ND

FEB 16 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

- A MOST

CONVENIENT VIRUS By Dmitry Orlov This virus was

genetically engineered in one of the Pentagon’s biological weapons laboratories

and introduced into China

====

ZERO HEDGE ECONOMICS

Neoliberal globalization is over.

Financiers know it, they documented with graphics

It's

"the other 1%" vs everyone else as scorching mega-cap earnings

strength from the FAAMG contrasts with small-cap earnings weakness.

The main reason why companies are beating is Trump himself:

i.e., a much lower

effective tax rate than expected (17% vs. 20%) aided in company margin beats, even as

overall margins contracted in every sector in the S&P 500 and declined in

aggregate for the fourth consecutive quarter.

Which brings us to the most fascinating aspect of Q4

earnings season, namely

the impact of what Morgan Stanley previously called "The

other 1 percent":the outsized influence of

the five biggest companies in the S&P.

As Goldman notes, results were disparate across the size

spectrum, with the 5

largest stocks (FB, AMZN, AAPL, MSFT, GOOGL) disproportionately boosting

aggregate S&P 500 results in 4Q. As

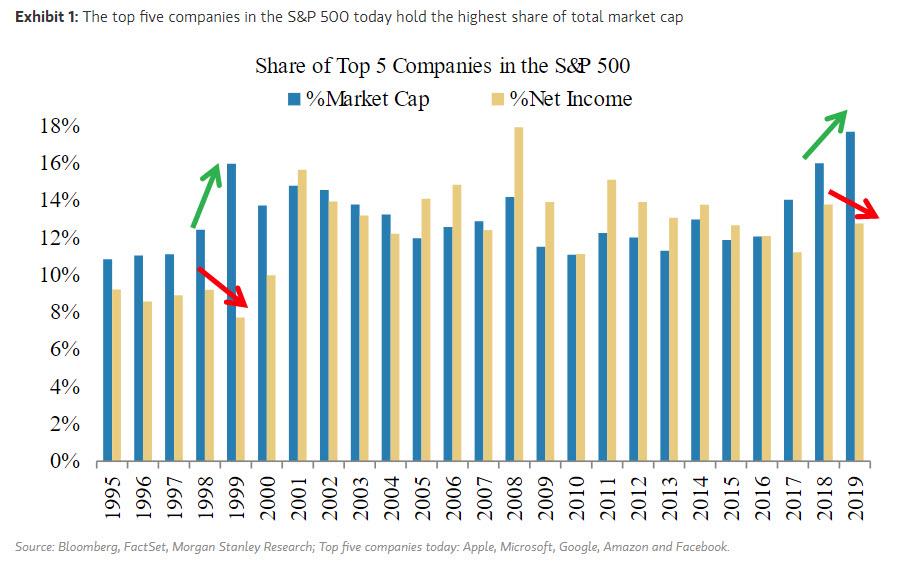

Morgan Stanley first noted a month ago, FAAMG account for 18% of S&P 500

market cap and 14% of S&P 500 earnings.

See Chart:

Share of 5 Top Companies in the S&P 500

{kind=link}

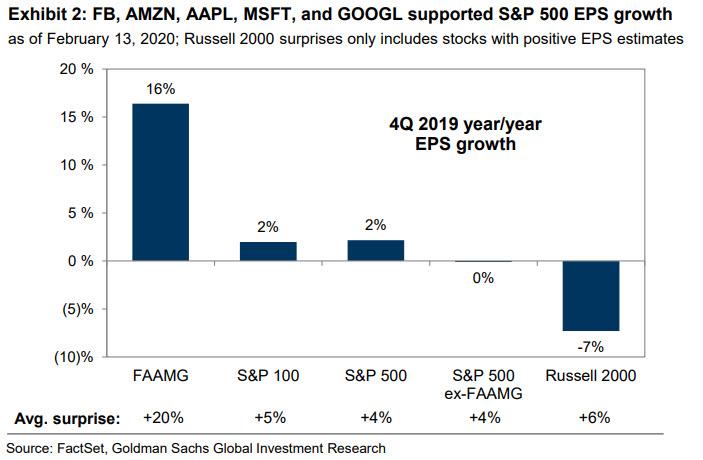

During the fourth quarter, these 5 stocks posted an average

earnings surprise of +20%, compared with just 4% for the average S&P 500

company. And the most striking conclusion from earnings season: the "other

1%", i.e., FAAMG, grew EPS by

16%, compared with 0% for the S&P 500 excluding these five stocks, or as Goldman puts it, "mega-cap earnings strength contrasts

with small-cap earnings weakness."

See Chart:

FB, AMZN, AAPL, MSFT and GOOGL

supported S&P500 EPS Growth

{kind=link}

WHO are d beneficiaries of Trump’

Economics?

As shown in the chart above, while the 5 biggest companies are just getting

bigger as they stretch their monopolistic wings, scorching EPS growth of 16%

Y/Y, the rest of the market is suffering, and the Russell 2000 experienced a

whopping 7% earnings drop during the fourth quarter, as many smaller firms posted weak top-line growth and had

difficulty absorbing rising wages and other input costs. The Russell 2000

has lagged the S&P 500 by 175 bp since the start of earnings season (+1%

vs. +3%).

Continue reading & see more

charts at:

----

----

The end of

the cycle is coming.

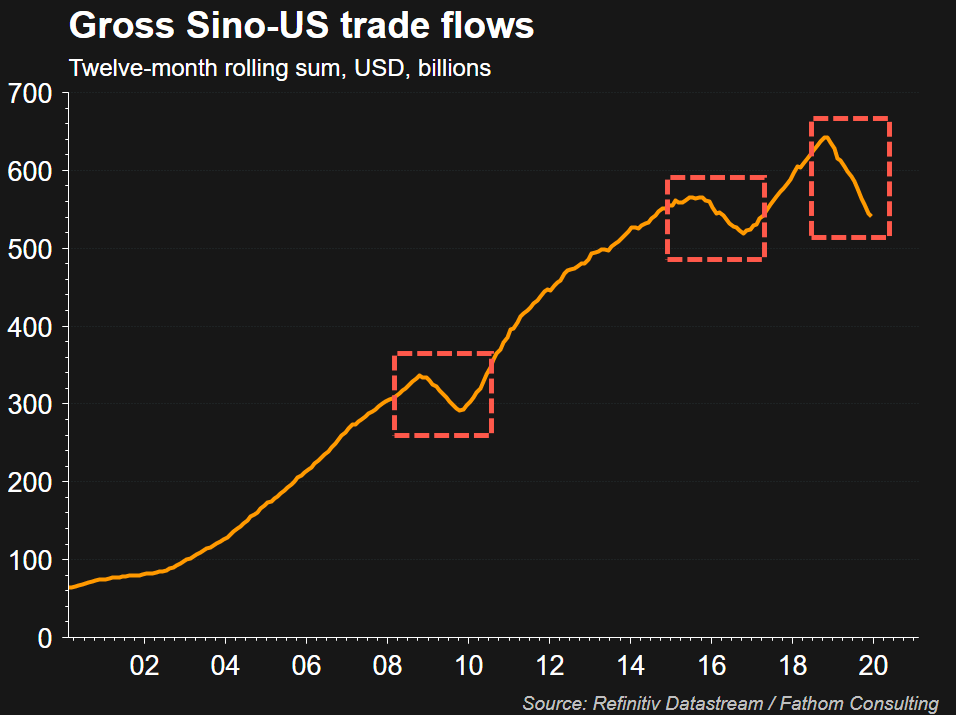

China and the US have enjoyed two decades of increasing

trade flows that have jumped from $61 billion a year in 2000 to $540 billion in

2019. But the ugly

end of globalization is starting to be

realized, as trade flows have plunged from Nov 2018 of $635 billion to $540

billion in Dec 2019, or about a 15% drop.

See Chart 1:

Gross Sino-US trade flows

{kind=link}

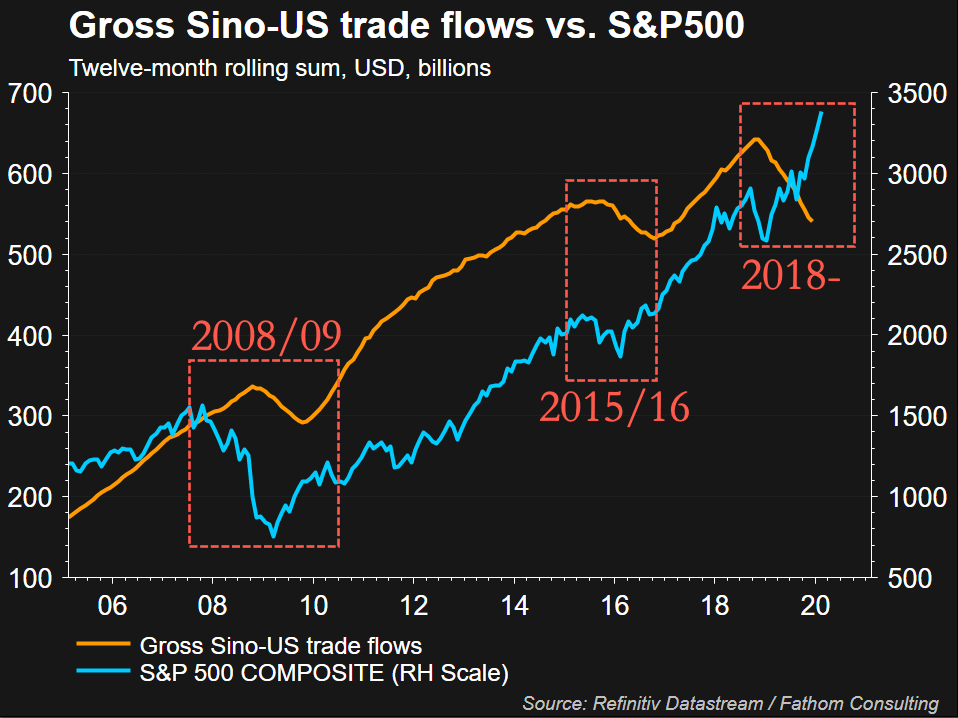

The IMF, WEF, and UN have already warned that the global

economy will continue to decelerate due to the

trade war – now it appears the virus shock will send the world deeper into

de-globalization that could lead to a financial crisis.

See Chart:

Gross Sino-US trade flows vs.

S&P 00

{kind=link}

….

SOURCE: https://www.zerohedge.com/markets/sino-us-trade-flows-reveal-next-market-crash-could-be-nearing

----

----

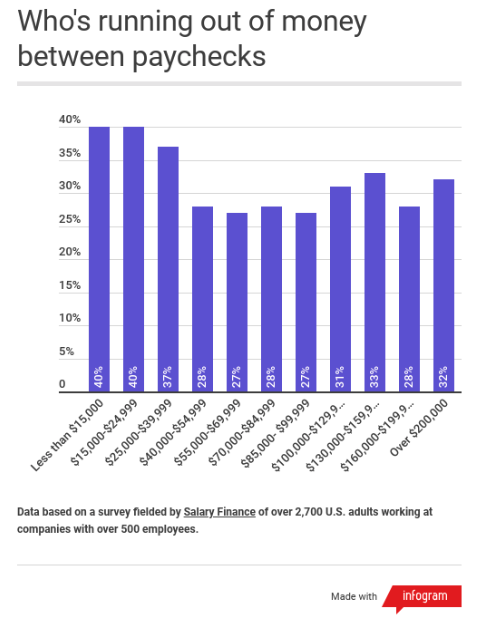

This will get worse when

the next recession strikes...

Amy is one of those Americans who are all too familiar with

her household running short on cash as her husband makes about $50,000 per

year.

And which

responders are running out of money in between paychecks?

Well, it's widespread according to the data – at least a third on average across all salary ranges.

See Chart:

Who’s running out of money between

paychecks?

{kind=link}

See more charts & comments at:

….

----

----

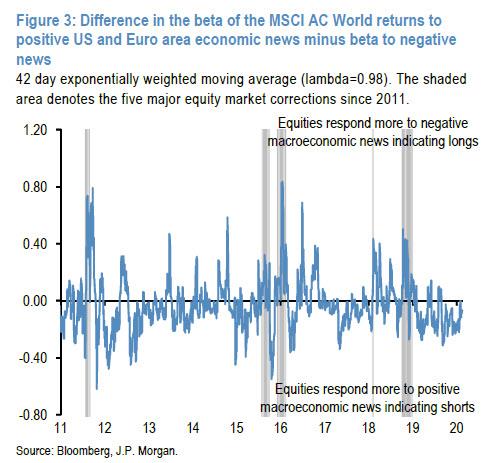

In a rising market, investors

typically find themselves shorter than desired, but once a correction arises,

investors quickly find themselves much longer than desired exposing market

vulnerabilities.

See Chart:

{kind=link}

What is notable here, is that when the MSCI AC World index is more responsive to positive economic news

and less responsive to negative news, this would point

to an overhang of short equity positions and vice versa.

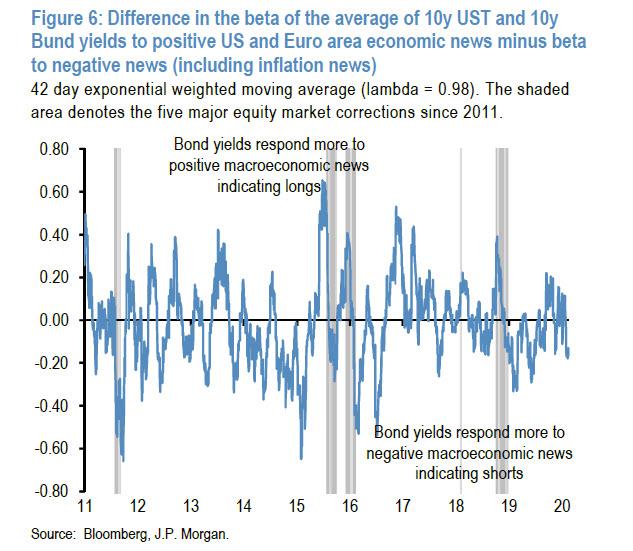

See Chart:

{kind=link}

Bond Yiels respond more to negative

macroeconomic news indicating Shorts

See Chart:

{kind=link}

Therefore the

fact that these indicators have been mostly negative this year does not

necessarily reflect investor positioning. In

fact, for equitiesthe bank's position

indicator look rather elevated especially among CTAs and Equity Long/Short

hedge funds. As such, the way to read these indicators is

that in a rising market,

investors typically find themselves shorter than desired, but once a correction

arises, investors quickly find themselves much longer than desired exposing

market vulnerabilities.

….

----

----

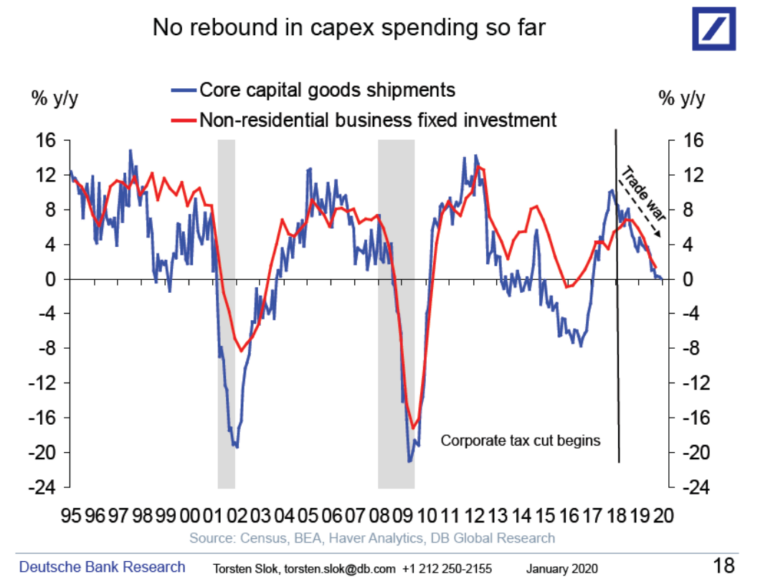

One of the most alarming aspects of this

buyback bonanza is that companies are repurchasing shares at a fever

pitchwhile insiders are dumping their shares at an equally feverish

rate...

In the US, senior

management teams have been pikers when it comes to what is typically referred to as “cap ex”. This is despite 2018’s monster corporate tax cut which was supposed

to accelerate capital expenditures. In reality, their long downtrend has

continued but what has truly exploded is the rate of share repurchases, aka,

buybacks.

See Chart:

No rebound

in cap-ex spending so far

{kind=link}

EXPLANATION: Summary

- The main international benchmark excluding the US has essentially flat-lined for 14 years, while the S&P has continued to set new records since 2009.

- China, which has been one of the most important developing countries for the last thirty years, outpaced the United States in terms of economic growth; however, its stock market has continued to lag.

- This has been the same story for emerging markets as a whole; superior economic growth with much lower stock market returns.

- A prime reason for this outcome is that faster growing countries need capital to fuel their expansions with a combination of debt and equity issuance.

- As such, fast economic growth requires large quantities of equity offerings, which often dilutes existing shareholders.

- In the US, senior management teams haven’t accelerated capital expenditures.

- Instead, what has truly exploded is the rate of share repurchases, aka, buybacks.

- In 2018 alone companies paid out a combined $1.25 trillion in dividends and buybacks.

- The dark side of this is that net debt to cash flow is at a 16-year high, as dividend and buybacks have been running above excess cash flow since 2013.

- To elevate debt to dangerous levels to enable share repurchases is the antithesis of judicious corporate stewardship.

- This is almost certainly destroying long-term value for shareholders (though this won’t be obvious for years to the market overall).

- Due to the Fed’s four QEs, the 2018 corporate tax cuts, and trillion-dollar federal deficits, this day of reckoning has been postponed.

- One of the most alarming aspects of this buyback bonanza is thatcompanies are repurchasing shares at a fever pitch while insiders are dumping their shares at an equally feverish rate.

- This hypocritical behavior has become a target of both political parties; this likely poses an immediate threat to the continuation of buybacks at any (long-term) cost.

BYE-BYE

BUYBACKS?

Continue reading at

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Much of Sander's appeal comes from his promises he can

deliver a more just society... exposing a glaring weakness in the democratic system, and that is, ahighly motivated minority can overwhelm an

unmotivated majority...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

China Adopts 'Cultural

Revolution-Style' Social Controls To Crush Outbreak As Death Toll Nears 2,000

"Can’t

get off here fast enough..."

====

"We

will support qualified firms so that they can resume work and production as

soon as possible, helping maintain stable operations of the economy and

minimizing the epidemic's impact."

====

Which is

good news - the closer we get to a depression, the closer we are to the moment

when central bankers will literally buy everything.

See Chart:

{kind=link}

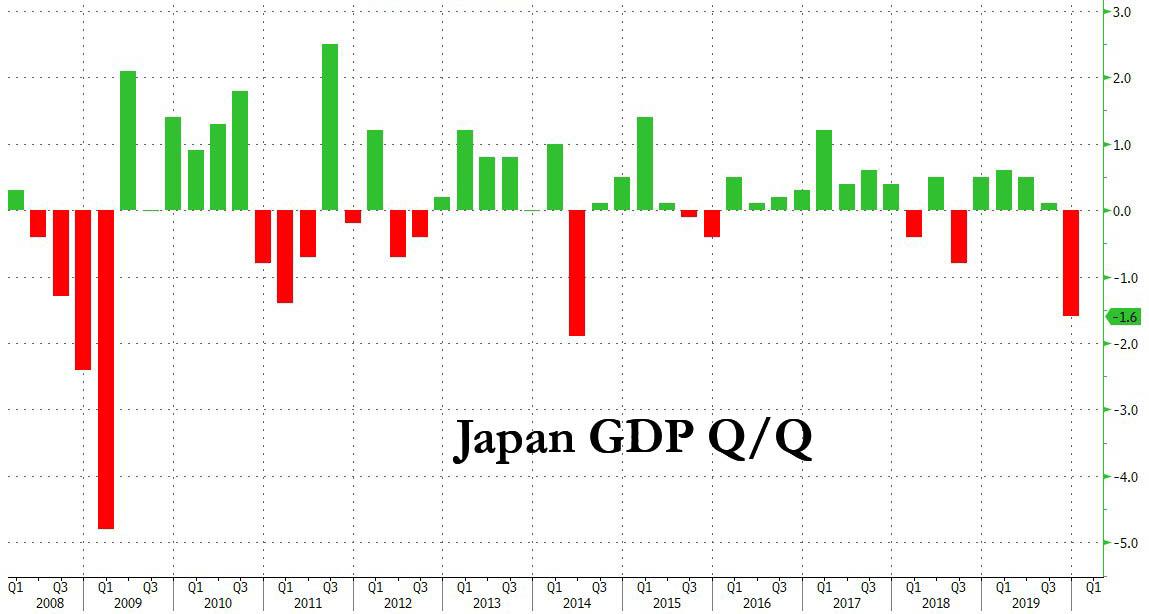

One look at the GDP components confirms that the plunge was

largely the result of collapsing consumption, with Houshehold Consumption plunging at an 11.5% annualized pace, the second

biggest drop that Private Demand plummeted at an -11.1% annualized basis...

See Chart:

Japan Real GDP Anualized Consumption

of Households

{kind=link}

….

SOURCE: https://www.zerohedge.com/economics/japan-unexpectedly-reports-terrible-gdp-it-slides-recession

====

"We

will preserve the Peace!"

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

RT EN ESPANIOL

Evo Morales: "En tres meses el gob de facto de

Áñez ha destruido todo lo que hemos construido con el pueblo" https://actualidad.rt.com/actualidad/343235-morales-acusar-gobierno-anez-destruir-meses-todo-construido

López Obrador: "'Don Dinero' ya no va a decidir

sobre la vida pública de México" https://actualidad.rt.com/actualidad/343247-lopez-obrador-don-dinero-no-decidir-vida-publica-mexico

Guaidó regresa a Venezuela tras su gira

internacional y se enfrenta a un escándalo de corrupción https://actualidad.rt.com/video/343244-guaido-regresar-venezuela-gira-internacional

Las fuerzas sirias toman el control de los

alrededores de la ciudad de Alepo https://actualidad.rt.com/video/343240-fuerzas-sirias-toman-control-alrededores-alepo

Tribunal Supremo Elect de Bolivia definirá la próx

semana si autoriza la candidatura de Evo Morales https://actualidad.rt.com/video/343226-tribunal-supremo-electoral-bolivia-definir-candidatura-evo-morales

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

-Andrew Levine Mayor

Mike, Worse Than Mayor Pete

-Russell Mokhiber NPR

and the Escalating Attack on Single-Payer Health Care

-Peter Certo Who’s

Afraid of Socialism?

----

----

ASIAN NEWS

Press TV

The Debate on Trump’s power

----

===

No hay comentarios:

Publicar un comentario