DEBT GRAVEYARD

or CURRENT US ECON CRISIS

If you are thinking this is a “Goldilocks economy,” “there

is no recession in sight,” “Central Banks have this under control,” and that “I

am just being bearish,” you would be right... But that is also what everyone thought in

2007.

Market

Review & Update

Last

week, we discussed the setup for a near-term mean reversion

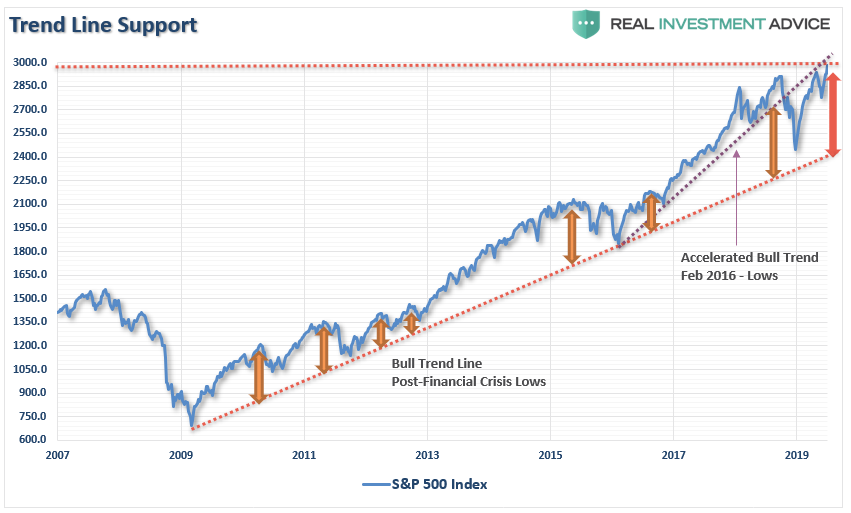

because of the massive extension above the long-term mean. To wit:

“There is also just the simple issue that markets are very extended

above their long-term trends, as shown in the chart below. A geopolitical

event, a shift in expectations, or an acceleration in economic weakness in the

U.S. could spark a mean-reverting event which would be quite the norm of what

we have seen in recent years.”

See Chart:

Trend Line Support

{kind=link}

My friends at Polar

Futures Group laid out the same concerns on Friday:

“The mean reversion trade: For the past few weeks I’ve been musing

that the “irresistible force” that has moved all markets has been the

aggressive repricing of future interest rate expectations since last

November. We’ve had a

HUGE rally in the bond market, MASSIVE flows into bond funds, record levels

(>$13.7T) of negative yielding bonds, inverted yield curves, even Greek

bonds trading through Treasuries…as markets anticipate a recession and much

more Central Bank largess…which might just take us into MMT and/or never-never

land where the Central Banks just buy all the bonds and that’s that. I’ve thought that this

irresistible force may have gone too far too fast and was due for a “set-back”

which would precipitate mean reversion trades across markets.

The core concepts of the mean reversion trades I’m considering are as

simple as, 1) the public buys the most at the top (thank you, Bob Farrell,) and 2)

when they’re yelling you should be selling, and 3) positioning risk leaves some

markets especially vulnerable.”

They are exactly right.

While the market is rallying in anticipation of more Central

Bank easing, especially following the recent announcement by the ECB of lower

rates and more QE, the markets are momentarily detached from weaker earnings

growth, weaker economic growth, and a variety of other market-related

risks.

However, in the very

short-term, the market is grossly extended and in need of some correction

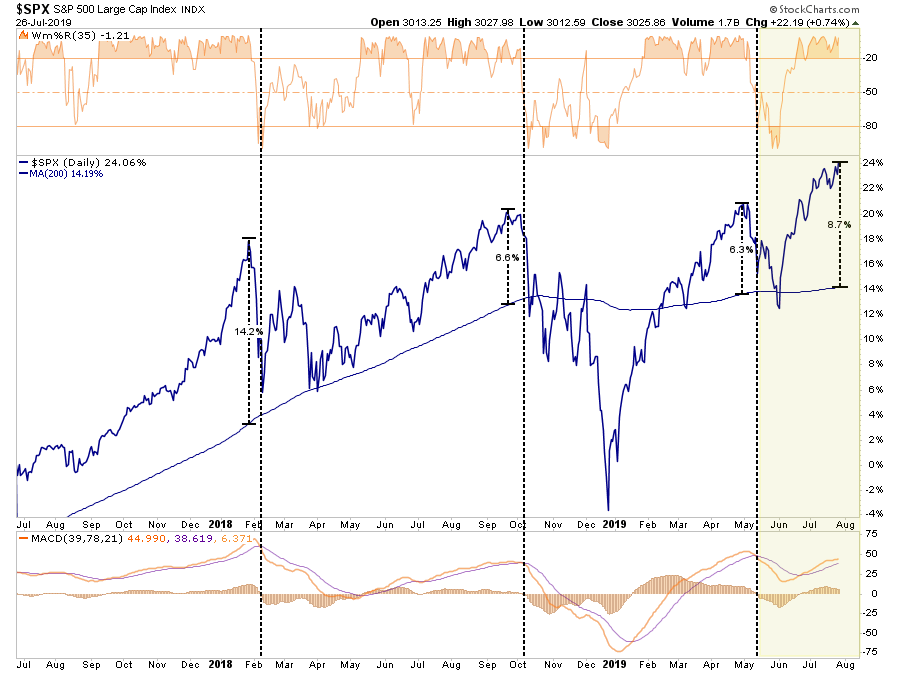

action to return the market to a more normal state. As shown below, while the market is on a near-term “buy signal” (lower

panel) the overbought condition, and near 9% extension above the 200-dma,

suggests a pullback is in order.

See Chart:

{kind=link}

As we have noted over the last few

weeks, the very tight trading range combined with negative divergences also

does not historically suggests continued bullish runs higher without some type

of corrective action first.

See Chart:

{kind=link}

The $70 Trillion

Dollar Graveyard

On

Thursday, Congress passed the spending bill we

discussed last week:

65 Republicans joined the Democratic majority

in the 284-149 vote, with 132 Republicans voting against the bill, despite

President Trump’s endorsement and pressure from key outside groups, including

the Chamber of Commerce, to avoid a potentially catastrophic default on the Government’s

debt.”

I highlighted the last sentence in red because it is an

outright “LIE” used to convince Americans that out of control spending must be

done.

The reality is that “interest payments on the

debt” are part of the MANDATORY spending in our budget along with

social security, medicare, etc. Currently, about $0.75 of every dollar of tax revenue goes to mandatory

spending. For the last few months

the Government has been at its statutory debt limit, and “surprise” we

didn’t default on our debt. Why? Because there is enough revenue currently

coming in to cover the mandatory spending.

As I noted specifically last

week,

“In 2018, the

Federal Government spent $4.48 Trillion, which was equivalent to 22% of the

nation’s entire nominal GDP. Of that total spending,

ONLY $3.5 Trillion was financed by Federal revenues, and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare

and interest on the debt, those payments required $3.36 Trillion of the

$3.5 Trillion (or 96%) of revenue coming in.”

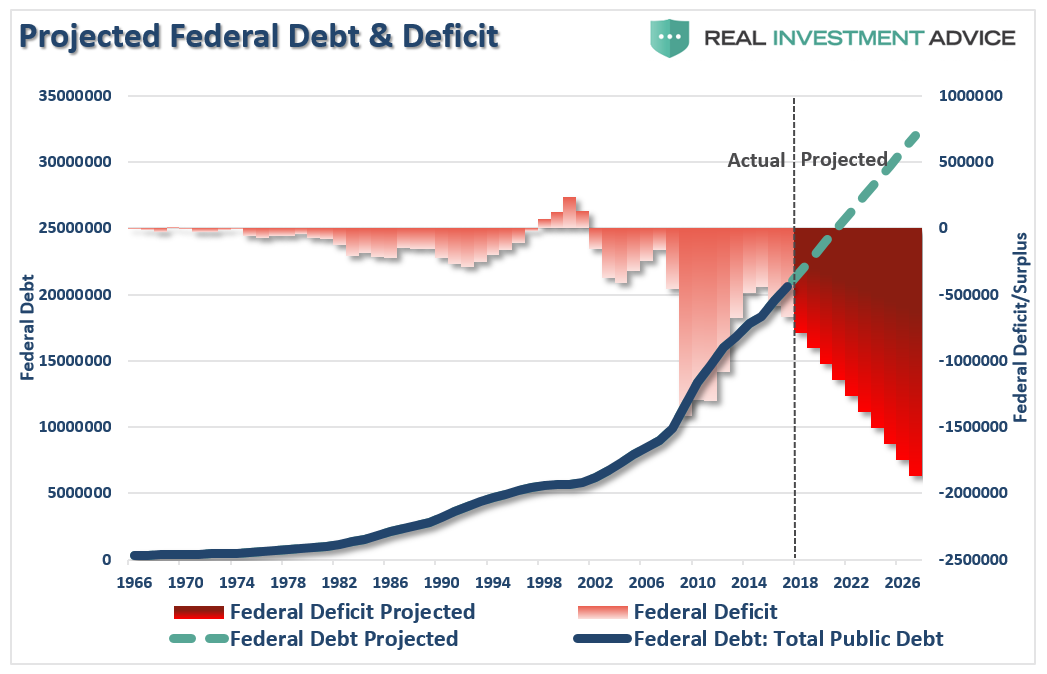

Do some math here.

The U.S. spent $986

billion more than it received in revenue in 2018, which is the overall

‘deficit.’ If you just add the $320 billion to

that number you are now running a

$1.3 Trillion deficit.

See Chart:

Projected FED Debt & Deficit

{kind=link}

The U.S.

will not default on its debt.

But that’s

not the real story.

The crux of that article was focused on the roughly $6

Trillion of unfunded liabilities of U.S. pension funds which Congress is now

drafting a piece of legislation for entitled the “Rehabilitation For Multi-employer

Pensions Act.”

As noted in that article, while Congress is preparing a

bailout for U.S. pension funds, there is a $70 Trillion pension problem globally which

is not being addressed.

“According to an analysis by the World Economic Forum (WEF), there was

a combined retirement savings gap in excess of $70 trillion in 2015, spread

between eight major economies…

See Chart:

{kind=link}

“America’s debt load is about to hit a record. The combination of cheap

money and soaring debt helped fuel the decade-long economic expansion and bull

market, but America’s gluttony of loans could work against it if its fragile

economic balance shifts.

In the first quarter of 2019, the United

States’ total public- and private-sector debt amounted to nearly $70

trillion, according to research by the Institute of

International Finance. Federal government debt and

liabilities of private corporations excluding

banks both hit new highs.”

Oh…you are

talking about THAT $70 Trillion.

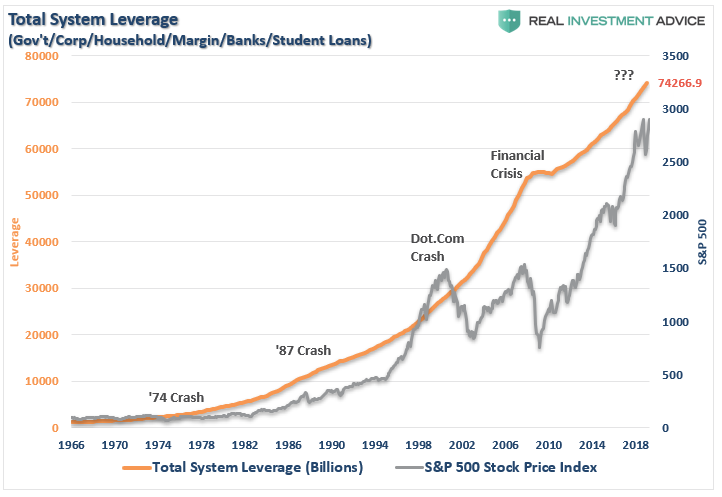

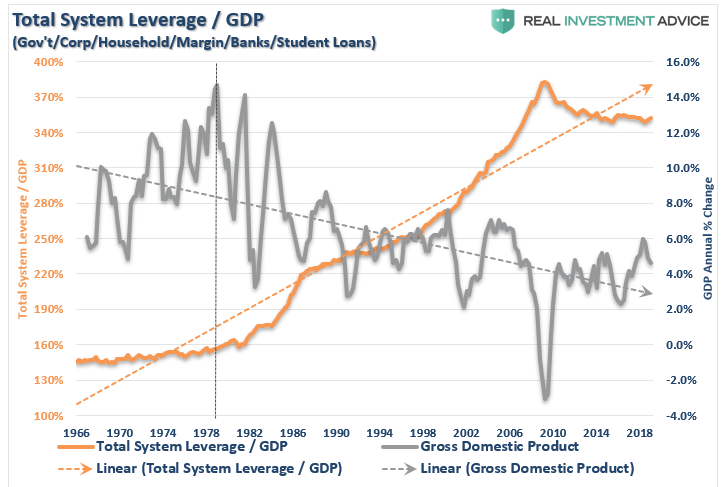

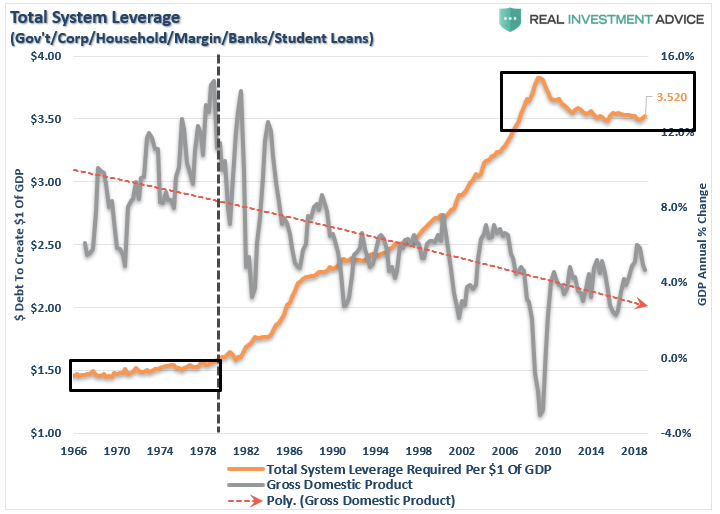

The chart below is Total U.S. Credit Market Debt (including

Student Loans) which is currently running just a smidgen over $74

Trillion.The last time there was even a hint of

deleveraging was during the “Financial

Crisis.”

See Chart:

Total System Leverage

{kind=link}

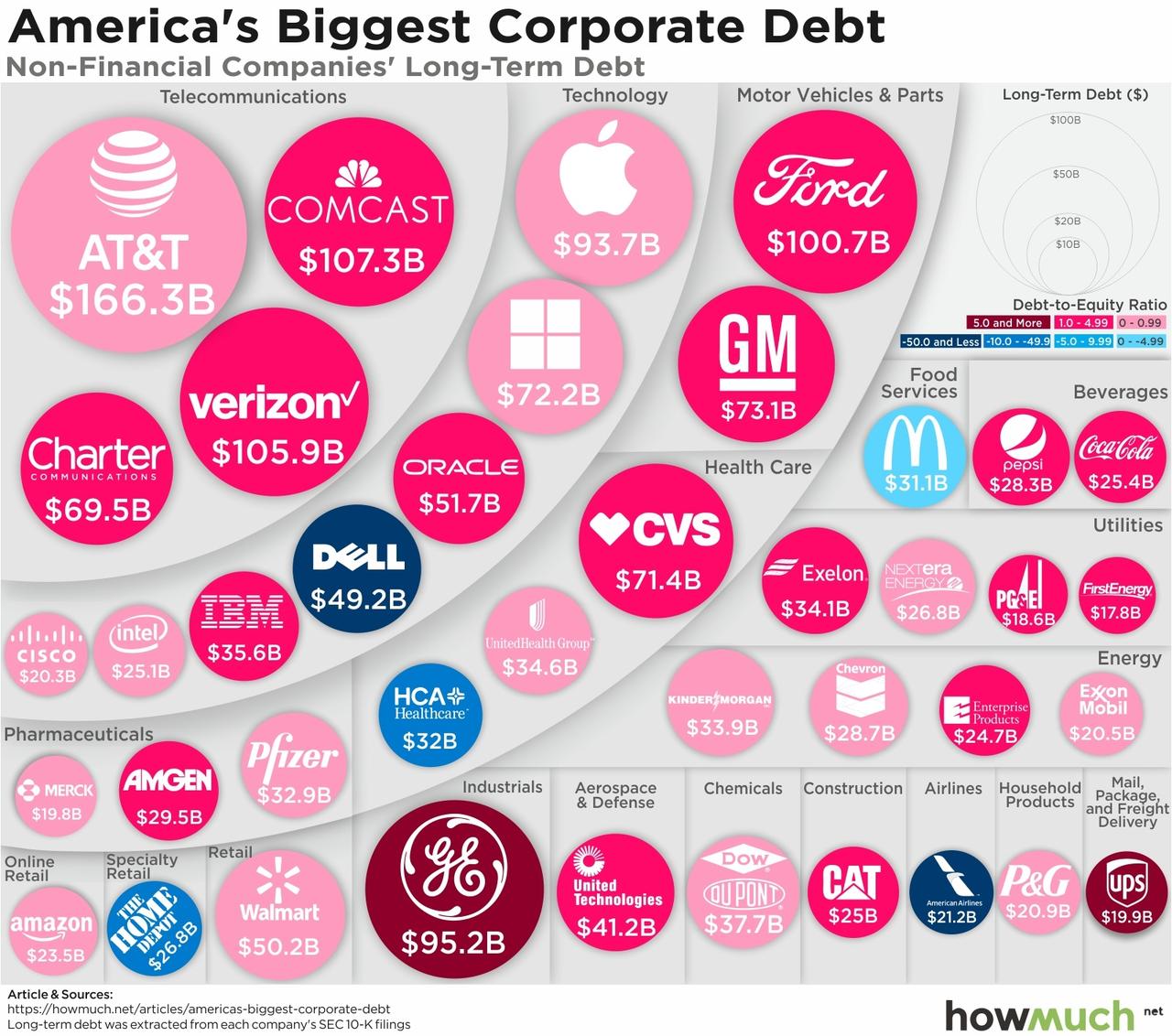

Corporate

debt is a problem.

The wonderful website “HowMuch” put

the corporate debt bubble into a graphic to help us visualize

the potential for widespread defaults during the next economic and market

downturn.

See Chart:

America’s Biggest Corporate Debt

{kind=link}

The problem with corporate debt is the amount of debt which

is at risk of default during the next economic recession. (This isn’t an “IF,” it’s a “WHEN”

statement.)

Let’s start with a note from Michael

Lebowitz:

“The graph shows the implied ratings of all BBB companies based solely

on the amount of leverage employed on their respective balance sheets. Bear in

mind, the rating agencies use several metrics and not just leverage. The graph shows that 50% of BBB companies, based solely on

leverage, are at levels typically associated with lower rated companies.”

See Chart:

{kind=link}

“If 50% of BBB-rated bonds were to get downgraded, it would entail a

shift of $1.30 trillion bonds to junk status. To put that into perspective, the entire junk market

today is less than $1.25 trillion, and the subprime mortgage market that caused

so many problems in 2008 peaked at $1.30 trillion. Keep in mind, the subprime mortgage crisis and the ensuing

financial crisis was sparked by investor concerns about defaults and resulting

losses.”

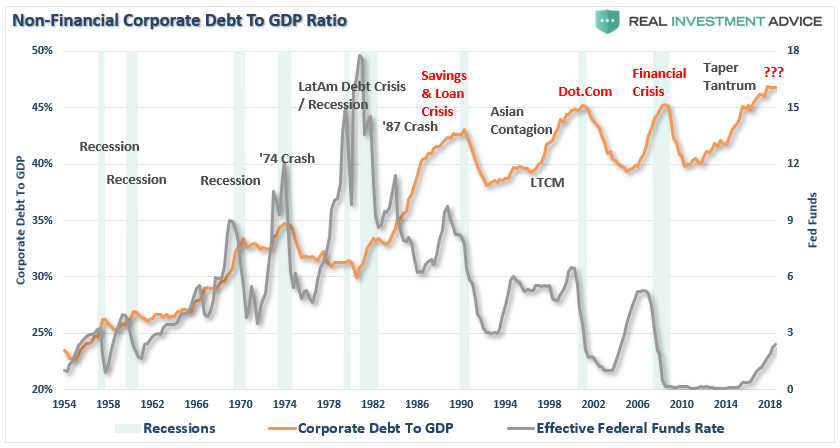

The reason BBB-rated debt is so plentiful is due to the

Fed’s ultra-low interest rate policy over the last decade. Near zero rates, and

easy credit terms, has seduced companies into taking on debt to fund

operations, dividends, and stock buybacks. The

consequence is we are now seeing corporate debt exceeding the levels of the

global financial crisis.

See Chart:

Non Financial Corp Debt to GDP Ratio

{kind=link}

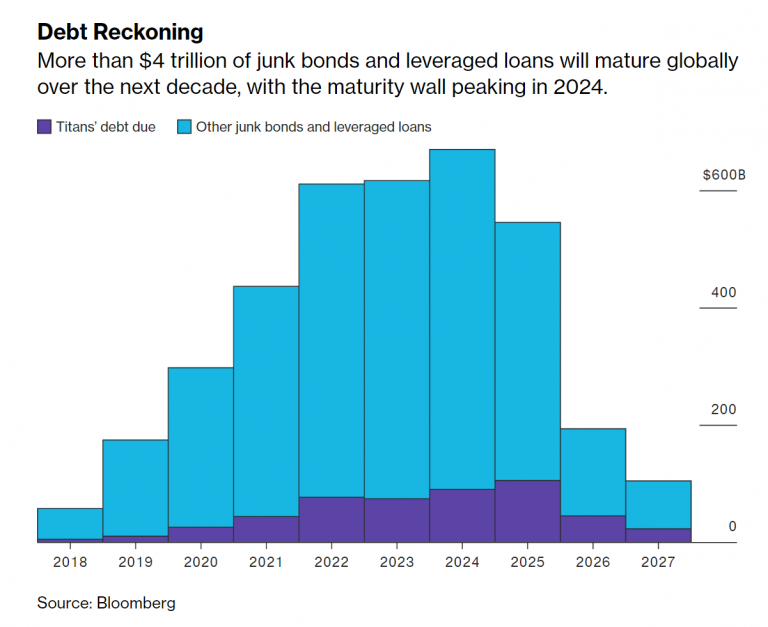

The real risk is that over the next

5-years more than 50% of the junk-bonds and leveraged-loans (which is

sub-prime debt for corporations) is maturing and must be refinanced

See Chart:

Debt Reckoning

{kind=link}

Let that sink in for a minute.

A weaker

economy, recession risk, falling asset prices, or rising rates could well lock

many corporations OUT of refinancing their share of this $4.88 trillion debt.

Defaults will move significantly higher, and much of this debt will be

downgraded to junk.

But it isn’t just corporate debt, that’s a problem.

Whistling

Past The $246+ Trillion Graveyard

“According to the latest IIF Global Debt Monitor released

today, debt around the globe hit $246

trillion in Q1 2019, rising by $3 trillion in the quarter, and outpacing the

rate of growth of the global economy as total debt/GDP rose to 320%.

This was the second-highest dollar number on record after the first

three months of 2018, though debt was higher in 2016 and 2017 as a share of

world GDP. Total debt was broken down as follows:

·

Households:

60% of GDP

·

Non-financial

corporates: 91% of GDP

·

Government

87% of GDP

·

Financial

Corporations: 81% of GDP

And while the developed world has some more to go before regaining the

prior all time leverage high, with borrowing led by the U.S. federal government

and by global non-financial business, total debt in emerging markets hit a new

all time high, thanks almost entirely to China.”

This is why Central Banks, from the ECB to the Federal

Reserve, are terrified of an economic recession or downturn. As I said

previously, “debt is the ‘weapon of mass destruction'”

Given that global debt is 320% of global GDP, a deleveraging

cycle will be too large for Central Banks to contain.

The deleveraging cycle WILL occur, all that

Central Banks can do is hope to extend the current cycle long enough that

“maybe” economic growth will catch up with the problem and lower the risk.

The irony is that it is the Central Banks on

actions (lowering interest rates to zero and flooding the system with

liquidity) which has inflated the debt bubble.

But that’s everyone else’s problem, right.

As noted above, the U.S. is currently running a debt-to-GDP

ratio of roughly 350% so we are certainly not immune to

the risk of a global “debt contagion.”

See Chart:

{kind=link}

We can

look at this a bit differently. The economy currently requires $3.50 of NEW

debt just to generate $1 of new growth.

See Chart:

Total

System Leverage

{kind=link}

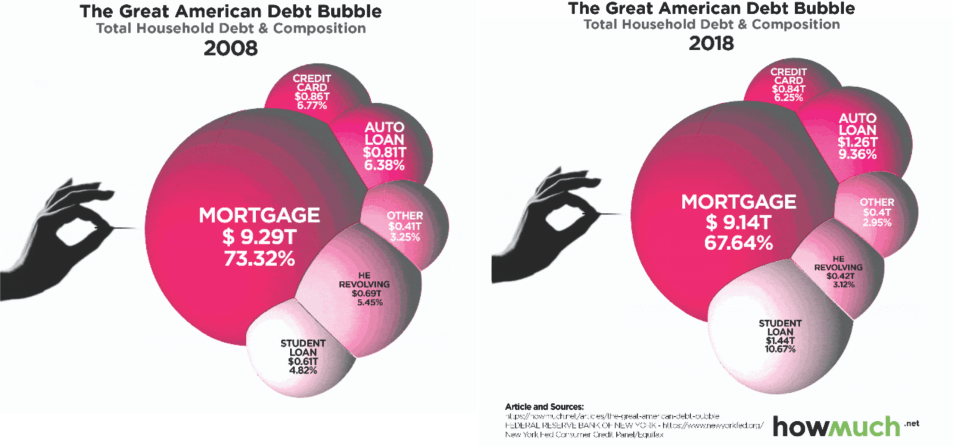

The problem with the exceedingly high debt levels is that

since economic growth is a function of debt-supported spending, there is a

finite limit to how much debt can be absorbed. As “HowMuch” showed, 10-years

after the financial crisis, individuals are more levered today than they were

then. (Notice the

doubling of auto and student loan debt in particular.)

See Picture:

{kind=link}

The Real

Crisis Is Coming

As I noted

this past week, the real crisis comes when there is a “run

on pensions.” With a large number of pensioners already

eligible for their pension, and a near $6 trillion dollar funding gap, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely.

The combined run on the system, which is grossly

underfunded, at a time when asset prices are dropping,

credit is collapsing, and shadow-banking freezes, the ensuing debacle will make 2008 look like mild recession.

It is unlikely Central Banks are

prepared for, or have the monetary capacity, to substantially deal with the

fallout.

Never before in human history have we seen so much

debt. Government debt, corporate debt, shadow-banking debt, and consumer

debt are all at record levels. Not just in the U.S., but all over the world.

If you are thinking this is a “Goldilocks economy,” “there

is no recession in sight,” “Central Banks have this under

control,” and that “I

am just being bearish,” you would be right.

But that

is also what everyone thought in 2007.

….

----

----

No hay comentarios:

Publicar un comentario