ND MAR 31 19 SIT EC y POL

ND denounce

Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

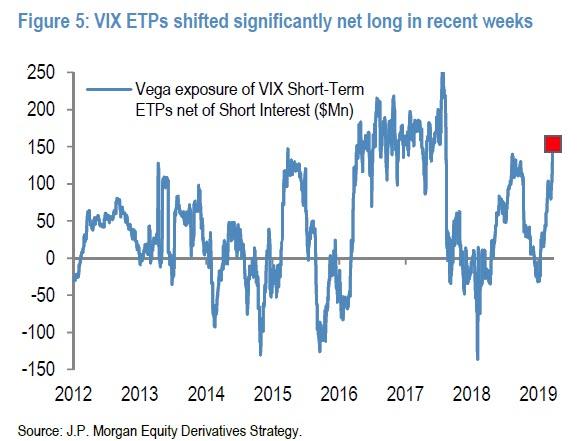

The long VIX trade in various ETPs is getting

dangerously crowded...

According to

JPMorgan's Bram Kaplan, after a years of relatively quiet, the net exposure

among VIX ETPs has recently spiked to their largest net long position in 1.5

years, tilted long by ~$150Mn vega, which is just shy of the record vega

exposure hit in early 2018 and which precipitated the VIX ETP implosion. However,

unlike 2018, this time

the trade is in the other direction as

investors piled into long and levered VIX ETPs beginning in February, as soon

as the VIX index fell below 16, to as JPM suggests. "position

for/speculate on the next volatility spike."

See Chart:

{kind=link}

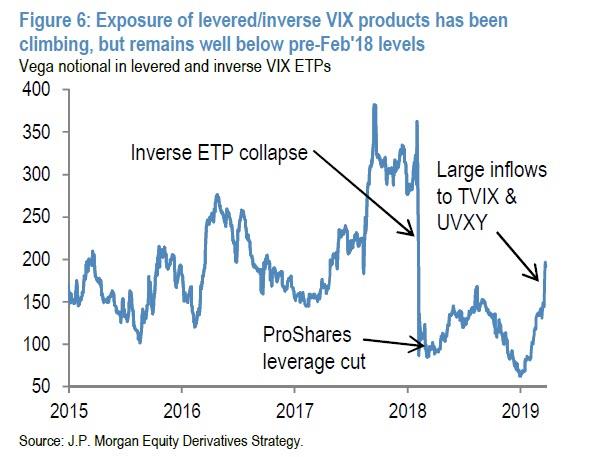

Specifically,

over this period, investors have deposited $600MM net into unlevered long VIX

ETPs, and $1.1Bn into levered products (the majority of which went into 2x

levered TVIX). Following these flows, the vega notional

in levered and inverse VIX ETPs has increased significantly, but remains well

below pre-Feb’18 levels.

See Chart:

Inverse ETP collapse

{kind=link}

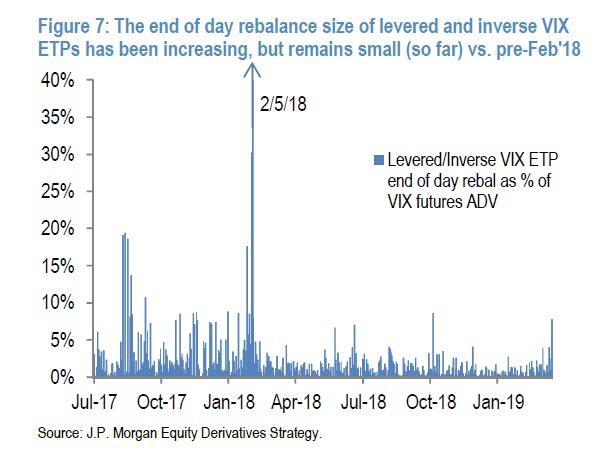

And here is

the cautious conclusion from JPM, which notes that while the bank doesn't - yet

- expect these ETPs to drive end-of-day short gamma rebalancing effects

anywhere close to those experienced on 2/5/18, "their end of day rebalances

are becoming material." To wit, the next chart illustrates how the end of

day rebalance requirements for levered and inverse VIX ETPs has been increasing

as a percentage VIX futures volumes, but remains small (so far, at least)

compared to pre-Feb’18.

The key thing is that as noted above, unlike last year's vol

selling stampede, the current build-up of long vega exposure in VIX ETPs

suggests they could provide a headwind to the next volatility spike...

See Chart:

{kind=link}

... as investors are likely to take profits on these positions

and/or invest in inverse products to monetize the spike. On the other hand,

should the EOD rebalance persist, growing increasingly skewed in one direction

as contrarian traders boost their bets on a VIX spike in the coming months

using various ETP products, then it is only a matter of time before another

major VIX spike takes place, only this time instead of wiping out the vol

buyers, it results in a very generous pay day.

….

SOURCE:

----

----

"As one client

quipped this week, it really depends from which direction the jaws close –

through higher rates or via lower equity prices."

There have

been two conflicting themes in the market so far in 2019: the first one has

been the relentless selling by equity investors since the start of the new year

despite the market's remarkable surge in 2019, offset by buying of fixed income

securities in a scramble to lock up yield ahead of potential rate cuts and/or

QE by the Fed later in 2019 or in 2020 (most recently

discussed here).

See Chart:

Dovish Central Banks are pushing more money into fixed income

v. equitites

{kind=link}

The second

theme, which is closely tied to the first, has

been the market's so-called "jaws", where stocks have

moved sharply higher while yields have tumbled to multi-year lows, sparking

investor confusion: is the bond market right in

anticipating a period of acute deflation and/or recession, or is it wrong and

stocks, which are less than 5% below their all-time highs, correct in their

optimistic outlook.

See Chart:

S&P500 10 Year Yield

{kind=link}

As Goldman's

David Kostin writes, it is this decoupling that is dominating client

discussions:

Ten-year US Treasury yields have plunged to 2.4%. From an investor

perspective, stable equity prices coupled with falling interest rates means a

wider earnings yield gap and implies a more attractive relative value for

stocks assuming the economy does not fall into recession.

As Kostin

recounts, one client told the chief Goldman equity strategist, that it all really "depends

from which direction the jaws close – through higher rates or via lower equity

prices."

That's the

question that the bank tries to answer in its latest US Weekly Kickstart

report.

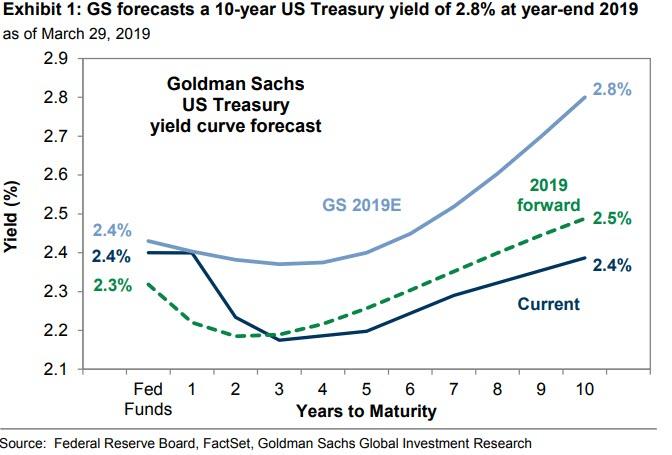

For its part, Goldman remains as usual cautiously

optimistic: The bank which last December incorrectly predicted no

less than 4 rate hikes in 2019, now forecasts the

10-year US Treasury yield will rise to 2.8% at year-end 2019 (down from the

previous forecast of 3.0%).

See Chart:

Golman Sachs US Treasury yield curve forecast 2.8% at year

end 2019

{kind=link}

Next up is the

deteriorating corporate earnings picture, with Q1 looking especially grim with

the risk of a mini earnings recession on the horizon. To be sure, starting with

Apple in early January, management teams have been tempering earnings

expectations. In fact, more than 140 firms have reduced 2019 EPS guidance since the start of the

year and 67 firms have cut guidance by more than 2%. As Goldman

notes, earnings revisions have been more negative than usual. During the

past three months, analysts have cut expectations for full-year 2019 S&P

500 EPS by 4%, nearly four times the usual rate of roughly 1% per quarter. On

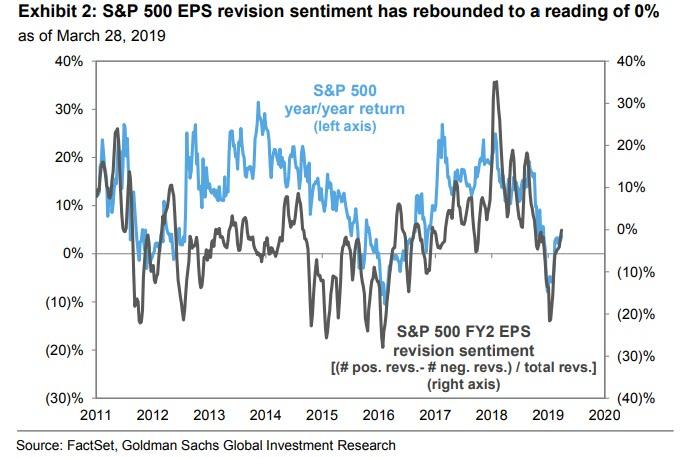

the other hand, 1-month revision sentiment has rebounded to a reading of 0%.

See Chart:

S&P500 EPS revision sentiment has rebounded to 0% as of

March 28, 2019

{kind=link}

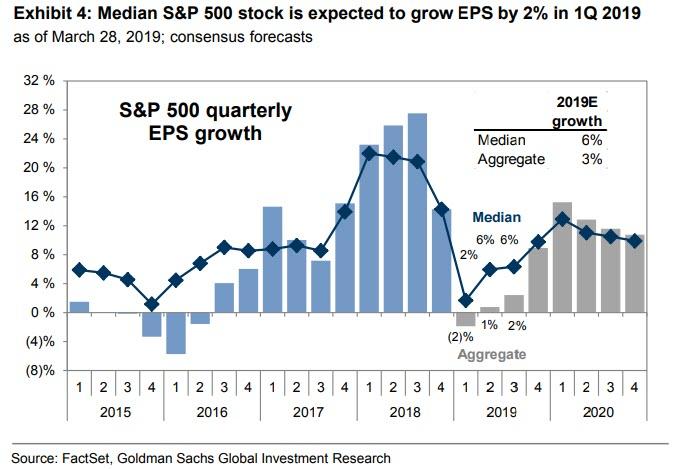

And while sell

ide earnings sentiment may have finally troughed,

consensus now expects aggregate S&P 500 EPS to fall by 2% in 1Q, which would be the first year/year decline

since 2Q 2016 even as consensus still expects strong 5% sales growth. One thing to note: while the

average print will be negative, the median S&P 500 stock is expected to

grow EPS by 2%, indicating that a few outsized firms (AAPL, MU, WDC, CVX, XOM,

NVDA) are weighing on the aggregate measure according to Goldman. This dichotomy is also present for full-year 2019 EPS growth,

with the median firm projected to grow EPS by 6% while the aggregate index

grows by just 3%.

See Chart:

Median

S&P500 stock is expected to grow EPS

by 2% in 1Q 2019

{kind=link}

Conslusion: JPM strategist concludes that "there appears

to be a disconnect between rate and risky markets at the moment with rate MARKETS SIGNALING MORE ELEVATED GROWTH AND

RECESSIONS RISKS, and equity, credit and commodity

markets pricing in more optimistic scenarios."

….

----

----

"But if

investors believe America is succumbing to the secular stagnation that has

gripped Japan and Europe, and if they’re growing scared that global central

banks are no longer capable of rescuing markets, then we have a real

problem."

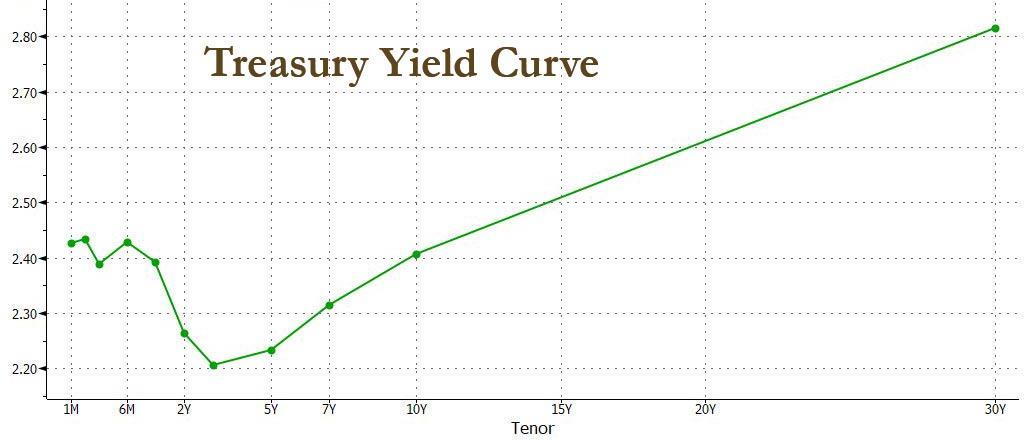

Three Worlds

“America’s yield curve inversion can mean one

of three things,” said the CIO. “We’re either

living in a world of secular stagnation and investors worry that central banks

no longer have sufficient policy tools to spur growth and inflation,” he

continued. “Or the economy is simply sliding toward

recession and the inversion will persist until the Fed panics and spurs a

recovery,” he said. “Or we’re living in a world,

where the market is moving in ways that defy historical norms because of global

QE. And if that’s the case, the curve is sending a false signal.”

See Chart:

Treasury Yield Curve

{kind=link}

“If we’re sliding toward recession, then it seems odd

that credit markets are holding up so well,” continued the same CIO. “So keep

an eye on those,” he said. “And

if the curve is sending a false signal due to German and Japanese government bonds yielding less than zero out

to 10yrs, then the recent Fed pivot and these low bond

rates in America may very well spur a blow-off rally in stocks like in 1999.”

A dovish Fed in 1998 (post-LTCM) and 1999 (pre-Y2K) provided the liquidity

without which that parabolic rally could have never happened.

See Chart:

S&P%500 10 Year

Yield

{kind=link}

“But if investors believe America

is succumbing to the secular stagnation that has gripped Japan and Europe, and

if they’re growing scared that global central banks are no longer capable of

rescuing markets, then we have a real problem,” said

the CIO. “Because a recession is bad for markets, but not catastrophic provided

that central banks can step in to spur recovery. But with global rates already so low, if investors lose faith in the

ability of central banks to do what they have always done, THEN WE’RE VULNERABLE TO A STOCK MARKET CRASH.”

….

----

----

Liquidity and central banks rule, nothing else matters... Yet, bulls have not proven their case.

The first

quarter of 2019 was a smash hit for bulls. Capitulating central banks, record buybacks flushing

the system with artificial liquidity, constant jawboning by dovish central

bankers and permanent promises of progress on a China trade deal, and a

collapsing yield picture bringing back TINA (there is no

alternative) all of which produced a relentless 3 month move higher back in

equities that rendered any fundamental issues of slowing growth, earnings and

even a yield curve inversion irrelevant and erased the losses of a disastrous

Q4 of 2018.

Liquidity and central banks rule,

nothing else matters. Optimism

is back and hope is pervasive that 2019 will replay the earnings recession case

of 2016 meaning that all bad news is priced in, any slowdown will be temporary

and markets will resume their 10 year bull trend with new highs to come.

Yet, bulls have not proven their

case. So far lower

highs on all key indices risking major potential topping patterns and hence the

upcoming earnings season may serve as a key pivot for markets in the weeks

ahead. Dovish central banks have been fully priced in

by markets and the liquidity of buybacks will at least temporarily disappear

during the buyback blackout window.

Bears have managed to keep price

below the January 2018 highs as well as the long term 2009 trend line, but are

also running out of time as a confirmed break above the January

2018 highs could set markets on a path to at least retest the highs or make new

highs.

Hence the time period in April into May sets

up for decision time for markets.

Risk to markets: The rally off of the December lows remains

untested and uncorrected with plenty of open gaps below while indices have

formed specific patterns that could be interpreted as bearish. Indeed the rally

has been so steep that it will require ever higher prices to avoid a confirmed

break of these patterns. Due to the vertical nature of this rally these

patterns are at risk of breaking to the downside if markets were to experience

just a few days of downside. As these patterns are very large sizable downside

and an increase in volatility could emerge on a confirmed break of these

patterns.

Timing matters as structurally

bulls have not been able to confirm a resumption of the larger bull trend hence

April may be a key month and bulls can hardly afford a down month.

I’m discussing

technicals and select key charts in the video below:

See VIDEO:

….

----

----

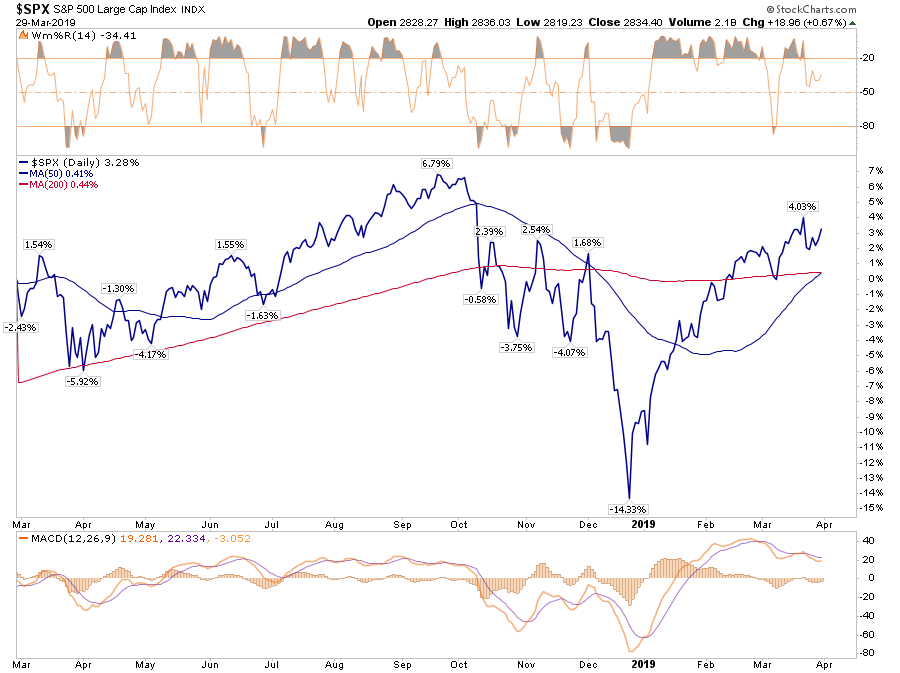

This time is unlikely to be different.

A Run For The Highs

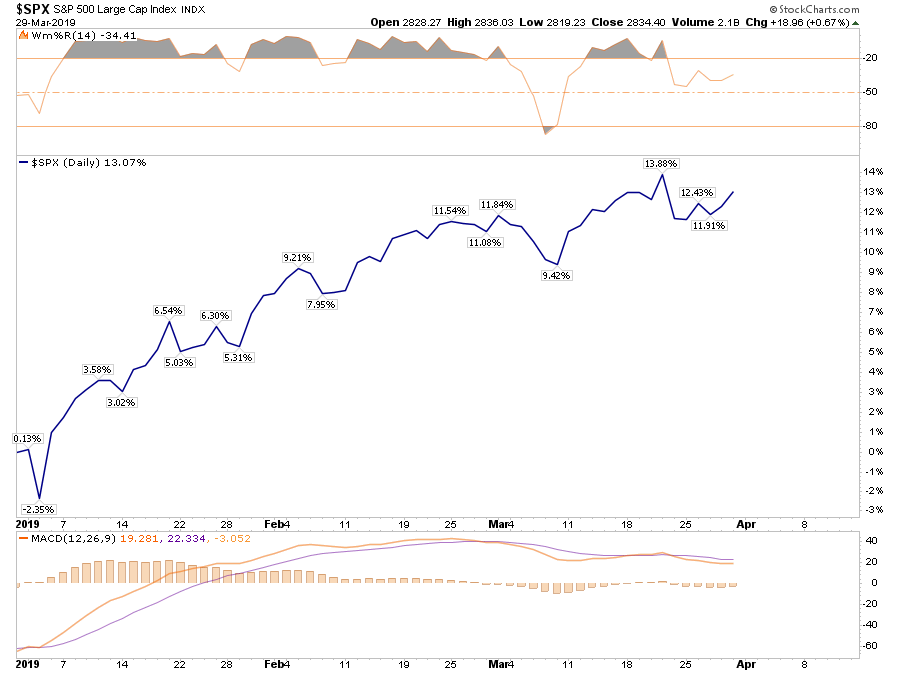

Friday wrapped up the first quarter of 2019, and it was the best quarterly performance since 2009. As shown in

the chart below, if you bought the

bottom, you are “killing it.”

See Chart:

{kind=link}

However, you didn’t.

Despite all of

the media “hoopla” about the rally, the

reality is that for most, they are simply getting back to even over the last

year.

See Chart:

{kind=link}

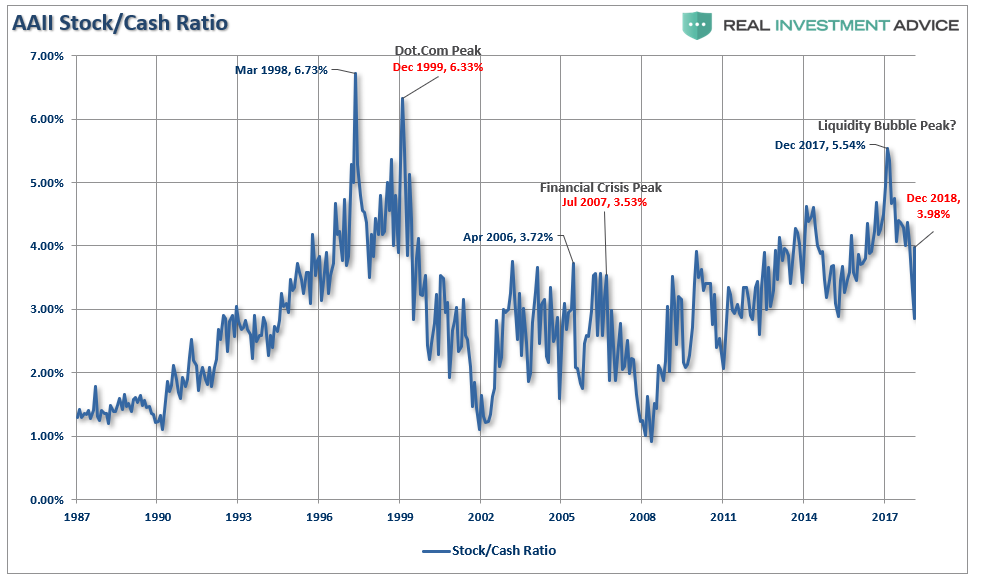

That is, assuming you didn’t “sell

the bottom” in December, which by looking at allocation changes,

certainly appears to be the case for many.

See Chart:

{kind=link}

If we deconstruct the ratio we can see the rotation a bit

better

See Chart:

{kind=link}

Not

surprisingly, historically speaking, investors had their peak stock exposure

before the market cycle peak. As the market had its first stumble, investors sold. When the

market bounces, investors are initially reluctant to chase it. However, as the

rally continues, the “fear of missing out or F.O.M.O” eventually forces

them back into the market. This is how bear market rallies work;

they inflict the most pain possible on investors both on the bounce and then on

the way back down.

However, for

the moment, we are still in the midst of a bear market rally. This will be the

case until the market breaks out to new highs. Only then can we confirm the

previous consolidation is complete and the bull market has been

re-established.

The good news is on a very

short-term basis, the market IS INDEED bullishly biased and coming off an

extremely strong first quarter rally. The

current momentum of the market is strong as bullish optimism has regained a

foothold.

But, as we

noted for our RIA PRO Subscribers last week, (Free 30-Day Trial with Code: PRO30) complacency

has moved back to extremes which suggests that a further rally isn’t “risk

free.”

“The graph below is constructed by normalizing VIX (equity volatility),

MOVE (bond volatility) and CVIX (US dollar volatility) and then aggregating the

results into an equal-weighted index. The y-axis denotes the percentage of time

that the same or lower levels of aggregated volatility occurred since 2010. For

instance, the current level is 1.91%, meaning that only 1.91% of readings registered at a lower level.

See Chart:

Multi-Asset Volatility Index

{kind=link}

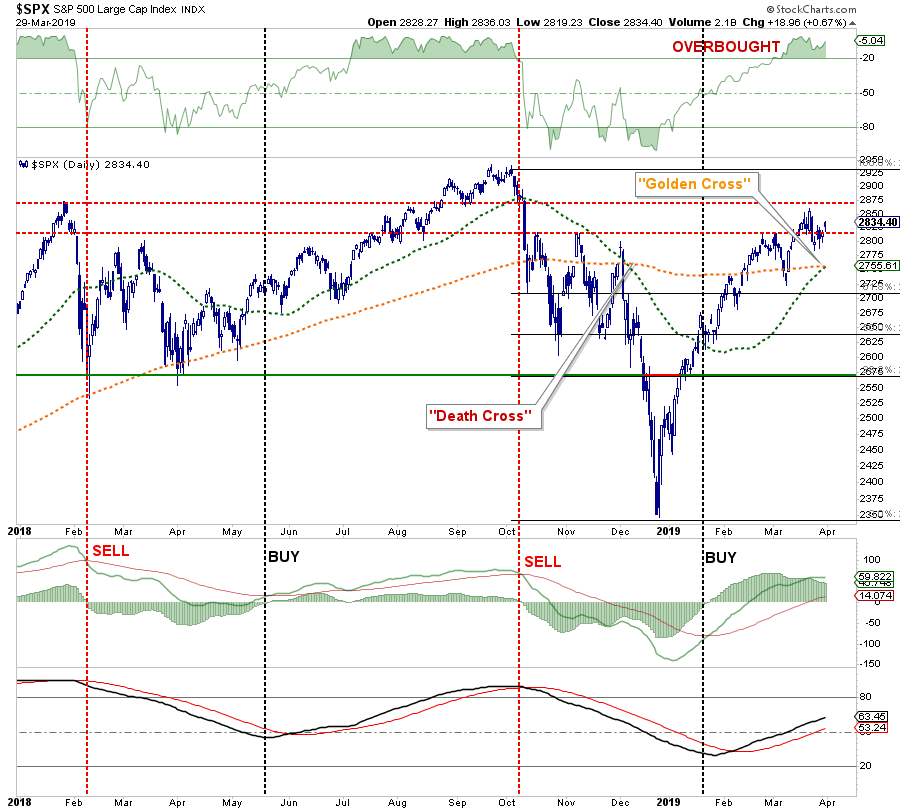

Nonetheless,

the markets are close to registering a “golden cross.” This is

some of that technical “voodoo” where the 50-day moving

average (dma) crosses above the longer-term 200-dma. This “cross” provides substantial support

for stocks at that level and limits downside risk to some degree in the

short-term.

See Chart:

{kind=link}

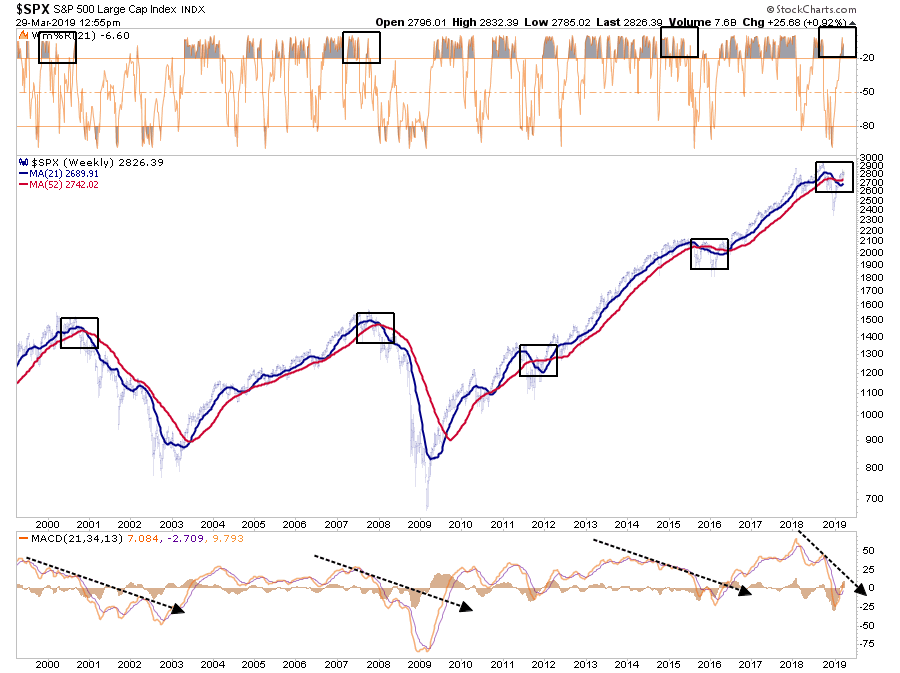

The next chart shows the longer-term version

of the chart above using WEEKLY data. The parameters are set for a

slightly longer time frame to reduce the number of “false” indications. I have accentuated the moving averages to have them more

clearly show the crosses.

See Chart:

{kind=link}

From a portfolio management standpoint, what

should you do?

In the short-term the market

remains bullishly biased and suggests, with a couple of months to go in the

“seasonally strong” period of the year, that downside risk is somewhat limited.

“Ignore the yield curve they said. It’ll be

fun they said.”

Last

week, Mark

Kolanovic of J.P. Morgan stated:

“Historically, equity markets tended to produce some of the strongest

returns in the months and quarters following an inversion. Only after [around]

30 months does the S&P 500 return drop below average,”

See Chart:

S&P500 after

inversion:

https://www.zerohedge.com/s3/files/inline-images/MW-HG413_JPMinv_20190326135102_NS.png?itok=wfrddGhL

{kind=link}

Conclusion

Pay attention

to these longer-term trend changes as historically they signify bigger issues

with the market.

It is unlikely

this time is different. There are too many indicators already suggesting higher

rates are impacting interest rate sensitive, and economically important, areas

of the economy. The only issue is

when investors recognize the obvious and sell in the anticipation of a market

decline.

The yield

curve is clearly sending a message which shouldn’t be ignored and it is a good

bet that “risk-based”investors will likely act sooner rather than

later. Of course, it is simply the contraction in liquidity that causes the

decline which will eventually exacerbates the economic contraction. Importantly, since recessions are

only identified in hindsight when current data is negatively revised in the

future, it won’t become “obvious” the yield curve was sending

the correct message until far too late to be useful.

While it is unwise to use the “yield curve” as

a “market timing” tool, it is just as unwise to completely

dismiss the message it is currently sending.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

... for “roughly three

minutes a night, every night, for an astonishing 791 days,” the

media has been poking this mystical Russian bear which has turned into – in the

president’s words – a Collusion

Delusion.

====

Why is it that no one defends free markets, and socialism, despite all the evidence of its failures, comes back

again and again? Unsurprisingly, the answer lies in politics...

Why is

it that no one defends free markets, and socialism, despite all the evidence of

its failures, comes back again and again? Unsurprisingly, the answer lies in

politics, which have always led to a boom-bust cycle of collective

behaviour. Furthering our understanding of this phenomenon is timely because

the old advanced economies, burdened by a combination of existing and future

debt, appear to be on the verge of an unhappily coordinated bust. But that does not automatically return us to the free markets

some of us long for.

Check these

subtitles:

CYCLES OF COLLECTIVE BEHAVIOR

To understand

why free markets are more often than not unpopular, we must put them into a

context of human behaviour. In this regard we can stylise a cycle of collective behaviour into three

characteristic phases.

- The first is a lawless condition of no secure ownership of property rights; in the absence of enforceable law the means of possession are necessarily violent and uncertain. It is the natural condition of tribalism and pre-civilisation societies. It is the condition to which humanity returns when the cycle completes.

- The second phase is the consolidation of property ownership, with enforceable laws to define and protect it. Out of the chaos that fails to advance the condition of the people comes order, and with it the aggregation of the means of production. Capital in all the forms necessary for production accumulates, and being scarce, is used most efficiently. The backbone of this phase is freedom for the individual to dispose of his or her resources at will. The pace of improvement in the human condition is governed by the level of accumulated wealth and technological innovation.

- The third phase is the abandonment of free markets in favour of state control. The state, whose primary function in economic terms is to act as provider and facilitator of the law, increasingly supresses commerce by extracting escalating levels of tax. Taxes are imposed to redistribute wealth from those that earned and conserved it to those that did not. The state takes control of money, issuing its own currency which it can print at will. The damages to the economy are covered up by all the artifices available to the state.

The state regulates. The state confiscates. The state deprives its people of their freedom. The

state’s demands become so insatiable, so counterproductive, so impoverishing

that the economy collapses back into the first phase of the next cycle.

EMPIRICAL EVIDENCE OF THE CYCLE.

The assembly of German states into a unified

nation in 1871 gave credence to a new socialising phenomenon, whereby Bismarck,

Germany’s first Chancellor, promoted the state as a socialising entity,

superseding free markets. He was the first politician to create a

welfare state, introducing accident and old-age insurance and socialised

medicine. Shortly after unification, in the mid-1870s Bismarck abandoned free

trade and introduced trade protectionism.

More

subtitles:

THE PSYCHOLOGY OF DENYING FREE

MARKETS

CONTEMPORARY SOCIALIST EVOLUTIONS

Conclusion?

Witness the

struggle with Brexit, where it turns out the Westminster Parliament is

comprised of an overwhelming majority of members who are committed to the EU’s

socialising masterplan to the exclusion of democracy. Even a majority of Tory

MPs, the party of free enterprise, prefers a federal socialist system to free

markets.

It is

the stuff of late-stage socialism. The

whole world is in its grip, rather than just Germany, just the USSR, just

America, just the EU, or just Britain. And these are only some among the

traditionally advanced nations. Being cyclical, the bankruptcy of it all in

time is for sure. It is set to throw up greater challenges than ever seen

before because of its ubiquity. Assuming it does not end in a nuclear

destruction of the human race, we will eventually turn our backs on the follies

of socialising governments and go back to free markets. Then the cycle of humanity’s socialising madness will start all

over again.

…

[[ Certainly this

author needs to know What is what is not socialism. I’be back on this ]]

The same with the coming article:

RELATED:

When the economy collapses, everybody will blame capitalism, because Trump is somehow, incorrectly, associated with

capitalism... the young and poor will look to the government to 'do

something'... andsocialism as a kind

and gentle answer.

----

----

"The political correctness people are the most alienated and emotionally weak element

in the society. Yet they dominate in the media, entertainment, universities, and art

world..."

====

"...If you don’t treat me right, my people will get you..."

====

US-WORLD ISSUES (Geo

Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

And Europe is starting to take notice, and follow

suit...

====

Several Russian banks have joined the China International Payments

System (CIPS) also known as

China's "SWIFT", to ease operations between the two countries

====

"Russia is not

changing the balance of power in the region, Russia is not threatening anyone."

====

SPUTNIK and RT SHOWS

GEO-POL n

GEO-ECO ..Focus on neoliberal expansion

via wars & danger of WW3

====

SHOWS RT

----

----

NOTICIAS IN SPANISH

Lat Am search

f alternatives to neo-fascist regimes & terrorist imperial chaos

VIENTO SUR

FEM Cambiarlo todo. Bases y

desafíos de la Huelga Fem Julia

Cámara

====

RT EN ESPAÑOL

- Maduro: "El sist eléctr nacional de Ven fue penet por virus desde USA"

- Bolsonaro apertura oficina de negoc en Jerusalén, no de la Embajada

- Papa: "Estamos en una tercera guerra mundial a pedacitos"

- Netanyahu: Israel está listo para una "campaña extensa" en Gaza

- Gob VEN suminist agua a nivel nacion mientras contrarrest cortes eléctric

- Zelenski y Poroshenko seenfrentarian en 2da vuelta de presid ucranianas

- Perros portarian nuevo virus potencialmente mortal para los humanos

- Líder comunero pide diálogo con el Gob peruano sobre mina Las Bambas

- comunidad internacional critica la decisión de Trump sobre Altos del Golán

- Especial Black lives: Agentes del cambio (Episodio 5)

----

----

GLOBAL RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

----

----

PRESS TV

Resume of

Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario