ND

DEC 28 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

"We are likely to see governments and central banks launch a coordinated blitz made up of additional

trillions of pseudo-money and unbridled spending should a recession

hit..."

SUMMARY

- Interest rates and inflation couldn’t be more different today than they were in the 1970s.

- One of the shocking surprises of the last decade is that despite ultra-low, zero, or, even, negative interest rates inflation has generally fallen rather than risen.

- Yet, when it comes to asset prices (US stocks, global bonds, and real estate), it has been a completely different story.

- One asset class that hasn’t risen as swiftly as others is gold and other precious metals.

- This underperformance has caused most American investors—be they retail or institutional—to give up on precious metals as an essential asset class.

- However, John Hathaway, who is considered to be the “Warren Buffett of the precious metals space,” is much more bullish given all of the macro-economic factors at play.

- In the short-term, John and top economist David Rosenberg anticipate we could have a recession in 2020.

- This becomes much more probable should financial markets correct hard next year after this year’s historic and euphoric rally.

- We are likely to see governments and central banks launch a coordinated blitz made up of additional trillions of pseudo-money and unbridled spending should a recession hit.

- With most US portfolios heavily skewed towards paper assets (i.e. stocks and bonds) and nearly devoid of hard assets (i.e. energy producers/transporters, gold miners, copper producers, and agriculture nutrient companies) the stage is set for a significant paradigm shift over the next decade.

TAKING

THE HARD WAY OUT

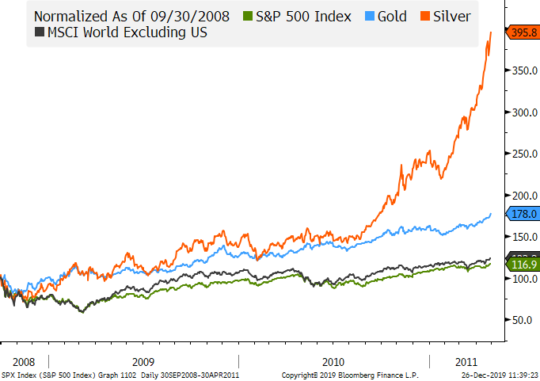

Early on, it looked like the assumed scenario would play

out. As QEs spread around the planet in the early part of this

soon-to-be-completed decade, the precious metals complex went postal. As usual

in bull phases, silver had the greatest surge, rising by 452% from its lows

during the Great Recession. Gold’s ascent was less spectacular, but it

nonetheless vaulted almost 170% from where it bottomed in late

2008. By the spring of 2011, both were far

ahead of global stock markets, including the S&P 500, once again measured

from the lowest points of the financial crisis.

See Chart:

2008 similarity wit current economics

{kind=link}

Fast forwarding to right now, it’s a very different story,

at least for the S&P. The most revered stock index on the Planet Earth is

up a prodigious 498.5% (total return) from its 2009 low-point, while gold and

silver have roughly doubled by comparison. However, they do look much better

compared to the global stock market index, excluding the US, since then; this

is due to how poorly international stocks have performed vis-à-vis the US.

(Ironically, in 2011 and 2012, overseas shares were all the rage, especially emerging

markets.) On the more embarrassing side, gold and

silver returns aren’t that much better than bonds over the past decade, despite

having a monster lead in the early years. (Platinum has performed even worse!)

See Chart:

From 2008 to 2019

{kind=link}

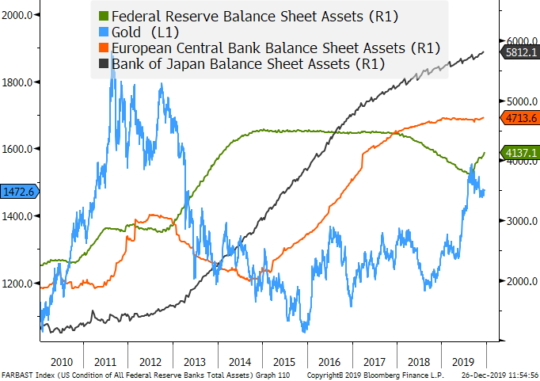

This long performance lag has caused most American

investors—be they retail or institutional—to give up on precious metals as an

essential asset class. After all, if they couldn’t deliver during a time of

ideal conditions (collapsing interest rates and binge-printing by central

banks), what could possibly cause them to rise now?

(Note: Central bank money fabrication causes their balance sheets to increase.)

See Chart:

Chart of Gold vs. Central Bank

Balance Sheet

{kind=link}

For those of you that don’t know of John, he is considered

to be the Warren Buffett of the precious metals space. He also lives near our

family’s winter home and I’ve had the pleasure of meeting him on two occasions.

Here is a bullet-point summary of Michael’s recap:

- With $13 trillion of negative yielding bonds around the world, it’s evidence of systemic risk that is far bigger than the housing/mortgage crisis of last decade.

- When interest rates do rise materially, it will trigger huge value declines for pensions and other institutions on their supposedly safe assets. He believes these losses will dwarf those seen in 2008.

- Almost no one today expects an inflation resurgence. That’s why gold is cheap insurance should governments resort to attempting to inflate away entitlement obligations (social security, Medicare, Medicaid, etc).

- We’re not going to see 1970s-type inflation, but it will be higher than we have now.

- The dollar is constantly described as the best house in a bad currency neighborhood but that’s crazy because the “hood” is going down the

- There’s a very good chance of a US recession next year.

- Gold is the “third rail” of money management. It’s been in the penalty box for so long that an investment advisor can get fired for even mentioning it.

- However, gold has recently broken out from a long basing period. The wind now appears to be at its back after six years of slogging. (Our “Going for the Gold” EVA in February, 2018, gave a strong endorsement to gold; since then it has generated a respectable 6% return.)

- Gold miners now have a reserve life that is the lowest in 30 years. They are very reluctant to build new

- Silver is gold on steroids. (Please refer back to the above chart of the former’s moonshot from 2008 to 2011.)

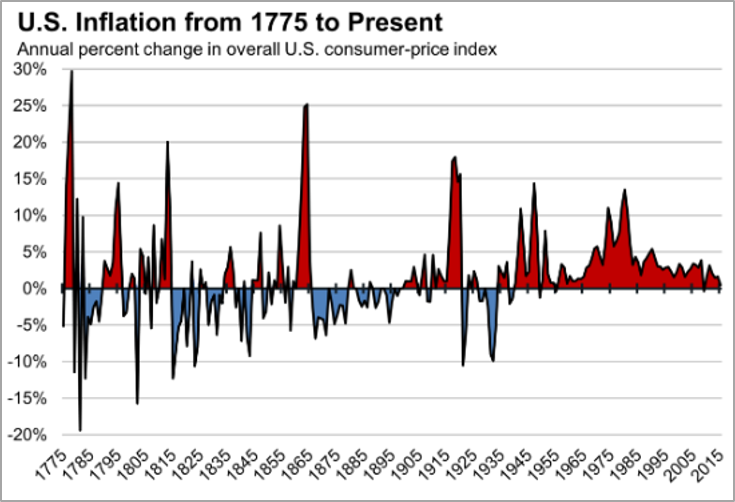

Ironically, prior to the creation of the Fed in 1913, US

consumer prices were stable for most of America’s 130-year history, outside of

the War of 1812 and the Civil War. The deflation in the non-war years prior to

1913 offset the brief inflation bursts, so that for over a century the dollar

roughly retained its purchasing power. Since then, outside of the Great

Depression and those eras when people like Bill Martin and Paul Volcker were in

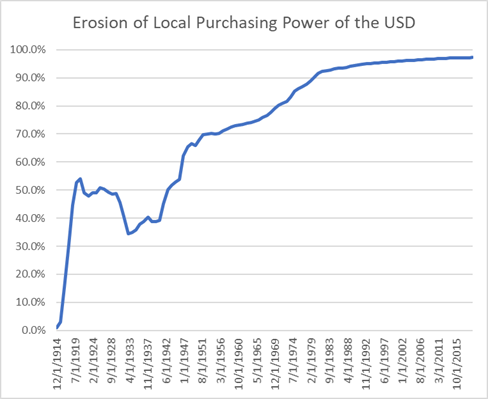

charge of the Fed, it’s been all downhill. The US dollar’s

purchasing power is less than 5% of what is was when the Fed opened its

impressive doors, on the eve of WWI.

See Chart:

{kind=link}

Erosion of Local Purchasing power of

USD

See Chart:

{kind=link}

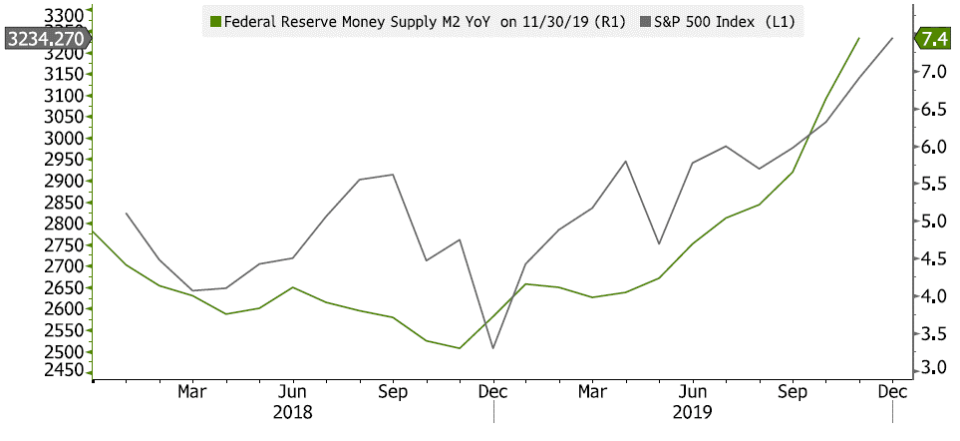

Due to the

Fed’s frenzied efforts, the money supply is in a ripping bull market of its

own. The correlation between M2 (the main

money supply metric) and the stock market recently has been remarkable.

See Chart:

{kind=link}

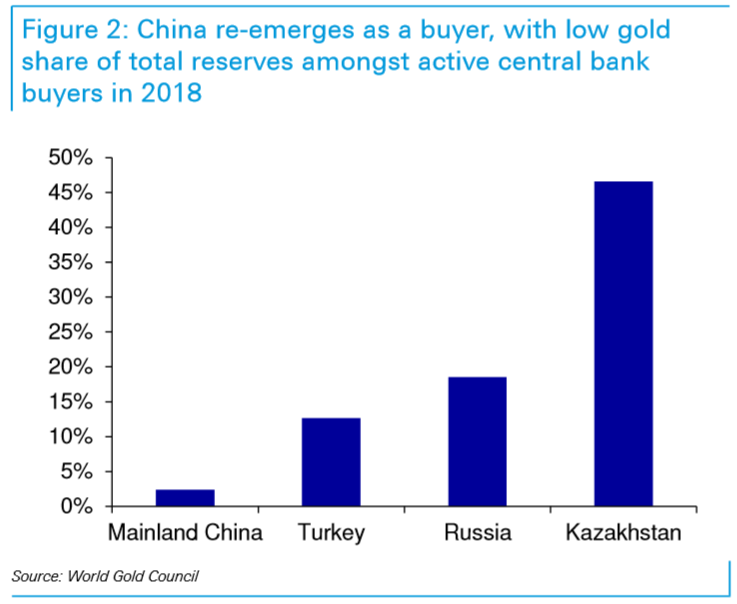

In China, however, that number is under 3%, implying that

gold could become a far larger component. This is particularly true given the

trade war with the US and China’s increasingly dim view

of the dollar’s long-term purchasing power. (I can’t blame them, can you?)

See Chart:

China re-emerges as a buyer with low

gold share of total reserves

{kind=link}

With most

US portfolios heavily skewed toward the paper asset category and nearly devoid

of hard assets, the stage is set for one of those paradigm shifts that is

exceedingly painful for backward-looking, trend-following investors. As noted in last week’s EVA, that is

everyone who is heavily involved with today’s most popular investment

vehicles--US-focused stock index funds.

Per Jack Ma’s quote at the opening

of this EVA, when money is too

abundant bad decisions are made and they typically involve the recent

performance stars. There’s never been a time in American history

when there has been this much excess liquidity greasing the markets for paper

assets. If there was ever time to channel your inner

contrarian, this is it—asap, if not sooner!

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

As the New Cold War gathers up speed and escalates, we are entering a “fact-free world” as

allegations are made that are proved not to be true are promoted...

====

====

Paging Neel

Kashkari...

====

"Wow Crazy Nancy,

what’s going on? This is big stuff!"

====

How George Soros

manipulates and corrupts governments for fun and for profit...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

"If we do not cut our

anger emissions immediately, the world will be consumed by fiery outrage by the end of next

year,"

====

By the end

of 2020, 6.5 million Venezuelans

are expected to have been forcibly displaced outside of their home

country.

====

Washington must think the

rest of the world is as stupid as many of its own politicians

are...

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

VIENTO SUR

====

RT EN ESPAÑOL

Un hombre apuñala a varias personas con un machete

en una sinagoga de N Y https://actualidad.rt.com/actualidad/338220-tres-apunalados-ataque-machete-sinagoga El que a hierro mata, a hierro muere.

-Evo Morales: El papel de EE.UU. es "tan evidente en el golpe de

Estado en Bolivia" que su Embajada en Argentina "habla por los

golpistas" https://actualidad.rt.com/actualidad/338181-evo-morales-participacion-eeuu-golpe-bolivia-evidente

-Lo que queda al descubierto tras el asedio del gobierno de facto de

Bolivia a la embajada de Méx https://actualidad.rt.com/opinion/javier-buenrostro/338135-asedio-gobierno-facto-bolivia-embajada

-Camacho aparece en un video admitiendo que su padre pactó con la Policía

y el Ejército (y Morales dice que eso confirma el golpe) https://actualidad.rt.com/actualidad/338212-luis-fernando-camacho-admite-publicamente-padre-acuerdo-policia-ejercito

----

===

No hay comentarios:

Publicar un comentario