ND FEB 17 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone

State-Social + Capit-compet in Econ

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know

it, they documented with graphics

"The

same old tired, failing inflationist responses are being lined up,

despite the evidence that monetary easing has never stopped a credit crisis developing..."

The major economies have

slowed suddenly in the last two or three months, prompting a change of tack in

the monetary policies of central banks. The same old tired, failing inflationist responses are being lined up,

despite the evidence that monetary easing has never stopped a credit crisis

developing. This article

demonstrates why monetary policy is doomed by citing three reasons. There is

the empirical evidence of money and credit continuing to grow regardless of

interest rate changes, the evidence of Gibson’s paradox, and widespread

ignorance in macroeconomic circles of the role of time preference.

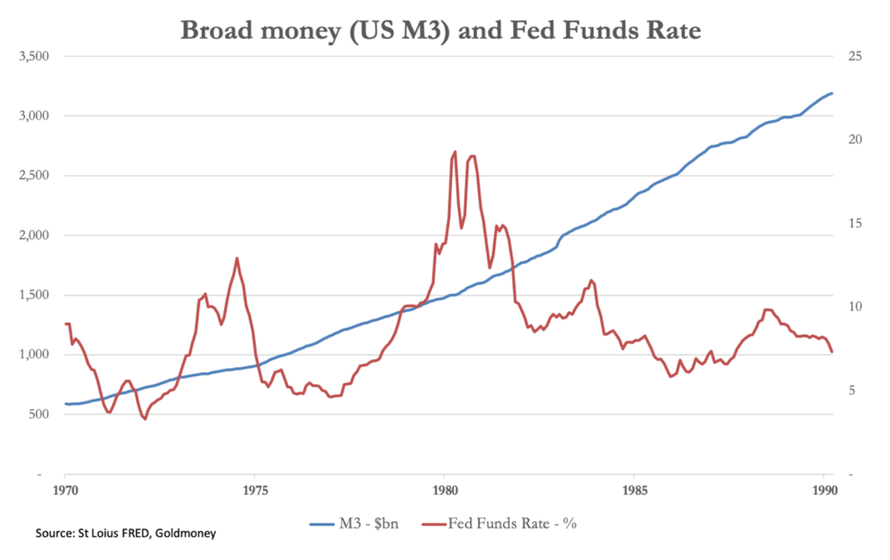

We which is to point out why the underlying

assumption, that interest rates are the cost of money which can be managed with

beneficial results, is plainly wrong. If demand for money and credit can be

regulated by interest rates, then there should be a precisely negative correlation between official interest rates and the

quantity of money and credit outstanding. It is clear from the following chart

that this is not the case.

See Chart:

Broad Money (US M3) and FED Funds Rate

{kind=link}

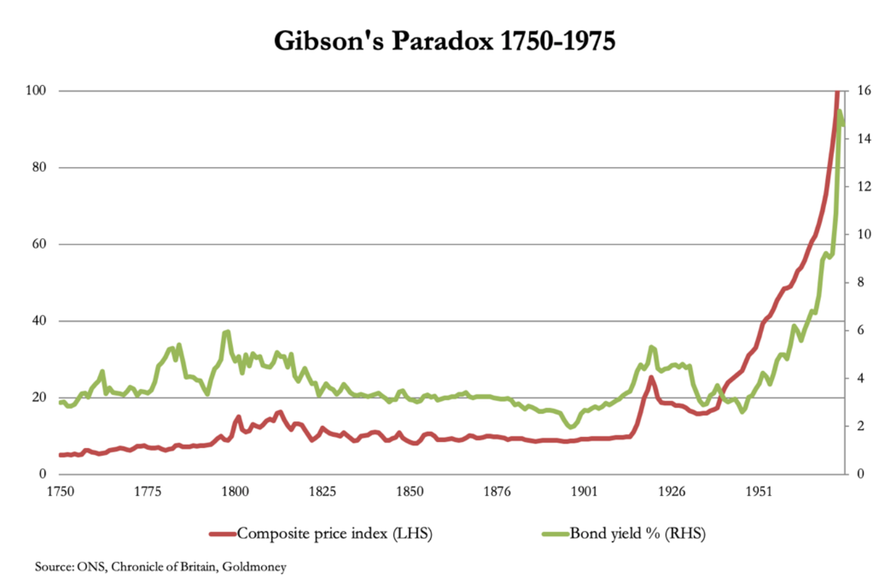

Gibson’s paradox

disproves the efficacy of monetary policy

From the chart above, it is clear that the central

tenet of monetary policy, that the quantity of money can be regulated by

managing interest rates, is not borne out by the results, and therefore the

role of interest rates is not to regulate demand for credit as commonly

supposed. This is confirmed by Gibson’s paradox, which demonstrated that a long-run positive correlation existed between wholesale

borrowing rates and wholesale prices, the exact opposite of that assumed by

modern economists. This is shown in our second chart, covering over two

centuries of British statistics.

See Chart:

Gibson’s Paradox

{kind=link}

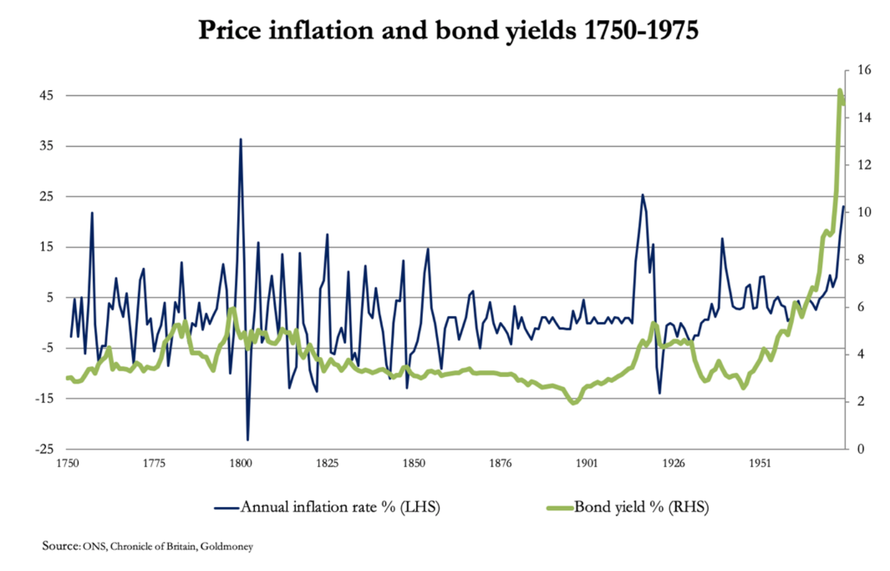

Economists dismissed the contradiction of

Gibson’s paradox because it conflicted with their set view, that interest rates

regulate demand for money and therefore prices[i]. Instead,

it is ignored, but the evidence is clear. Historically,

interest rates have tracked the general price level, not the annual inflation

rate. As a means of managing monetary policy, interest rates and

therefore borrowing costs are ineffective, as confirmed

in our third chart below.

See Chart:

{kind=link}

The only apparent correlation between

borrowing costs and price inflation occurred in the 1970s, when price inflation

took off, and bond and money markets woke up to the collapsing purchasing power

of the currency.

Continue reading at:

----

----

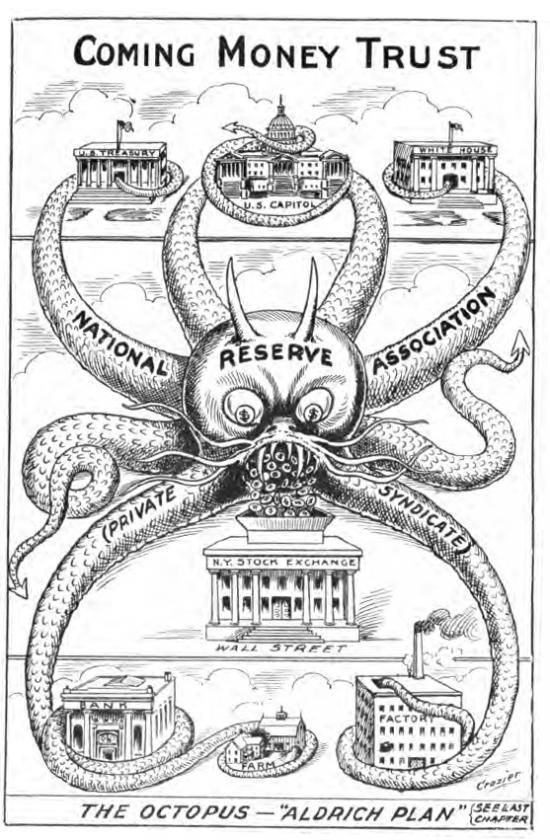

"When

upstarts periodically challenge their dominance, central bankers throw the

economy into recession, bankrupting new money, consolidating and preserving the

existing power structure. That’s how capitalism mixed with democracy and rule

of law works."

See Draft 1:

The Conspirators

{kind=link}

See Draft 2:

Coming Money Trust

{kind=link}

…

----

----

[[ Even main profiteers of the system can't believe that the

US Econ is OK ]]

Markets frequently change their mind, but even adjusting for that, the

shift in ‘conventional wisdom’ in recent months has been nothing short of

whiplash.

Markets frequently

change their mind, but even adjusting for that, the shift in ‘conventional

wisdom’ in recent months has been nothing short of whiplash. In December, there was widespread agreement among

investors that recession risk had risen sharply, that rising inflation

pressures would keep central banks tightening policy, and that US-based risks

around trade and government funding had risen sharply. Skip

forward two months and these fears have been replaced by a different (if

familiar) term: Goldilocks.

See Draft:

https://www.zerohedge.com/s3/files/inline-images/MS%20goldilocks.jpg?itok=eR6mqDqk

The Goldilocks

narrative depends on a lack of inflation, which gives central banks the

opportunity (although not the obligation) to continue accommodative policy. Core inflation readings in developed markets have

moved sideways in recent months, forward-looking inflation expectations have

dropped sharply, and my colleague Chetan Ahya notes that emerging market

inflation currently sits near 15-year lows. Taken

together, investors sound more emboldened that a lack of inflation pressure

means that central banks have nothing but time.

All these

suggest that DM economies are working with significantly less spare capacity

than they were under prior periods when ‘Goldilocks’ reigned. .. And lest one thinks that inflation

provides a true late-cycle warning signal, this is a good time to remember that

core CPI is currently at the same level as May 2007 and higher than

May-December 1999.

But Goldilocks

is about more than a lack of inflation; it also requires enough growth to allay

downside fears. And that’s our

other problem with this argument. Global growth data remain poor.

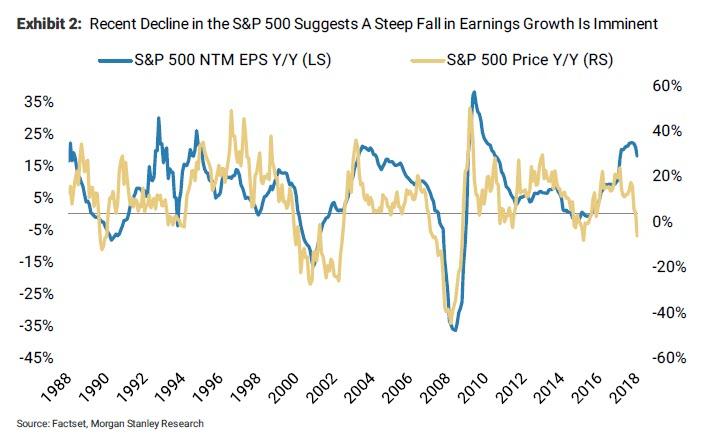

Meanwhile, it’s important

to remember that, for US earnings, the weakness is just beginning. Our US equity

strategists now expect just 1% EPS growth for the entire year, a reminder that

the challenges to the US fundamental story aren’t going away any time soon.

See Chart:

Recent decline in the

S&P500

{kind=link}

In short, we think that

investors should be sceptical of the Goldilocks narrative, and look for

strategies that benefit from inconsistencies within it. Big picture, we are not

looking to add exposure here, and have been looking to reduce some emerging

market beta into strength. Our forecasts for stimulus

that will help China growth stabilise while US growth continues to moderate

support the strategic case to be short the broad USD and overweight

international over US equities, and a bullish view on both A-shares and

the renminbi. On a smaller scale, our rates strategists continue to think that

the level of US real rates is too high relative to expectations that the Fed is now done hiking for the cycle. Either those

expectations of further hikes should come up, or 10-year real rates should come

down.

…

----

----

...the Fed was not birthed from nothing in

1913. The monster was the natural outgrowth of an increasingly troubled banking

system.

The Federal

Reserve’s doors have been open for “business” for one hundred years. In explaining the creation of this money-making

machine (pun intended - the Fed remits nearly $100

bn. in profits each year to Congress) most people fall into one of

two camps

Those inclined to view the

Fed as a helpful institution, fostering financial stability in a world of

error-prone capitalists, explain the creation of the Fed as a natural and

healthy outgrowth of the troubled National Banking System. How helpful the Fed has been is questionable at best, and in

a recent book edited by Joe Salerno and me — The

Fed at One Hundred — various contributors

outline many (though by no means all) of the Fed’s shortcomings over the past

century.

Others, mostly those with

a skeptical view of the Fed, treat its creation as an

exercise in secretive government meddling (as in G. Edward

Griffin’s The

Creature from Jekyll Island) or crony

capitalism run amok (as in Murray Rothbard’s The Case Against the Fed).

Read theses subtitles:

Before

the Fed

Why Did

Clearinghouses Have So Much Power?

Fractional-Reserve

Free Banking and Bust

In conclusion, the Fed was not birthed from nothing in 1913. The monster was

the natural outgrowth of an increasingly troubled banking system

….

----

----

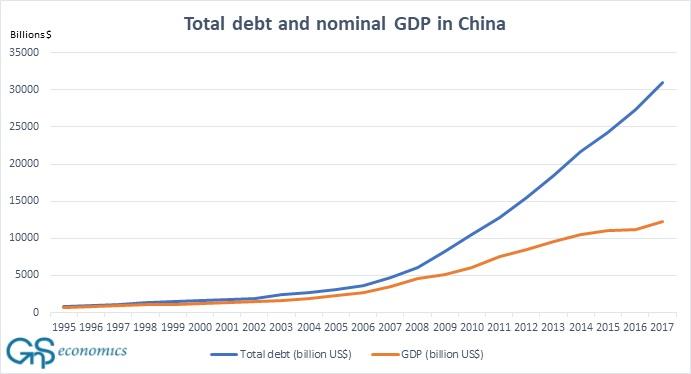

Based on what

has happened in the global economy, one should be extra careful when calling

for more stimulus. It will most likely not benefit the real economy, but it is

likely to propel over-valued asset markets even higher.

See Chart:

Total Debts and Nominal GDP in China

{kind=link}

see more charts at:

….

----

----

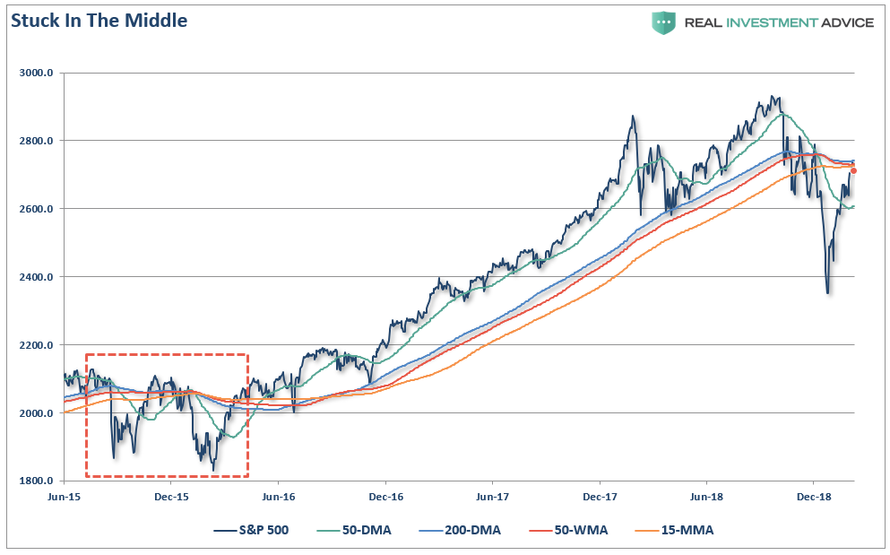

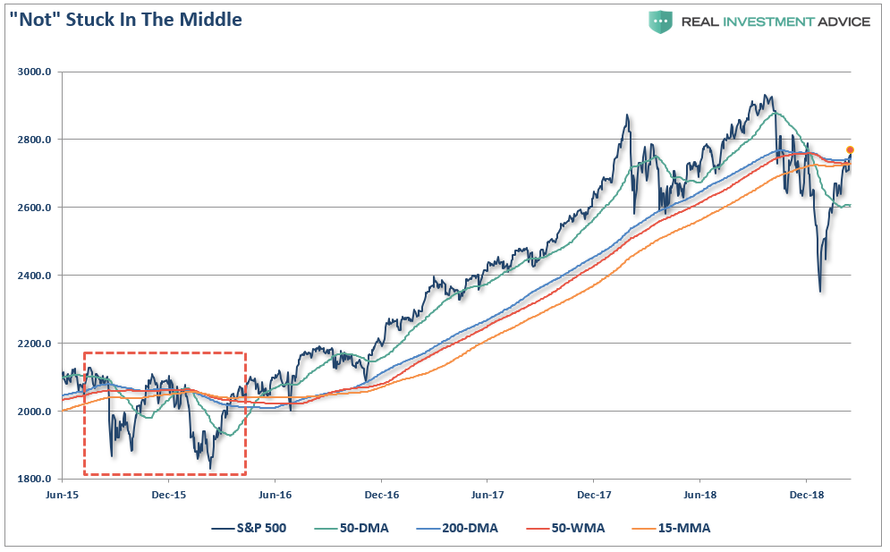

This is a classic “bull trap” in the making which sucks investors in

before inflicting as much pain as possible. Erring to the side of caution, for now, will likely be the right

choice...

See Chart:

Stuck in the middle

{kind=link}

There are two things driving the advance

currently.

The first, is

the Fed.

As we discussed with our RIA PRO subscribers (use code PRO30 for a 30-day free trial) last

week,

“Today, [Cleveland Fed Reserve Governor Loretta Mester] all but put the

kibosh on further rate hikes and, per Mester’s comments, will end balance sheet

reduction (QT) in the months ahead.”

John

Rubino also made an important note in this regard as well.

“Take the

world that we were in over the past five years and flip it upside down. For the Fed, the risk that another rate

increase could cause significant economic harm outweighs the risk that not

raising rates could lead to slightly higher inflation.” – Gennadly

Goldberg, TD Ameritrade.

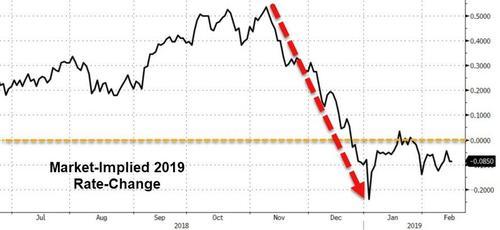

And with that, the odds of a rate “hike” in

2019 have evaporated in favor of a rate “cut.”

See Chart:

{kind=link}

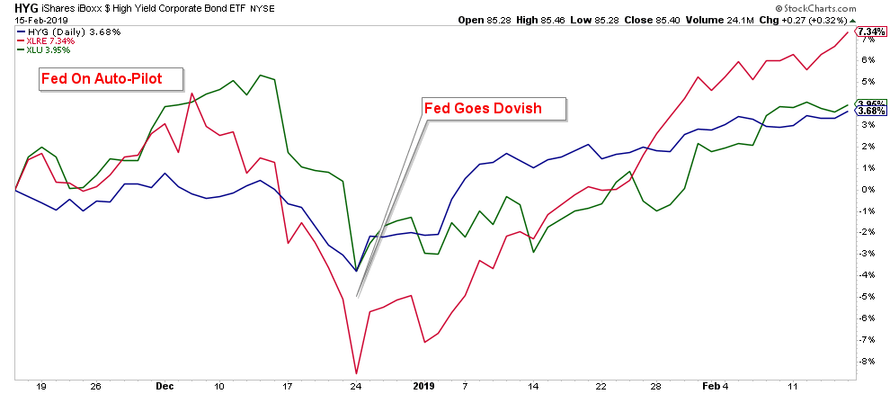

However, the problem for the Fed is that

they have now effectively “boxed” themselves in. As John

notes:

“If caving to the stock market re-energizes

the bond market, leading corporations to increase their already record-high

debt load, that will

boost economic growth while

raising both inflation and commodity/real estate prices – thus forcing the Fed to go back to tightening, thus causing chaos in

the financial markets, thus

forcing the Fed to back off and return to easing. And so on, with each

iteration ratcheting up overall leverage in the economy.”

Opps….Too Late

See Chart:

{kind=link}

The second, is “hope.”

On Friday, on headlines that talks are continuing

with China, the market pushed through those resistance levels as shown

below.

See Chart:

NOT Stuck in the middle

{kind=link}

While there is

nothing wrong with “hoping” for a positive outcome from “trade

talks,” the rush to “buy” equities has

effectively “priced in” the best of all possible outcomes. This leaves investors vulnerable a whole

host of possible disappointments:

- Trade deal isn’t reached as China refuses to give in to demands for economic reform.

- Trade deal is made but the magnitude of concessions is disappointing.

- Trade deal gets extended, again, with no real progress towards a “deal.”

- Trade deal made and tariffs are ended, but such is likely already priced into current asset prices.

- Trade negotiations collapse. (Worst possible outcome.)

The point here is that there are few outcomes for

the trade deal which are extremely optimistic which would support a further

surge in assets prices. The

most likely outcome is this simply a “buy the rumor, sell the news” type

event, and if the news is bad, the resulting sell-off could be substantial.

Market Has

Gotten Way Ahead Of Itself

See Chart:

{kind=link}

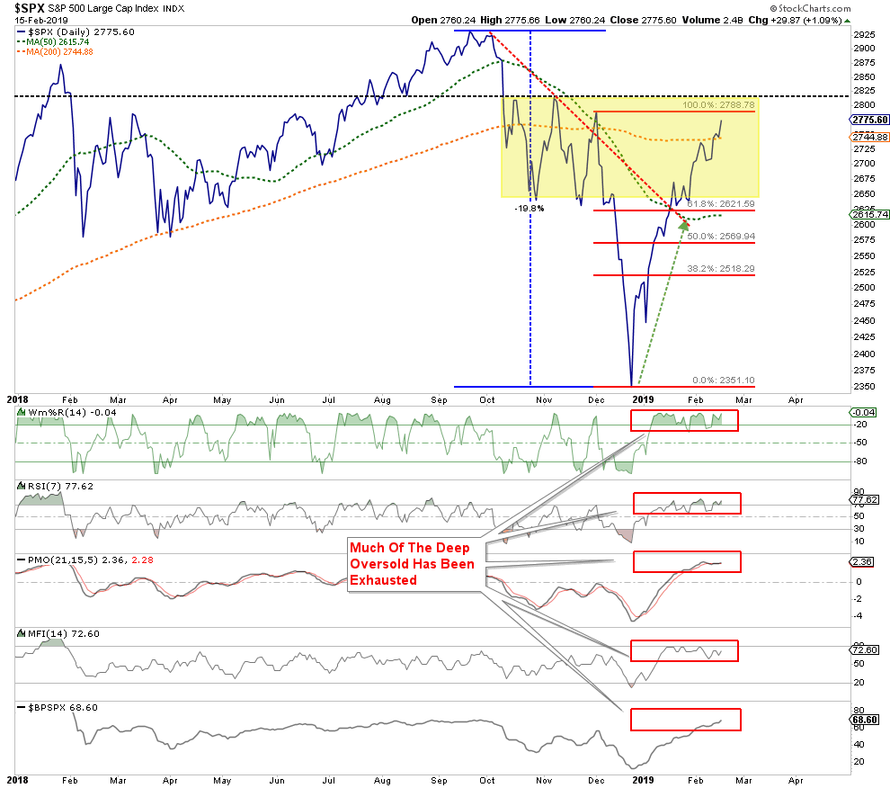

A correction

following that rally SHOULD be highly anticipated.

Read

Level 1 = 38.2%:

Level

2 = 50%:

Level 3 = 61.8%:

This analysis also corresponds to the extremely

rapid reversion of both technical and sentiment measures.

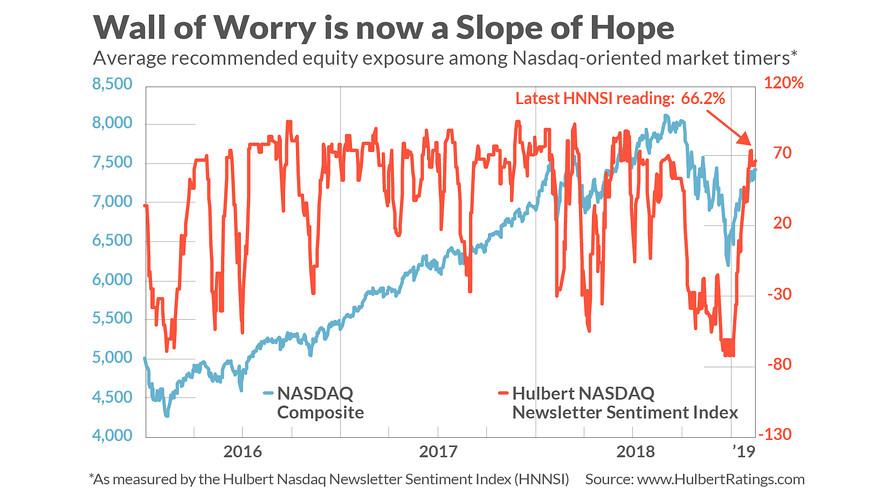

As Mark

Hulbert noted on Friday:

“That’s because the mood has shifted from the extreme pessimism that

prevailed in late December to nearly as extreme optimism today. Some call

current conditions a ‘slope of hope.'”

See Chart:

Wall of worry is now a slope of hope

https://www.zerohedge.com/s3/files/inline-images/MW-HD992_slope__20190214133201_ZH.jpg?itok=YYP8dn8U

{kind=link}

….

----

----

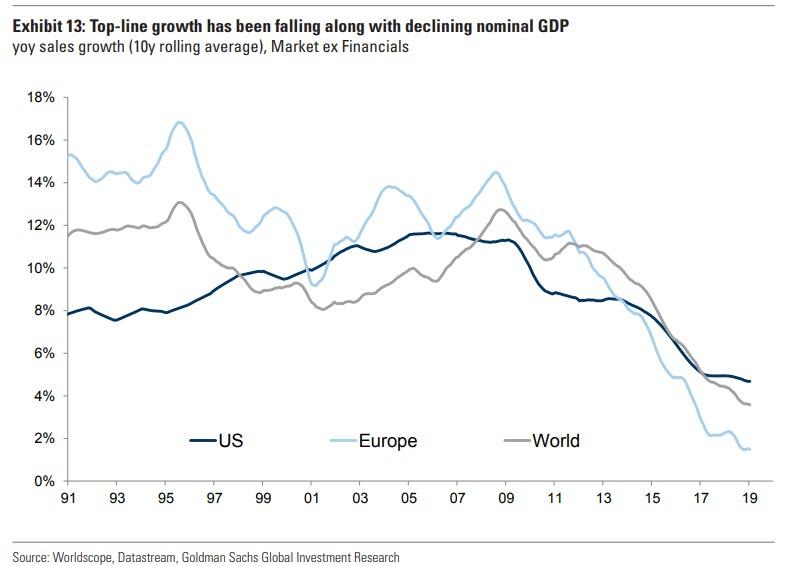

"We now expect a reversion to a period of low-single-digit earnings

growth without the driver of higher valuation, which was a key driver of

returns in recent years."

See Chart:

Top Line growth has being

falling along with declining nominal GDP

{kind=link}

See more interesting

charts at:

…

SOURCE: https://www.zerohedge.com/news/2019-02-17/world-full-zombies-global-revenue-growth-has-collapsed

----

----

the total

amount is twice the amount the U.S. Treasury paid to bail out the auto

industry during the last recession

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full

of frauds & corruption. Urge cambio

False News:

A torrid post-crisis recovery in the NYC housing market came to a

screeching halt last year as a chasm opened up between what sellers were asking

and what buyers were willing to pay.

----

----

Reputed master of the clapback Alexandria Ocasio-Cortez just got a taste

of her own medicine...dished out by Amazon senior vice president for worldwide

operations Dave Clark.

----

----

"He is

going to protect his national emergency declaration, guaranteed..."

----

----

US-World ISSUES (Geo Econ, Geo Pol &

global Wars)

Global depression is on…China, RU, Iran search for

State socialis+K-, D rest in limbo

In the latest

"serious blow" to US efforts to persuade allies to ban the Chinese

supplier from high-speed telecommunications systems, the FT reports that the

British government has concluded that it can "mitigate the risk from using

Huawei equipment in 5G networks."

----

----

TRAMP Theater: TRUMP

TO EUROPE: TAKE BACK 800 ISIS FOREIGN FIGHTERS OR WE'LL BE FORCED TO

RELEASE THEM

They'll

"permeate Europe"...

----

----

More stupid theater: MEASLES

ARE BACK AFTER 900 DEAD IN MADAGASCAR; TIME TO BLAME RUSSIA

"Are

Russian Trolls Saving Measles From

Extinction?"

----

----

Jail’ Business: How much they will pay for Sweden’

comforting hotel ? how much for T?

"I was angry when I read

about how it worked with immigrants and how they avoid punishment for

everything they do. They get acquitted, though they steal and do other things. It is unfair that those who commit gross

crimes can go free..."

----

----

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

----

----

----

IF RU and US Billionaires went out of earth .. that

will be the greatest news in history

----

----

OSCE

Urges Kiev to Contribute to Democracy, Allow Russia to Observe Ukrainian

Presidential Election Neo-nazis are masters

in democ elections? Hi Hitler?

----

----

Le encontraron el culo al mundo? What is next?

----

Now I know what is next: UK

Military to Introduce Swarm Drones ‘By End of the Year

----

Fueron por lana y salieron trasquilados?

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes

& terrorist imperial chaos

REBELION

---

----

Diferencia económica entre hombre y mujer Hedelberto López

----

----

----

----

----

----

----

----

----

RT EN ESPAÑOL

----

----

----

----

----

----

----

----

PARA MAÑANA

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism &

internal conflicts that favor WW3

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

DEMOCRACY NOW

Amy Goodman’s team

----

----

PRESS TV

Resume of Global News described by Iranian

observers..

----

----

----

----

----

----

----

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario