ND MAR 17 19 SIT

EC y POL

ND denounce

Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

It’s not just “hard” data, either...

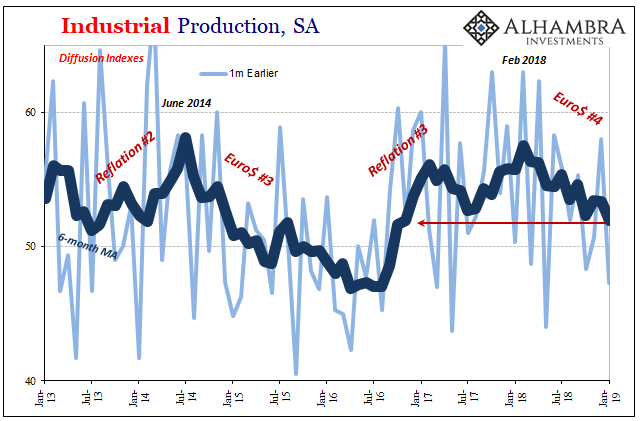

The Federal

Reserve, as part of its data on Industrial Production, calculates just such a

diffusion index (lagged by one month, meaning the updated diffusion indices are

for January 2019). The

monthly numbers are volatile and noisy, the average however unmistakable in

timing and interpretation.

Even the ISM’s PMI for the manufacturing sector has

tended to follow, not lead, the Fed’s diffusion numbers.

See Chart:

{kind=link}

…

----

----

by Tyler Durden

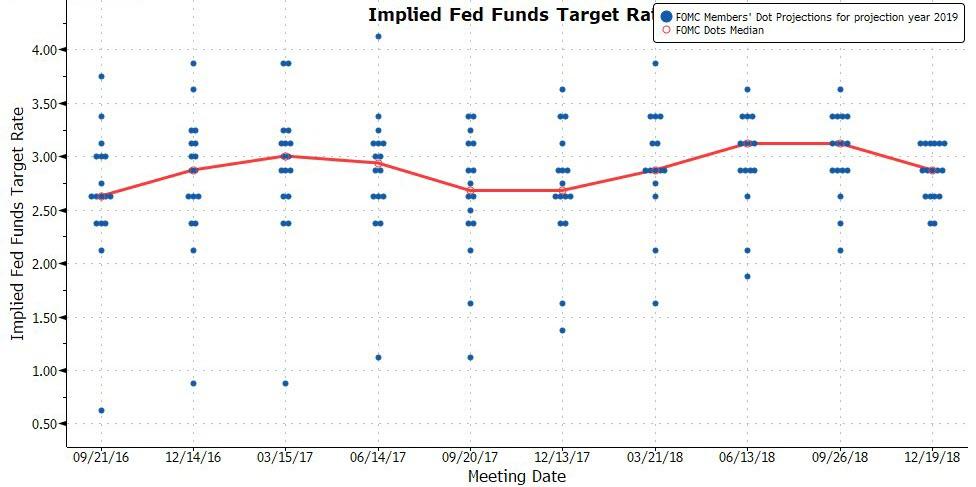

The Fed's March 19-20 two day

meeting will be to many at the FOMC a crash course in humility. Here's why.

Back in

December, when Powell infamously stated that the Fed's balance sheet unwind is

on "autopilot", a statement the Fed Chair promptly came to regret

just a few days later when the S&P briefly tripped into a bear market

before staging a historic rebound after Powell reversed dovishly on every

possibly occasion, the Fed indicated in its Summary of Economic Projections

that the US economy is growing at a solid pace, with GDP expected to reach 2.3%

in 2019 as the unemployment rate tumbled to 3.5% even as 2019 Core inflation

remained subdued at just 2.0%, a drop from the 2.1% projected at the prior,

September, SEP forecast.

See

Chart:

{kind=link}

But

more importantly, the Fed also revealed that it expects at least 2 more rate

hikes in 2019 (down from 3 in September), which would see the Fed Funds rise to

3.1% in Dec. 2019, and another rate hike in 2020 bringing the US rate to 3.1%

at which point it would peak before drifting lower to its longer-run rate of

2.8%.

See Chart:

{kind=link}

In a

February Bloomberg op-ed, Mohamed El-Erian made the case to eliminate the dots,

when Bill Gross' former partner suggested the Fed could consider following the

template of the Bank of England's "Inflation Report," which releases

a complete staff assessment of monetary policy conditions with fan charts

rather than point estimates. This gives more detail about the Fed's reaction

function and takes out the perceived precision of the dots.

In

retrospect, following the huge hit to the Fed's credibility that Powell's 180

degree reversal in the past three months created, it would certainly be

convenient to make the dots more conditional and scenario-based at this point

in the cycle. As Mester noted, the Fed has returned to "normal"

monetary policymaking, which means the outlook will be more conditional on the

outlook and less programmatic.

However, as

BofA warns, removing the dots at this

point would be helpful in the near term, but hurtful in the long run. When

the time comes to cut rates again, the Fed is likely to return the ZLB quickly.

The dots will then become a critical tool for the Fed who will otherwise have

limited ammunition. It is possible the Fed could stash the dots away during

good times and reintroduce them in downturns, but that only adds to the Fed's

credibility challenges. Moreover, such a move would

need consensus within the FOMC and many still see benefits in releasing the

dots.

How

will this happen?

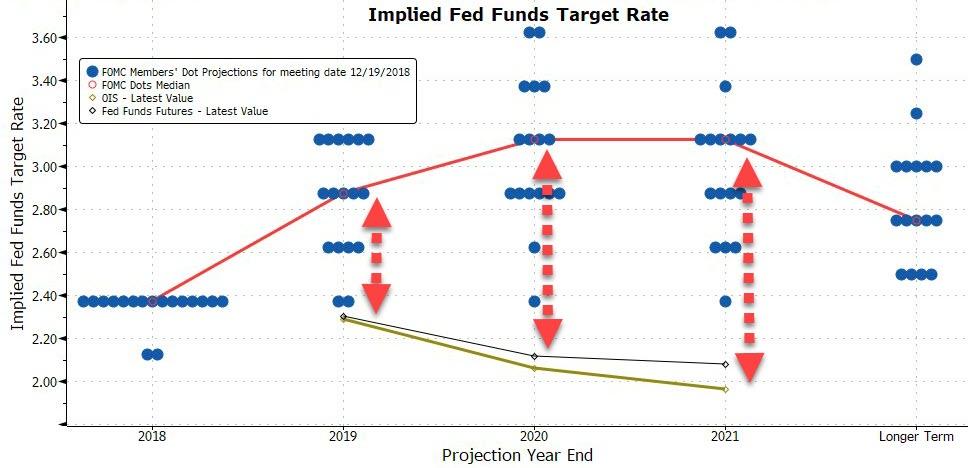

Looking at

the distribution of the dots, only

three FOMC officials would need to shift from two hikes this year to one hike

to move the median to one hike for 2019. That's the easy part; the difficult part is that no less than seven

officials would need to move to get the median to zero for this year which - as

BofA concedes - is a "much harder case to make", especially

without sparking fresh recession fears.

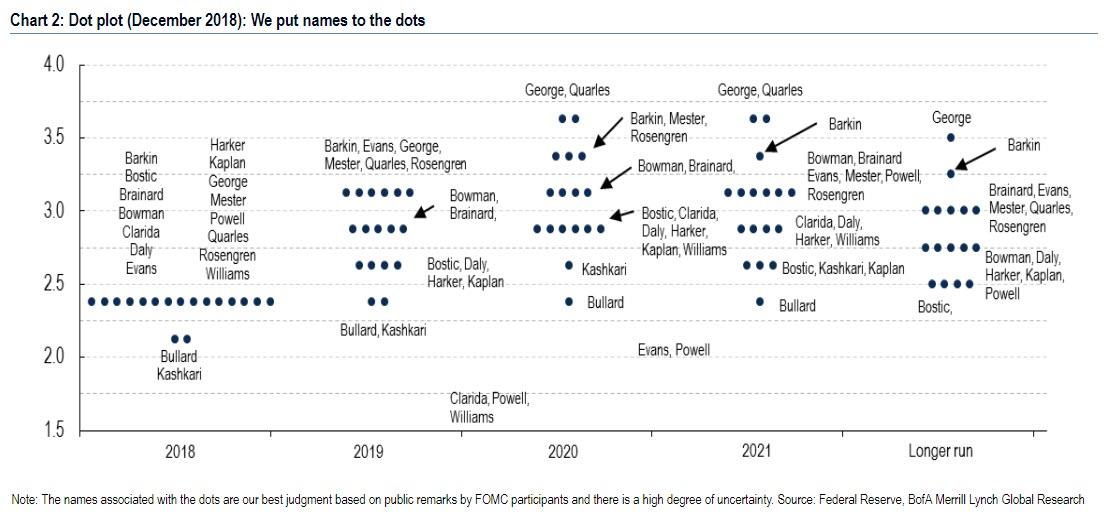

According to BofA's "dot exercise" the "core"

members of the FOMC were likely forecasting two hikes for this year in December

(Bowman, Brainard, Clarida, Powell, and Williams). Based on speeches since then, it appears these Fed officials

are all at risk of revising down their outlook for the path of policy. Other

Fed officials we pegged at three hikes in 2019 (eg, Evans) could also make the

move down to one hike.

See Chart:

{kind=link}

So once

again the dots will be confusing.: while the median will likely still show

hikes in the outlook (absent a shocking capitulation by most on the FOMC), the

core of the committee, which holds the trifecta, will likely shift lower,

perhaps removing all hikes for the year.

And just to

make sure the humiliation is complete, keep in mind that the market now expects

1 rate cut in 2020 (whether that happens is a different

matter as discussed earlier), so there is the

distinct chance that the Fed's capitulation may be even worse if, in order to

give the market comfort, Powell & Co. somehow manage to hint at a rate cut

in the coming year.

See Chart:

{kind=link}

How will

the market react, and whether all this dovishness (and

more) has already been priced in, will be revealed at 2pm on Wednesday.

….

----

----

About That Impending 'US Demographic Tailwind'

Narrative

According to a recent Morgan Stanley report,

linked HERE, the Millennials and Gen Z are about to

provide a positive "youth

jolt" to power the US economy higher, and "provide a rosier outlook for Social

Security and Medicare".

In Morgan

Stanley's own words;

"For

the U.S. economy, the demographic tailwinds created by these high-population

cohorts could be significant, delivering the kind of “youth jolt” that the Baby

Boomers were famous for. However, according to a recent report from Morgan

Stanley Research, the implications of these demographic shifts aren’t baked

into current Congressional Budget Office forecasts, in particular, the

projections for labor-force growth".

"Work by

the firm’s economic team, along with an in-depth survey of Generation Y and Z

consumers, uncovered a significantly brighter outlook for the U.S. in the

coming decades than previously thought. As Gens Y and Z combine in the

workforce, these two outsized generations could power higher consumption, wages

and housing demand, all pillars of GDP growth".

"In

addition, these new projections on labor-force growth could also mean a rosier

outlook for Social Security and Medicare solvency, offering investors an

overall bullish view for the U.S. between the 2020s and 2040s—and policymakers

a different perspective on the road ahead."

Before

reading my rebuttal, I really encourage readers to read through Morgan

Stanley's Research.

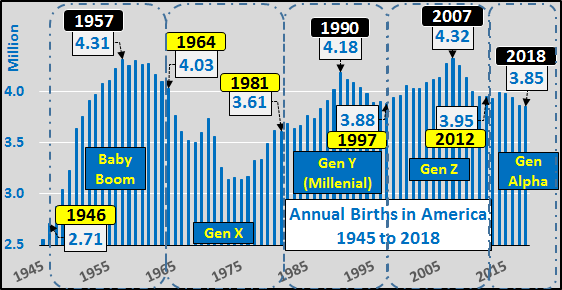

First,

I really struggle with the whole generational labels

as they represent uneven and ill-defined time periods. The chart below

shows annual US births since 1945 plus generation callouts. Meh?!?

See

Chart:

{kind=link}

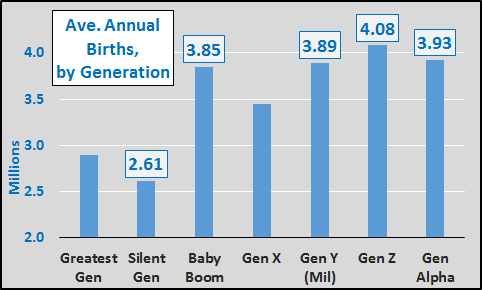

So, to put

some sense to the generations, I simply summed the total births during

each and divided them by the duration of each generation. Couple of

big noteworthy points:

- The Baby Boom represented a massive average increase of 1.6 million births annually over that of the previous Silent generation or a 66% uptick

- Gen Y (Millennials) average annual births increased less than 42 thousand annually over the Baby Boom, a 1.1% increase

- Gen Z average annual births were 230 thousand more than the Baby Boom, a 6% increase

- Gen Alpha (now 6 years underway) average annual births have declined by 155 thousand (-4%) compared to Gen Z

Due to

tanking fertility rates, a significantly larger total population (inclusive of

rising numbers of legal/illegal immigrants) has essentially had no more

children than during the Baby Boom.

See Chart:

{kind=link}

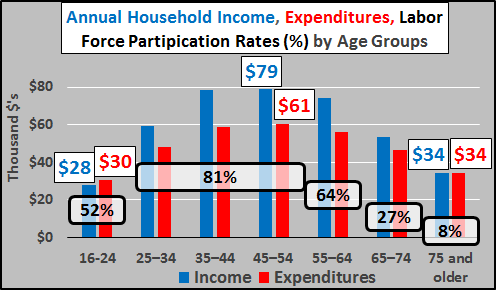

The

chart below highlights the average earning, spending, and labor force

participation differentials of the demographic segments. On average,

75+ year olds earn and spend half of what the peak age groups do...and have

just an 8% labor force participation rate compared to the 80% of the peak age

groups.

See Chart:

Annual Household

Income-Expenditure Labor

{kind=link}

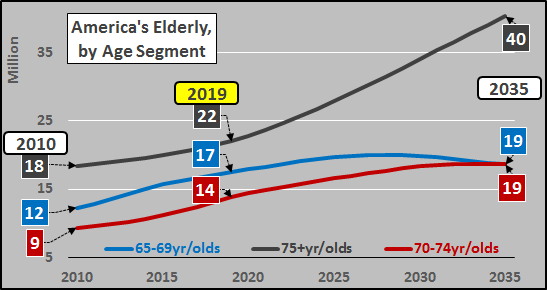

I

mention this because the 75+ year old population will be the driver of US

population growth for decades, as the chart below details.

See Chart:

American

Elderly by Age Segment

{kind=link}

Concluding Thoughts:

Given

mortgage rates still have little room to move lower, the mismatch of

elderly potential sellers versus younger potential buyers, and the student loan

hindered young adults choosing to delay marriage and have significantly fewer

children...I'm of a mind housing (anywhere near current prices) is oversupplied

and a variant of 2008's housing crisis is more likely than not. The US

economy is not about to be positively "jolted". But then again,

I'm just a blogger with no research team, nothing to sell, and no book to

talk. This is America, so when in doubt, just pick the source with the

happy story that suits you best.

….

----

----

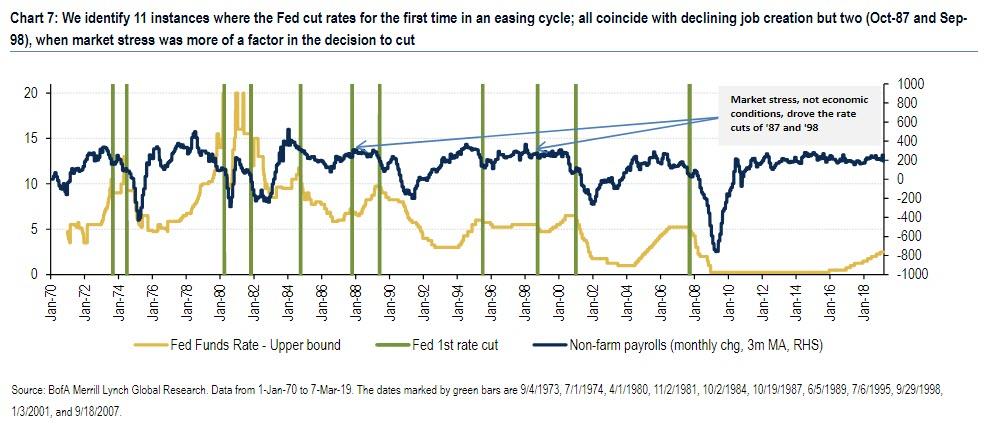

Today's low levels of recent

S&P realized volatility (30-day is around 10 vol points) appear

inconsistent with a rate-cutting environment, given that in only one instance

out of 11 historically was realized volatility lower than it is today

See Chart:

{kind=link}

Assuming

that is indeed the case, what does

history tell us about the behavior of equity vol in the lead-up to a cut"

To answer

this question, BofA looked at all major first cuts in Fed Funds since 1972.

While changes in short-term rates serve as a good barometer of monetary policy,

the means used by the Fed to pursue its mandate have varied over the years. For

example, between 1979 and 1982, under Volcker's leadership, the Fed used money

supply as the main tool to tame inflation, letting short-term rates fluctuate

more freely than in other periods. For those instances, BofA relied on

historical archives to pinpoint dates of important changes in Fed policy. The chart below shows the resulting dates, which the bank

used in its analysis of the relationship between Fed rate cuts and US equity

vol.

See Chart:

https://www.zerohedge.com/s3/files/inline-images/first%20rate%20cut%20in%20history.jpg?itok=HdIHey_e

{kind=link}

While

aggregate summary stats point to higher vol as we move towards a potential rate

cut, it is also worth considering

whether one of the periods where vol fell would be a relevant analogue to

today. Realized vol fell in the 6 months leading up to the cuts of

Jul-74, Jun-89, and Jul-95, while it barely rose in Jan-01. However, according

to BofA these periods in which vol fell are not appropriate analogues for

today, as:

- In 1974, this decrease in vol happened towards the end of an 18-month, 48% drawdown, where vol reached local highs prior to the Fed intervening. While we saw some market weakness in Q4-18, it doesn't compare to the depth of that selloff.

- In 1989, vol was still on the way down following the '87 crash, also not comparable to today's vol rising from record lows in 2017.

- In 1995, the Fed began a mild easing cycle seemingly in response to slowing growth and significant volatility in bond markets. Equity markets showed little concern leading up to the cut and, in fact, rose 50% in the 18 subsequent months, far from most people's outlook for markets today.

- In Jan-01, the episode when vol rose the least in the preceding 6 months, realized vol was already in the mid-20s following the pop of the Tech bubble, limiting its response higher to the cut in rates.

Finally,

looking at what the Fed Funds futures market was implying ahead of "first

cuts" in interest rates since 1989, it seems that in most cases the rates market was in fact

pricing in varying degrees of a hike, and was hence "surprised" by

the cut. Even though this didn't lead to a consistent response

from volatility across episodes, one may still wonder whether a potential rise in volatility is less

likely if markets accurately price the cut well in advance (as they may be

doing today). and by extension, whether such market discounting may prevent the

very event that is supposedly being priced in (i.e., not rate hikes until

stocks slide again and vol surges).

As BofA

concludes, while history doesn't help us establish much precedent here, today's low levels of recent

S&P realized volatility (30-day is around 10 vol points) appear

inconsistent with a rate-cutting environment, given

that in only one instance out of 11 historically was realized volatility lower

than it is today. All else equals, this suggests that all those who are

convinced the Fed's next act will be a rate cut in approximately 9 months may

be in for a rude awakening.

…

----

----

Is the winter of Europe's discontent coming to an end?

See Chart:

The

European Economy tends to follow China

{kind=link}

See More

charts at:

…

SOURCE: https://www.zerohedge.com/news/2019-03-17/spring-coming-why-europe-looks-set-surprise-upside

----

----

US DOMESTIC POLITICS

Seudo

democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge

cambio

Trump is hopping mad the EU for at least seven reasons. Mad enough to foolishly smack them with

tariffs? I Believe so.

----

----

It’s

just another name for an old, and very

stupid, set of economic ideas... MMT is about radically increased government control.

Now, this concept isn’t new. It’s been around for

decades. But its popularity has skyrocketed, thanks to endorsements from

Democratic presidential candidate Bernie Sanders and Congresswoman Alexandria

Ocasio-Cortez (AOC), the new rising star of the Democratic Party.

The left ? has a new obsession: Modern Monetary

Theory (MMT).

MMT is an economic theory which essentially argues

that the U.S. government wouldn’t need to collect taxes or borrow money to

finance spending. It could simply print more money if necessary.

….

[[ This view on MMT doesn’t fit with Keynesian

Economics where spending drives Econ growth and much less with Austrian

Economics (Mises Inst) where savings and

production (not mere speculation) drives

Economic growth. This MMT “theory”

doesn’t fit with the lines of most notorious

schools of Economics of our time (Keynes and Misses ) and much less with socialism.

That is because they still in the time of Smyth & neoclassical that believe

the market can cure itself its imperfections

without any intervention from the State-Gvt. The fact is that the 1930 crisis put

that theory in the trash bag. They couldn’t prevent the great depression and not even offered a solution to the

problem. I was Keynes

in his “General Theory of employment ,

Interest and Money” who offered a

solution to full employment and regular

growth. Since then the private sector (BIG

Corp) has to be monitor and regulated by Central Banks & Govt. The republican Eisenhower, Nixon, Ford and Regan failed, they did not get the GDP growth

expected, and the pro Keynesians FDR, Truman, Kennedy and Carter succeeded. .

“The left ?? has a new obsession for Modern Monetary Theory (MMT)”. That is false.

“MMT is an

economic theory which essentially argues that the U.S. government wouldn’t need

to collect taxes or borrow money to finance spending. It could simply print

more money if necessary”. It is what Trump is doing it.

The

socialists instead are in favor of regulation but in the interest of the labor

or workers. That is the difference. To classical Keynesians: whatever State expending generates growth

& they consider 4 factors: 1- Consumer spending (distorted by Corp propag).

2- Govt expending (in weapons & wars) 3- Business investment (based on

speculacion and Wall Street artificial

booms & burst) and 4- Net exports

(now we have a deficit with the USD at the point of collapse). All Economy depends on who is in power and in

whose interest it works. AOC and other socialists are

very clear on this point.

[[ In short This article depart from false premises: and arrive to false conclusion. Does AOC HAS SUSTAIN & DEFEND

MMT? Not that I know. WHERE? .. Then, this start with a grossness lie to finish with

insults to AOC, that is not way to debate decently. Are the debaters in

this art notorious Economists? NOT, that

I know. Then their insults came back to both comedians like a boomerang on

their head. ]]

----

----

Around 20% of Americans have a medical claim on their credit

report...

===

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

Missile launch plans were being relayed as the crisis

unfolded.

….

[[ What stupid

conflict: their enemy is not there.. It is here, in the US ]]

----

----

The meeting between US

President Donald Trump and Chinese counterpart Xi Jinping to end the trade war

which was tentatively pushed back from March to April, may be pushed back

again, this time to to June, the SCMP reported.

----

[[ Intentional or not.. this delay contribute to the fall of Trump ]]

====

SPUTNIK

and RT SHOWS

GEO-POL n

GEO-ECO ..Focus on neoliberal expansion

via wars & danger of WW3

They want WW3, if RU-China would’ve wanted too.. they will hit now

----

----

Election with duopoly system will

reproduce chaos.. no point in more circus

----

----

----

----

----

----

----

----

----

----

----

----

----

RT SHOWS

----

----

----

----

----

NOTICIAS

IN SPANISH

Lat Am

search f alternatives to neo-fascist regimes & terrorist imperial chaos

VIENTO SUR

Hezbolá Fundamentalismo religioso vs neoliberalismo Joseph Daher

----

----

RT EN ESPAÑOL

- Maduro pide renuncia a todo su gabinete de ministros para una "reestructuración profunda"

- The NYT revela que prácticas para pilotar los Boeing 737 MAX se hacían con un iPad

- Reporte: India y Pakistán amenazaron con atacarse mutuamente con misiles

- Advierten al US de graves consecuencias si aprueban ley que permita demandar a la OPEP

- Especial

del Califato Filipino: Testimonios de menores reclutados

por el EI: "Nunca olvidaré cómo maté a un cristiano"

----

----

GLOBAL

RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

-It

Started in Daraa on March 17, 2011: The US-NATO-Israel Sponsored Al Qaeda

Insurgency in Syria. By Prof Michel

Chossudovsky,

-

Fukushima

at Eight: Ongoing Cover-Up of the Nuclear Hazards in Japan and Abroad

By Michael Welch,

Dr. Helen

Caldicott

- Veterans

Call on U.S. Troops to Resist Illegal Orders to Invade Venezuela in Response to

Trump By Veterans for Peace

----

----

PRESS

TV

Resume of

Global News described by Iranian observers..

Programs The Debate

Ryach atrocities in Yemen

----

===

No hay comentarios:

Publicar un comentario