ND DEC 24 19

SIT EC y POL

ND denounce

Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

FELIZ

NAVIDAD y PROSPERO AÑO NUEVO

La navidad

es día de paz, reconciliación y unidad familiar

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

"If

the market never reacted negatively to all the bad news that it had to digest

throughout 2019, aren’t they already pricing in all the good things that may or

may not come?"

See Chart:

{kind=link}

----

See more interesting charts at:

SOURCE: https://www.zerohedge.com/markets/market-has-priced-fastest-economic-recovery-financial-crisis

----

----

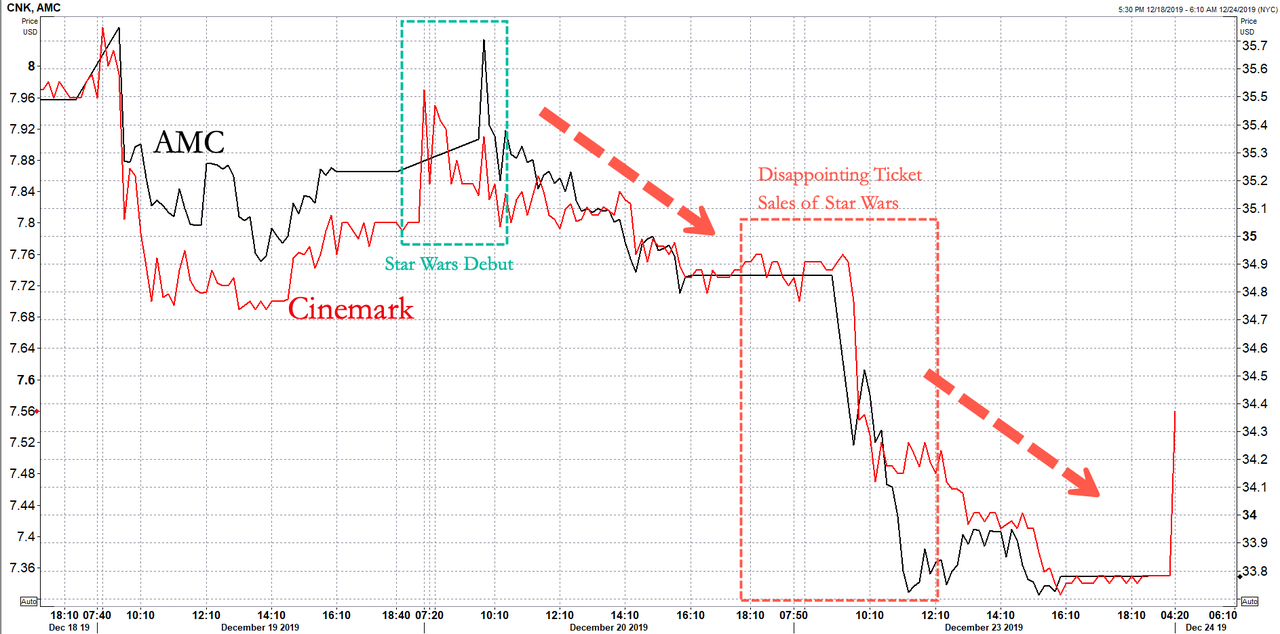

Only Trump can ruin the Economy more than it is now

"The

reception, far below predecessors, may have been partly due to mixed critical

reviews."

See Chart:

{kind=link}

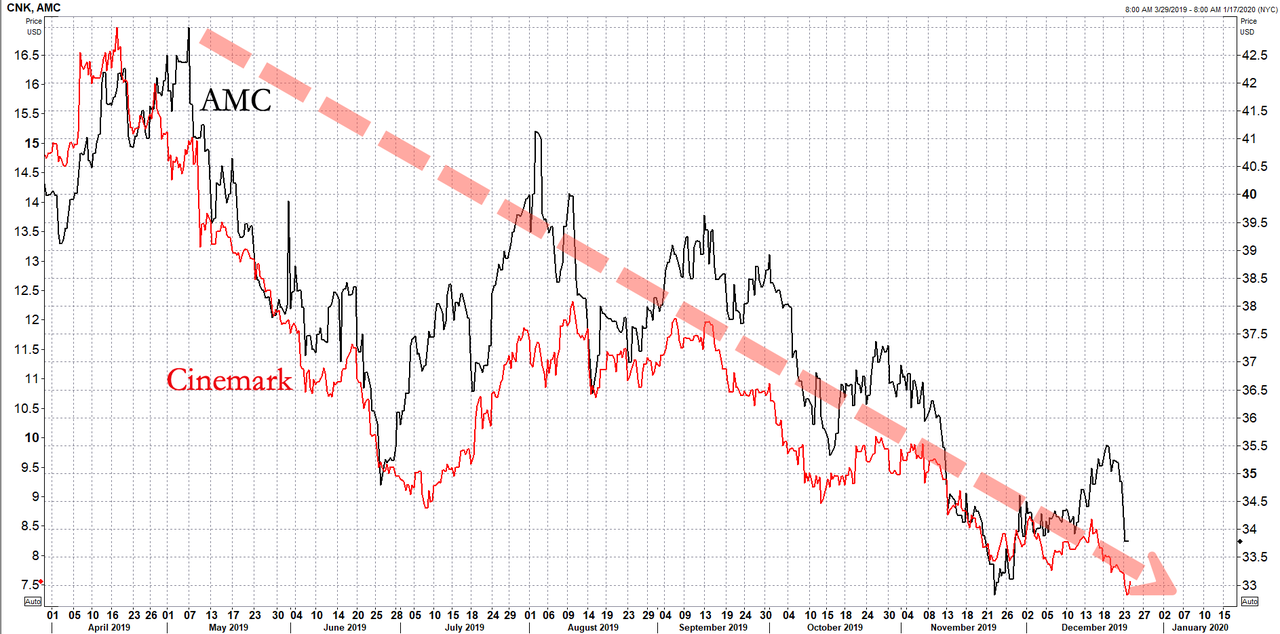

Theater stocks have exhibited

declines throughout most of the year.

See Chart:

{kind=link}

You will find more infographics at Statista

The movie theater industry is always changing, there are ups

and downs, but these days -- it's in a secular decline as streaming services

have undoubtedly changed consumer preferences of how they watch movies. So in the next decade, or let's say by 2030 -- will movie theaters even

exist?

….

----

----

As one would expect volumes today

were dismal, around 50% below average (pro-rata) ahead of the early close...

See Chart:

{kind=link}

Bonds were bid after a very strong

5Y auction

See Chart:

{kind=link}

Today's drop in yields erased

yesterday's price losses...

See Chart:

{kind=link}

Here's why Small Caps were bid -

Shorts squeezed out of the gate again...

See Chart:

{kind=link}

The Dollar trod water once again -

following a similar pattern to yesterday...

See Chart:

{kind=link}

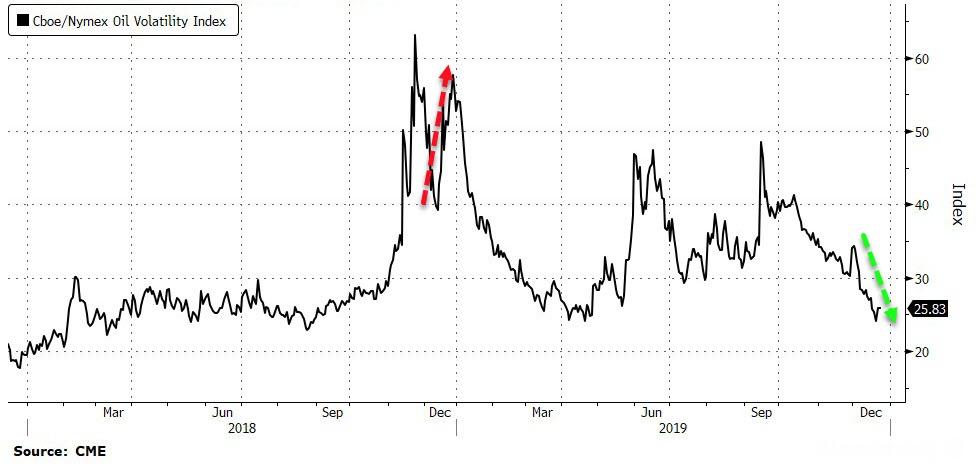

And oil vol is less than half what

it was last Xmas Eve...

See Chart:

{kind=link}

Finally, we note the difference

between now and one year ago exactly...

See Chart:

Fear & Greed Index Xmas eve 2019 vs. Xmas Eve 2018

{kind=link}

And here's why the ‘grate bubble:: .. The addition

of $5 trillion in global liquidity!!

See Chart:

Global Liquidity Proxi S&P

{kind=link}

Is Jay Powell the real ‘Santa’?

[ or a true ‘Satanas’ ]

….

----

----

The sale of

$41 billion in 5Y notes was nothing short of stellar, with the high yield

stopping through the When Issued by a whopping 1.6bps, the biggest stop through

since February 2016.

====

The idea that money

printing is an insurance policy that does not come with a cost is simply wrong...

See Chart:

FED Balance Sheet (USD Millions)

{kind=link}

REPO CRISIS

The Fed is in fight-or-flight mode because there are very

real credit bottlenecks in the plumbing of the banking system that have created

a US Treasury funding emergency. The central bank has been forced to add $364

billion of Treasury securities to its balance sheet over last four months and

has committed to another $471 billion though mid-January. The money printing

was necessary to fight a repo market funding shortage that warns of a systemic

financial crisis in the making. Usually when the repo alarm bell flashes, it’s

too late.

The 10-year yield had its biggest year-over-year decline

ever. After such a move, this trade simply became too crowded. In our

view, it has already played out. Today, we believe

there is a strong case for rising global yields on the long end of the curve as

we explain below.

See Chart:

US 10 Y Yield

{kind=link}

RUNNING HOT

The Fed’s monetary policy is running hot and long-term

interest rates aren’t aligned accordingly… For instance, the 10-yr yield vs.

the Baseline Taylor Rule rate is now at its most extreme in 44 years. Inflation

became a problem during all times this spread went negative. What makes this

issue even more unique is the fact that on top of

running an extreme loose rate policy, the Fed is printing money in a massive

way. It’s hard to say monetary policy won’t come at a major cost this time.

See Chart:

US 10 Y Yield -Taylor Rule Rate

{kind=link}

Below are similar disparities across

the globe to consider.

See Table:

{kind=link}

THE LABOR MARKET

AND CONSUMER CONFIDENCE – FALLING INTO PLACE

Stocks are on pace for their best performance in 22 years

all the while many key fundamentals such as corporate earnings and industrial

production have been deteriorating all year. Continued

gains for the broad stock market in 2020 are highly improbable in our

view as even more of the key fundamentals in the jobs

and consumer market are only just starting to roll over from exuberant extremes.

See Chart:

S&P 500 Annual Performance

{kind=link}

The ADP report calls into question the more optimistic BLS

job numbers with the largest negative divergence since 2010. The year-over-year

change for ADP payrolls is decelerating in a pattern last seen directly ahead

of the Global Financial Crisis. What’s crucial is that

the 3-month rolling average of ADP payrolls leads the rate of change in

unemployment rate by 3 months with a correlation of almost 0.9!

See Chart:

US LABOR MARKET

{kind=link}

US CONSUMER CONFIDENCE

We have likely reached peak consumer complacency, another

key piece of the macro puzzle. After retesting tech bubble levels, the

Bloomberg Personal Finance Survey index is now falling and significantly

diverging from the Conference Board’s Consumer Confidence. With the jobs market topping out, we believe consumer

confidence will be the next shoe to drop.

See Chart:

US CONSUMER CONFIDENCE

{kind=link}

COST OF

CAPITAL POISED TO RISE

The bull case for stocks rests on one major liquidity force,

the cost of capital. That’s driven by the availability of credit and the

strength of company fundamentals. When looking at equities broadly, aggregate earnings

per share for Russell 3000 index just started to fall on a year over year basis. Furthermore, corporate balance sheets never looked so weak.

For instance, the Bloomberg Barclay

High Yield (Ex-Energy) Index today is at its lowest premium to 10-year

Treasuries since June of 2007.

See Chart:

{kind=link}

We believe this shift in mindset is already forcing

companies to either raise prices of goods and services or cut costs to improve

margins, and we expect this trend to continue. These

changes should have a significant impact on consumer prices, labor markets, and

the business cycle.

In this backdrop, we question if the demand for low-rated

bonds will remain strong relative to higher quality assets. Junk bonds only yield 180 basis points higher than median

CPI! It’s the lowest level in the history of the data.

See Chart:

Junk Bonds Real Yields (Ex Energy)

{kind=link}

PRECIOUS

METALS

We believe strongly that this time monetary policy will come

at a cost. Look in the chart below at how the new wave of global money printing just initiated by the Fed in response

to the Treasury market funding crisis is highly likely to pull depressed gold

prices up with it.

See Chart:

Global Central Bank Assets vs gold

{kind=link}

ZERO

DISCOUNTING FOR INFLATION RISK TODAY

With historic Federal debt relative to GDP and large

deficits into the future as far as the eye can see, if the global financial

markets cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money printing at

this point in the economic cycle may hasten the unwinding of the imbalances it

is so desperate to maintain because it has perversely fed the last-gasp melt up

of speculation in already record over-valued and extended equity and corporate

credit markets. It is reminiscent of when the Fed injected emergency cash into

the repo market at the peak of the tech bubble at the end of 1999 to fend off a

potential Y2K computer glitch that led to that market and business cycle top.

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Another

bite at the apple?

----

Could come the Scorpion bite. If crimes against humanity is the aim

====

The sheer number of people

involved in just the FBI scandal is phenomenal...

….

Trump got the PENTAGON & Dems the FBI. The one who get the People

win. There was not “great cover up”. It was a sisi & weak cover up. Now we

may have a great open up.. starting with election IF & only IF we have free & fair elections. This implies starting

by cutting the freedom from billionaires’

to buying election. This is fraud, worse if they control the machines to

counting votes. Fair election mans ‘inclusion” and it implies to include the 3rd

option in the distribution of power. The ideal

is: 50% of power to winner, 30% to the 2nd voted party and

20% to the 3rd option, it doesn’t matter the amount of votes each

get in the ballot-box . This 3rd option open the chance to mediate

the stupid conflict bet Dems & Reps (both financed by same/similar corp ). To

get this point we need an asap meeting bet

Dems-Reps to reform the current

electoral rules. With the current one whoever wins won’t have chances of

governability. The obsolete duopoly system we have will lead to rush political

confrontation and possible civil war. That is more clear than water.

====

Current neoliberal research: an enemy of future generation.

"...this ‘invisible’ approach could create new possibilities for data storage, biosensing, and vaccine

applications that could improve how medical care is

provided..."

====

There are only two constitutionally viable alternatives: either Pelosi

must announce that Trump has not

been impeached; or the Senate mustinitiate a trial...

====

Are we on the right track as

a nation?

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

WW3 IS CLOSE:

Geopolitics has moved from a slow-moving, relatively predictable chess

match to rapidly evolving 3-D

chess in which the rules keep changing inunpredictable ways.

====

Andrei Martyanov’s latest book provides unceasing evidence about the kind of lethality waiting for U.S. forces in

a possible, future war against real armies (not the Taliban or Saddam

Hussein’s)...

====

...the launch of the first

ever floating nuclear power plant has become an important

engineering breakthrough that will

impact the energy sphere on a global scale...

====

"The

US quest for a partnership with China was fated to fail once China's growth in

economic capabilities was gradually matched by its rising military

power."

….

Trump style of mixing geopolitics

with geoeconomics (uses of military power to force deal & agreements) is a

real obstacle to negotiate with China. We need Chia, they don’t need as. Either

Trump change his style [ impossible in

my view] or we change him (very possible

with both Sanders & Elizabeth Warren alliance. The one who win take the

other as VP).

====

...even Stalin found the

Santa Claus aspect of Christmas worth preserving, and he apparently

calculated that a father figure bearing gifts might be useful after all.

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

====

ALAI NET

ORG

----

===

No hay comentarios:

Publicar un comentario