Labor’s share of the national

income is in

free-fall as a direct result of the optimization of financialization...

The Achilles Heel of our socio-economic system is the

secular stagnation of earned income, i.e. wages and salaries. Stagnating wages undermine every

aspect of our economy: consumption, credit, taxation and perhaps most

importantly, the unspoken social contract that the benefits of productivity and

increasing wealth will be distributed widely, if not fairly.

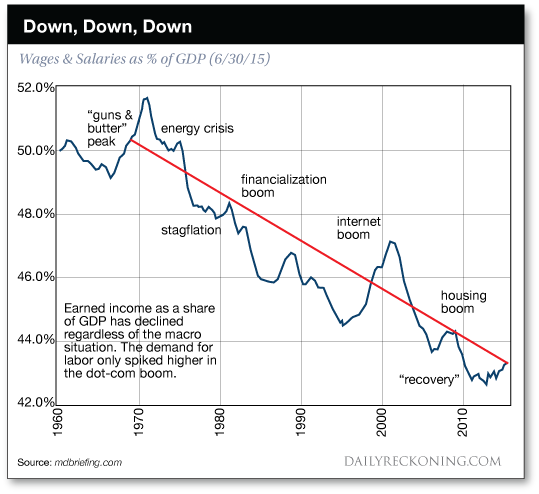

This chart shows that labor’s

declining share of the national income is not a recent problem, but a 45-year

trend: despite occasional

counter-trend blips, labor (earnings from labor/ employment) has seen its share

of the economy plummet regardless of the political or economic environment.

This chart shows that labor’s

declining share of the national income is not a recent problem, but a 45-year

trend: despite occasional counter-trend blips, labor (earnings from

labor/ employment) has seen its share of the economy plummet regardless of the

political or economic environment.

{kind=link}

Given the gravity of the

consequences of this trend, mainstream economists have been struggling to

explain it, as a means of eventually reversing it.

The explanations include automation,

globalization/offshoring, the high cost of housing, a decline of corporate

competition (i.e. the dominance of cartels and quasi-monopolies), a failure of

our educational complex to keep pace, stagnating gains in productivity, and so

on.

Each of these dynamics may well exacerbate the trend, but

they all dodge the dominant driver of wage stagnation and rise income-wealth

inequality: our economy is optimized for financialization, not labor/earned

income.

What

does 'our economy is optimized for financialization' mean?

It means that capital and profits flow to the scarcities

created by asymmetric access to information, leverage and cheap credit — the

engines of financialization.

Financialization funnels the economy’s rewards to

those with access to opaque financial processes and information flows, cheap

central bank credit and private banking leverage.

Together, these enable financiers and corporations to get

the borrowed capital needed to acquire and consolidate the productive assets of

the economy, and commoditize those productive assets, i.e. turn them into

financial instruments that can be bought and sold on the global marketplace.

Labor’s share of the national

income is in freefall as a direct result of the optimization of

financialization.

Meanwhile, the official policy goal of the Federal Reserve

and other central banks is to generate 3% inflation annually. Put another way:

the central banks want to lower the purchasing power of their currencies by 33%

every decade.

In other words, those

with fixed incomes that don’t keep pace with inflation will have lost a third

of their income after a decade of central bank-engineered inflation.

But in an economy in which wages

for 95% of households are stagnant for structural reasons, pushing inflation

higher is destabilizing.

There is a core structural problem with engineering 3%

annual inflation. Those whose income doesn’t keep pace are gradually

impoverished, while those who can notch gains above 3% gradually garner the

lion’s share of the national income and wealth.

Wages for the bottom 95% have not kept pace with official

inflation (never mind real-world inflation rates for those exposed to real

price increases in big-ticket items such as college tuition and health care

insurance).

Most households are

losing ground as their inflation-adjusted ( real) incomes stagnate or decline.

The stagnation of wages is

structural, the result of multiple mutually reinforcing dynamics.

These include globalized wage competition (everyone in

tradable sectors is competing with workers around the world); an

abundance/oversupply of labor globally; the digital industrial revolution’s

tendency to concentrate rewards in the top tier of workers; the soaring costs

of labor overhead (health care insurance, etc.) that diverts cash that could

have gone to wage increases to cartels, and the dominance of credit-capital

over labor.

The only possible output of pushing inflation higher while

wages for the vast majority are stagnating is increasing wealth-income

inequality — precisely what’s happened over the past decade of Federal Reserve

policy.

The stagnation of wages isn’t

supposed to happen in conventional economics. Once unemployment drops to the 5%

range, full employment is supposed to push wages higher as employers are forced

to compete for productive workers.

Alas, conventional economics is incapable of grasping the

fluid dynamics of labor, automation, capital, globalization and cost structures

dominated by monopolies and cartels in the 4th (digital) industrial revolution.

In sector after sector, employers can’t afford to pay more

wages as labor overhead costs march ever higher while prices are held down by

competition and oversupply. In other sectors, the rigors and supply, demand,

stagnant sales and productivity push employers to automate whatever can be

automated, and push tasks that were once performed by employees onto customers.

So why are central banks

obsessed with pushing inflation higher?

The conventional answer is that a

debt-fueled economy requires inflation to reduce the debtors’ future

obligations by enabling them to pay their debts with constantly inflating

currency.

This same dynamic enables the central state to pay its

obligations (social security, interest on the national debt, etc.) with

“cheaper” currency.

After a decade of 3% inflation, a $100 debt is effectively

reduced to $67 by the magic of inflation. If wages rise by 3%, the worker who

earned $100 at the start of the decade will be earning $133 by the end of the

decade, giving the worker 33% more cash to service debts.

The government benefits from

inflation in another way: incomes pushed higher by inflation push wage earners

into higher tax brackets, and their higher incomes generate higher taxes.

All this wonderfulness of inflation is negated if wages

can’t rise in tandem with inflation. In the view of the central banks,

deflation (i.e. wages buy more goods and services every year) is bad, and it’s

not hard to understand why.

The private banking sector benefits from inflation as well.

The lifeblood of banking profits is transaction and processing fees from

issuing new credit. Since inflation enables households to buy more stuff with

credit and service more debt, banks benefit immensely.

Deflation, on the other hand, is

Kryptonite to bank profits - households earning less every year are more likely

to default on existing debt and eschew new debt. As wages stagnate, an

increasing percentage of the populace becomes uncreditworthy, i.e. a marginal

borrower who isn’t qualified to borrow (and thus spend) more.

Unfortunately for the Fed and other central banks, there is

no way they can push wages higher to keep pace with inflation. Short of

creating $1 trillion in new currency and sending a check for $10,000 to every

household (something central banks aren’t allowed to do), central banks can’t

force employers to pay higher wages or force customers to pay higher prices to

enterprises.

Pushing

inflation higher while wages stagnate can be charitably called insane. Less

charitably, it’s evil, as it strips purchasing power and wealth from all whose

income isn’t keeping pace with central bank-engineered inflation.

….

----

----

No hay comentarios:

Publicar un comentario