ND FEB 24 19 SIT EC y POL

ND

denounce Global-neoliberal debacle y propone State-Social + Capit-compet in

Econ

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

The only thing that’s “well anchored” is

the stupidity of the belief that inflation

expectations matter...

The amount of sheer nonsense written about inflation

expectations is staggering.

Let’s

take a look at some recent articles before making a mockery of them with a

single picture.

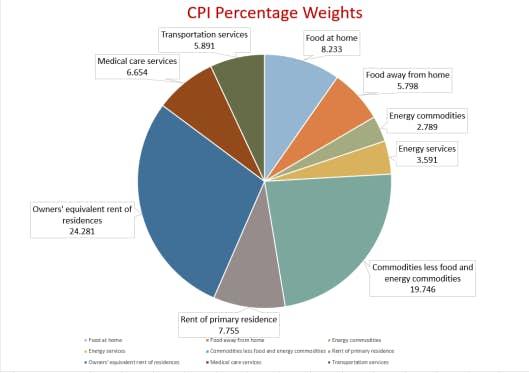

See Graft:

CPI Percentage Weights

{kind=link}

….

----

----

"...markets have gotten way ahead of the underlying fundamentals..."

Last

weekend, we discussed the two things driving the markets currently:

The

first is the Fed.

As we discussed

with our RIA PRO

subscribers (use code PRO30 for a 30-day free trial) last week,

“Today,

[Cleveland Fed Reserve Governor Loretta Mester] all but put the kibosh on

further rate hikes and, per Mester’s comments, will end balance sheet reduction

(QT) in the months ahead.”

The

second is “hope.”

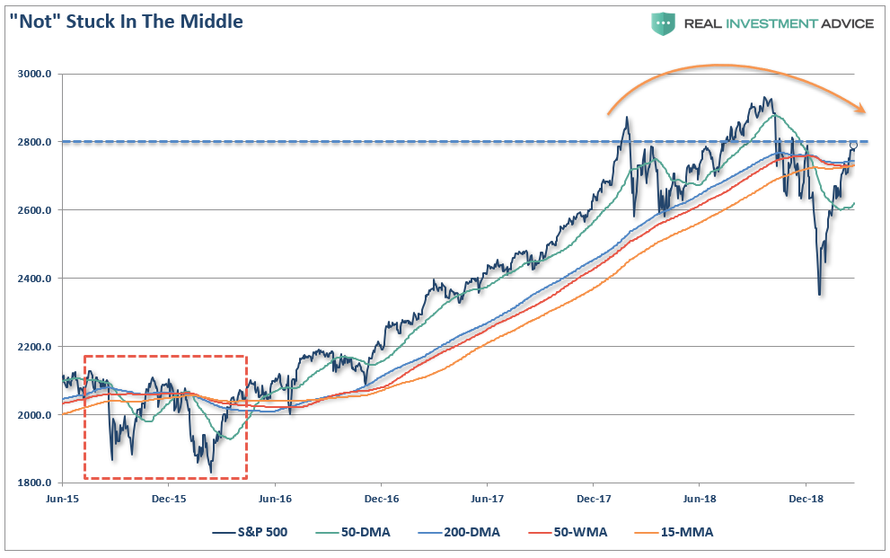

On Friday, on

headlines that talks are continuing with China, the market pushed through those

resistance levels as shown below. “

See Chart:

Not Stuck in the Middle

{kind=link}

It is EXACTLY the same story this

week.

- The release of the Fed minutes showed a broad consensus by the Fed to end “Quantitative Tightening” or “QT” by the end of 2019 as well as a removal of any effort to normalize the Fed’s balance sheet.

- The markets rallied on continued hopes of a resolution to the ongoing trade dispute between China and the U.S.

However,

the Fed’s actions should actually make you question the significance of any

resolution on trade.

“Why do you say that? Everyone knows the trade dispute was a big

factor in the sell-off last year?”

Maybe.

But, if

that was indeed the case, then the economic turmoil should be primarily tied

between the U.S. and China. However, as I

discussed in “The

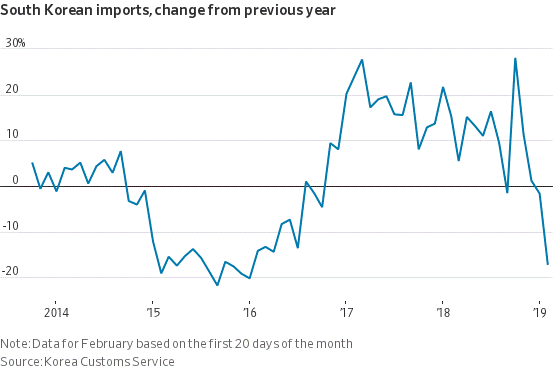

‘There Is No Recession In Sight’ Chartbook,” the economic disintegration has gone global.

See

Chart 1:

South Korea Imports change from Previous year

{kind=link}

See

Chart2:

The negative surprise in Q4 so far is…

{kind=link}

And as David Rosenberg noted:

The Citi Global Economic Surprise index, at -21.6, is nearly the

same as it was at the Dec 24th market low. It's now 227 days below zero -- only

exceeded by the Great Recession of 2008-09. Markets totally devoid of economic

realities.

See

Chart at:

https://www.zerohedge.com/news/2019-02-24/bulls-charge-ahead-economic-slowdown

In other

words, there is more going on globally which has very little, if anything, to

do with U.S. trade wars with China.

Which

brings us back to the Fed.

“Participants supported the removal of

the hiking bias and its replacement with a sentence emphasizing a ‘patient and

flexible approach.’ Participants pointed

to tighter financial conditions, softer inflation, slower foreign growth, and

trade policy uncertainty as justifying a patient approach to policy. However,

a range of views were expressed on what adjustments to the funds rate may be

appropriate later this year. ‘Several’ participants argued rates increases were

necessary ‘only if’ inflation was higher than in their baseline, but ‘several’

other participants indicated that hikes would be appropriate if the economy

evolved as they expected. In addition, ‘many participants noted that if

‘uncertainty abated,’ the FOMC could alter the ‘patient’ statement language.”

Why the

sudden switch from “hawkish” to “dovish?”

Was it just the market correction that sent Jerome Powell scurrying for cover,

or, despite still optimistic views on U.S. economic data, is there more to the

story than they are currently saying.

If such is the case, then the recent rally

in the markets may NOT be justified and further deterioration in forward

earnings may become more problematic. This is particularly the case as

valuations have quickly reverted back to near 30x earnings.

The bull

charge into an economic slowdown is not a trivial matter.

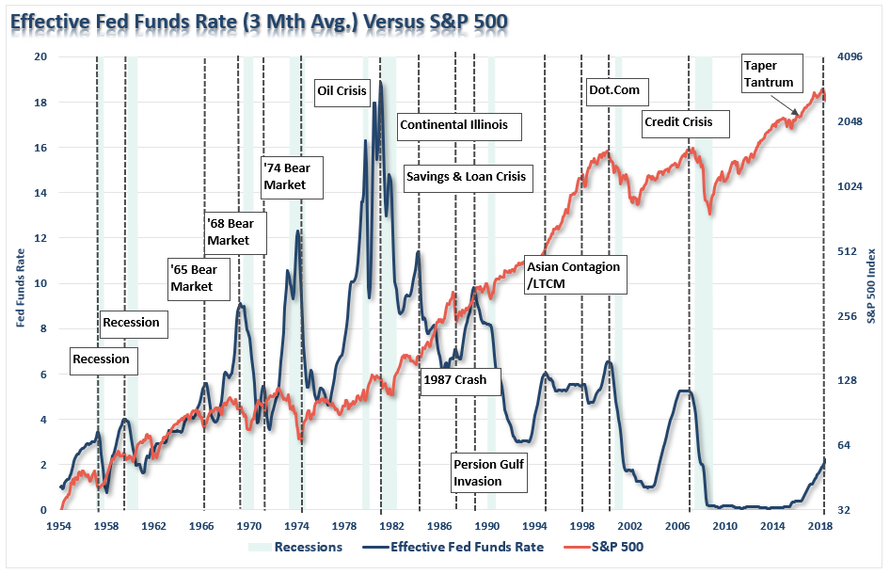

Historically,

it is the point where Fed has stopped their monetary policy interventions that

things have gone wrong.

See Chart:

Effective FED Funs Rate vs. S&P500

{kind=link}

But that

is not necessarily a bad thing. As we discussed with our Pro-Subscribers last

week, this is where opportunity also lives:

“Those who see that the last 10-years of

experimental stimulus has been on par with, or arguably exceeded, policies

historically reserved for major wars gain a unique and valuable perspective of

the current monetary mirage. The

demise of those policies, as they are bound to unravel, will reveal a multitude

of investment opportunities left behind in the ill-advised euphoria of

anti-capitalism.”

There

is nothing wrong with “hoping” for a

positive outcome from “trade talks.” We should

be hoping for that. The

problem is the rush to “buy” equities has effectively “priced in” the

best of all possible outcomes which suggests any resolution could be

disappointing.

The Technical Backdrop Is No Longer

Optimal

Continue reading

What To Expect Next

Continue reading

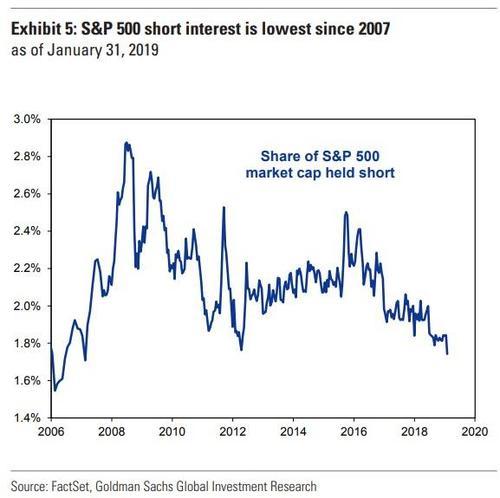

This

analysis also corresponds to the extremely rapid reversion of both technical

and sentiment measures, as well as the level of short-interest in the market

which has now fallen to levels not seen since 2008.

See Chart courtesy of Zero

Hedge

S&P 500 short Interest is lowest since 2007

As of Jan 31, 2019

{kind=link}

Let me

reiterate from last week:

“The important

point here is that from a contrarian standpoint, markets have gotten way ahead

of the underlying fundamentals. While the market may indeed end the

year on a higher note, it will most likely not do that without lower prices

first.”

While

our portfolios remain primarily long -biased currently, we are holding a higher

level than normal of cash and have added small levels of “hedges” to

portfolios which we will begin building into as the market reverses.

Statements like these are always

misinterpreted to mean that we are “bearish,” hiding in cash,

and have 6-cases of spam and a carton of Twinkies sitting on our desk.

Our job

as investors, and portfolio managers, is to navigate the market capitalizing on

opportunity when they are available, and preserving capital when risks exceed

our thresholds.

Currently, risk exceeds our

threshold.

….

Read the

full article at:

…

----

----

US DOMESTIC POLITICS

Seudo

democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge

cambio

WE'RE

LIVING IN 'THE GROUNDHOG SHOW' MUST READ!

...in which our leaders make the same mistakes over &

over...

----

----

"The terms ‘gang association’ or ‘gang membership’ have become

a form of criminalizing mostly young

people of color"

----

----

US-World ISSUES (Geo Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

"@SecPompeo and their assassins are desperate to fabricate a pretext for war."

----

----

It is a

request of US military attack en VEN

Opposit leader seeks outside help for "the liber of our

homeland"

----

----

President Maduro addressed the nation on state-owned TV

urging his supporters to revolt if he is harmed and telling Trump

"Yankee, go home!"

----

----

SPUTNIK and RT SHOWS

GEO-POL

n GEO-ECO ..Focus on neoliberal

expansion via wars & danger of WW3

Lo que necesita el SUR es la liberación del neo-nazi

Bolsonaro en BRA.

RELATED

----

----

----

Tendria que sacar de la carcel a su padre por juicios

pendientes que viene acumul

----

----

----

----

----

----

----

----

----

NOTICIAS IN SPANISH

Lat Am

search f alternatives to neo-fascist regimes & terrorist imperial chaos

VIENTO

SUR

----

----

----

----

----

----

----

----

----

----

----

----

RT EN ESPAÑOL

----

----

----

----

----

----

----

----

Keiser Report "El bitcóin es como oro

sintético, nuevo oro o oro 2.0"

----

----

GLOBAL RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

----

----

----

----

----

PRESS TV

Resume

of Global News described by Iranian observers..

----

----

----

----

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario