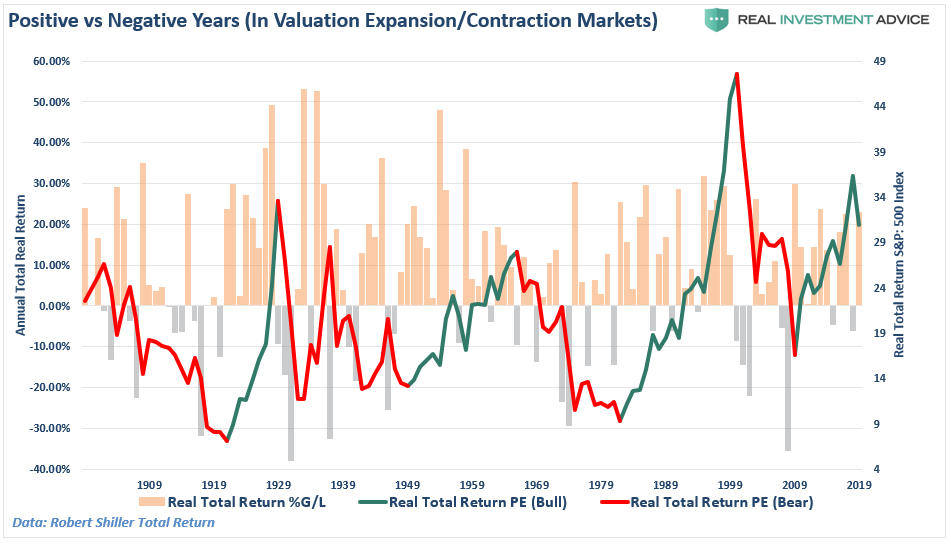

Valuations

While valuations are a terrible

market timing device, they do impact long-term returns and investment outcomes.

Currently, at 30x earnings, valuations are elevated, which suggests that the

next decade of returns will be significantly lower than the last.

Statistically, returns in the very low single digits should be expected.

Importantly, it is worth noting

that negative returns tend to cluster during periods of declining valuations. These “clusters” of

negative returns are what define “secular

bear markets.”

See Chart:

Positive vs

Negative Years ( In Valuation-Expansion/ contraction markets )

{kind=link}

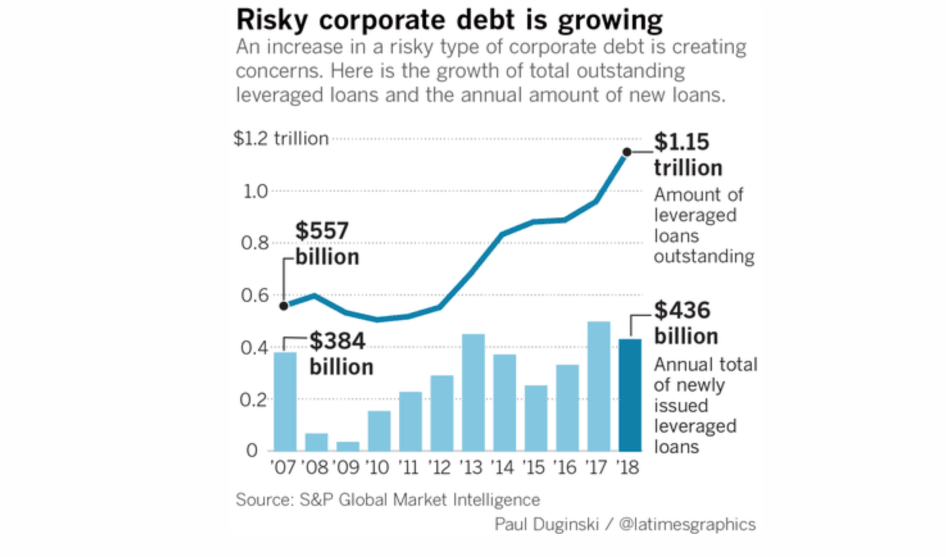

The Debt Risk

One of the common

misconceptions in the market currently, is that the “subprime mortgage” issue

was vastly larger than what we are talking about currently.

Not by a long shot.

Combined, there is about $1.15

trillion in outstanding U.S. leveraged loans — a record that is double the level five years ago — and, as

noted, these loans increasingly are being made with

less protection for lenders and investors.

See Chart:

Risky Corporate Debt is growing

{kind=link}

Just to put this into some

context, the amount of sub-prime mortgages peaked slightly

above $600 billion or about 50%

less than the current leveraged loan market.

Of course, that didn’t end so

well.

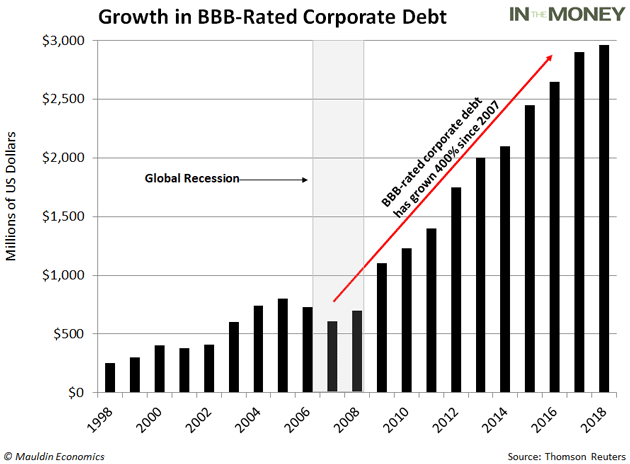

Currently, the same explosion in low-quality debt is

happening in another corner of the US debt market as well.

See Chart:

Growth

in BBB-Rated Corporate debt

{kind=link}

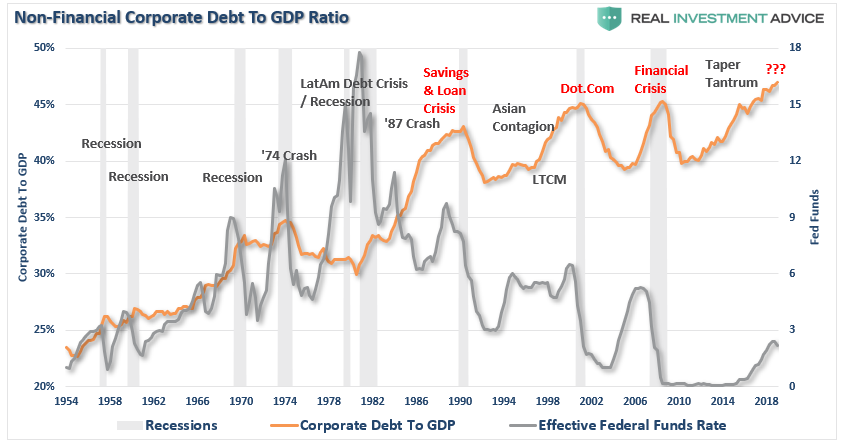

As noted by John

Mauldin:

“In just the last 10

years, the triple-B bond market has exploded from $686 billion to $2.5

trillion—an all-time high. To put that in perspective, 50% of the investment-grade bond

market now sits on the lowest rung of the quality ladder.

And there’s a reason

BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies

to pile into the bond market and corporate debt has

surged to heights not seen since the global financial crisis.”

See Chart:

Non-Financial

Corporate debt to GDP Ratio

{kind=link}

CONTINUE

SEEING more charts & comments

CONCLUSION

Statistically speaking, the

odds suggest that the market could

indeed be higher in 2020. However, there are numerous risks which

could derail the markets which should not be dismissed.

This is not a “bearish

forecast.” It is just an assessment of trends, statistics, and

probabilities given the current monetary, financial and economic backdrop.

If we are wrong, and

stocks do post gains in the coming year, being more conservative will only mean

a small relative under-performance in your portfolio next year.

If we are right, the preservation of capital will be far more beneficial. As

we have stated previously, participating in the bull market over the last

decade is only one-half of the job. The other half is keeping those gains during the second half of the full

market cycle.

As we enter into 2020 it may

pay to be a little more cautious after such a large rise in the financial

markets.

Let me leave you with Bob Farrell’s 10 Rules:

- Markets tend to return to the mean over time

- Excesses in one direction will lead to an opposite excess in the other direction

- There are no new eras — excesses are never permanent

- Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways

- The public buys the most at the top and the least at the bottom

- Fear and greed are stronger than long-term resolve

- Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names

- Bear markets have three stages — sharp down, reflexive rebound and a drawn-out fundamental downtrend

- When all the experts and forecasts agree — something else is going to happen

- Bull markets are more fun than bear markets

Our job is managing risk to

conserve principle and create absolute returns over time. What matters most to

us is that we provide a disciplined management process suitable for our clients

who seek long-term performance as measured by annualized and risk-adjusted

returns, and conservation of investment principle.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

We are, all of us, living in a fiction. A fiction authored by those in power to serve

the interests of those in power...

====

“America is a corpse being consumed by

maggots. Liberals are rooting for the maggots. Conservatives are

rooting for the corpse...”

====

"The base, deep in the

California desert near Death Valley National Park, is where the Navy develops and tests its newest weapons."

====

We are asleep, naive, and unaware of the creep of Big Tech...

====

The most

important 5G applications will not

be intended for civil use, but for the military domain...

====

“The base case is that Trump will

win...because the Democrats are a

mess.”

....

Here we have more than 2 undergraduate naïve

fallacies:

1-type of “ad hominems”: to attack not the arguments or reasons in

other persons but their personal characteristics. In Politics this is

known as “mudslinging”

(tirarle barro o basura al opositor, lo que refleja ignorancia y deshonestidad).

2-Straw

Man fallacy. Se ataca en otra oponente una posición o defecto que no tiene o si la

tiene se la exagera, a pesar de que el acusador practica el mismo defecto (se

mira la paja en el ojo ajeno y no el basural que lleva en el propio cuerpo) .

Si uno practica lo que se acusa en el otro, eso además deshonesto es

hipocresía. This also contain

other falacies like Slippery Slope: from unrelated issue or weak premise is

derived a strong wrong & derogatory

conclusion without evidence and

3-Circular Argument where

a derogatory conclusion appears as

premise in the argument of the accuser. If both Dems

& Reps are in Political mess (no one can deny this reality) it is ridiculous to take one as premise & the other as

conclusion. Besides: there is not causation-effect-relation between

bond’ Investors and Politics. SO, It is just stupid to

conclude that “Trump will win, because Dems are a mess”. In fact, what we have here is wrong

premise (mere wishful thinking) as the base for idiotic conclusion.

----

----

"He needs to be

humiliated..."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

“(This clause) troubles some of

our political analysts and public figures...”

====

What could possibly go wrong?

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

--

Jailbreaks, Secret Tunnels, Hunts for

Missiles: Top-4 Soviet Counterintelligence Operations Revealed

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

----

----

PRESS

TV

Middle East n world news

- Cuba names first prime minister in over 40 years

- Netanyahu rejoices as UAE FM floats Israel-Arab alliance

- Serie A: Inter Milan 4-0 Genoa

- Australia's PM apologizes for being on vacation while wildfires raged

- Trump invites Britain's Johnson to White House in new year

- Iranians celebrate Yalda Night in Vienna

- 18 prisoners killed in clashes at Honduras jail

- Macron urges suspension of strikes during Christmas

- No Xmas vacation for France’s Yellow Vests

- West retaliates after Russia, China veto UN resolution on Syria

- EU, Russia, Germany blast US sanctions on gas pipeline

- Hamas praises ICC plan to probe into Israeli war crimes

- PROGRAMS

- US prison industry

- US, Iran tensions

- Iran nuclear deal

----

===

No hay comentarios:

Publicar un comentario