ND DEC 3 19

SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

"So, where are we today? Today,

we have the S&P 500 is killing everybody..." But what happens next

could be devastating.

Jeff Gundlach sat down

with Yahoo

Finance and discussed how US stocks would get

absolutely crushed in the next recession. Gundlach said 2019 was the year when

investors could pick "just about anything...Just throw a dart, and you're up 15-20%, not just the United States, but global

stocks as well." He warns that it could all change in 2020, as a

recession is fast approaching.

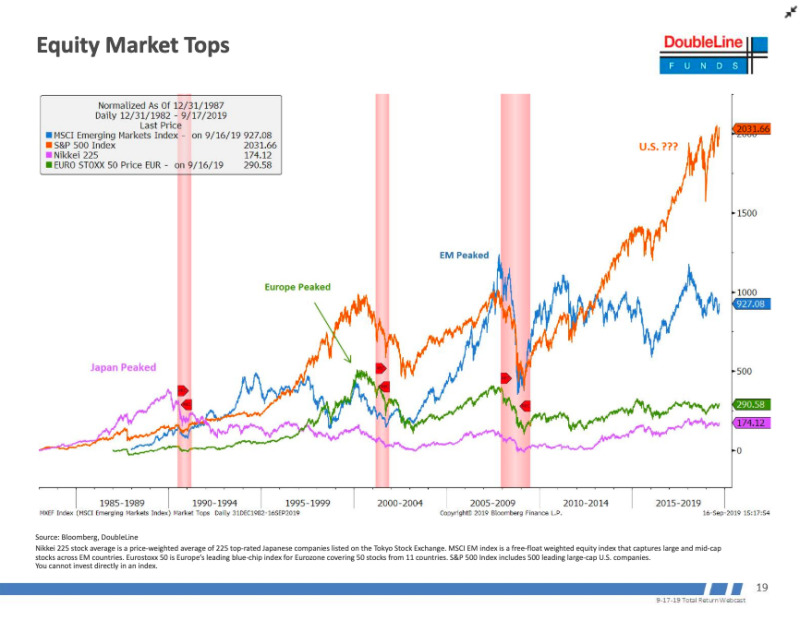

"So,

where are we today? Today, we have the S&P 500 is killing everybody else

over the last ten years, almost 100% outperformance versus most other stock

markets," he said.

See Chart:

Equity

Market Tops

{kind=link}

"My

belief is that pattern will repeat itself," said Gundlach, who has spent much of 2019 warning of a downturn ahead

of the 2020 elections.

"In other

words, when the next recession comes, the United States will get crushed, and

it will not make it back to the highs that we've seen, that we're floating

around right now, probably for the rest of my career, is what I think is going

to happen," he added — suggesting that a recovery won't be seen for years.

Last month, Gundlach warned about the levels of government debt, and the US equity markets are not sustainable. He told

investors that they should brace for significant disruptions.

"The

corporate bond market in the United States is rated higher than it deserves to

be. Kind of like securitized mortgages was rated way too high before the global

financial crisis. Corporate credit is the thing that should be watched for big

trouble in the next recession."

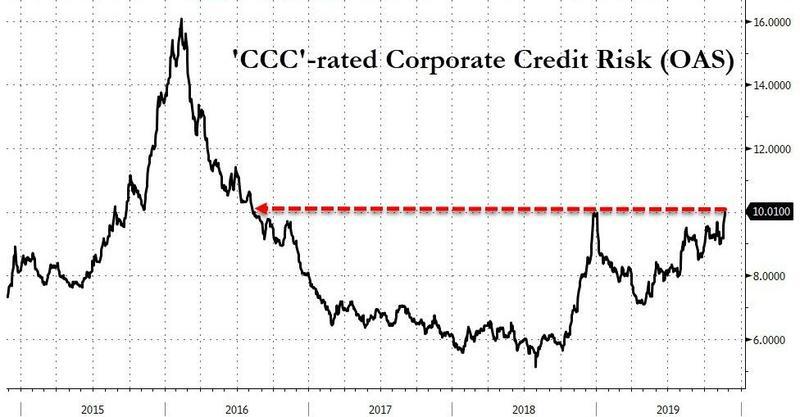

And maybe a downturn in the economy has already started, considering

credit markets usually lead. As shown below, significant

cracks in the junk bond space are beginning to appear:

The spreads on CCC US junk bonds have jumped above 1,000bps for the first time in more than three years as

a sell-off in energy weighs on the lowest-rated debt.

See Chart:

‘CCC’

–rated Corporate credit risk (OAS)

{kind=link}

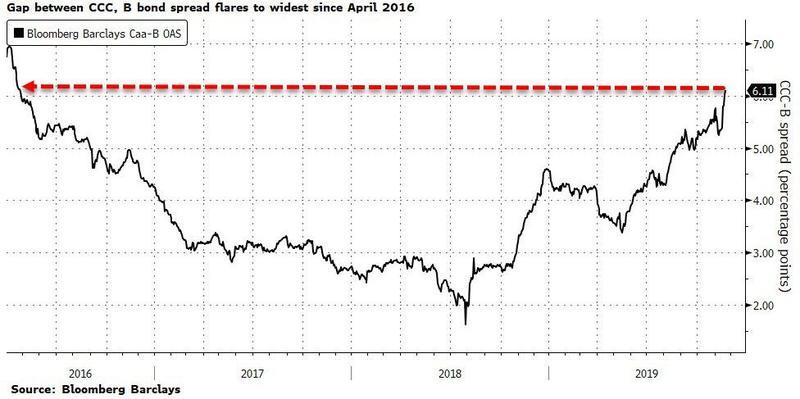

Blowing

the CCC market's risk out to its widest against single-B since April 2016...

See Chart:

Gap

between CCC, B bond spread flares to widest since April 201

{kind=link}

Generic

CLO BBB tranche is starting to flash very red...

See Chart:

DOW vs. Generic CLO

‘BBB’ tranche

{kind=link}

The broader junk bond market posted negative returns last

month... as stocks have soared..

See Chart:

S&P vs HYG

{kind=link}

Gundlach's

Sept. presentation titled "The

Greatest Economy Ever!" made it clear that the next big move for the dollar is lower, and warned

that when the next recession occurs, the US dollar and

stocks will be in trouble, recommending investors to diversify into

other currencies and markets.

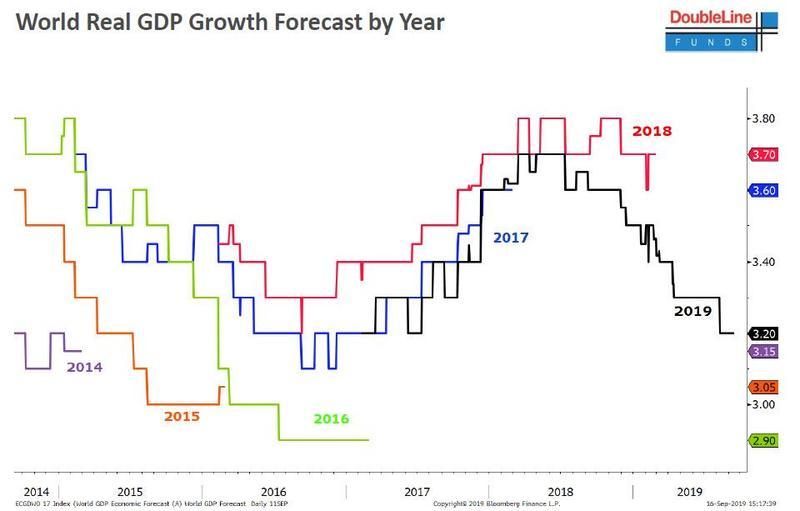

And since

his view on the economy is that it is anything but the

"Greatest Ever", pointing out the sharp slump in 2019 global GDP

projections...

See Chart:

World Real GDP Growth Forecast by Year

{kind=link}

And as we've

said on multiple occasions, the next

shoe to drop is likely the consumer. Something that Gundlach is waiting for

as well explained in the latest interview with Yahoo.

Highlight: A recession probability "is around 40% right now," @truthgundlach says. "The ISM looks bad... Consumer sentiment, though, remain

at a decent level. What we have to watch for is consumer confidence declining,

because that's almost definitional we cause a recession."

LISTEN THIS VIDEO-Interview with Gundlush on

recession concerns:

….

----

----

Puedes agarrar este toro por donde

quieras, menos por las astas. Por allí se lo mata o mueres

...and now bulls need to

prove that they can sustain new highs. It is key for how the rest

of 2019 plays out...

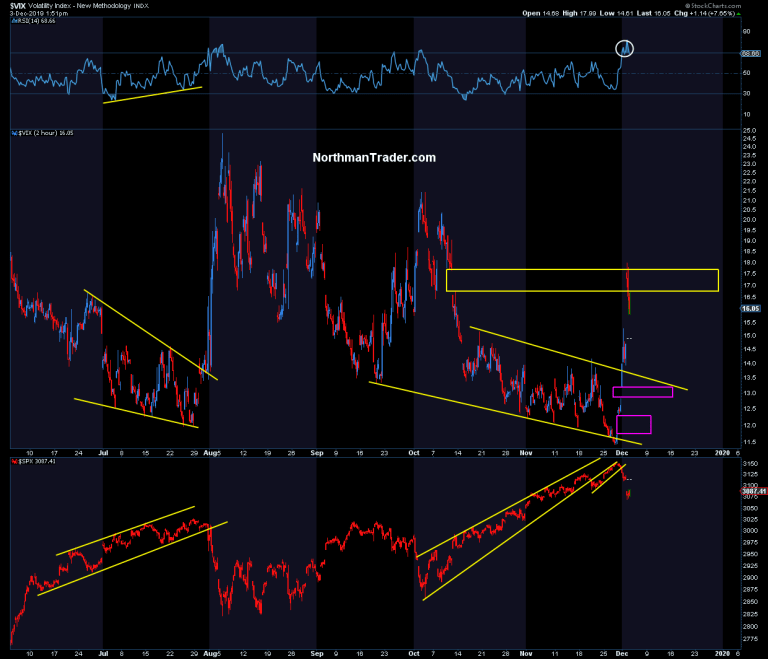

After weeks

of rallying on low volume on virtually relentless volatility compression the

inevitable has happened: $VIX has busted out of its latest compression

phase for another big spike very similar to what we saw this summer.

In process

most of the November gains were wiped out in 3 days. What does this mean for

the rally? Let’s have a look at a few key charts.

Firstly, like this summer, the $VIX burst

targeted an open gap above, the 17/17.5 gap left open

following the Fed’s QE announcement:

See Chart:

{kind=link}

And like this summer $VIX has become short term overbought and

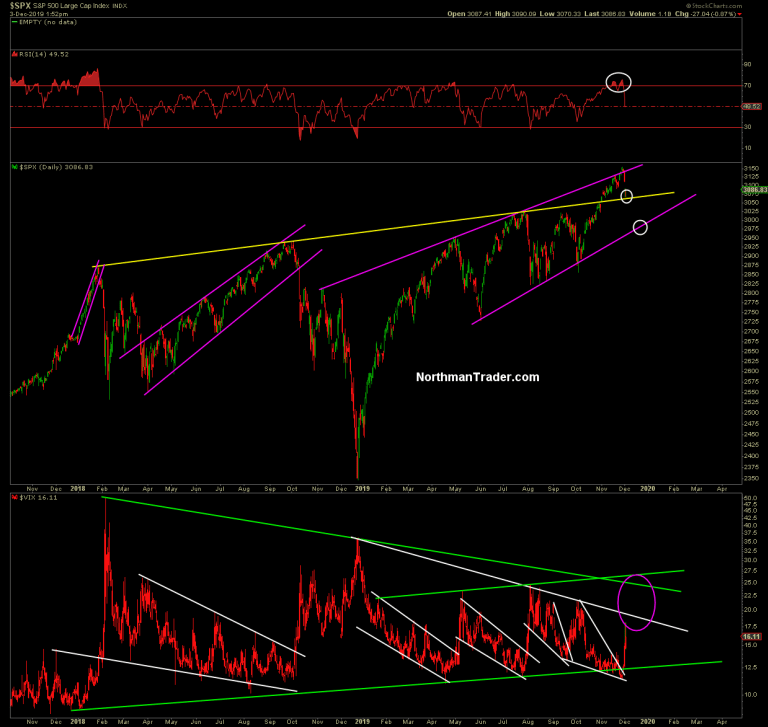

like this summer $SPX broke its up trend in the process. Hence on the surface this is all a very similar looking replay of structures.

BUT there is

a difference. Since the massive liquidity injections by

the Fed began $SPX managed to break above the megaphone and rallied until it

hit trend line resistance last week:

See Chart:

{kind=link}

Oh yes,

markets can be this simple, trend lines matter:

Markets are simple.

We just make them complicated.$SPX

We just make them complicated.$SPX

See Chart:

At this link address:

And so the

rejection of $SPX makes perfect technical sense.

In the

summer I had pointed out that a breakout above the megaphone trend line that

gets successfully retested would be bullish, likewise a retest that fails would

be bearish.

Today $SPX is engaged in that retest process and it’s key

that bulls defend this trend line:

See Chart:

{kind=link}

A COUPLE COMMENTS:

One: During

the recent rally the RSI became the most overbought in 2019.

Two: In

October $SPX broke above resistance (yellow line), and has now reverted and is

retesting this line as support. If a bounce can hold and make new highs from

here it’s bullish. If it can’t hold support or a bounce fails to make new highs

this would suggest a potential move to the lower trend line 3000-3030 support.

If that breaks watch out, things could get very shaky in markets.

Three: $VIX broke out of its most recent compression

pattern and filled its open gap of 17/17.5 today. Hence resistance and reversal

intra-day now along with $SPX are support conducive for a bounce/rally.

BUT should support fail on $SPX, $VIX has risk higher.

There are 3 trend lines above that suggest resistance on any $VIX spikes. Above

the first line the secondary line suggests 21/23, the next larger line, if the

previous doesn’t hold, suggests a move toward 27/28.

OF NOTE: Despite successive marginal new highs on $SPX

$VIX has maintained a general trend of higher lows. Hence if $VIX were to

break above all of these trend lines we may see a revisit of the 30-50 range.

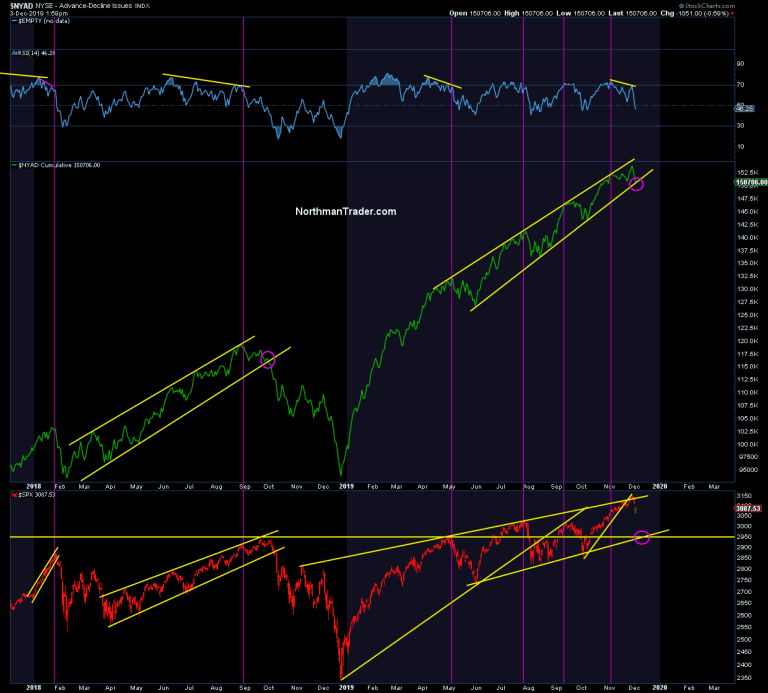

Unfortunately? Not really if you look at $NYAD:

See Chart:

{kind=link}

Here too we

can observe a very repetitive structure, in this case a large channel that is

now sitting at key support.

When the 2018 channel broke it led to a very ugly period for

markets marked by a period of very high volatility with lots of long and short

trading opportunities. Indeed the chart above suggests key trend line support

below on $SPX should this $NYAD channel break to the downside.

If it does

and $SPX experiences a more sizable correction than currently, bulls are faced

with a larger issue: That the megaphone breakout was

false and did not sustain. As I outlined in Game Over? $VTI is sending a different message altogether.

So yes, defending these support zones here is key for

bulls. Falling below the megaphone trend line would

risk that markets are repeating the pattern that we’ve seen over the past 2

years: That new highs are not sustained. The September 2018 highs

petered out 3.5% above the January 2018 highs. The July 2019 highs petered out

3% above the September 2018 highs. In all of these

previous cases we saw sizable corrections off of new highs. These highs here have

so far ended at 4% above the July 2019 highs.

And now bulls need to prove that they can sustain new highs. It is key for how the rest of

2019 plays out.

….

----

----

Como y por que el capitalism nos

aplasta. Why capitalism smash & crash us?

This time really is different.

To regular

readers of Zero Hedge, and generally contrarians, it will come as no surprise

that the structural forces Lambregts is referring to relate principally to

our financialization thesis:

this refers to a trend that has been evident for decades in Western economies

(but arguably increasingly elsewhere in recent years) whereby corporations have increasingly favored

investment in financial rather than fixed assets.

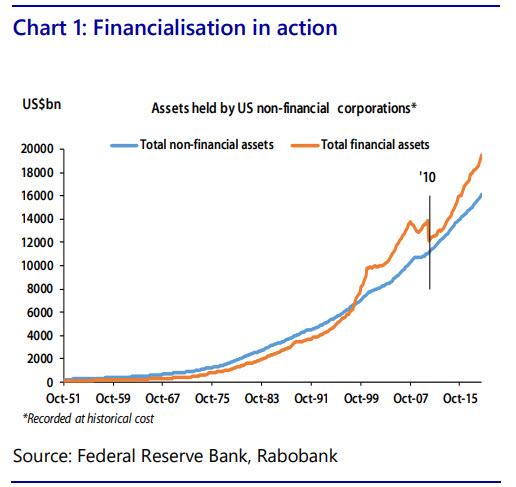

The first chart below stylizes this thesis by showing

the holdings of financial and non-financial assets on the part of US

non-financial corporations since the beginning of the 1950s. As can be seen, since the

mid-1990s, US companies have clearly favoured financial investment vs. the

“real” thing. 2010

is highlighted on this graphic as it is at this point that the crisis-induced

correction in corporate financial asset holdings rapidly reverses. This is attributable to the onset of QE which only served to further encourage corporate

investment in financial assets owing to the de facto government put implied by

the central bank purchase program.

See Chart 1:

Financialisation in action

{kind=link}

As

corporations focused largely on growing their financial assets, the flip side

was made apparent in the corporate behavior encapsulated in the next chart,

which as ING notes, shows the collapse in net fixed investment demand as a share of GDP

during the financial crisis and the fact that the subsequent

recovery has only taken investment’s share of the economy back to the cyclical

lows repeatedly forged through the post-WWII period.

This, then,

helps explain a conundrum economists have been struggling with in recent years which is why

fixed investment demand is still so slow this many years after the crisis

despite the historical and, in certain instances, record low cost of

capital. Rabobank's thesis argues that corporates have taken advantage of low borrowing costs but

not to invest in organic growth but as a means of undertaking financial value engineering.

Se Chart 2:

Fixed Investment demand remains in

the duldrums

{kind=link}

This view

also provides a plausible means of addressing another post-crisis puzzle which is

why productivity growth has remained so low (since

2010, US productivity has been growing at its slowest speed on average in the

post-war era). This, as Rabobank further notes, should be no surprise given the clear bias of corporates to accumulate

non-productive financial assets rather than undertake productive fixed

investment.

This, in turn, helps explain why estimates of US potential

output have collapsed in the post-crisis period. The chart below

highlights this development in showing the sharp decline

in recent years of New York Fed’s estimate of the natural, or neutral, policy

rate. This is the real policy rate level deemed suitable for meeting the Bank’s dual mandate of full employment and 2%

inflation. Crucially, trend growth is a key

assumption underpinning this assessment.

See Chart 3:

The bi-product of a sharp decline in estimated US potential

output:

The US‘ estimated

natural rate of interest

{kind=link}

This "financialisation"

thesis can also help explain the scarcity of developed world wage inflation

despite historically low levels of unemployment.

In large part, this is owing to the fact that higher wages in the

absence of productivity growth implies lower margins. This is a development

that has arguably been resisted by Anglo-Saxon

companies as higher wages within this context would result in workers enjoying seniority in terms of access to profits vs.

shareholders – the very opposite of the share-value maximisation corporate

governance model that ING argues has been increasingly prevalent since the

mid-90s.

The next

chart shows the long-running crowding out of the US

workforce in the form of labor’s share of (declining) national income from the

1960s onwards. The chronic nature of this trend reflects the fact that

there are other structural forces at play which have been disadvantageous to

developed world workers – specifically, globalization and robotization. Yet

while these factors have long been widely acknowledged, Rabo's focus is upon

the less appreciated “-ation” - that of financialization.

See Chart 4

US workers

taking home a a historically small slice of the pie

{kind=link}

The

accelerated crowding out of labor at the turn of this millennium is also

reflected in the explosion of US corporate profitability shown in the next

chart. Taken together

with charts 2 and 4, Rabobank argues that these three visualizations make it

clear that these profits failed to make their way either to labor or to fixed

investment while Chart 1 implies

that financial value engineering was the ultimate destination.Taken

together, Charts 4 & 5 reflect a post-crisis

development that has been crucial from a social perspective.

See Chart5:

US Corporate

profits has exploded in post crisis period

{kind=link}

To

summarize, Rabobank's core thesis is that recent decades have seen corporates

(initially in the Developed world) increasingly avoid fixed investment in favor

of that of a financial variety. Central banks have, ironically, accelerated this process by directly

intervening in financial markets. The upshot

of this has been a rapid appreciation of financial asset values BUT at the

direct expense of real world activity (a cannibalization of fixed investment

demand), a concomitant stymieing of productivity growth and, by extension, a

crowding out of labor.

In other

words, it is central banks themselves that are behind

the global economy's dismal - and ever slowing - growth rate.

Viewed in

this way, financialization

can be judged to be a zero-sum game whereby what is good news for those long

financial assets is bad news for those long income. The divergence of the lines in

Charts 4 and 5 thus reflects a yawinng inequality gap that has grown markedly

in the post-crisis period. This, in turn, has resulted in a growing segment of

developed world populations becoming disaffected as they fall further behind

and are, as a result, increasingly looking for none stablishment

political solutions. This

is not simply of sociological interest but also of keen strategic importance as

it argues that populism itself is structural in nature – it is a struggle for a

fairer slice of the pie.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

"The decision to move forward

with an impeachment inquiry is not one we took lightly."

====

The bill is an amended version of the

Senate’s S. 178 to support the Uighurs, a Muslim ethnic group in western China,

and it passed Tuesday, on a vote of 407 to 1

The bill is an amended version of the Senate’s S.

178 to support the Uighurs, a Muslim ethnic group in western China, and it

passed Tuesday, on a vote of 407 to 1. Chinese

state media warned before the vote that the government could release a list of

“unreliable entities” that could lead to sanctions against U.S. companies. The

measure follows legislation supporting Hong Kong protesters signed into law

last week by President Donald Trump.

Based on what I know, since US

Congress plans to pass Xinjiang-related bill, China is

considering to impose visa restrictions on US officials and lawmakers who've

had odious performance on Xinjiang issue;it might also ban all US diplomatic

passport holders from entering Xinjiang.

China wants real human rights

in Xinjiang: people’s rights to have a peaceful life. West’s

hypocrisy won’t affect Xinjiang internally, nor will it influence Muslim

countries’ attitude. It’s just a few media outlets and politicians

pretending to be representing the world.Pathetic.

IF

Beijing will finally publish its black list, which it has been

threatening to do since May and which may include such names as Apple and Micron… well, now that the House has

passed the Uighur bill, Beijing may no longer be able

to delay, ... Needless to say, for a president for life such as Xi Jinping, that is hardly an option, so

stay tuned for China's response which may be due any moment.

….

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

Threats & nuke-blackmail again.. Potus put at

risk or save NATO? This depends on Pol

"I hope he lives up to the agreement, but we're going to

find out."

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

-Save

your insidious comment & tell us when you are going to quit from the race…

Trump

Campaign Congratulates Gabbard Over Harris’s Exit From 2020 Race IF you win is

because buying election (corp finance). IF win: you’ve no chances of

‘gobernability’

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELLION

Am-Lat: Se acortan los ciclos, se agudiza la crisis Colect Nuestra América

====

ALAI NET ORG

====

RT EN ESPAÑOL

-Países del

TIAR aprueban restricción de tránsito contra funcionarios venezolanos https://actualidad.rt.com/actualidad/335711-paises-tiar-aprueban-restriccion-transito

- ¿Quién es quién en el escándalo de corrupción

de la oposición en la Asamblea Nacional de Venezuela? https://actualidad.rt.com/actualidad/335514-escandalo-corrupcion-diputados-opositores-venezuela

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political

crisis: neofascism & internal conflicts that favor WW3

-Impeachm Rep Alleges Trump Solicited Foreign

Election Interfer By Adam

Schiff,

-

Iraq rise up against 16 years of 'made in the

USA' corruption By N J S

Davies

-

Could The U.S. Survive a Truth Commission? By Charles Hugh Smith

-

Hong Kong Unmasked Watch

-

Violence and the State By Craig Murray

----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

-R

Lachmann Can

the US Get Out of Its Endless Wars?

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

----

PRESS

TV

Middle East n world news

- US House report accuses Trump of power abuse

- 'US invasion has left Iraq devastated'

- Gaza switches on its Christmas lights

- NATO summit: Trump condemned by British protesters

- ‘Iran, Russia, China to hold joint naval drills on Dec. 27’

- No to racism, no to Trump: Protesters at NATO summit

- Bipartisan support for US military aid to Israel

- Trump’s bald-faced Big Lies on Iran continue

- PROGRAMS

- ISR: Tuition crisis

- Israeli land grab

- US Hong Kong interference

- EU INSTEX moves

----

===

No hay comentarios:

Publicar un comentario