ND DEC 15 19

SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

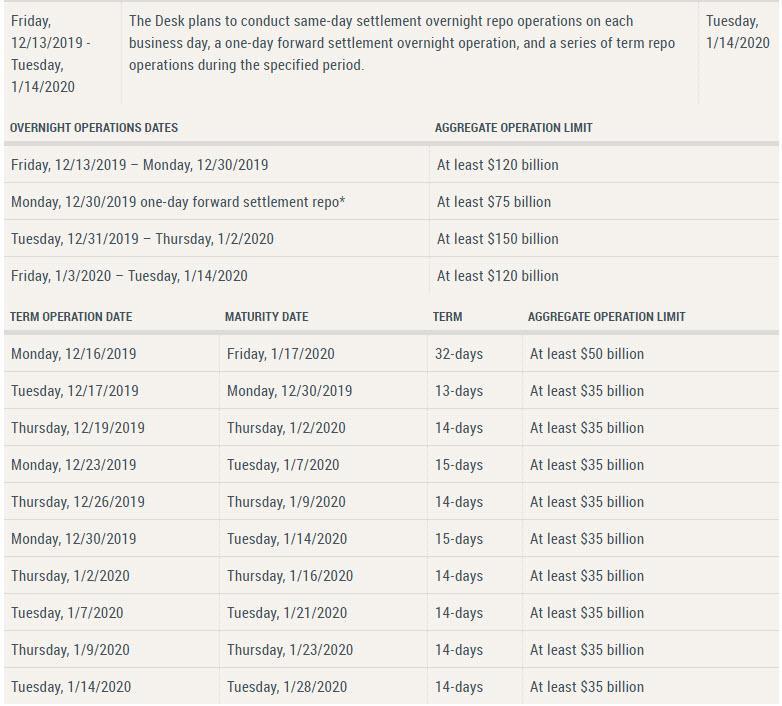

When looking at tomorrow's $100

billion liquidity drain, the repo market should be able to digest it without a

surge in the G/C repo rate. If, however, the first repo prints on monday come

in at 2% or higher, it will mean that Pozsar's year-end doomsday forecast may

well come true.

Last week's apocalyptic

report by repo market guru Zoltan Pozsar, which for those who missed

it predicted that an imminent market crash and loss of control of overnight

rates by the Fed would spark nothing short of QE4, sparked an unprecedented

panic at the Federal Reserve, which just two days

later unveiled a historic liquidity injection,

in which the Fed promised to inject no less than $500

billion in the next 4 weeks to avert a catastrophic freeze in the repo market

as we approach the year end "turn", which would consist not only of a

continuation of the Fed's T-Bill POMO, but also a massive injection of nearly

$500 billion in overnight and term repos in the coming days.

See Table:

{kind=link}

In other words, instead of a reactive QE4 - as predicted

by Pozsar - the Fed will flood the repo market with a proactive firehose of

liquidity.

There's more: add in the

incremental liquidity from the expanded overnight repo of about $50 billion and

another $60 billion in T-Bill purchases, and the Fed will inject a total of just shy of $500 billion in the next

30 days. This also means that by Jan 14, the Fed's balance sheet

would have grown by a cumulative $365BN in "temporary" repos, and

together with the expanded overnight repos, and the

$60BN in monthly TBill purchases, and

by mid-January, the Fed's balance sheet, currently at $4.066 trillion, will

surpass its all time high of $4.5 trillion!

See Chart:

FED

Balance Sheet

{kind=link}

Well, since the next key catalyst in the potential

repo market turmoil is imminent, we may know as soon as tomorrow, when

there is another large December corporate tax payment date (with as much as

$78BN being remitted to the TSY) and another $54 billion in US Treasury

settlements.

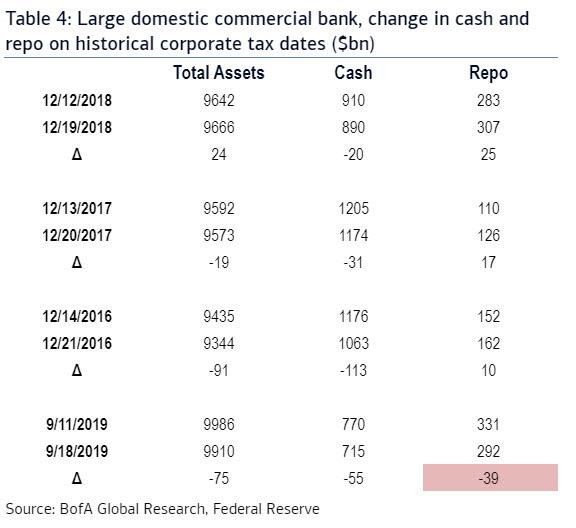

Recall, that as we explained

last week, the mid-December funding dynamics looks very similar to mid-Sep

except for the outsized role of the Fed. On Monday, Dec 16, Bank of America anticipates that $54Bn of UST

coupon settlements coupled with what has historically been $30-50BN of

corporate tax payments to UST. This could

result in a UST cash balance inflow - or a liquidity drain - of up to

$80-$100bn in just one day.

See Table

{kind=link}

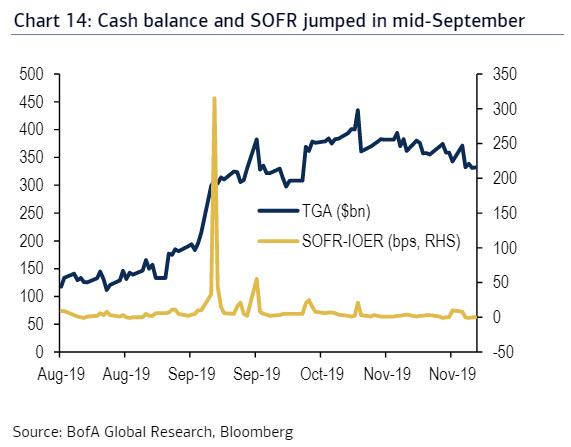

Also

recall, every dollar of UST cash

balance increase represents a similar USD reserve drain from the banking

system, and a similar liquidity drain in mid-September culminated with the now

historic explosion in overnight repo rates.

See Chart:

Cash Balance and SOFR jumped in

mid sept

{kind=link}

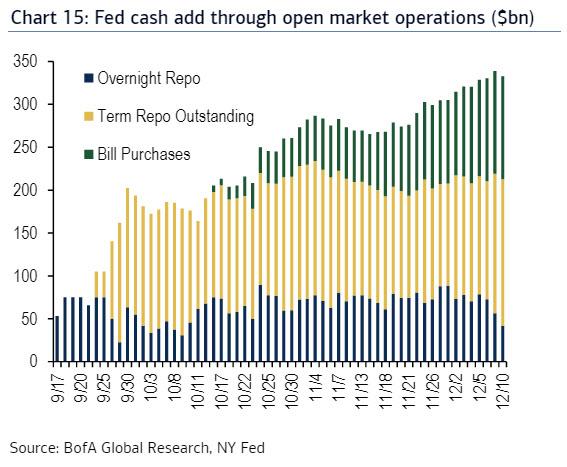

Consider

that as of last week, the Fed has provided $340bn in funding through their

existing repo and bill purchase operations:

See Chart:

FED

cash add through open market operations ($ Bill)

https://www.zerohedge.com/s3/files/inline-images/liquidity%20injections%20so%20far.jpg?itok=eVNRgPds

{kind=link}

As a result, Cabana notes that

even with this operational change, funding could still be volatile as bank portfolios and money fund

deposits get pared back amidst corporate outflows, while dealer intermediation of

Fed repos may also be challenged with year-end regulatory reporting dynamics

limiting how smoothly this funding gets passed along,

something Pozsar discussed extensively last week.

See Table:

{kind=link}

Still, as Skyrm cautions, "there is still

one major phantom year-end risk looming around the market. If the

Fed's term RP operations fully fund the Primary Dealer bank balance sheets and

the banks cannot increase their

balance sheets further, the last few Fed operations of the month might not have

any takers. There

is a chance there will be little Primary Dealer bank balance sheet left by

year-end."

In any case, when looking at

tomorrow's massive $100 billion liquidity drain, the repo market should be

able to digest it without a spike in the G/C repo rate now that the Fed has

effectively backstopped any and all year-end liquidity needs. If, however, the first repo prints

come in elevated: at 2% or higher, it will mean that not even the Fed's half a

trillion dollar liquidity injection was enough, and that Pozsar's fire and

brimstone forecast is starting to come true.

….

----

----

Paul Volcker from USA : un

Paretiano a destiempo: connect actions with

Nat-needs

Volcker understood at a deep and

intuitive level that all government institutions – including the Fed - have to

connect their actions to the needs of ordinary citizens.

====

Economically

speaking, hyperinflation is the inevitable

consequence of an ever-greater rise in the amount of money...

Increases in the Money Supply

Hyperinflation is perhaps the darkest side of a government fiat money

regime. Among mainstream economists, hyperinflation

typically denotes a period of exceptionally strong increases in overall prices

of goods and services, thus denoting a period of exceptionally strong

erosions in the exchange value of money. Some people

consider a rise in overall prices of 10 percent per month (which implies an

annual rate of price increases of around 214 percent) as hyperinflation; others

indentify hyperinflation as a monthly price rise of at least 20 percent (which

implies an annual increase in prices of nearly 792 percent).

According to the Austrian school, money is, like any other good, subject

to the irrefutably true law of diminishing marginal utility.

Money Demand

People hold money because money

has purchasing power (which people desire, given the fact of

uncertainty as an undeniable category of human action), and the purchasing

power of money is determined by the supply of and demand for money.

If a rise in the money supply is accompanied by an

equal rise in money demand, overall prices and the purchasing power of money

remain unchanged.

The Unrelenting Power to Inflate

If people expect a forthcoming,

drastic increase the money supply — but if they at the same time expect that

such an increase will be limited (i.e., a one-off increase) —

the central bank can actually orchestrate a debasing of money without causing

its complete destruction.

Debt Levels

Today's fiat-money regimes are characterized by

ever-greater amounts of debt relative to real income — caused by policies that try to solve the

economic problems caused by credit and money creation out of thin air by using

even greater amounts of credit and money created out of thin air. And it is fair to say that the higher an economy's overall

debt level is, the more likely hyperinflation becomes.

Should investors in such a situation expect that the government and its central bank would opt for bailouts financed through

additional money creation, the demand for money and fixed claims would most

likely dry up. This would make it necessary for the central bank

to extend ever-greater amounts of money to struggling borrowers in order to

prevent the spread of bankruptcies. The larger the

amount of outstanding debt is, the larger will be the potential increase in the

money supply. The more the money

supply grows, the more likely it is that there will be hyperinflation and a

potential breakdown of money demand: the unfolding of a crack-up boom.

Read the full article at

….

----

----

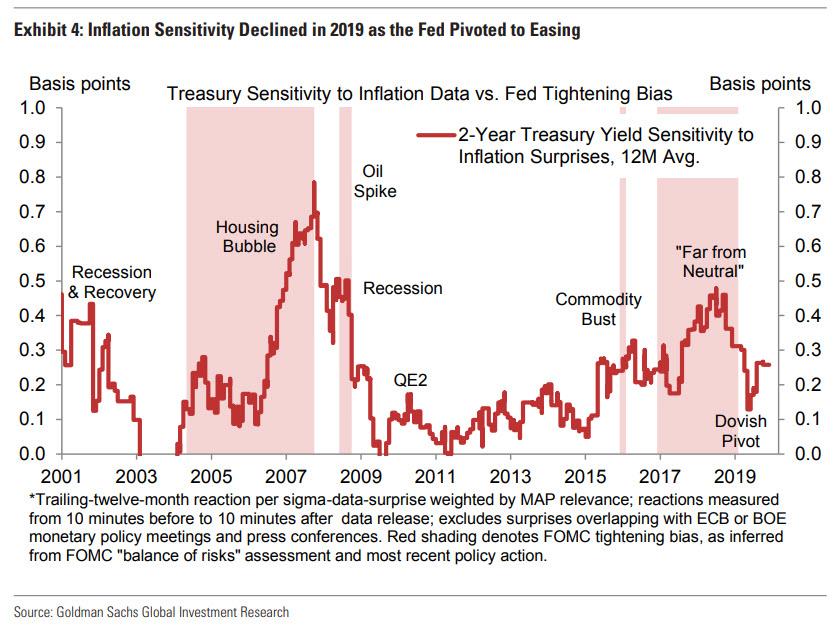

Market performance in 2020 will

largely depend on two things: response sensitivity to inflation and growth

data.

See Chart:

Inflation

sensitivity declined in 2019 as the FED pivoted to easing

{kind=link}

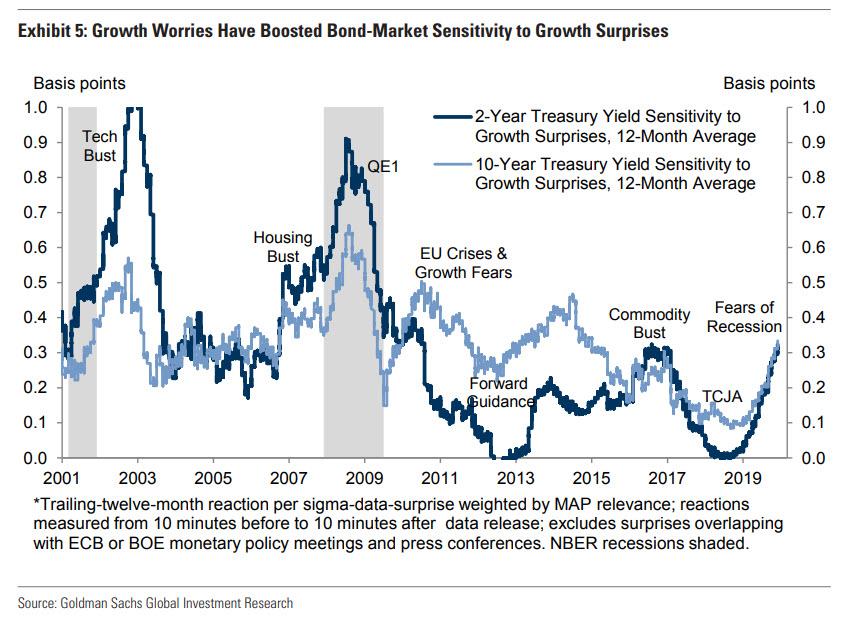

In

contrast, sensitivity to growth

data picked up sharply in 2019, reflecting slowing growth

and the return of recession fears. In fact, growth sensitivity in the bond

market is already back to its level during the shale

bust and capex-driven growth scare of 2016-17.

See Chart:

{kind=link}

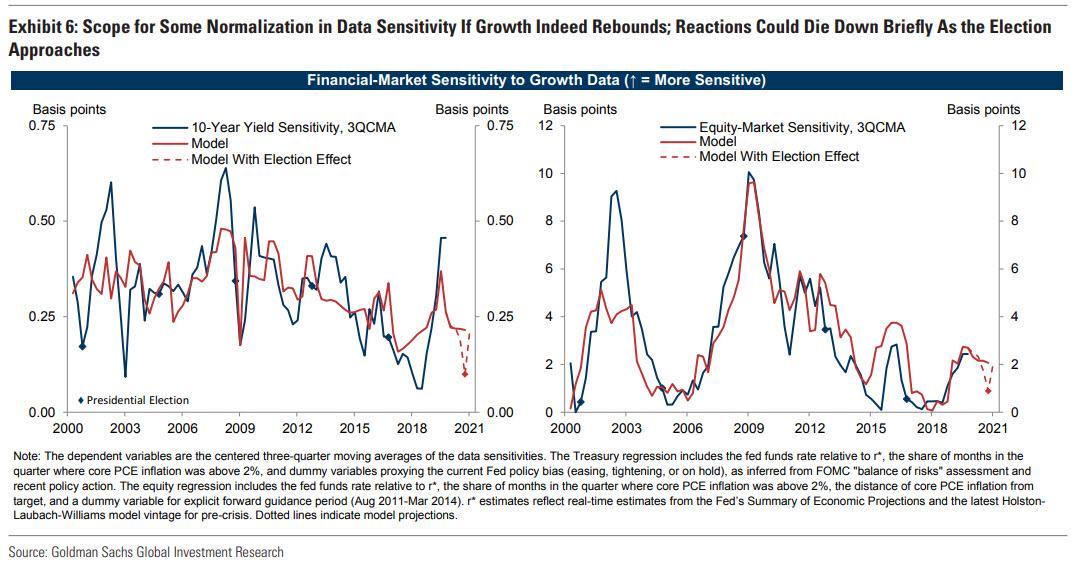

Looking

ahead to 2020, Goldman expects another signal reversal, as its forecast

of improving growth and diminished trade risks suggests scope for a modest pullback in sensitivity to growth data. Treasury-market sensitivity has already overshot relative to

the bank's predictions (see blue and red line in the left panel of

Exhibit 6), and the end of the mid-cycle adjustment

coupled with its expectation of firming US growth argues for more a normal

degree of data sensitivity in early 2020.

See Charts:

https://www.zerohedge.com/s3/files/inline-images/data%20senstivity%20normalization.jpg?itok=c1a0RvlN

{kind=link}

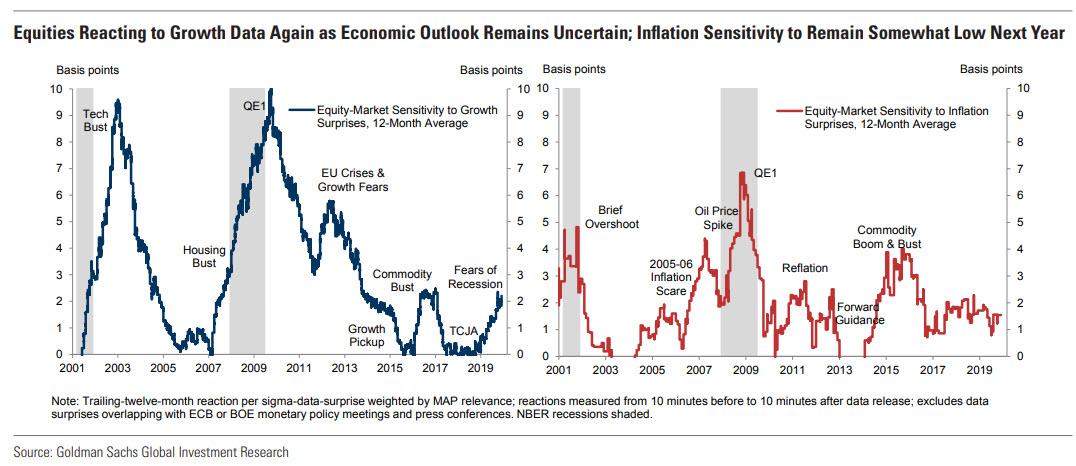

Similarly,

equity-market reactions to growth data could also wane a bit early next year if growth picks up.

See Charts:

Equities

reacting to growth data remains uncertain

{kind=link}

The implications for 2020 are

shown by the dotted lines above (i.e., a short-lived lull in data reactions in

the coming fall 2020).

In

contrast, the bank finds no such effects for inflation sensitivity. This may suggest that market participants

view elections as more important for the growth outlook than for the near-term

trajectory of core inflation (such that inflation news

continues to be an important driver of price action, even if growth surprises

are faded). In conclusion, Goldman expects inflation reactions to pick up

gradually in 2020 as inflation rebounds towards the target and the Fed begins

to contemplate its next move. All of that, of course,

assumes that inflation will rebound next year as most on Wall Street now openly

expect. However, if there is anything that 2019 once again vividly

demonstrated, it is that when everyone expects something, the opposite happens.

….

----

----

"Predictions

that seem obvious are obviously not obvious. How do you build a probability

tree for what comes next? What’s the output?"

====

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

It’s been a bad last 24 hours for the war propagandists...

====

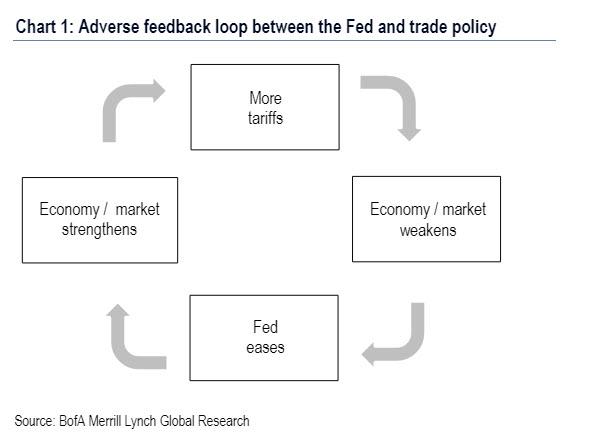

Trump may have taken what wasn't

broken, namely the tried and true strategy of ramping the market higher on

daily speculation and "trade deal optimism", and "fixed

it", in the process opening a trade deal Pandora's Box.

See Chart:

Adverse

feedback loop between the FED and Trade policy

{kind=link}

….

SOURCE https://www.zerohedge.com/economics/how-trump-opened-pandoras-box-announcing-phase-one-trade-deal

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

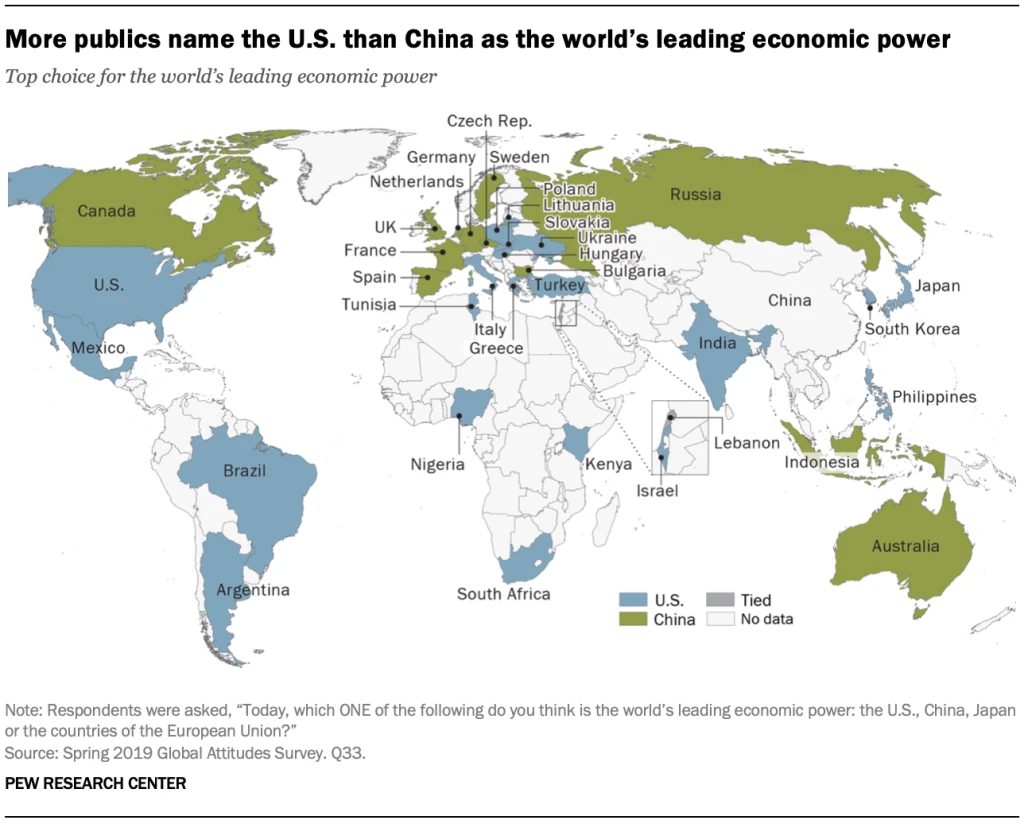

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

More countries see China as their No. 1 friend than you might

think...

See Map:

{kind=link}

The Pew survey was pretty

ambitious: 38,426 people in 34 countries participated between May and October

of this year.

….

See Source: https://www.zerohedge.com/geopolitical/china-or-us-worlds-superpower-heres-what-world-thinks

----

----

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

VIENTO SUR

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

===

No hay comentarios:

Publicar un comentario