JUNE 20 16

SIT EC y POL

….

HILLARY’ GLUTTONY FOR

MONEY DOESN’T HAVE LIMITS

MAKE MONEY FROM UNDOCUMENTED MIGRANTS JAILED IS HORRIBLE

“93% of the people

who are locked up in the U.S. in order to meet the minimum legal requirements must

be locked up with possible violations of U.S. immigration laws: they are locked in for-profit prisons, which are owned by

corporations that heavily fund a few politicians, including Hillary Clinton

“On 6 October 2015,

Vice News revealed that fact when they headlined “How

Private Prisons Are Profiting from Locking Up US Immigrants”, and showed that Hillary Clinton was by far the top recipient

of funds from Corrections Corporation of America, and that Marco Rubio

was by far the top recipient from the other of the industry’s giants, GEO

Group, and that both candidates had raked in around the

same total amounts from the industry. Furthermore: “The political contributions

are the visible tip of the iceberg of the influence these folks

wield.”

….

….

NOTE: OF COURSE WE ALL

WANT A LADY AS PRESIDENT.. BUT NOT THIS

ONE

WE WILL HAVE IT IN 5

YEAR of EXPERIENCE WITH SANDERS’ ADMINISTRATION

JILL STEIN and ELIZABETH WARREN WILL BE READY TO TAKE THAT

JOB

----

----

ZERO HEDGE

ECONOMICS

In a DB note over the

weekend titled the "Illusory Benefits of Cheap Money" the

author Oleg Melentyeb turns his attention to relative performance in broad

equity benchmarks. Surely, Oleg writes, "easy monetary policy now coupled

with direct involvement by central banks in pushing down the price of credit

risk, equity performance distribution must be in direct proportion to those

efforts." He finds something unexpected: "Wrong, the answer is exactly the opposite."

To prove that he

shows the charts below which depict relative performance of US, EU, and Japan

broad equity benchmarks against the MSCI World index (MXWO) since Jan 2008. The

timeframe here was chosen to fully capture the period of extraordinary central

bank activity around the globe.

DB's conclusion:

if the central banks behind extreme policy measures have

little to show for the risk they have taken on their balance sheet to this

point, and the pressures they have subjected their savers and financial

institutions to, why should we expect such actions to be extended much further

into the future? Any benefit of additional central bank accommodation appears

to have been largely exhausted at this point in the cycle.

If that is indeed the case, it is much more likely that a

year from now we would see those programs on their way to curtailment rather

than further expansion. Fundamentals would once again prevail over technicals,

just as they always do over time. Recent market moves suggest investors are

beginning to position themselves accordingly in anticipation of such an

outcome.

----

----

IMAGINE... WHAT IF

SND THEN IMAGE WHAT MIGHT HAPPEN NEXT...

1- Imagine the collapse of an extended

speculative tech bubble, resulting in a broad economic recession.

2- Imagine that investors found the

higher yields they sought in mortgage securities, which had historically

always been safe, and that Fed policy inadvertently created voracious demand

for more of that debt.

3- Imagine that this Fed-induced

yield-seeking speculation changed the dynamics of the housing market,

and produced a bubble in home prices, coupled with overbuilding and

malinvestment.

4- Imagine that this

second speculative bubble collapsed anyway, producing the worst economic downturn since the Great Depression, and

that persistent easing by the Fed failed to stop any of it, just as it failed

to do so during the preceding collapse.

5- Imagine that the Fed violated the existing provisions of section 13.3 of the Federal

Reserve Act (later rewritten by Congress to spell it out like a children’s book)

and created off-balance sheet shell companies called “Maiden Lane” to take bad

assets off of the ledgers of certain financial institutions, in order to

protect the bondholders of those companies and facilitate their acquisition by

purchasers.

6- Imagine that the crisis continued, and that what

actually ended the crisis was a change in FASB

accounting rules in the second week of March 2009, which relieved the need for

financial institutions to mark their distressed assets to market value, and

instead allowed them “significant judgment” in valuing those assets, instantly

removing the specter of widespread financial insolvencies with the stroke of a

pen.

7-Imagine that legislation following the crisis was heavy on

paper regulation, signed assurances, and living-wills, but was light on

capital requirements, and contained provisions

that essentially tied the hands of the FDIC and instead gave veto power to the

Treasury and the best friend of the banking system, the Federal Reserve Board

itself, in deciding whether a “too-big-to-fail” bank would actually go into

receivership (where bondholders often lose money, but depositors are protected)

if it was to become insolvent.

8-Imagine that in response to the

collapse of a yield-seeking mortgage bubble, a resulting global

financial crisis, and a 55% collapse in the S&P 500, the Federal Reserve

insisted on pursuing more of what created the bubble in the first place;

refusing to admit the weak cause-and-effect relationship between monetary

easing and the real economy, pushing interest rates to zero, and expanding the

monetary base to the point where $4 trillion of

zero-interest hot potatoes constantly had to be held by someone in

the financial markets.

9- Imagine that

despite pursuing this experimentation for years, the response of the

real economy was no

different than could have been predicted using prior values of non-monetary

variables alone.

10-Imagine that the main effect of this unprecedented intervention

was to drive the most reliable measures of stock market valuation (those best

correlated across history with actual subsequent 10-12 year market returns) well beyond double

their historical norms, and that it prompted massive issuance of low-grade, “covenant

lite” debt, in much the same way yield-seeking speculation encouraged the

issuance of low-grade mortgage debt in the preceding bubble.

11 Imagine that

the Fed not only refused to take serious account of the distorting impact of

yield-seeking speculation

on the financial markets, but actually welcomed it, citing it as an example of

the “effectiveness” of quantitative easing, in the appallingly misguided belief

that “wealth” is inherent in the price you pay for a security, rather than in

the long-term stream of cash flows that the security will deliver over time. Imagine

that investors adopted the same overconfidence in a

Fed “put option” that they held before the 2000-2002 and 2007-2009 market

collapses.

12-Imagine the Fed failed to take any steps at all to reduce

the size of its balance sheet at historically low interest rates, and

painted itself into a corner because despite the weak relationship between

short-term interest rates and the real economy, any normalization of policy

threatened to burst a bubble that was already at a precipice.

13-Imagine that as a result of a

massive combined deficit in the government and household sectors after

the housing collapse, corporate profit margins temporarily soared to the

highest level in history (an implication of the

saving-investment identity under assumptions that typically hold in U.S. data).

14- Imagine that because of this temporary elevation of

profit margins, many of the borrowers that issued debt most heavily

during this yield-seeking bubble were companies with elevated short-term

profitability, but more fragile prospects over the full economic cycle.

15- Imagine that energy and mining companies were among these,

but were only the tip of the iceberg, exposed sooner than the rest because of

early weakness in commodity prices.

16- Imagine the collapse of an

extended speculative tech bubble, resulting in a broad economic

recession. Imagine if the Federal

Reserve had persistently slashed short-term interest rates during the downturn,

to no avail, leaving rates at just 1% by the time the S&P 500 had lost half

of its value and the Nasdaq 100 collapsed by 83%.

17 Imagine that the Fed kept rates suppressed, in the

initially well-meaning hope of encouraging lending, growth and employment.

Imagine that the depressed level of interest rates made investors feel starved

for yield, and drove them to look for safe alternatives to Treasury bills.

18 Imagine that

investors found the higher yields they sought in mortgage securities, which had historically always been safe,

and that Fed policy inadvertently created voracious demand for more of that

debt.

19- Imagine Wall Street had weak enough requirements on

capital and underwriting standards that financial institutions had an

incentive to create more “product” by lending to borrowers with lower and lower

creditworthiness.

20-Imagine that by the magic of “financial engineering” and

lax oversight of credit ratings, Wall Street could pass these mortgages off to

investors either directly by bundling, slicing and dicing them into

mortgage-backed securities or by piggy-backing on the good faith and credit of

the government by transferring them to Fannie Mae and Freddie Mac in return for

funds obtained from investors in these “agency” securities.

21- Imagine that this Fed-induced

yield-seeking speculation changed the dynamics of the housing market,

and produced a bubble in home prices, coupled with overbuilding and

malinvestment.

22- Imagine that the

Federal Reserve, focused exclusively on exploiting the very weak links

between monetary policy and its “mandates” of employment and price stability,

ignored the phrase

“long-run” in those mandates, and wholly disregarded the speculative effects of

its actions, which any thoughtful central banker should have viewed as a

significant risk to the long-run economic health of the nation.

23-Imagine that the

then-head of the San Francisco Federal Reserve, Janet Yellen, answered

questions about 1) whether speculative risks existed, 2) whether the Fed had

any role in addressing them, and 3) whether there was any doubt that the Fed

could halt a resulting economic downturn if it occurred, responding with a

dismissive “No, No, and No.”

24 Imagine that this second

speculative bubble collapsed anyway, producing the worst economic

downturn since the Great Depression, and that persistent easing by the Fed

failed to stop any of it, just as it failed to do so during the preceding

collapse.

There are many more imaginations

Now imagine what might happen next.

A side-note. Though I

was one of the few market participants who correctly anticipated the tech and

housing collapses (also adopting a constructive or aggressive investment

outlook following every bear market decline in three decades as a professional

investor, and navigating complete market cycles admirably over that span), I

regularly acknowledge that my 2009 insistence on stress-testing our discipline

against Depression-era data, coupled with a Fed policy focused on intentionally

encouraging financial speculation, inadvertently created an Achilles Heel for

us in the advancing portion of this market cycle. We addressed those challenges

in mid-2014. See the “Box” in The Next Big Short for

the complete narrative.

A few charts

Some of the following charts have appeared in prior

market commentaries, but are presented again below to provide a graphic

overview of the current situation.

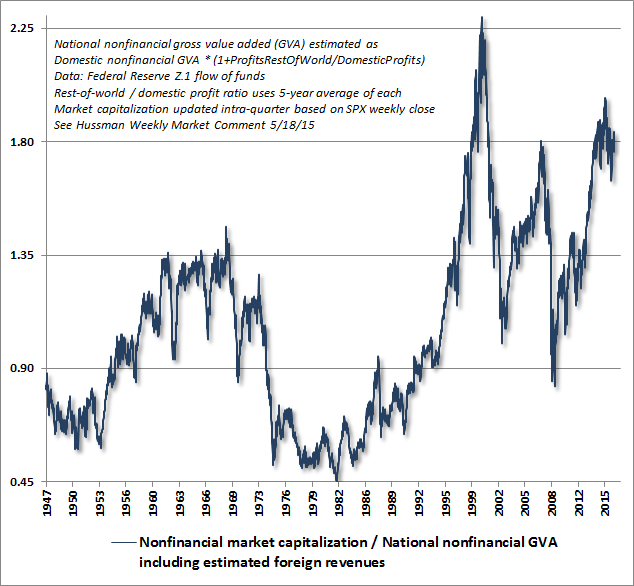

That said, MarketCap/GVA, shown below, has a stronger

correlation across history with actual subsequent S&P 500 total

returns than any of a score of alternative measures we’ve examined, including

the Fed Model, price/earnings, price/forward operating earnings, the Shiller

CAPE, Siegel’s NIPA CAPE, Tobin’s Q, price/dividend, and numerous other

metrics.

SEE BIG IMAGE AT: http://www.hussmanfunds.com/wmc/wmc160620a.png

{kind=link}

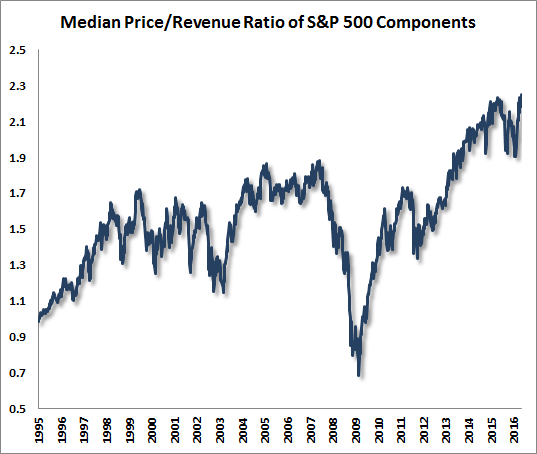

Finally, the chart below shows the median

price/revenue ratio of S&P 500 component stocks, which recently pushed to

the highest level in history, exceeding both the 2000 and 2007 market peaks.

This dispersion has created a headwind for hedged-equity

strategies in U.S. stocks, particularly value-conscious strategies, but investors

should understand that beneath the surface of this short-term outcome is

singularly the most extreme point of overvaluation for the median stock in

history.

GRAPHIC LOCATION AT http://www.hussmanfunds.com/wmc/wmc160620g.png

{kind=link}

----

----

POLITICS

For those concerned

that there may be a conflict of interest for US Attorney General Loretta Lynch

as it relates to the Clinton investigation, you can rest at ease. On Sunday,

Lynch promised that there is no conflict of interest, period. In an

interview with Fox News Sunday, Lynch told Chris Wallace that there is nothing

to worry about, even if her boss is openly campaigning

for Clinton to become the next president of the United States.

----

----

----

ME & WORLD ISSUES

U.S. and Russian fighter jets bloodlessly tangled in the

air over Syria on June 16 as the American pilots tried and failed to stop the

Russians from bombing U.S.-backed rebels in southern Syria near the border with

Jordan. The aerial close encounter underscores just how chaotic Syria’s skies

have become as Russia and the U.S.-led coalition work at cross-purposes, each

dropping bombs in support of separate factions in the five-year-old civil war.

----

----

As

we warned last week was likely, Nigeria's decision to throw in the towel

on maintaining its currency peg has resulted in a collapse in the Naira.

Ending a 16-month-long effort to 'fix' its currency, Nigeria's shift to a free

float has resulted in a 30% crash in the currency as the central bank began

auctioning dollars to try and clear backlogs of orders for hard currency.

However, as the forward market suggests, the pain is far from over as the

hyperinflationary endgame remains more than likely

----

----

- "My 60 years

of experience tells me the pound will plummet, along with your living

standards. The only winners will be speculators" - George Soros

- "All the evidence shows that Brexit would be a disaster" - Jacob Rothschild

- "You cannot in the end protect people from the economic shock that leaving the EU would bring about." - George Osborne

- "All the evidence shows that Brexit would be a disaster" - Jacob Rothschild

- "You cannot in the end protect people from the economic shock that leaving the EU would bring about." - George Osborne

----

----

Mises argues that whenever the state meddles with the free

market, it reduces the standard of living that had prevailed prior to

any state intervention. Essentially, a Brexit will remove another layer of

government intervention from the lives of Brits, and therefore there shouldn’t be any fear of a Brexit. On the

contrary. A Brexit may hold the key to make Europe abandon a doomed course,

bringing it to its senses and back onto the road of freedom and prosperity.

DEMOCRACY NOW

----

----

----

----

----

GLOBAL RESEARCH

By Patrick Martin Global Research, June 20, 2016

----

----

Dirty

“Progressive” Politics, Liberals and “Leftists” for Hillary Clinton. Voters’

only “Rational Choice”: Oppose Both Candidates By Stephen Lendman, Global

Research, June 20, 2016

----

----

COUNTER PUNCH

----

----

Michael Barker Are

You a Racist? Take the EU Test

----

Elliot Sperber The

World is a Gas Chamber

----

Kathy Kelly Why Go To

Russia?

----

----

INFORMATION CLEARING HOUSE

Western officials “pull the wool over [their news outlets]

eyes,” who in turn misinform their audiences.

----

If You

Value Life, Wake Up! By Paul

Craig Roberts

The crazed, insane, nazified, neoconized government in

Washington, is driving the world to extinction in nuclear war

----

The State

Department’s Collective Madness. By Robert Parry

These hawks are so eager for more war that they don’t mind

risking a direct conflict with Russia.

----

Imprison people and exploit them for cheap labor — often at

50 cents an hour or less.

----

The US Is

Sleepwalking Towards A Nuclear Confrontation By Dmitry Orlov

Chris interview Dmitry Orlov this week about the potential

likelihood for actual direct conflict to break out between the world powers

----

Before Omar

Mateen Committed Mass Murder, The FBI Tried To 'Lure' Him Into A Terror Plot

By Max Blumenthal, Sarah Lazare

By Max Blumenthal, Sarah Lazare

The FBI dispatched an informant to "lure Omar into some

kind of act and Omar did not bite."

----

----

RT SHOWS

On

contact Kshama

Sawant: How to counter establishment politics Kshama Sawant, the only socialist on the

Seattle City Council. RT Correspondent Anya Parampil reports on the obstacles

third party...

----

Keiser Report Episode

929 Max and Stacy discuss

Ronald Reagan’s warning that inflation is as ‘violent as a mugger, as

frightening as an armed robber and as deadly as a hit man,’ yet forgetting to

warn us that so were...

----

----

----

----

WASHINGTON BLOG

U.S.

Study Finds Immigrants Imprisoned to Boost Prison-Corporation Profits Posted on June 20, 2016 by Eric Zuesse.

93% of the people who

are locked up in the U.S. in order to meet the minimum legal requirements for

the number of people who must be locked up on possible violations of U.S.

immigration laws, are locked in for-profit prisons,

which are owned by corporations that heavily fund a few politicians, including Hillary Clinton.

That 93% finding was

published on June 20th, in a study by the Center for Constitutional Rights,

titled, “Banking

on Detention: Local Lockup Quotas and the Immigrant Dragnet”.

On 28 April 2015, the

Washington Post published an article, “How for-profit

prisons have become the biggest lobby no one is talking about: Sen. Marco

Rubio is one of the biggest beneficiaries.” It failed to include one crucial

fact: Hillary Clinton is the other.

On 6 October 2015,

Vice News revealed that fact when they headlined “How

Private Prisons Are Profiting from Locking Up US Immigrants”, and showed that Hillary Clinton was by far the top recipient

of funds from Corrections Corporation of America, and that Marco Rubio

was by far the top recipient from the other of the industry’s giants, GEO

Group, and that both candidates had raked in around the same total amounts from

the industry. Furthermore: “The political contributions

are the visible tip of the iceberg of the influence these folks

wield.”

----

----

By Paul Craig Roberts

Great Danger: US-NATO Missiles

Threatening Russia.

For a number of years

I have been warning that the recklessness of a half century ago has reappeared

in spades. The crazed, insane, nazified, neoconized government in Washington

and Washington’s despicable Europeran vassal states, especially the UK,

Germany, and France, are driving the world to extinction in nuclear war. See,

for example, http://www.paulcraigroberts.org/2013/12/14/washington-drives-world-toward-war-paul-craig-roberts

⇒ Keep Reading

⇒ Keep Reading

----

----

NOTICIAS IN SPANISH

----

----

La crisis venezolana y la narrativa

neoliberal. Steve Ellner

----

----

Mujeres condenadas por las

religiones Marcelo Colussi

----

----

Perú. #KeikoNoVa Yorka Gamarra. Ya fue y perdio .. por que pelar gallina?

----

----

US Sanders convoca simpatizantes a continuar

revolución política David Brooks http://www.jornada.unam.mx/2016/06/17/mundo/025n2mun

----

----

----

----

----

----

----

----

----

----

----

----

----

----

----

Keiser

report Por qué US. es "excelente caldo

de cultivo para una insurrección" VIDEO: Keiser Report

en español: Políticas mortales (E929)

URL https://youtu.be/-PO8Pcsd7jw

----

----

----

PRESS TV

----

----

----

----

----

----

----

----

----

----

----

----

I got the impression

that Erdogan is going to be wiped out first

----

===

No hay comentarios:

Publicar un comentario