ND MAR 20 19 SIT

EC y POL

ND denounce

Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

Are

you not entertained: Enjoy this US ECON SITUATION TODAY

We don’t need

WW3 to take Trump out.. We need a Nation

in streets demand resigna IF Trump doesn’t

resign & use Fascist violence: REV is the

solution. No more fake Dem Que se vayan todos! The financial parasites in Wall St must be

jailed & confiscated.

Why he

should leave: Autorit-fascism, Inefic & lies, War crimes & crimes agst

humanity

This is

what it looks like when doves cry...Watch later https://youtu.be/UG3VcCAlUgE

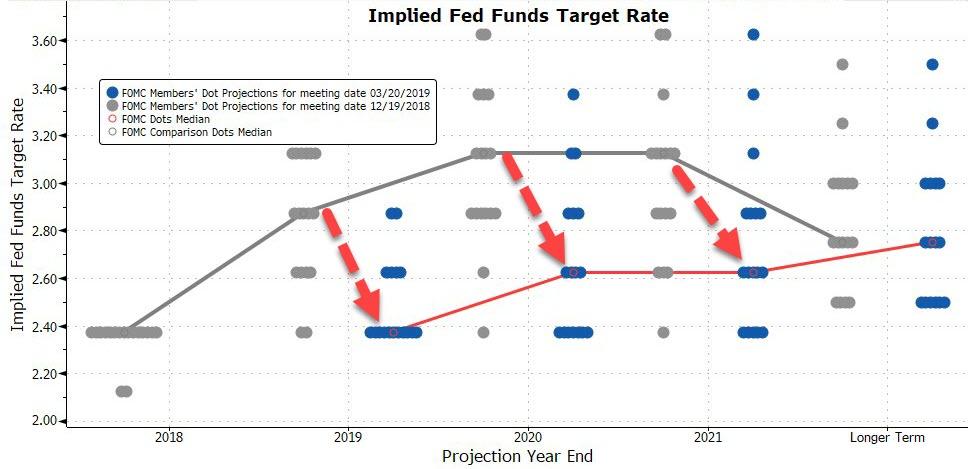

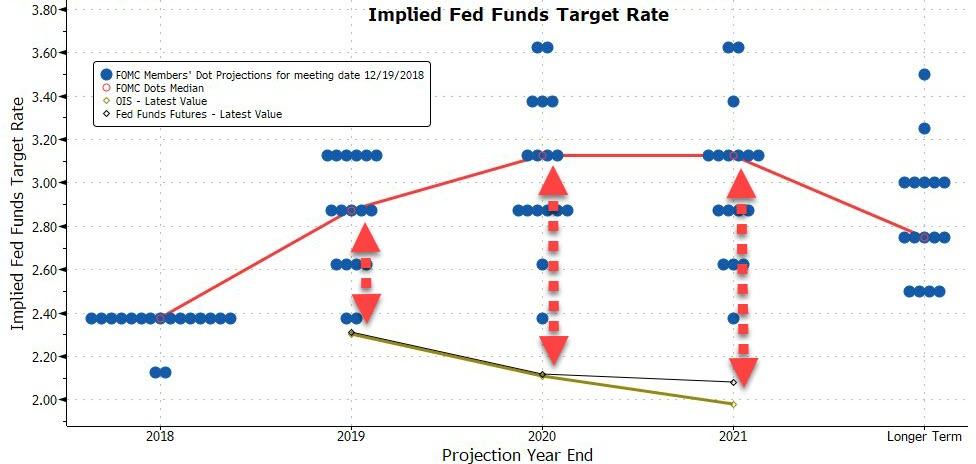

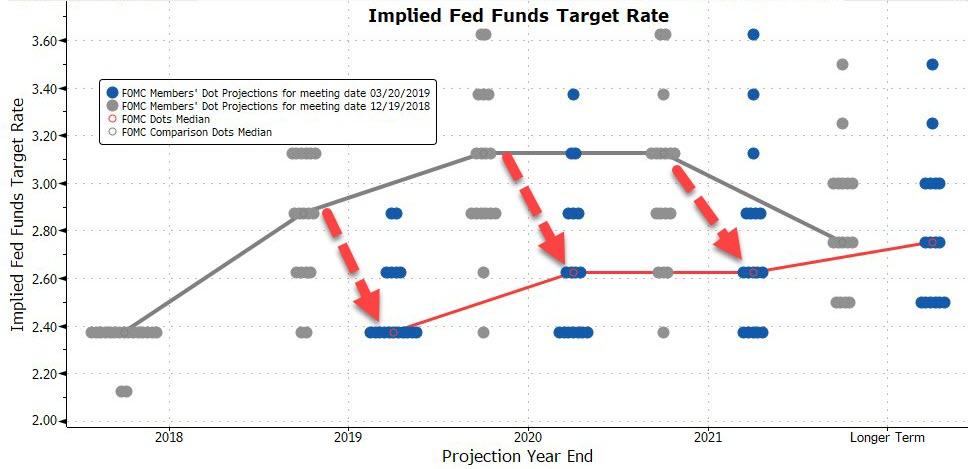

The

Fed folded entirely to the market today, slashing its rate trajectory

dramatically lower nearer the market's implied dovishness...

See Chart:

Implied

Fed Funds Target Rate

{kind=link}

Bloomberg's

Ye Xie noted that if we take the dot plot at face value (which, mind you, may

not be a wise thing to do), then it seems the Fed will hold rates steady this

year before raising one more time in 2020. If that pans out, it would be

unprecedented. Since the 1970s, there have been three times

when the Fed held rates steady for more than a year after raising them in the

previous three months: 2006, 2000 and 1997. Invariably, the next move was a rate cut.

However, the market has shifted even more dovish, pricing in almost an

entire rate-cut in 2019 now...

See Chart:

{kind=link}

Stocks

initially surged on the dovish surprise, dragging the Dow green, but as the last

hour went on, traders wondered just how much fear The Fed must be feeling about

growth to take such a machete to its rate forecasts and started to sell stocks...

See Chart:

{kind=link}

Only

Nasdaq managed to cling to gains on the day...

See Chart:

{kind=link}

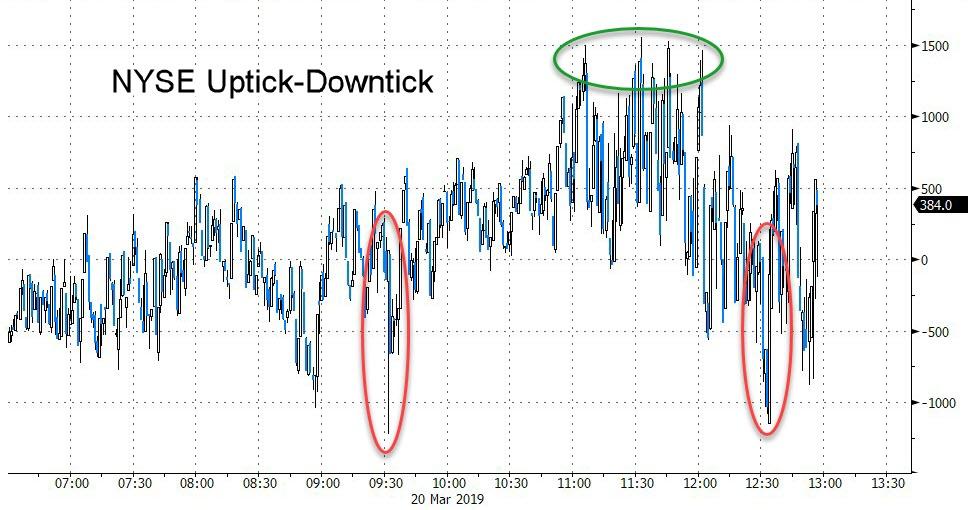

TICK gives

us a sense of the flow as programs charged in long as The Fed statement hit but

sellers dominated the last hour... (NOTE the drop

earlier in the day when Trump commented on China tariffs)

See Chart:

{kind=link}

Regional

Banks were battered...

{kind=link}

S&P

Buyback-related stocks pumped-and-dumped after The Fed...

{kind=link}

The

Dollar Index crashed to its lowest since early Feb - perfectly back to the Jan

FOMC meeting levels...

See Chart:

{kind=link}

And

finally, one wonders at the irony of a massively dovish Fed's action driving

the yield curve to collapse sparking the highest recession risk of the cycle...

See Chart:

{kind=link}

----

----

Despite doubling down on

dovish, things today did not pan out quite as Powell had expected...

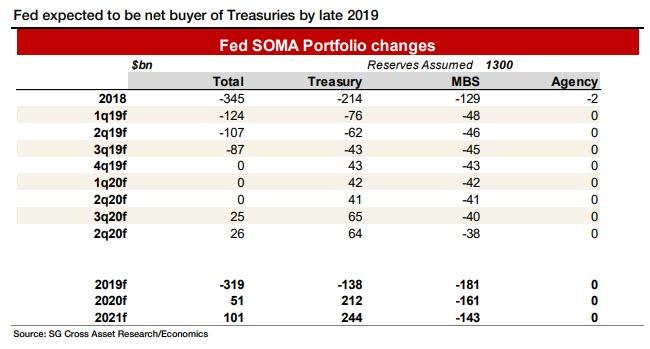

Looking

ahead, while the overall Fed portfolio will be flat after September, the Fed should be buying roughly $45bn per

quarter to offset the liquidation of MBS. Annualized,

the Fed should be a net buyer of about $180bn per year of Treasury securities.

If the Treasury is financing $1.0tn deficits annually,

purchases by the Fed become a meaningful source of funding, which according to

Socgen "will enhance its ability to offer fiscal

stimulus when or if a slowdown takes place."

See Chart:

FED

expected to be net buyer of Treasuries by late 2019

{kind=link}

Does the Fed know something Others don't?

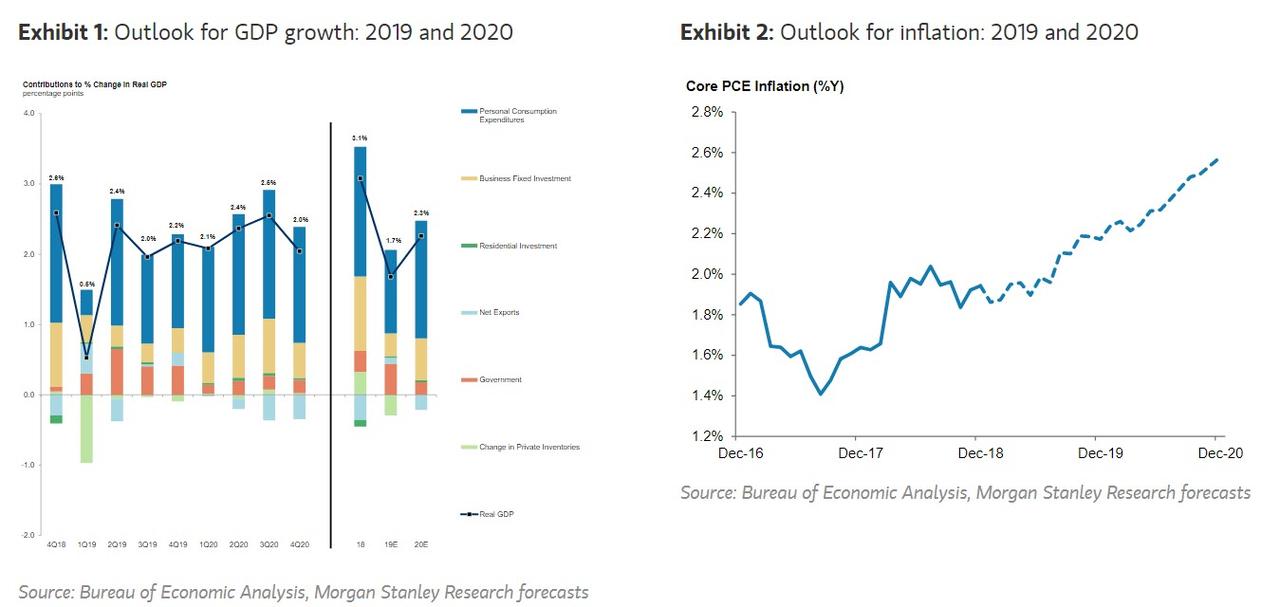

The policy

prescription is therefore for the Fed to hold policy and be "patient"

for inflation to move up. This also means that the only gating factor for a

reversal to a more hawkish Fed will be a jump in inflation, something Morgan

Stanley expects

will take place in late 2019 and early 2020, at

which point the Fed will resume hiking an additional three times in 2020.

See Chart:

Exhibit

1: Outlook of GDP Growth

Exhibit

2: Outlook for Inflation: 2019 and 2020

{kind=link}

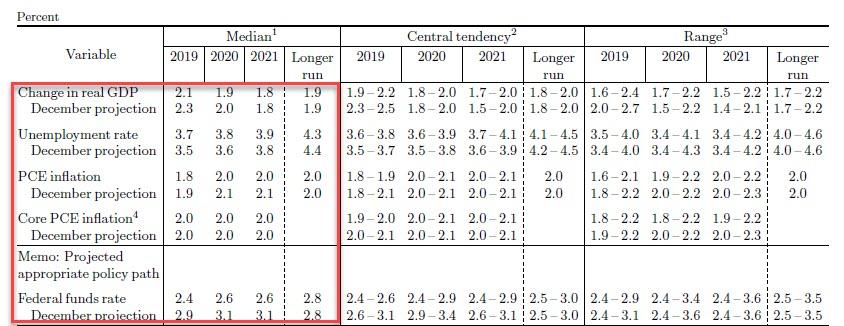

The Fed

also tweaked its projection forecasts, looking for weaker growth this year and

next and a slightly higher unemployment rate. The forecast for inflation did

not change as the Fed looks for core PCE to hold at 2.0% through the forecast

horizon. This shows that

the Fed believes that the Phillips Curve is flat, penciling in no inflation

response despite the unemployment rate persistently sub-NAIRU and easy monetary

policy.

See Chart:

{kind=link}

As Powell

said, the key tools for managing financial stability

are "regulatory" rather than rates. How regulation will bail

out the financial system once this current bubble pops, remains unclear.

Market implications

Since this

was an unexpectedly dovish statement, the reaction was abrupt and violent: the

rates market viewed Fed communications, especially through the SEP fed funds

projections, as signaling a very dovish stance by the FOMC. This was manifest

in the rates market rallying sharply following the release of the SEP led by

the front end given the expectation the Fed will not hike rates any time in the

near future. In fact, the yield curve is now

inverted between the effective Fed Funds rate

(2.40%) all the way to the 5 Year.

See Chart:

Effective

FED Funds Rate

{kind=link}

What is

surprising, is that despite the Fed's express desire to increase future growth

and potentially allow the economy/inflation to run hot, the 10Y yield also

tumbled, as the bond

market is now growing concerned the Fed committed another policy error, with a

curve inversion once again imminent.

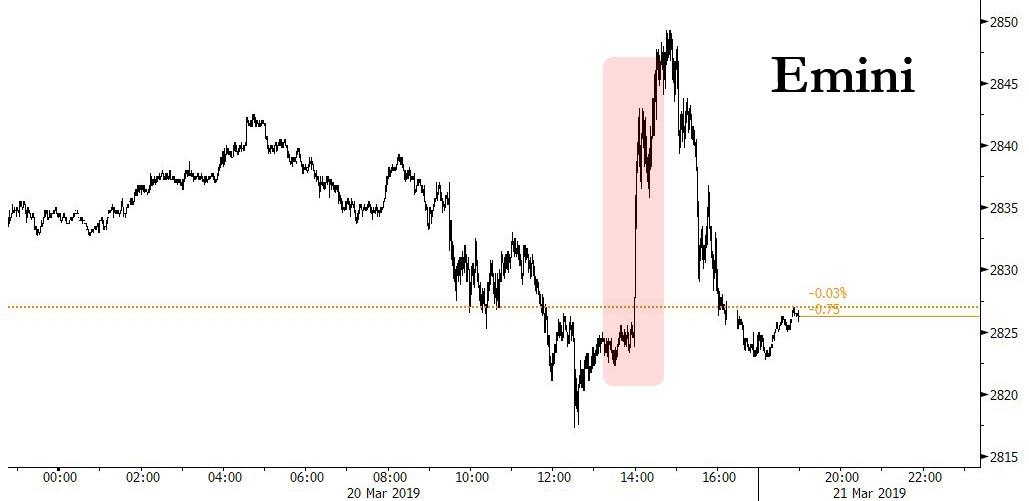

Finally,

and perhaps related to this, was the surprise reaction in stocks: after

initially spiking higher, as risks always does when the Fed surprises dovishly,

the market then sold off, and while the drop wasn't substantial, the fact that

the day's biggest sell program hit at precisely 3:30pm and pulled stocks

sharply lower, indicates that at least one player decided that - for one reason

or another - the top was in. Whether that has to do with the recurrent concern

of "what does the Fed know about the economy if it is doubling down on

dovish", and is signaling

an imminent recession, or because of growing conviction that the Fed is now powerless and has committed a policy error

will be revealed in due time.

See Chart:

Emini

{kind=link}

However,

the most disturbing feature of today's late-day selloff, is that after the aggressive seller emerged, not only major investor

had the conviction to reverse the late-day drop in what appears to have been a

major hit to the "dovish Fed is bullish" narrative.

If today's

late day swing lower is not reversed tomorrow now that traders have had time to

digest the FOMC decision, it will be a concerning indication that all the market upside that can be extracted from monetary

policy has now been priced in, and would suggest that another retest of the

December lows would be required to force Powell to commence rate cuts or even

launch QE4.

….

----

----

Huge dovish surprise as Fed

folds - seesno rate-hikes in 2019,

one rate-hike in 2020, and will end

balance sheet normalization in September.

Summary:

- Fed leaves rates unchanged, says economic growth has slowed form Q4, even as labor market still strong, job gains solid

- As expected, the Fed will taper its balance-sheet rolloff, sees it ending by the of September

- Fed signals no rate hike this year with one increase in 2020

- 11 officials for zero 2019 hikes, four for one hike

- Fed says median funds rate 2.4% in 2019, 2.6% in 2020-2021

- But, the median estimate for the neutral funds rate remains unchanged at 2.8%

The Fed has some 'splaining to do. The market is pricing in 16bps of rate-cuts in 2019 while

they are forecasting - at last call - 2 rate-hikes...

See Chart:

Implied

Fed Funds Target rate

{kind=link}

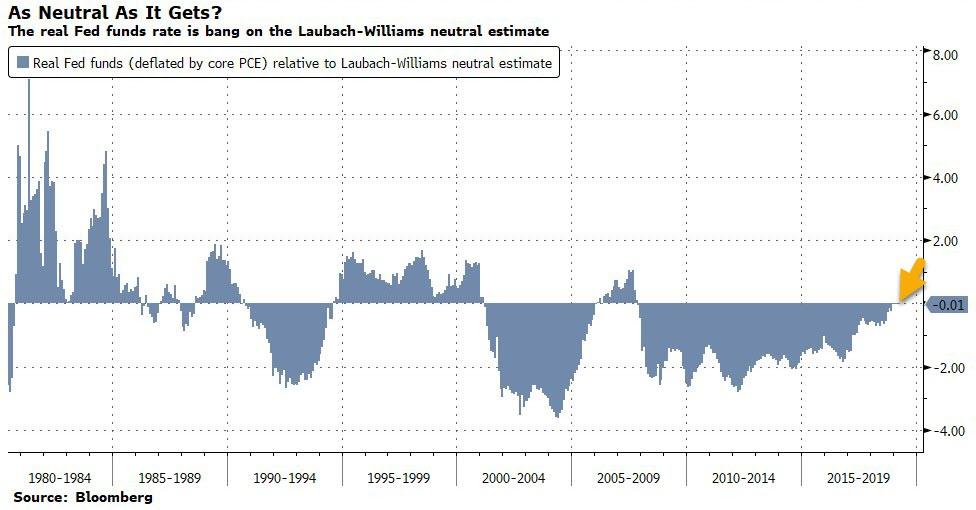

One of the big issues the Fed's wrestling with is

what constitutes neutral, and while there's a

lot of false precision in the r* framework, by one popular measure the funds

rate is already bang on neutral. Bloomberg notes that if we compare the real

policy rate (deflated by the core PCE price index) with the Laubach-Williams

estimate of the real neutral rate, we find a perfect match.

See

Chart:

AS Neutral

as it Gets?

{kind=link}

And

furthermore, 10Y yields have been glued to the Fed's long-term dot-plot rate

forecast since the start of 2018...

See Chart:

FED

Long Term Dot vs. 10Y UST Yield

{kind=link}

Expectations

are that the FOMC will maintain its more dovish

"patient" stance and shift from two hikes to one (zero would

likely scare the markets) in 2019. Currently, there is

a 73% chance that the Fed doesn't

hike in 2019. This will be evident in the

SEP with a lowered inflation and

growth outlook. As

of December, the Fed was anticipating 2.3% growth in 2019 and 2.0% in 2020.

“The focus is

going to be entirely on their dot plot and whether or not the Fed

has taken any chance of a rate hike out of their own internal forecast,” said Lara

Rhame, chief U.S. economist at FS Investments, which manages $24 billion.

“It’s going to be interesting to see if any of

the Fed has priced in a rate cut, which I doubt they have, and then how many are thinking they may still

need to adjust rates higher once or twice more throughout the year -- because I

think it’s been a little premature for the market to

discount any rate hike.”

And, along with when to stop shrinking

its asset portfolio, the Fed faces another decision - what mix of Treasurys it

holds, with implications for the economy.

Of course,

The Fed's biggest issue is being perceived as dovish enough - the rates market

is priced for 16bps of cuts... and how dovish is too dovish (what does Powell know that we don't?) and too hawkish risks a violent repricing in bonds and stocks which are expecting the

Fed to be patient, data-dependent and on hold.

See Chart:

{kind=link}

So what did

the Fed do today to bridge the gap between their hawkish, optimistic forecasts

for growth and their pessimistic narrative for rate trajectories. Well, Jay Powell went full dovetard:

- *FED LEAVES RATES UNCHANGED, SAYS ECONOMIC GROWTH HAS SLOWED

- *FED SIGNALS NO RATE HIKE THIS YEAR WITH ONE INCREASE IN 2020

As

expected, Fed officials reaffirmed their commitment to being “patient” on

future rate moves, while downgrading their assessment of the U.S. economy. They left the fed funds rate target at 2.25%-2.50% and kept

much of the statement relatively unchanged since January.

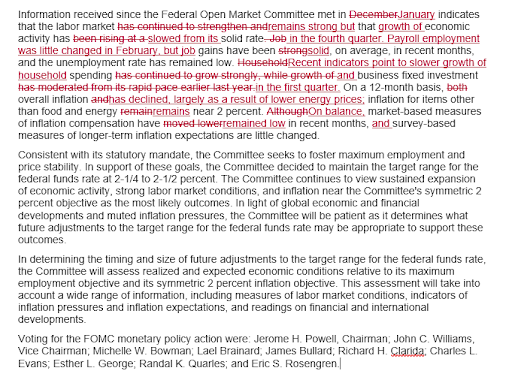

- ECONOMY: Policy makers now say economic activity has slowed from a solid rate in 4Q, say labor market remains strong; job gains still seen as strong on average amid low unemployment rate. Recent indicators point to "slower growth of household spending and business fixed investment in 1Q."

- GUIDANCE: Federal Open Market Committee still sees a sustained economic expansion, strong labor market conditions, and inflation near 2% objective as the most likely outcomes; will be “patient” in determining what rate moves may be appropriate, given global economic and financial developments and “muted” inflation pressures

- RISKS: Fed makes no reference to balance of risks

- INFLATION: Now says overall inflation on a 12-month basis has declined, largely due to lower energy prices, while core gauge remains close to 2 percent; now says market-based measures of inflation compensation have remained low in recent months; continues to see survey-based measures of longer-term inflation expectations as little changed

- VOTE: The decision was unanimous

On

the balance sheet, the Fed provided more specificity and detail than most had

expected. The Fed announced that they would:

- End the securities portfolio unwind at end Sept '19.

- Taper the Treasury unwind by reducing the cap on monthly redemptions from the current level of $30 billion to $15 billion beginning in May '19.

- Reinvest maturing MBS across the UST curve, not towards the front end as some expected.

- Cap MBS redemptions at $20 bn/month, which would limit impact of a large pre-pay wave.

- Prepayments above this amount would be reinvested into MBS.

- Hold their aggregate securities holdings constant for a time and allow for a continued shrinking of reserves via non-reserve liability growth (i.e. currency in circulation).

Looking at

the dots, the median assessment of appropriate pace of policy was slashed as the Fed's "dots" lose all credibility:

- 2019 2.375% (range 2.375% to 2.875%); prior 2.875%

- 2020 2.625% (range 2.375% to 3.375%); prior 3.125%

- 2021 2.625% (range 2.375% to 3.625%); prior 3.125%

- Longer Run 2.75% (range 2.500% to 3.500%); prior 2.75%

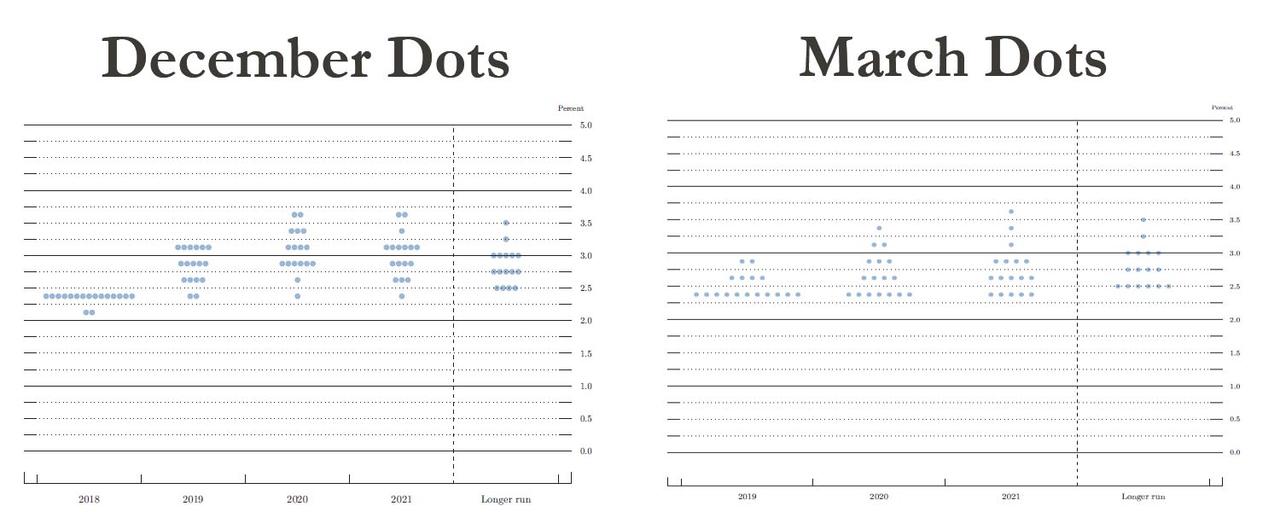

Compare

December vs March:

See

Charts:

December

dots vs.

March dots

{kind=link}

And

simplified:

See Chart:

Implied Fed Funds Target Rate

{kind=link}

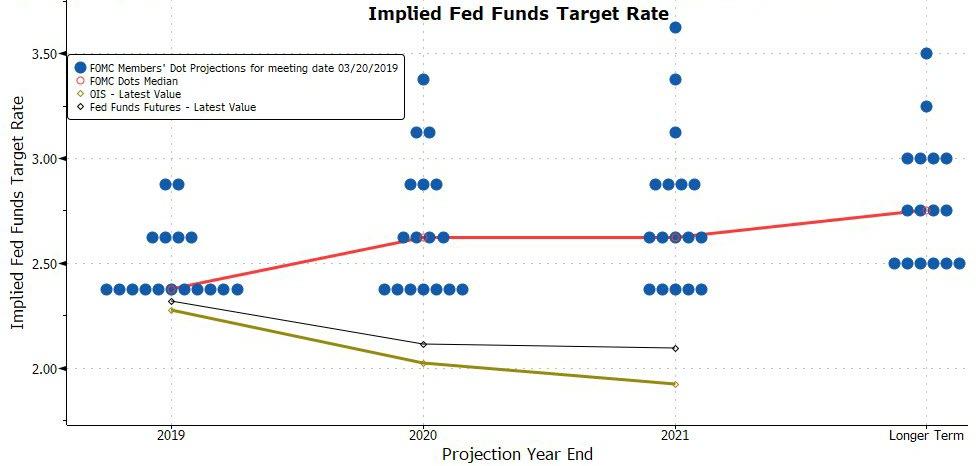

The Fed has

entirely folded to the market (but the market is still

pricing more dovishness)...

See Chart:

Implied

FED Funds Target Rate

{kind=link}

As

expected, to justify its Dovishness, the Fed cut its economic outlook, now

seeing 2.1% GDP in 2019 (from 2.3% in Dec) and 1.9% in 2020 (from 2.0%). The

unemploymen rate is projected to rise modestly to 3.8% by the end of 2020, from

2.6% in 2019, while inflation remains subdued, rising from 1.8% to 2.0% in 2020

vs 1.9% and 2.1% in the previous forecast. Finally, as noted above, the

median Fed Funds rate was slashed from 2.9% in 2019 to 2.4% and from 3.1% in

2020 to 2.6%

See Graph

GDP,

Unemployment & Inflation

Additionally, The Fed plans to end balance sheet

normalization in September.

Read the Full Red line below:

{kind=link}

…

----

----

Very usefull

----

----

US DOMESTIC POLITICS

Seudo democ

duopolico in US is obsolete; it’s full of frauds & corruption. Urge cambio

We talk about the 'Deep

State'...

===

“We’re on really risky ground when we’re

trying to place conditions on a federal election.”

====

The US is formally committed to dominating

the world by the year 2020...

“Full spectrum dominance” is not only a

danger to the world, it is a danger to US citizens who would also suffer the

consequences, if and when something goes wrong with their leaders’ complicated

space weapons.

See Chart:

{kind=link}

….

----

----

"Today we will launch a

criminal investigation about this and we will give legal assessment

of this information."

====

Governments

have lost control of the

narrative that they are in control of events... and they are scared to death...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

WORLD

investors in big trouble..

For

investors, one of the most important pieces of information is understanding where we are in the economic

cycle as it offers a critical gauge in risk-taking...

====

Citibank plans to sell the gold held as a guarantee... and deposit the excess of roughly

$258 million in a bank account in

New York... out of reach of Maduro.

====

... the Trump administration’s coup-by-narrative has not gone as planned...

====

SPUTNIK

and RT SHOWS

GEO-POL n

GEO-ECO ..Focus on neoliberal expansion

via wars & danger of WW3

----

----

----

----

----

----

----

----

----

----

----

----

NOTICIAS

IN SPANISH

Lat Am

search f alternatives to neo-fascist regimes & terrorist imperial chaos

REBELION

Banda d Trump vs el mundo: Rubio, Pompeo,

Bolton, Pen, Abrams

Ramón Pedregal Casa

Ramón Pedregal Casa

====

ALAI ORG

----

----

COUNTER

PUNCH

Analysis on

US Politics & Geopolitics

Binoy

Kampmark Global Kids

Strike

T.J.

Coles Countdown

to “Full Spectrum Dominance”

----

----

GLOBAL

RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy

Goodman’ team

----

----

PRESS

TV

Resume of

Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario