ND

JUL 18 19 SIT

EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

REALITY BEHIND PROSPERITY: Lower, Longer More

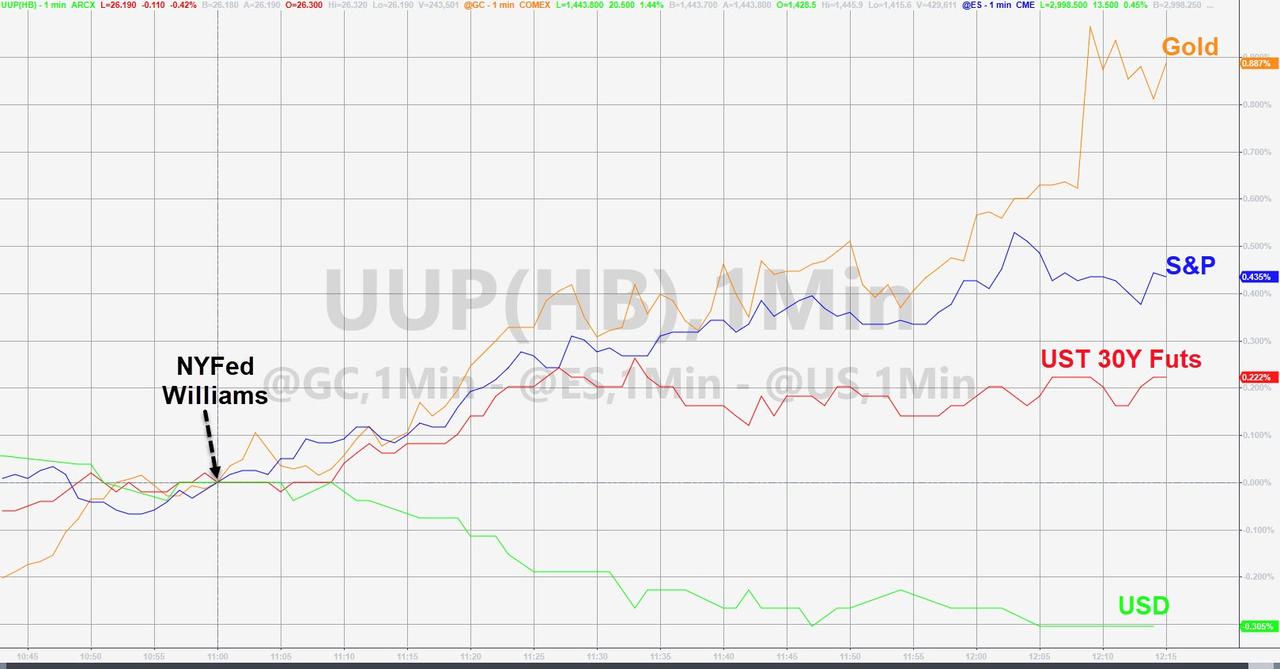

NYFed Williams basically

implied ZIRP is coming back and soon and

that sent the market's

expectations for July rate cuts soaring (50bps now at 65%!)...

See Chart:

July

Rate-Cot Odds

{kind=link}

2019 rate-change expectations now

back above 50bps...

See Chart:

{kind=link}

Piling on, Fed's Clarida added

that research suggests acting

preemptively when rates are low.

Gold, Bonds, & Stocks soared as

the dollar dumped...

See Chart:

{kind=link}

Seriously!! At record high stock

prices!!!!

And all of that silliness sent

stocks soaring... The Dow scrambled back to unchanged at the bell

See Chart:

{kind=link}

S&P 500 desperately pushed

higher to try and regain 3,000...

See Chart:

{kind=link}

Trannies were tempestuous this week

but remain entirely decoupled from global growth...

See Chart:

{kind=link}

Stocks and bonds remain drastically

decoupled...

See Chart:

{kind=link}

Treasury yields tumbled after Fed's

Williams comments..

See Chart:

{kind=link}

The (3m10Y) yield curve was

steepening intraday (heading back towards 0) until Williams spoke...

See Chart:

{kind=link}

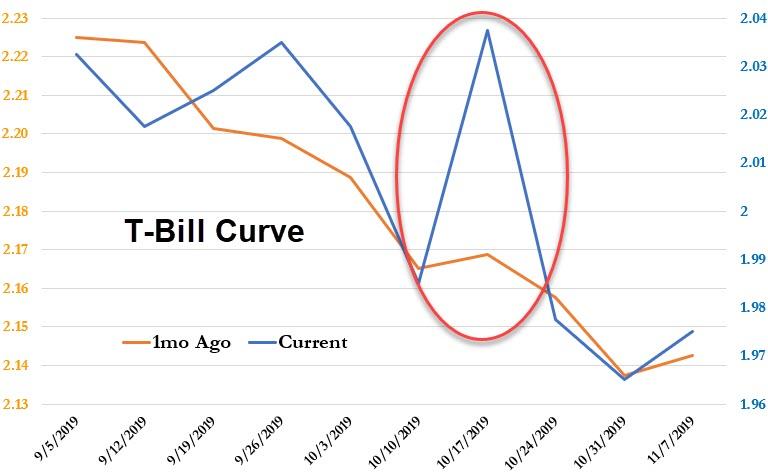

Debt Ceiling Anxiety is building

fast in the Bills curve...

See Chart

T-Bill Curve: Neoliberal crash/collapse is close

{kind=link}

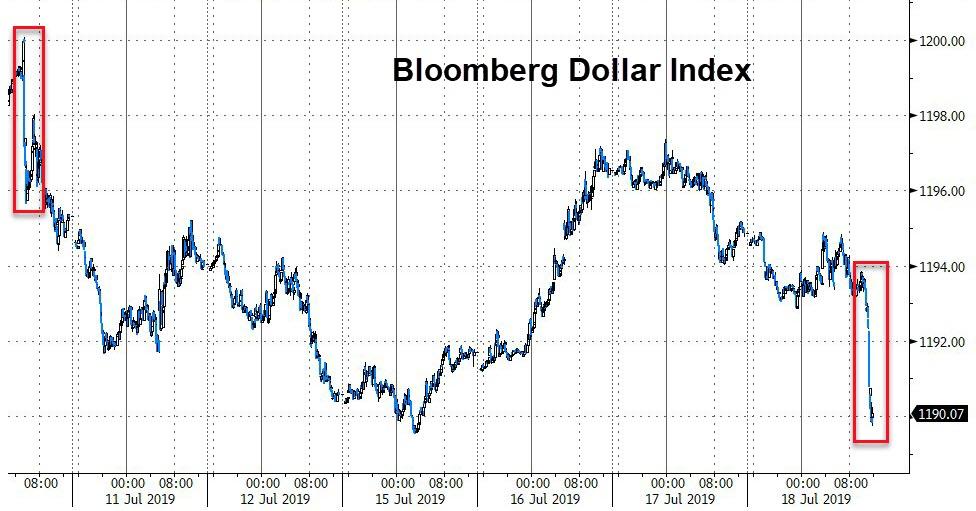

The Dollar collapsed after Fed's

Williams ZIRP comments...

See Chart:

{kind=link}

Yuan spiked...

After more ugliness overnight,

Cryptos surged today...

With Bitcoin blasting back above

$10k...

Silver extended its huge week as

CRUDE CRASHED...

Gold surged on Williams comments...

WTI continued its rapid decline,

accelerating further on Iran nuclear deal headlines...

See Chart:

{kind=link}

HY Energy credit has widened

dramatically...

Oil's slide has been largely ignored

by stocks...

Finally, what do you want to hold

here? Stocks or Silver?

See Chart:

Stocks/Silver (Russel 3000 TR/Spot

Silver

{kind=link}

And as far as the ridiculous spike in Philly Fed (the

biggest jump in a decade), Gluskin-Sheff's David Rosenberg clarifies:

Philly Fed should get its story

straight. The index soared but Beige Book said "manufacturers reported

slight growth in activity - a slower pace than in the prior period" and

"...expectations of activity over the next six

months changed little and remained subdued."

Trade accordingly…

See Chart:

{kind=link}

….

----

----

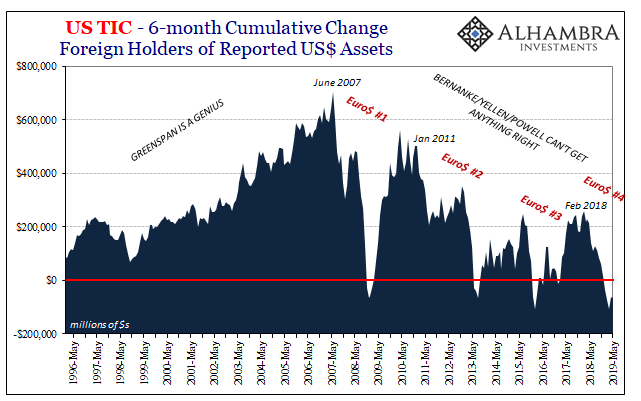

...selling UST’s is an act

of geopolitical defiance rather than the sustained monetary incompetencewhich,

when truly discovered, will actually point the world in the direction of actual

rather than imagined recovery. The

final false dawn.

See Chart:

US TIC -6 Months Cumulative Change

foreign holders of Reported US $ Assets

{kind=link}

----

----

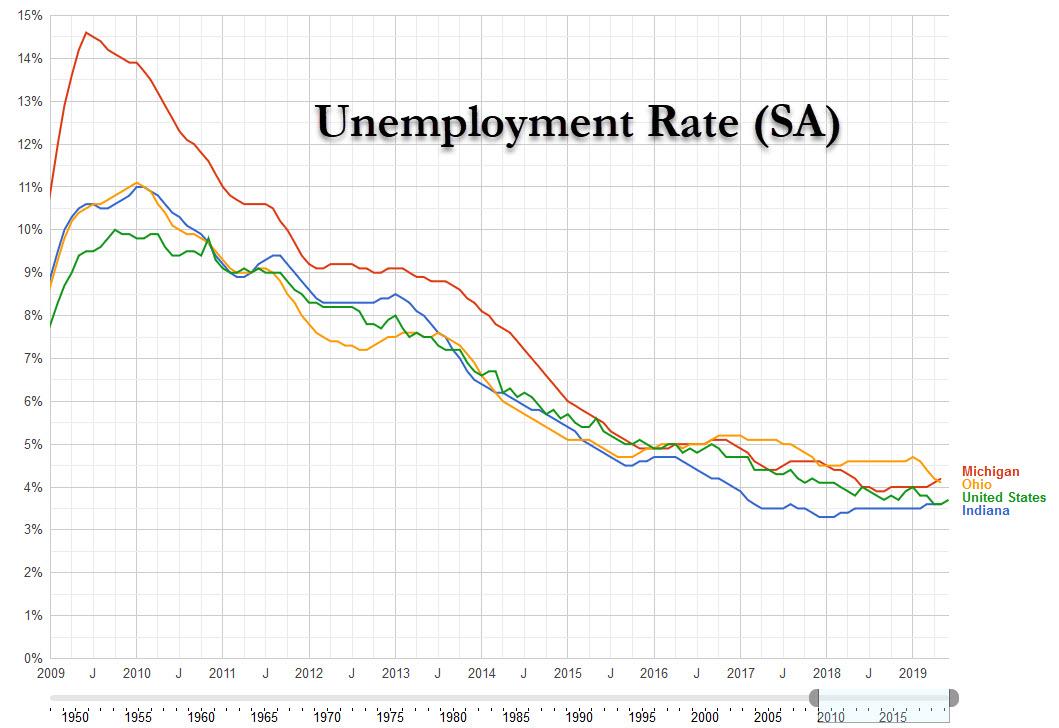

The next US recession (or

“epidemic”) will start with a pullback (“outbreak”) in

manufacturing, since that’s the most important growth driver for the

economies of MICHIGAN, OHIO AND INDIANA.

As for where the

next recession will begin, the data points to one 3-state area: Michigan, Ohio and Indiana. Here is how we

come to that conclusion:

- All 3 states were especially hard hit during the Great Recession, with unemployment rates anywhere from 0.6 – 4.1 points higher than the national average. This fits the pattern of our historical examples noted above.

- Now, unemployment rates in MI, OH and IN are either equal to the national reading (IN) or within 0.3 points (MI and OH). While not yet below the countrywide unemployment rate, all 3 states are experiencing far lower joblessness than the 2000s cycle.

- Also, workers in these states have lower-than-average educational attainment. According to the US Census Bureau, Michigan ranks 34th in the US for the percent of inhabitants with a 4-year college degree. Ohio is 34th and Indiana is 43rd.

- That these states are seeing a better labor market with less-educated workers fits well with the national numbers; the only real slack left in the system is in this cohort.

- Chart of these 3 states versus the national unemployment rate below (link):

See Chart:

Unemployment Rate (SA)

{kind=link}

Summary point: by this reckoning the next US recession (or “epidemic”) will

start with a pullback (“outbreak”) in manufacturing, since that’s the most

important growth driver for the economies of Michigan, Ohio and Indiana. Viewed through this epidemiological lens, the

Federal Reserve’s desire to essentially inoculate the region with lower

interest rates at least fits the paradigm.

Other

sources: US educational

attainment by state.

….

SOURCE: https://www.zerohedge.com/news/2019-07-18/where-next-recession-will-start-epidemiological-study

----

----

"Both global and U.S.

economic conditions had been unusual this year, to say the least,

and have impacted our volumes. You see it every week..."

“We expect solid cost side execution from CSX but weaker markets are a meaningful headwind to

both EPS performance and the stock,” Landy said.

In case you need a point of

reference: U.S. GDP is generally viewed to have grown by 2% in the second

quarter. Judging by

CSX’s results, that’s not a real number.

–Yahoo

The economy has been acting odd for

over a year now.

See Chart:

{kind=link}

The

Federal Reserve will likely cut interest rates during an economic expansion, the United States government is running historically high

deficits while unemployment is at low levels.

There is something else going on below the surface we aren’t

being told about, and yet we’re just expected to believe the mainstream media when they say things

are going great.

….

SOURCE: https://www.zerohedge.com/news/2019-07-18/railroad-ceo-economy-most-puzzling-my-40-year-career

----

----

...negative rates must eventually

destroy the long-term savings industry run by pension funds, banks

and insurance firms.

Back in May 2016, an institutional investor bought a

five-year zero coupon bund at €103. Five years on, the bond will be repaid at

€100, generating a loss of €3. How this loss appears will depend on the type of

investor in question:

- Pension fund. The €3 loss will reduce the market value of assets by €3. Holland also has a rule that pension funds must buy more government bonds the closer they get to being underfunded. Yet buying such negative-yielding bonds and keeping them to maturity ensures losses, making it more likely the fund will be underfunded, and so forced to buy more loss-making bonds (spot the feedback loop). Soon the fund will be distributing returns from capital, rather than returns on capital. Hence, it is not inflation that will destroy pension funds, but the mix of negative rates and rules that stop managers from deploying capital as they see fit. These protect governments, not pensioners who are forced to buy bad paper.

- Bank. As a leveraged player, let’s assume it lends a fairly standard 12 times its capital. This capital has to be invested in “riskless” assets that are always liquid. In the old days, this would have been gold or central bank paper exchangeable into gold. Today, the government bond market plays the role of “riskless” (you have to laugh) asset, which has no reserve requirement. As a result, banks are loaded up with bonds issued by the local state. Now let us assume that a bank has just lost €3 on the zerocoupon bond mentioned above. The bank’s capital base will be reduced by €3. Based on the 12x banking multiplier, the bank will have to reduce its loans by a whopping €36 to keep its leverage ratio at 12. Hence, the effect of managing negative rates while also respecting bank capital adequacy rules means that the capital base can only shrink.

- Insurance company. These institutions have two centers of profits. First is the core business of assuming risk on behalf of clients. Second, they manage premiums paid by the clients in a way that aims for a profit over the present value of the risks covered. A standard solution is to cover the maximum amount of risk with a government bond of similar duration to the client’s contract period, and then put the remainder into equities or real estate to help build up the firm’s capital base. This gets very difficult when government bonds offer negative yields. The insurance company could raise its premium by the amount of the expected loss from holding the bond (not very commercial), or it could just underwrite less business. Either way, it will have less money to invest in equities and real estate. Simply put, either the insurance company’s clients will pay the negative rates, or the company itself will do so by increasing its risks without raising returns. This means that either the client pays more for insurance, and so becomes less profitable, or the insurance company takes a hit to its bottom line.

The conclusion is

that negative rates must eventually destroy the

longterm savings industry run by pension funds, banks and insurance firms.

As Peter Bernstein showed in Against the Gods: The Remarkable Story of Risk, financial institutions

can bet against the gods and win if they compute the odds intelligently. If those odds are 100% you lose, then betting is just stupid.

….

----

----

"Borrowing our way out of debt" generates the three Ds of

Doom: debt leads to default which ushers

in Depression.

Let's

start by defining Economic Depression: a

Depression is a Recession that isn't fixed by conventional fiscal and monetary

stimulus. In other words, when a recession drags on despite massive

fiscal and monetary stimulus being thrown into the economy, then the

stimulus-resistant stagnation is called a Depression.

Here's why

we're heading into a Depression: debt exhaustion. As the charts below illustrate, the U.S. (and

global) economy has only "grown" in the 21st century by expanding

debt roughly four times faster than GDP or earned income.

Costs for

big-ticket essentials such as housing, healthcare and government services are

soaring while wages stagnate or decline in purchasing power. What's purchasing power?

Rather than get caught in the endless thicket of defining inflation, ask

yourself this: how much

of X does one hour of labor buy now compared to 20 years ago? For example, how much healthcare does an hour of

labor buy now? How many days of rent does an hour of

labor buy now compared to 1999? How many hours of labor are required to

pay a parking ticket now compared to 1999?

Our

earnings are buying less of every big-ticket expense that's essential, and we've covered the gigantic hole in our

budget with debt. The only way the status quo could continue

conjuring an illusion of "prosperity"

is by borrowing fantastic sums of money, all to be paid with future earnings and taxes.

Take a

look at systemwide debt in the U.S. Does this look remotely sustainable? If the answer is yes, you might want to dial

back your Ibogaine consumption.

See Chart:

{kind=link}

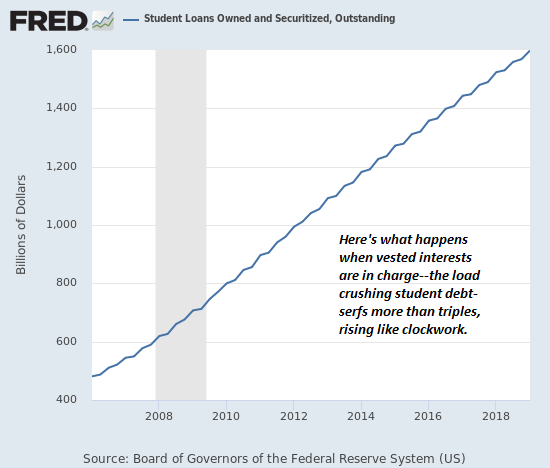

Here's

student loans. One trillion here and

one trillion there, and pretty soon you're talking about entire generations of

debt-serfs and a bunch of pension funds that are going

to suffer catastrophic losses when the student borrowers default.

See Chart:

{kind=link}

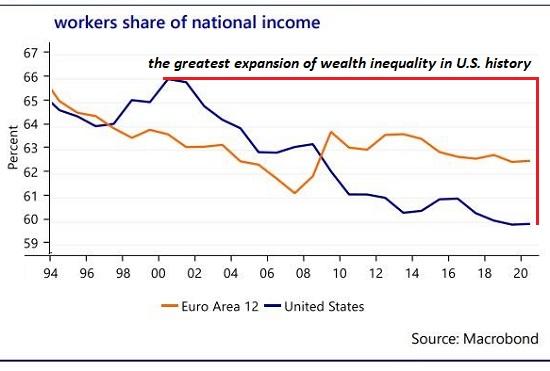

Meanwhile,

labor's share of the economy (wages and salaries) has been in structural

decline the entire 21st century. Lowering

interest rates to zero doesn't mean it's free to borrow more; the principal

payments loom large in every student loan, auto loan, mortgage, etc.

See Chart:

{kind=link}

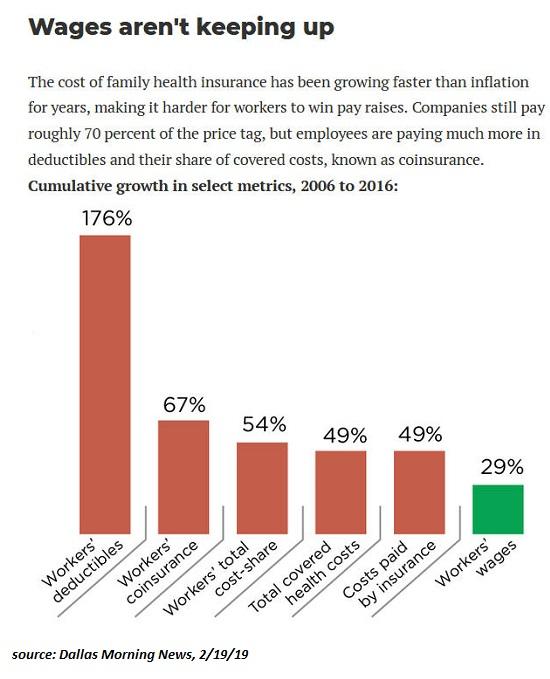

There's

less--a lot less--available to fund more borrowing after those stagnating wages

pay for rent or a mortgage/property taxes, healthcare, childcare, student

loans, etc. This chart depicts healthcare

costs, but rent, childcare, higher education, etc. all mirror similar

increases.

See Chart:

Wages are not keeping up

{kind=link}

"Borrowing

our way out of debt" generates the three Ds of Doom: debt leads to default

which ushers in Depression.

….

----

----

This sent

the odds of a 50bps rate-cut in

July to a shocking 55%..

So much for Powell's jawboning expectations back.

The dollar slumped...

See Chart:

{kind=link}

Bond yields tumbled...

See Chart:

UST 10Y Yield

{kind=link}

And stocks levitated (with Nasdaq

getting back to unch)...

See Chart:

{kind=link}

Another potential catalyst for the

move was headlines from The Guardian claiming that Iran offered to agree to a nuclear deal if US dropped sanctions.

….

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

President Eisenhower’s proposed

counterweight to the power of the military-industrial complex was

to be “an alert and knowledgeable

citizenry.” And there are signs that significant numbers are

beginning to pay more attention...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

"I

believe we were few minutes away from a war. Prudence prevailed and we’re not

fighting. So that gives reason for us to be optimists. If we work, if we are

serious, then we can find a way forward."

====

"These are people who smuggle our oil" — Iran FM

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

ARG:

other error: 25 años sin justicia por atentado a la AMIA

====

ALAI ORG

====

RT EN

ESPAÑOL

- Turquía advierte sobre consecuencias para la OTAN por la decisión de EE.UU. sobre los F-35

- Piden castigo ejemplar a la minera mexicana que derramó ácido sulfúrico en el "acuario del mundo"

- En US advierten de las 'huellas rusas' de FaceApp y recomiendan eliminarla: ¿tan peligrosa es esta aplicación?

- La nueva arma electrónica con la que EE.UU. habría derribado al dron iraní

- Trump se contradice sobre las sanciones contra Turquía por la compra de los S-400 rusos

- Racismo: Empleado de gasolinera en US insta a unas clientas latinas a "regresar a su país", diciendo que llegará el Servicio de Inmigración

- Canciller iraní afirma no tener información sobre la pérdida de un dron

- El medioambiente, la excusa de los ricos de San Francisco para oponerse a la construcción de un refugio para los sintecho

- Abogado investigador del caso AMIA evalúa la pesquisa del Gob de Macri

- Keiser Report "El sinsentido económico de la fracturación hidráulica está acabando con el sector petrolero tradicional"

- El Zoom US: Inmigrantes entre dos fuegos

----

----

INFORMATION CLEARING HOUSE

Deep on the US political crisis: neofascism & internal

conflicts that favor WW3

-The Military-Industrial Complex on Steroids By William D. Hartung

-Pompeo’s Big Lie on Iran By Jacob G. Hornberger

-When Muslims saved Jewish lives By Dr. César Chelala

-S-400 Ultimate Shoot-Down By Finian Cunningham

-Media Faced with Dilemma in Next Phase of

Deep State-gate By Ray

McGovern

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

-Julian

Assange: US Coopts Patriotic Opposition in Ecuador, Former President Correa

goes against Wikileaks Founder

By Andrew Korybko

----

----

DEMOCRACY NOW

Amy Goodman’ team

- “It

Is Not Just War. It Is Life”: Acclaimed Doc “For Sama” Offers Rare Glimpse into

War-Torn Syria

----

----

PRESS TV

Resume of Global News described by Iranian observers..

Hundreds

protest in New York over white officer’s

acquittal of black man's death

----

====

No hay comentarios:

Publicar un comentario