ND

MAR 29 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

US Economic situation today:

Summarizing

Q1 in one chart: Stocks soared

alongside a renewed surge in global money supply as top-down and bottom-up

fun-durr-mental data collapsed...

See Chart:

{kind=link}

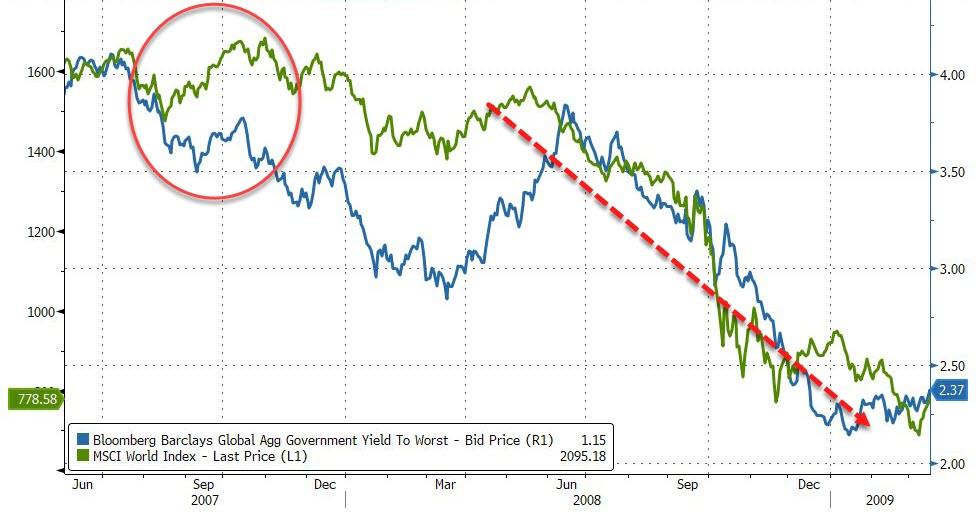

Global stocks and global bond yields

have decoupled dramatically in Q1...

See Chart:

{kind=link}

We have seen this before...and it

did not end well.

See Chart:

{kind=link}

Quite a quarter!

- Best quarter for world stocks since 2012

- Best quarter for US stocks since 2009

- Best quarter for oil since 2009

And...

Chinese stocks were panic bid

overnight, ending the quarter up 24% (China's

best quarter since Q4 2014, and best Q1 since 2009)... while EU

Ec went up too

See Chart:

{kind=link}

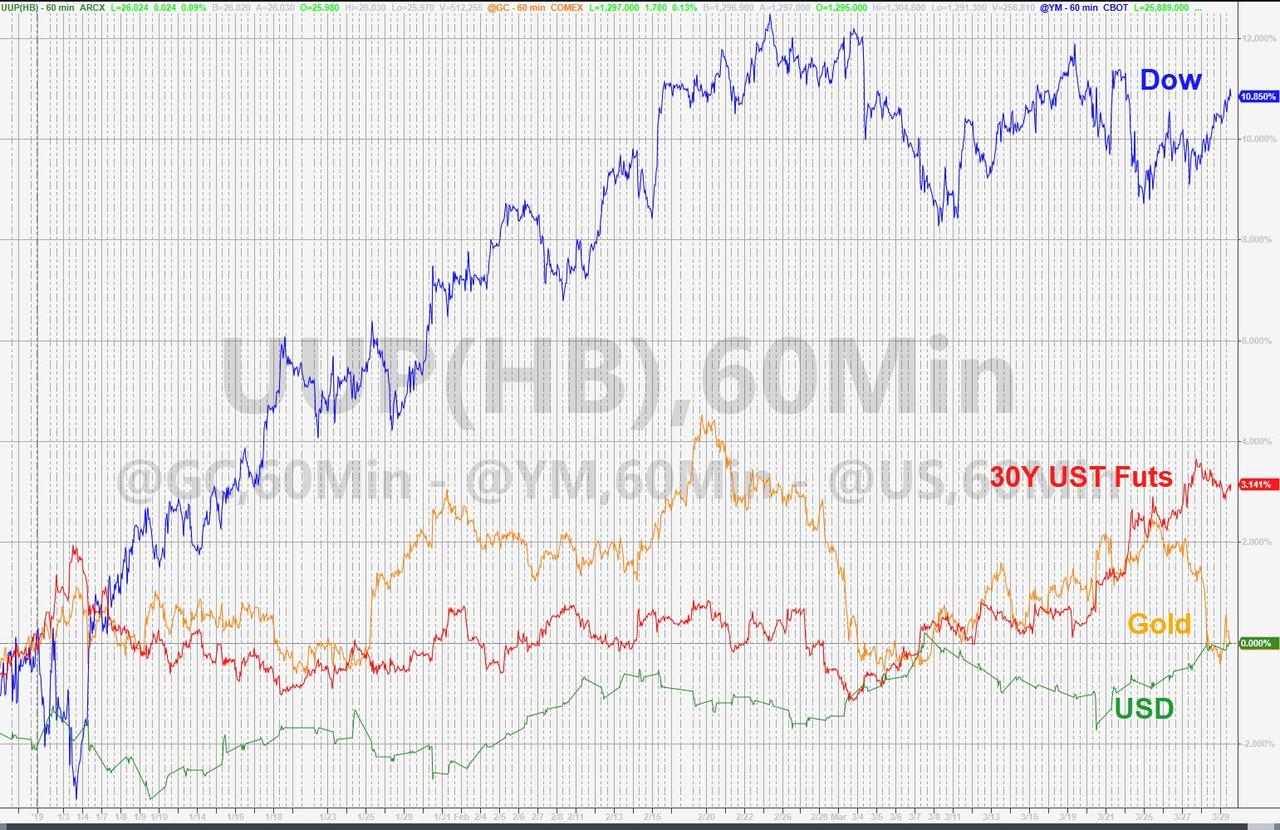

US Stocks outperfomed bonds

dramatically as Gold and the dollar ended unchanged in Q1...

See Chart:

{kind=link}

The S&P 500 manage to get back

above 2800 but is still struggling to follow-through...

See Chart:

{kind=link}

LYFT IPO opened at $87.24 (after

pricing at $72) but faded from the open...they defended $80 but that broke into

the close...

See Chart:

{kind=link}

FANG stocks soared in Q1 by 23.5% -

the best quarter since Q3 2013

See Chart:

{kind=link}

Credit (HY CDX -100bps, IG CDX

-24bps, biggest quarterly drop since Q1 2012) and equity (VIX -11.6 vols,

biggest Quarterly drop since Q4'11) protection costs collapsed in Q1...

See Chart:

{kind=link}

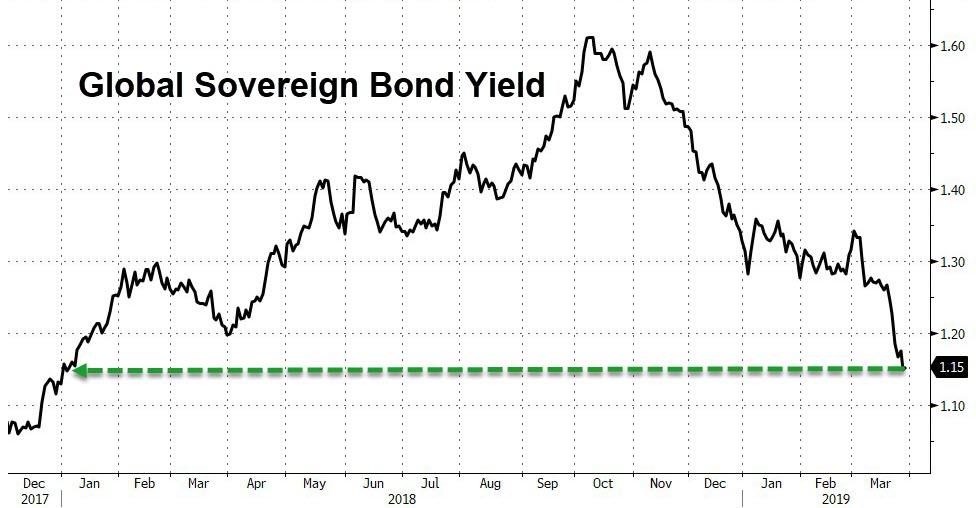

Global sovereign bond yields plunged

in Q1 (and Q4 2018) to their lowest since Jan 2018... (this is the biggest 2Q

drop in sov yields since the growth crisis in 2016)

See Chart:

{kind=link}

US Treasury yields plunged in Q1

(extending Q4's collapse)...

See Chart:

{kind=link}

30Y Yields are below 3.00%, 10Y

below 2.50%, and the rest of the curve plunged...

See Chart:

{kind=link}

The US yield curve has now flattened

for 8 of the last 9 quarters, plunging into inversion this week...

See Chart:

{kind=link}

Finally, we note that the markets

have seen an unprecedented swing in their outlook for The Fed...

{kind=link}

Rescuing stocks (for now) from their

1937 analog...

{kind=link}

…

SOURCE: https://www.zerohedge.com/news/2019-03-29/global-stocks-surge-best-quarter-2012-bond-yields-plunge

----

----

The controversy converted the inflation index from a "cost of

things" to a "cost of living" index. However, in reality, today’s inflation index is not a true

"cost of living" index as it’s missing important items, such as

financial assets.

Submitted

by Joseph Carson, Former

Director of Global Economic Research, Alliance Bernstein.

Inflation has often been involved in political controversy,

but today the pendulum has swung from politicians to monetary policymakers.

Politicians used the controversy over high inflation to force change in its

measurement. Monetary policymakers are using the controversy over low inflation

to force change in its policy guidance.

As monetary policymakers have become enmeshed in the

politics of the numbers it is important to understand

how the politics of inflation has shaped its measurement. Inflation for politicians is to be as low as

possible, while inflation for policymakers is to be as accurate as possible.

Those two are not always the same, and policymakers mistook it to be

true during the housing boom and failed to recognize market price signals. Are

policymakers risking making the same mistake again?

The relationship

between the two methods is not constant since

"cost of living" is more of an academic concept and not based fully

on market prices.

The politics of inflation often involved discussions over

which approach to employ for the indexation of social programs, and politicians

oftenfavored

whatever approach yielded low inflation.

See Chart:

{kind=link}

For example, in the early 1980s, consumer inflation (CPI),

based on the "costs of things" framework, was driving up the federal

government costs of indexation for social programs and the controversy over

measurement provided Congress a convenient format to use its statistical

policy-making role to force change, while also trying to reduce the budget

deficit. The controversy ended with Congress endorsing

its first shift towards a "cost of living" framework as it

recommended removing actual house prices and replaced them with a subjective

measure of owner’s rents.

The politics of inflation erupted again in the mid-1990s

when Federal Reserve Chairman Alan Greenspan told Congress the current measure

of inflation was over-stating actual inflation by a full percentage point,

costing the federal government billions in its indexation of government social

programs. Congress

demanded immediate action, with one piece of legislation going as far as

holding back on appropriations for the government statistical agencies until it

lowered the inflation index.

Soon

after, with Congress insistence government statisticians started to implement

various statistical changes in measurement, moving the inflation index one

large step closer to the concept of "cost of living".

The politics of inflation demonstrated how politicians have

used their political clout to lower reported inflation. While there were

legitimate issues of concept and design involved in both debates, political

opinion was mainly shaped by the dollars to be saved at the federal government

level if the inflation index were to increase more slowly.

The

controversy converted the inflation index from a "cost of things" to

a "cost of living" index. However,

in reality, today’s inflation index is not a true

"cost of living" index as it’s missing important items, such

as financial assets. So, in practice, the inflation index is mishmash, or a

hybrid, as it includes actual prices with "imputed" prices.

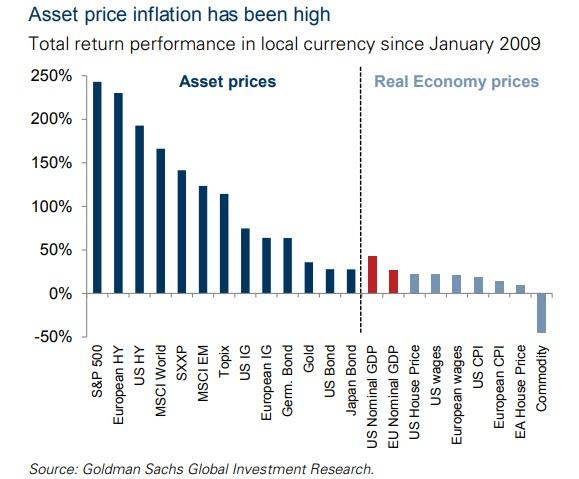

See Chart:

Asset Prices Inflation has been high

{kind=link}

A hybrid inflation index is not appropriate for monetary

policy as the focus needs be on the actual "cost of things." And

targeting a hybrid index becomes a problem when there is a great variance

between actual prices and imputed prices as evident in the 2000s when house

prices skyrocketed and "imputed" rents hardly moved. That trend is also present today

but on a smaller scale, suggesting the "cost of things" has been

moving up at a faster rate compared to the "cost of living".

Policymakers should borrow a page from the politicians

playbook and conduct a study of price measurement to ensure today’s measures

meets their purpose of economy wide inflation. It would also be wise to examine

why asset price cycles have been much greater since the shift towards a

"cost of living" index and numerical price targeting. Politics of inflation should never favor one type over

another as history has clearly

shown easy money creating or promoting inflation in only two areas (real and

financial assets) can be just as bad economically and financially as if it

shows up in all of the items.

….

----

RELATED:

This is a disturbing image reminiscent

of the Weimar Republic. Regardless of where it happens, hyperinflation

invariably equals economic

destruction.

----

----

...contrary to the popular view, a fall in the growth momentum of prices is always good news for

the wealth-generating process and hence for the economy.

Currently

we can observe a general slowdown in the annual growth rate in price inflation

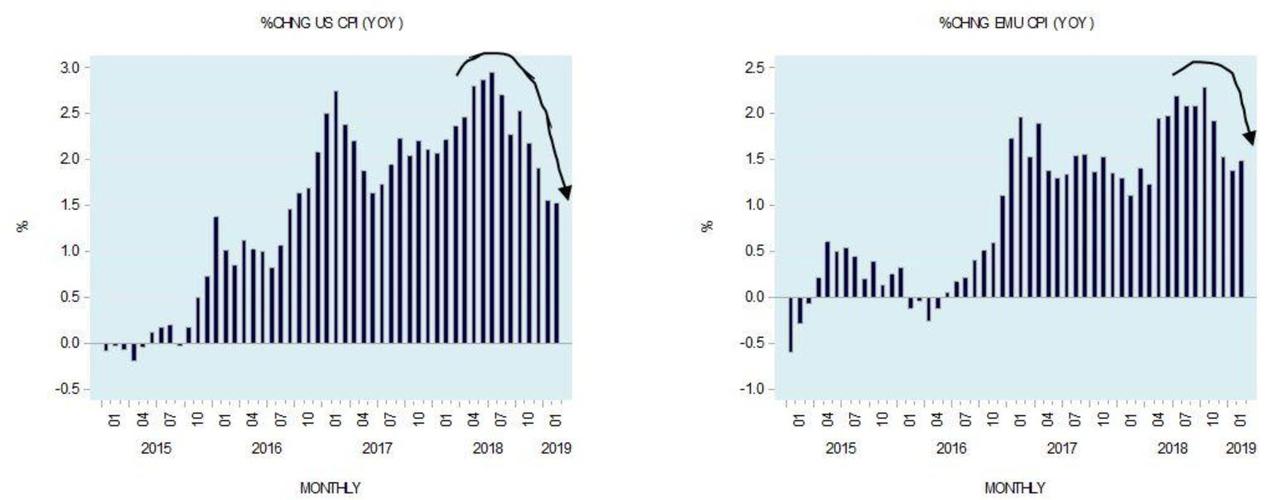

across major countries around the world. For instance the yearly

growth rate of the US consumer price index (CPI) fell to 1.5% in February from

1.6% in January and 2.2% in February last year. In Europe, the yearly growth

rate of the EMU CPI stood at 1.5% in February versus 1.4% in January and 2.3%

in October 2018.

See Charts:

{kind=link}

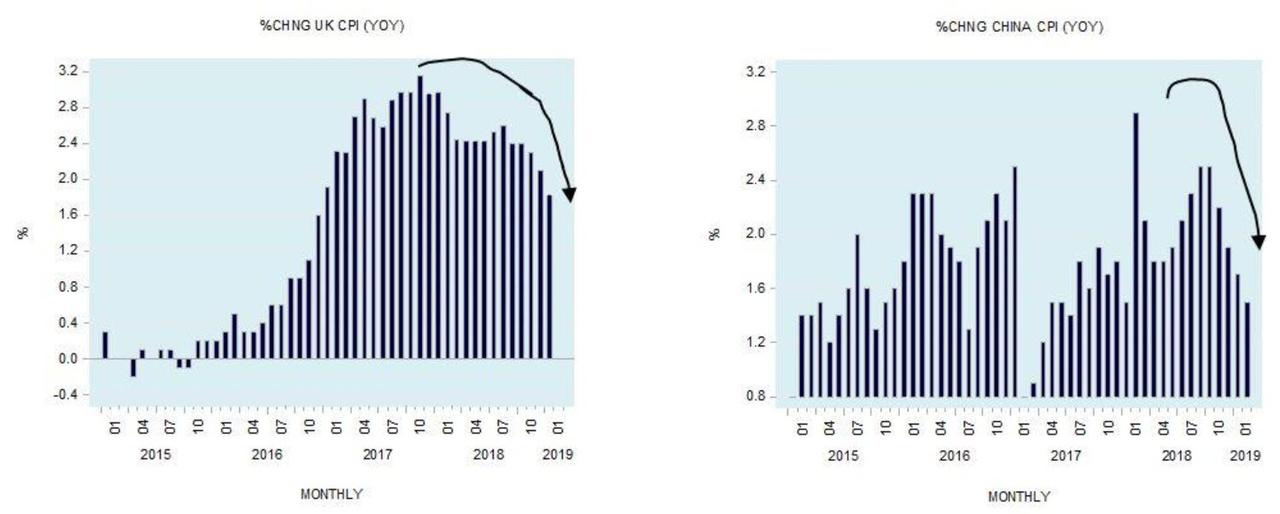

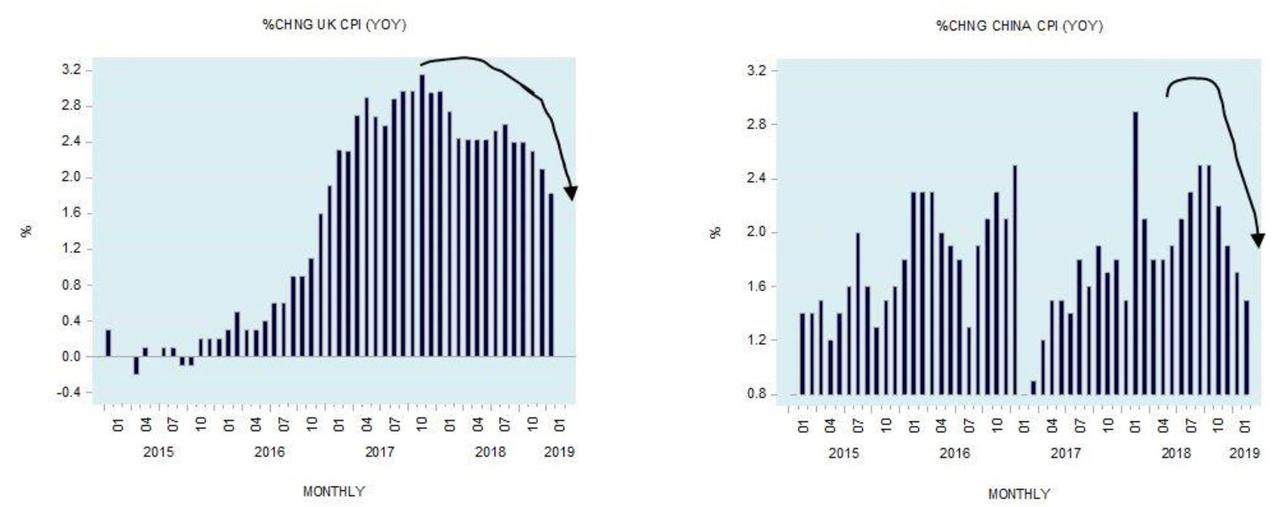

The annual rate of China’s CPI has also eased in February

falling to 1.5% from 1.7% in January and 2.9% in February the year before. The growth momentum of the UK CPI also displays softening

with the yearly growth rate standing at 1.8% in February against 2.1% in the

month before and 3% in January 2018.

See Charts:

{kind=link}

Most commentators are of the view that deflation generates

expectations for a decline in prices. As a result, it is held, consumers are

likely to postpone their buying of goods at present since they expect to buy

these goods at lower prices in the future. This weakens the overall flow of

spending and in turn weakens the economy.

Hence, such commentators believe that policies that counter

deflation will also counter the economic slump.For many commentators and

economic experts to counter a decline in the annual growth of the CPI, which

they fear could develop into a general decline in prices; they advocate that

central banks should maintain a very loose monetary stance. For these

experts a possible decline in prices — which they label as deflation

— poses a major threat to the economy.

See Charts:

{kind=link}

It would appear that if deflation leads to an economic slump

then policies that reverse deflation should be good for the economy. Reversing

deflation will simply involve introducing policies that support general

increases in the prices of goods, (i.e., price inflation). By this way of

thinking, inflation could actually be an agent of economic growth.

According

to most experts, a little bit of inflation can actually be a good thing. Mainstream economists believe that inflation of

2% is not harmful to economic growth, but that inflation of 10% could be bad

for the economy.

Why should

a rate of inflation of 10% or higher be regarded as a bad thing? If anything at inflation rate of 10% it is

likely that consumers are going to form rising inflation expectations, and

according to popular thinking, in response to a high

rate of inflation, consumers will speed up their expenditure on goods at

present, which should boost economic growth. Clearly, there is a problem with

the popular way of thinking.

Inflation Is not

Essentially a Rise in Prices

Inflation is not about general increases in prices as such,

but about the increase in the money supply. As a rule, the increase in money

supply sets in motion general increases in prices. This, however, need not

always be the case.

The price of a good is the amount of money asked per unit of

it. For a constant amount of money and an expanding quantity of goods, prices

will actually fall. Prices will also fall when the rate of increase in the

supply of goods exceeds the rate of increase in the money supply.

For instance, if the money supply increases by 5% and the

quantity of goods increases by 10%, prices will fall by 5%.

Now,

consider a situation in which money is created out of "thin air." This new money is no

different from counterfeit money. The counterfeiter exchanges the printed money

for goods without producing anything useful. He in fact exchanges nothing for

something. He takes from the pool of real goods without contributing to the

pool.

The

economic effect of money that was created out of thin air is the same as that

of counterfeit money — it impoverishes wealth generators.

The money created out of thin air diverts

real wealth towards the holders of new money. This weakens wealth

generators ability to generate wealth and this in turn leads to a weakening in

economic growth. Note that as a result of the increase in the money supply what

we have here is more money per unit of goods, and thus, higher prices.

What

matters, however, is not price rises as such but the increase in money supply

that sets in motion the exchange of nothing for something or "the counterfeit

effect."

Furthermore, if a fall in the growth momentum of prices emerges on the

back of the collapse of bubble activities in response to a softer monetary

growth, then this should be seen as good news. The less non-productive bubble

activities the better it is for the wealth generators and hence for the overall

pool of real wealth.

Likewise, if a fall in the

growth momentum of the CPI emerges because of the expansion in real wealth for

a given stock of money, obviously this is great news since more people could

now benefit from the expanding pool of real wealth. We can thus conclude that

contrary to the popular view, a

fall in the growth momentum of prices is always good news for the wealth-generating process and hence for the

economy.

…

----

----

You can spend more money

than you are bringing in for quite a while, but eventually a day of reckoning arrives.

The United

States is on a path to financial ruin, and everyone can see what is happening,

but nobody can seem to come up with a way to stop it. According to the U.S. Treasury, the federal

government is currently 22 trillion dollars in debt,

and that represents the single largest debt in the history of the planet.

Over the past decade, we have been adding to that debt at

a rate of about 1.1 trillion dollars a year, and we will add more than a

trillion dollars to that total once again this year. But when you add in

our unfunded liabilities, our long-term financial outlook as a nation looks downright

apocalyptic. According to Boston University

economics professor Laurence Kotlikoff, the U.S. is currently facing 200

trillion dollars in unfunded liabilities, and when you add that number to our

22 trillion dollar debt, you get a grand total of 222 trillion dollars.

Of course we are never going to pay back all of this debt.

The truth

is that we are just going to keep accumulating more debt until the system

completely and utterly collapses.

When you add it all

together, the total amount of debt in our society is

well above 300 percent of GDP, and it keeps rising with each passing year.

Our exploding debt is an existential threat to our nation,

and we are literally destroying the bright future that

our children and our grandchildren were supposed to have.

Boston University economics professor Laurence Kotlikoff has

been studying our unfunded liability crisis for many years, and according to

him the real number is

200 trillion dollars…

Consumers will largely bear the brunt of the country’s financial ruin,

according to Kotlikoff, which is why it is crucial to give them the power to

make better financial decisions.

While the United States’ official debt is $20 trillion, the fiscal gap

is really 10 times larger — $200 trillion. That comes from adding in

off-the-book liabilities, including debt that’s in the Federal Reserve’s hands,

Kotlikoff said.

If Kotlikoff is correct, that means that the true size of the financial

obligation that we are imposing upon future generations is 222 trillion

dollars, and that number just keeps rising month after month.

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

More troubling is that 37

million Americans had a 90-day delinquent strike added to their credit report last

quarter...

====

The American dream has morphed

into the American grift. And we normal people are the marks...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

ALL TIMERS way of thinking:

Bolton

unsheathes the Monroe doctrine...

…

Of course RU & China won’t pay

attention to this “b..t”. They’re ready to resp

====

Beijing is not backing down on its demands that all tariffs imposed

since the start of the trade war be lifted as part of any trade pact with the

US...

====

Real Economics on US:

"Yea, you need a 50bp rate cut, cause otherwise the math doesn’t work..."

“I don’t think the underlying economy is

slowing” when

everyone with a brain and basic understanding of data knows it is.

It’s cheerleading and playing the confidence game, while at the same

time demanding a 50bp rate cut by the Fed, an utterly ridiculous suggestion

especially in light of the earlier statement.

Getting the Fed to

stop the balance sheet rolloff and to stop rate hikes was the first obvious

step and the Fed acquiesced claiming to be data dependent.

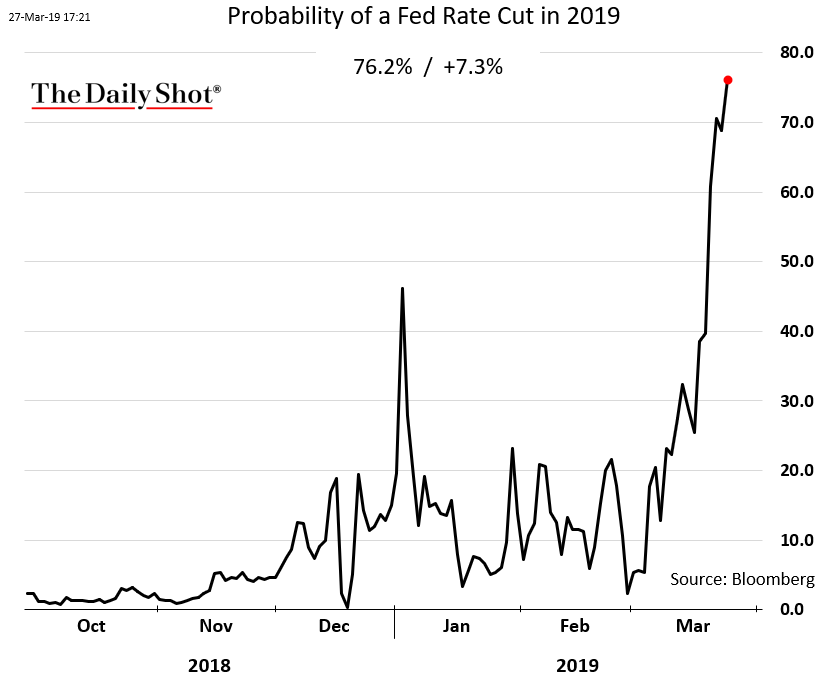

The second step: Get the Fed to cut

rates. Markets are already pricing

in a rate cut for 2019:

See Chart:

The Daily Shot

{kind=link}

But see this:

See Chart:

This is a recessionary image

{kind=link}

That’s recessionary risk this late in the cycle. But Larry Kudlow apparently thinks

a recession can get averted by juicing markets with more cheap money.

You know what else is recessionary?

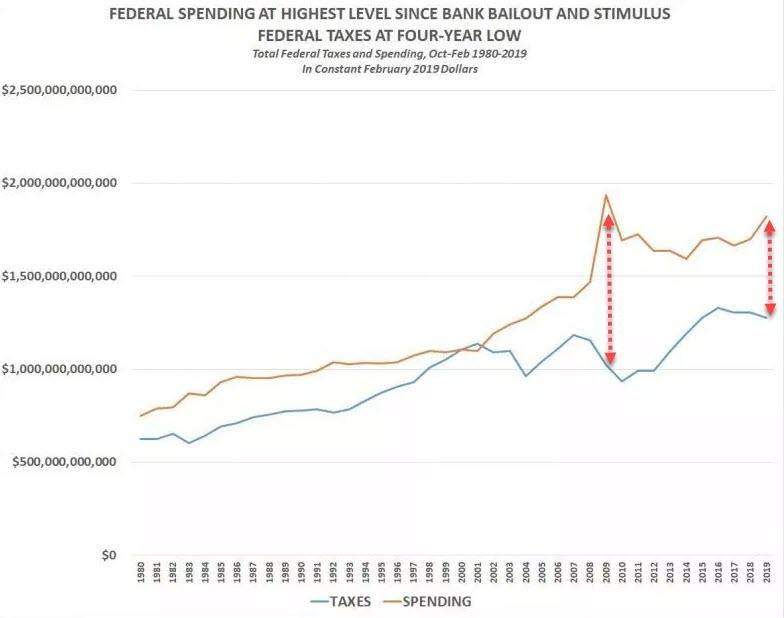

This:

See Chart:

{kind=link}

Oh it’s just the tax cuts. Really? Weren’t tax cuts supposed

to bring in all this growth that would pay for itself?

It hasn’t and it won’t, but the

spread between increased government spending and reduced government income is

widening the most since, well, the last recession:

See Chart:

{kind=link}

Yea, you

need a 50bp rate cut, cause otherwise the math doesn’t work.

To say that would be honest. But instead you get two faced

nonsense. Don’t fall for it. Recession coming is a real risk here. But nobody will admit it.

For the latest

public analysis please visit NorthmanTrader.

…

----

----

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

====

SHOWS RT

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

ALAI ORG

====

RT EN

ESPAÑOL

- Trump le pidió a Kim transferir sus armas nucleares a EE.UU.

- EE.UU. considerará el despliegue de fuerzas armadas de otros países en Venezuela "como una amenaza directa a la paz"

- Elliott Abrams afirma que "Rusia pagará" por su apoyo a Maduro

- Cuadrillas VEN de paz realizan ejercicios de defensa en todo el país

- ¿Cómo sale a la luz un diario VEN en medio de la oscuridad o apagón?

- Venezuela recibe 65 toneladas de medicament provenientes de China

- RU abre un centro para entrenar pilotos de helicópteros en Venezuela

- López Obrador responde a Trump por crisis en la frontera

- Trump arremete contra I Duque: " más drogas salen de COL Ahora"

- Apple cancela su ambicioso proyecto de carga inalámbrica AirPower

- 2019 : fin de los tiempos: video muestcómo será la desap del Universo

- "Presos políticos" y "exilio", palabras prohibidas en Cataluña

Keiser Report ¿El fin de Silicon Valley?

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

====

COUNTER PUNCH

Analysis on US Politics & Geopolitics

Jeffrey St. Clair Roaming

Charges: Rachel Maddow and the Muellers Invention

Andrew Levine Democratic

(Party) Socialism

====

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

====

DEMOCRACY NOW

Amy Goodman’ team

====

PRESS TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario