ND FEB 20 19 SIT EC y POL

ND

denounce Global-neoliberal debacle y propone State-Social + Capit-compet in

Econ

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

"Inflation-proxies are on the move", notes Nomura's

Charlie McElligott who posits that "something is happening" in US

equities, highlighting some notable shifts compared to 2018.

See

Chart

Value vs. Growth

{kind=link}

See more INTERESTING

charts at:

----

----

The

market's hopes that today's snow-delayed Fed minutes would resolve the debate

over the fate of the balance sheet unwind, were dashed with the Fed confirming

what traders already knew: the Fed would remain patient, data dependent,

focused on the fading inflation impulse, and would seek a plan for when the

Fed's balance sheet unwind end by the end of 2019 suggesting that the QT may

continue well into 2020 depending on what the Fed concludes is a "sufficient"

amount of bank reserves.

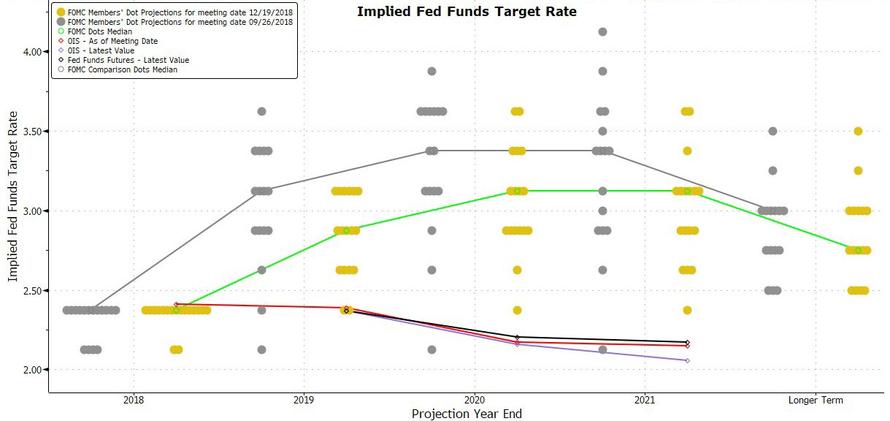

Following the ambivalent minutes, rate hike expectations were

broadly unchanged, with the Fed Funds still pricing in a rate cut in 2020 as

the divergence with the Fed's hawkish dots continues.

See

Chart:

Implied FED Funds target rate

{kind=link}

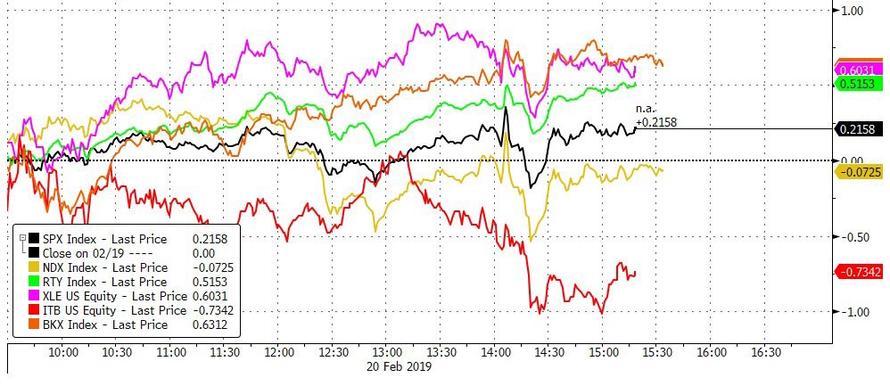

As a result, stocks initially slumped, then rebounded, and traded

modestly in the green, with the nasdaq hugging the flatline, as banks, small

caps and energy stocks outperforming, offset by losses in homebuilders.

See

Chart:

{kind=link}

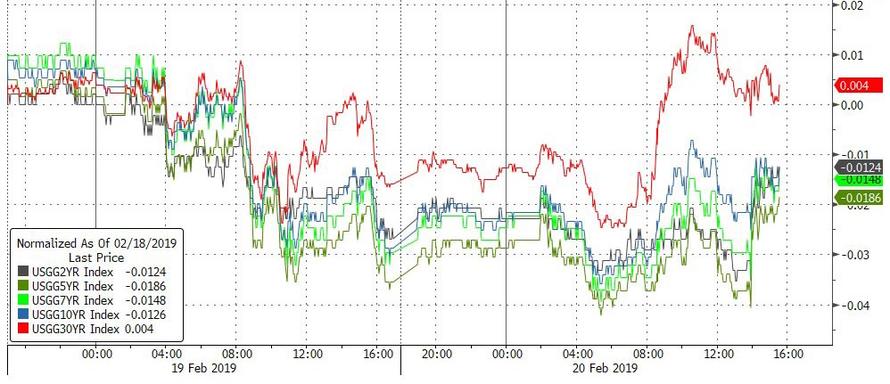

Treasurys were mixed, with the long end taking on water and the

curve initially steepening led by 30Y yields higher, even as the short end and

10Ys were more or less flat for the day...

See

Chart:

{kind=link}

Despite today's modest appetite, the scramble into safe havens

observed in late December remains a distant memory, and the short end continued

to trade about 10bps higher than Fed Funds.

See

Chart:

{kind=link}

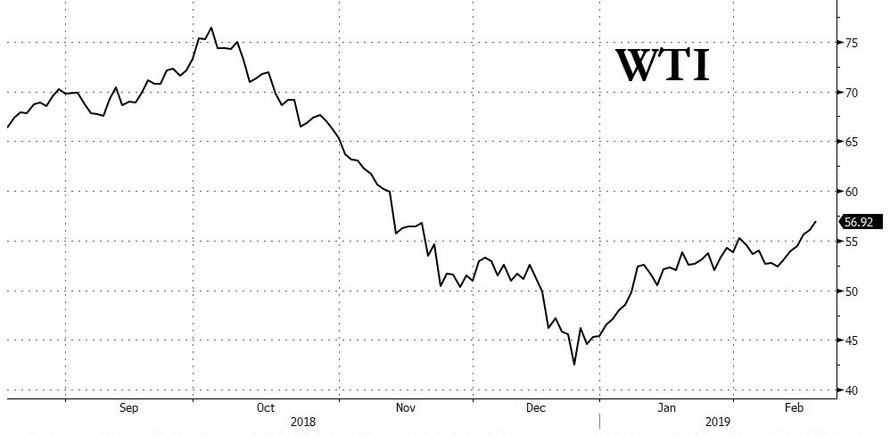

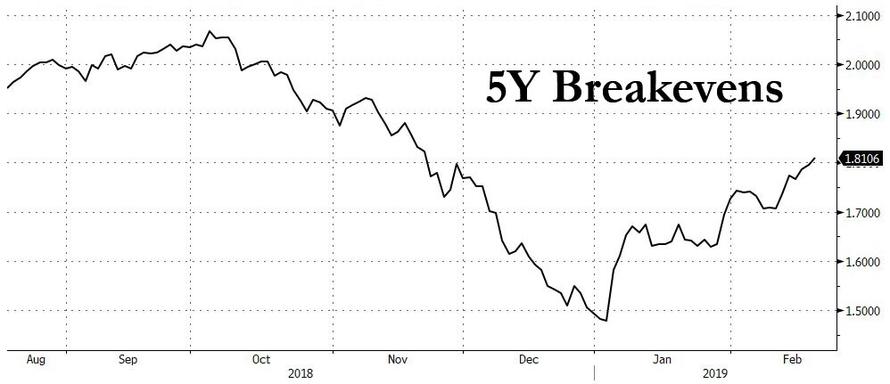

In commodities, WTI crude rose to 2019 highs, up roughly a dollar on

the day...

See

Chart:

{kind=link}

helping to push 5Y breakevens similarly to 2019 highs...

See

Chart:

{kind=link}

And so, with the Minutes coming and going, the critical 2,800 level

in the S&P remains untouched, with the broader index trading about 15

points away, and facing massive resistance to break out above what has now been

called a "quadruple top."

See

Chart:

{kind=link}

When and how the S&P can breach this level remains a question

for another day after today's sleepy, snowy, stock drift.

…

SOURCE: https://www.zerohedge.com/news/2019-02-20/sleepy-stocks-drift-fed-minutes-fail-ignite-buying-boost

----

----

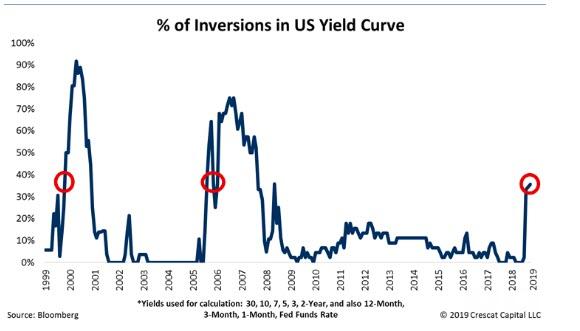

Have the collective curves already sounded the alarm, but everyone

is too focused on a flat 2s/10s curve to hear it?

The

graph below plainly shows that when 2-year Treasury yields exceed 10-year

Treasury yields, otherwise known as “a curve inversion,” a recession has always

followed. Following the inflection point of the

inversion, as circled, the curve steepens through a recession and for some time

afterward.

See

Chart:

2S/

10S Yield Curve

{kind=link}

For those of you that are stubborn and waiting on the curve to go to

zero to sound the recession warnings, we share the graph below, courtesy of

Crescat Capital LLC.

See

Chart:

% of

Invesion in US Yield Curve

{kind=link}

The

graph looks at numerous yield curves and computes the percentage of them that

were inverted at various points of time. Note that about 40% of curves are

currently inverted. Have the

collective curves already sounded the alarm, but everyone is too focused on a

flat 2s/10s curve to hear it?

…

SOURCE:

https://www.zerohedge.com/news/2019-02-20/yesterdays-perfect-recession-warnings-may-be-failing-you

----

----

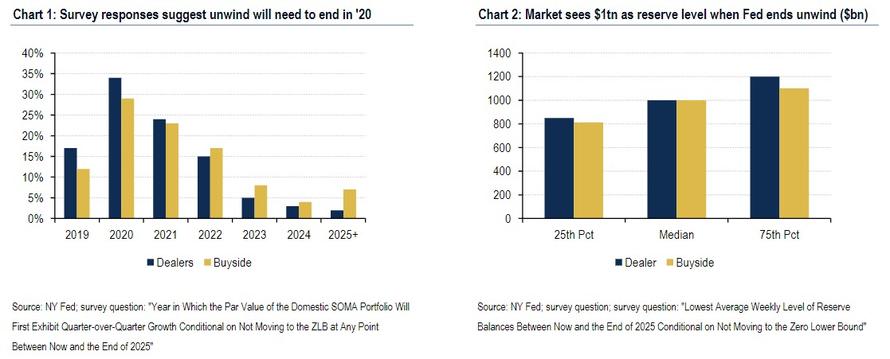

Goldman now expects an announcement at the March meeting that runoff

will stop at the end of Q3.

See

Chart:

Blocked

….

Finally

the punchline: according to Goldman, the Fed will end its balance sheet unwind

before the end of the year, long before primary dealers and the buy side had

expected (which according to the majority, was some

time in 2020).

See

Charts:

Survey

responses suggest unwind will need to

end in 20th

{kind=link}

…

----

----

Did Bloomberg just make a big mistake in its snap take on the Fed

minutes?

READ

THIS:

Key

highlights from a Plan proposal: Focus in 5 issues

1- DOWNSIDE RISKS HAD INCREASED

2 CONTINUED SUSTAINED EXPANSION

3 HOUSEHOLD DATA HAVE BEEN STRONG

4 STRONG LABOR MARKET, INFLATION NEAR TARGET

5 BUSINESS INVESTMENT HAD MODERATED

On the increase in "downside risks": "the decline in

inflation compensation might reflect in large part declines in risk

premiums or increased concerns about downside risks to the outlook for

inflation. This interpretation was seen as consistent with the behavior of

the most recent survey-based measures of expected inflation, which were

little changed."

On inflation expectations,

the Fed appears to be turning more dovish; in fact according to the last

bullet, the Fed may finally be realizing that Japanification is coming:"many participants commented that upward pressures on inflation appeared to be more muted than they appeared to

be last year despite strengthening

labor market conditions and rising input costs for some industries."The upside risk that inflation could

increase more than expected in an economy that was projected to move

further above its potential was

counterbalanced by the downside risk that longer-term inflation

expectations may be lower than was assumed in the staff forecast, as well

as the possibility that the dollar could appreciate if foreign economic

conditions deteriorated."

"In

their discussion of indicators of inflation expectations, participants

noted that market-based measures of inflation compensation had moved lower

in recent months. Participants expressed a range of views in interpreting

the decline in inflation compensation. On the one hand, that decline could

stem from a decrease in expected inflation on the part of market

participants. In that case, the current low levels of

inflation compensation could suggest that inflation expectations are below

the Committee's 2 percent inflation objective."

"A few participants expressed concern that

longer-run inflation expectations may be lower than levels consistent with

the Committee's 2 percent inflation objective. Several participants

judged that risks that could lead to higher-than-expected inflation had

diminished relative to downside risks. The potential that various sources

of uncertainty might abate more quickly than expected was mentioned as a

potential upside risk for the economic outlook."

On the market's influence over the Fed: FOMC communications were reportedly perceived by market participants

as not fully appreciating the implications of tighter financial

conditions and softening global data over recent months for the U.S.

economic outlook

Market

participants pointed

to a number of factors as contributing to the heightened volatility and

sustained declines in risk asset prices and interest rates over recent

months including a weaker outlook and greater uncertainties for foreign

economies (particularly for Europe and China), perceptions of greater

policy risks, and the partial shutdown of the federal government.

Market

participants appeared

to interpret FOMC communications at the time of the December meeting as

not fully appreciating the tightening of financial conditions and the

associated downside risks to the U.S. economic outlook that had emerged

since the fall.

Participants agreed that it

was important to continue to monitor financial market developments and

assess the implications of these developments for the economic outlook.

On the key issue of balance sheet reduction:

- Consistent with recent communications that the FOMC would be flexible in its approach to balance sheet normalization, the survey results also suggested that the respondents anticipated that the Committee would slow the balance sheet runoff in scenarios that involved a reduction in the target range for the federal funds rate.

- Some market reports suggested that investors perceived the FOMC to be insufficiently flexible in its approach to adjusting the path for the federal funds rate or the process for balance sheet normalization participants raised a number of questions about market reports that the Federal Reserve's balance sheet runoff and associated "quantitative tightening" had been an important factor contributing to the selloff in equity markets in the closing months of last year

- some other investors reportedly held firmly to the belief that the runoff of the Federal Reserve's securities holdings was a factor putting significant downward pressure on risky asset prices, and the investment decisions of these investors, particularly in thin market conditions around the year-end, might have had an outsized effect on market prices for a time

On the Fed balance sheet's composition in the future, the Fed appears willing to

shift its MBS holdings to zero:

- "Participants commented that, in light of the Committee's longstanding plan to hold primarily Treasury securities in the long run, it would be appropriate once asset redemptions end to reinvest most, if not all, principal payments received from agency MBS in Treasury securities"

On the dot plot:

- “A few participants expressed concerns that in the current environment of increased uncertainty, the policy rate projections prepared as part of the Summary of Economic Projections (SEP) do not accurately convey the Committee's policy outlook. These participants were concerned that, although the individual participants' projections for the federal funds rate in the SEP reflect their individual views of the appropriate path for the policy rate conditional on the evolution of the economic outlook, at times the public had misinterpreted the median or central tendency of those projections as representing the consensus view of the Committee or as suggesting that policy was on a preset course.”

- “However, some other participants noted that the policy rate projections in the SEP are a valuable component of the overall information provided about the monetary policy outlook.”

And the one section that the market will be mostly focused on: the

Fed is actively contemplating ending QT in the second half: "the staff presented options for substantially slowing

the decline in reserves by ending the reduction in asset holdings at some

point over the latter half of this year and thereafter holding the

size of the SOMA portfolio roughly constant for a time so that the average

level of reserves would fall at a very gradual pace reflecting the trend

growth in other Federal Reserve liabilities."

And this:

- Almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve's asset holdings later this year

Amusingly,

as Bloomberg economics analyst Ben Baris notes, there was a discussion on the

efficacy of the SEP projections, and whether they are conveying a useful

message to the public. Some

participants were concerned that the point estimates were being misinterpreted

as committee members' consensus view on the appropriate policy path -- they are

not. The projections look to be caught up

in the larger discussion of appropriate communication strategies as we hover

near the neutral rate.

….

….

See the full plan and debate at this source:

----

----

Just like in 2016, the Fed shocked markets by its recent dovish

reversal. But - like in 2016 - what can force the Fed to kickstart rate hikes

again, and how will it communicate this decision to the markets? Here are the three key things to watch for.

----

----

US DOMESTIC POLITICS

Seudo

democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge

cambio

And Bernie's donors aren't "millionaihs and billionaihs."

----

----

The bill will raise the state minimum wage incrementally to $9.25 on

Jan. 1, 2020, then to $10 an hour the following July, and it will continue to

increase by $1 a year until 2025...

----

----

US-World ISSUES (Geo Econ, Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

[[ The

FACT IS that we are using US military planes to deliver guns and mercenaries to create violent chaos inside

VEN. Of course VEN Gvt will defend their

sovereignity We Americans are responsible for

whatever happens in VEN ]]

...the opposition would have to pass over "our dead bodies" to

impose a new government...

----

----

China's Foreign Minister said Wednesday

said that China "doesn't engage in competitive currency devaluation"

and reportedly hopes that the US doesn't politicize exchange-rate issues.

----

----

Beijing has poured cold water over expectations of an imminent trade

deal, saying on Wednesday that China will not allow the use of the yuan’s

exchange rate as a bargaining chip to resolve the trade war with the United

States.

----

----

"If the US imposes more tariffs on Chinese products while China

responds with fiercer countermeasures, it would be a catastrophic strike to

global stock markets."

----

----

SPUTNIK and RT SHOWS

GEO-POL

n GEO-ECO ..Focus on neoliberal

expansion via wars & danger of WW3

RELATED:

…

Since US missiles are already surrounding RU & China, as reported in RT, then Tit x Tat

proceeds. The US is creating in VEN the same type

of Nuke apocalypse of 1962 in Cuba. RU

must use the possible US attack on Ven not only to stop US mercenaries’

intervention, but to wipe out all US-NATO

threats to RU-China & to the

whole world PEACE. It is now or never. If RU allows this attack, the

US-NATO will continue doing so &

worse. Now is the time to stop them. IF RU-China don’t

do it, they will be seen as world traitors. “Eres

libre de quedarte en la trinchera y sentarte sobre la bayoneta del fusil, pero si

te veo hacerlo, tu caso no va a una Corte Marcial, seré yo quien te fusile, le

dijo un capitan Bonapartista a un soldado traidor. En buena hora lo dicho: los dos

enfrentaron al enemigo y vencieron”. From: ‘Anécdotas Bonapartistas’. von

Clausewitz

----

----

----

----

RELATED:

another BOL.shit

----

----

----

----

SHOWS RT

----

----

----

----

NOTICIAS IN SPANISH

Lat Am

search f alternatives to neo-fascist regimes & terrorist imperial chaos

REBELION

----

----

Que

hacer en repudio al Imp en tu país?: Piénsalo, Organiza y actúa

----

----

----

----

----

----

----

Que

hacer en repudio al Imp en tu país?: Piénsalo, Organiza y actúa

----

Españ España acaba donde empieza el rey Miguel Pastrana

----

----

----

ALAI ORG

----

----

----

----

----

----

----

----

RT EN ESPAÑOL

----

----

----

----

----

----

----

----

----

INFORMATION CLEARING HOUSE

Deep on

the US political crisis: neofascism & internal conflicts that favor WW3

----

Mapping the American War on Terror By Stephanie Savell

{kind=link}

----

Venezuela Under Washington’s Gun By Paul Craig Roberts

----

Venezuela and the Left By Gabriel Hetland

----

Trump’s Demagoguery Goes Off the Rails By Finian Cunningham

----

A step towards presidential dictatorship By Patrick Martin

----

Women’s Critical Role in Saving the

Environment By Cesar Chelala

----

----

COUNTER PUNCH

Analysis

on US Politics & Geopolitics

Dean Baker Modern

Monetary Theory and Taxing the Rich

----

Michael T. Klare War

With China? It’s Already Under Way

----

Norman Solomon What

the Bernie Sanders 2020 Campaign Means for Progressives

----

Matthew Johnson Why

Protest Trump When We Can Impeach Him?

----

----

GLOBAL RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

----

----

----

----

DEMOCRACY NOW

Amy

Goodman’s team

----

----

PRESS TV

Resume

of Global News described by Iranian observers..

----

----

----

----

----

----

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario