ND JAN 29 19 SIT EC y POL

ND

denounce Global-neoliberal debacle y propone State-Social + Capit-compet in

Econ

ZERO

HEDGE ECONOMICS

Neoliberal

globalization is over. Financiers know it, they documented with graphics

Econ

situation today:

Investors

clung to the positivity of The Dow today, ignoring the recessionary indications

from sentiment indicators, tumble in earnings expectations, Nasdaq slump, and

bod for safe-haven bonds and bullion... remember again "The Dow was

green... Don't forget the FOMC 'Drift'"...

US markets were very mixed with The Dow positively diverging from

Nasdaq at the cash open, then all tumbling together into the European close...

See

Chart:

{kind=link}

The Dow desperately clung to green into the close as Small Caps,

S&P and Nasdaq all ended red...Trannies outperformed

See

Chart:

{kind=link}

It appears for now that the squeeze has run out of ammo...

See

Chart:

{kind=link}

Bonds were bid today safe-havens rallied on Nasdaq weakness.

Notably, the long-end continues to underperform...

See

Chart:

{kind=link}

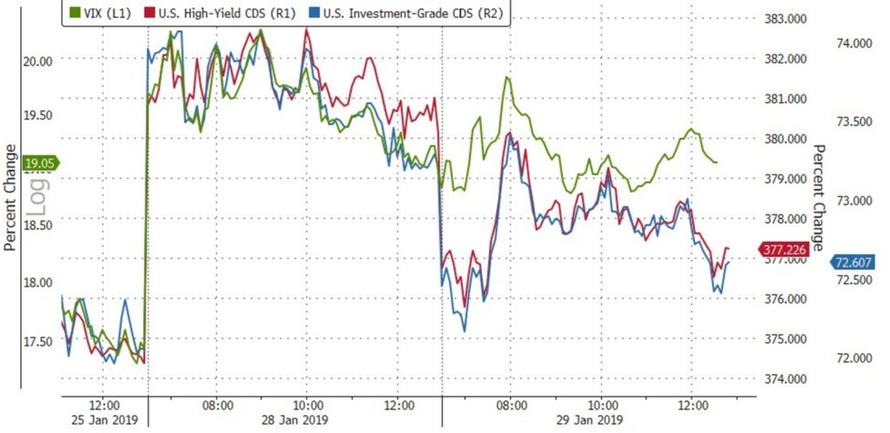

Credit spreads compressed today but VIX was flat...

{kind=link}

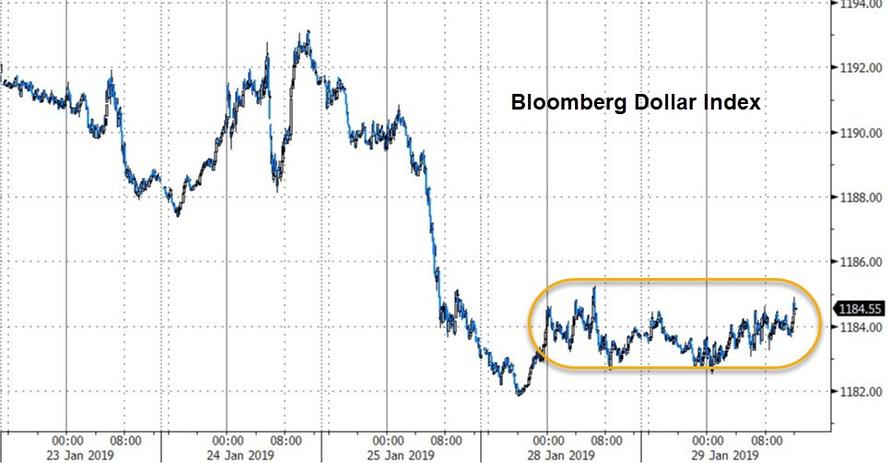

For the second day in a row, the dollar trod water in a very narrow

range...

See

Chart:

{kind=link}

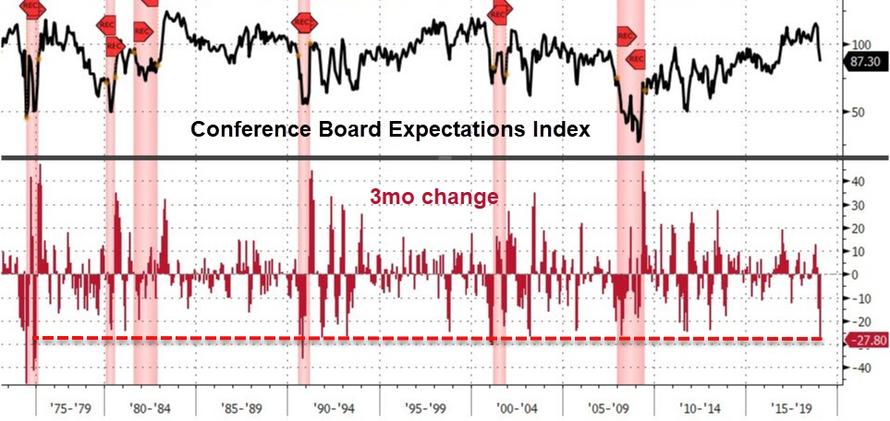

And as The Fed prepares to tell us how everything is still awesome

BUT they want to be cautious - or some such bollocks - we note the Conference Board's expectations index has

crashed in the last 3 months by an amount that has always been associated with

recession...

See Chart:

{kind=link}

And the spread

between current sentiment and expectations is the widest since

March 2001, the first month of the U.S. recession that year.

See Chart:

{kind=link}

And Jeff

Gundlach agrees:

The most recessionary signal at present is consumer future

expectations relative to current conditions. It’s one of the worst readings

ever.

….

----

----

"We suspect risk assets may react negatively to the lack of

balance-sheet guidance and contribute to a further flattening of the rates

curve."

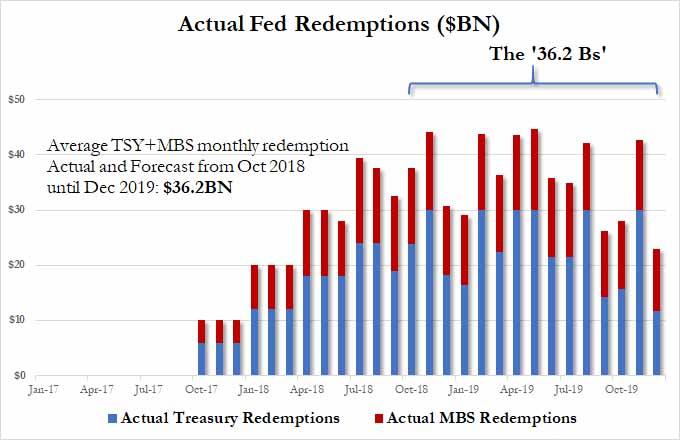

Fed's

balance sheet, which after expanding for the better part of the past decade has

been shrinking at an "autopilot" pace of roughly

$36 billion per month ever since it hit its

"peak shrinkage" in Q4 of 2018...

See

Chart:

Actual

FED Redemptions ($BN)

{kind=link}

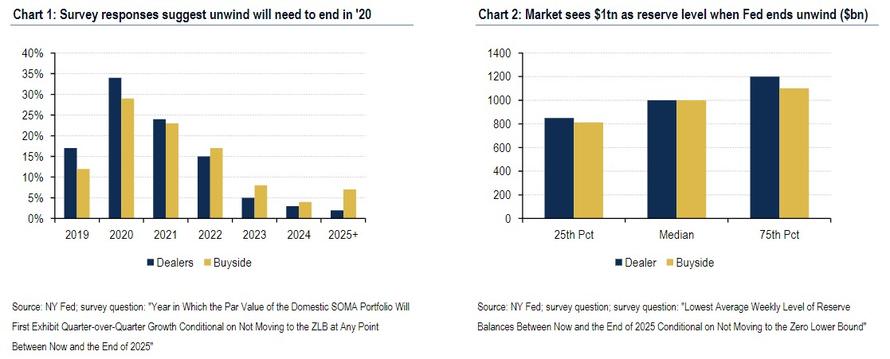

The

market has already signaled to the Fed an expectation that it will need to

maintain a relatively abundant reserve regime and that the

unwind likely will not last beyond 2020 with around $1tn in reserves...

See

Charts:

{kind=link}

To summarize: the Fed will likely be challenged

to deliver a sufficiently dovish message vs market expectations, which risks a

sharply negative reaction in stocks, a flatter rates curve and a risk off USD

reaction.

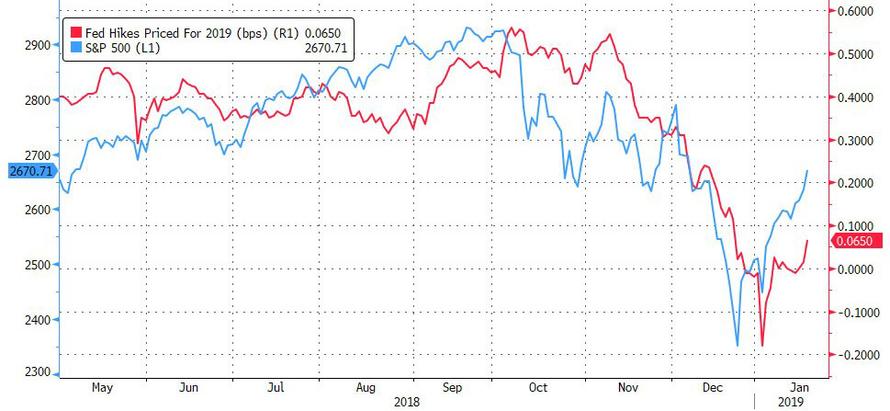

And in keeping with the reflexive nature of the market which has

rebounded sufficiently in recent weeks to push rate hike odds for 2019 back

into the green, and away from an expected rate cut...

See

Chart:

{kind=link}

...

Nomura's Charlie McElligott provides yet another reason why the Fed may

disappoint markets tomorrow, and it has to do with the

ongoing "standoff" between markets and monetary policy:

As the

data stabilizes (which it is currently attempting now, with Citi U.S. Economic

Surprise Index pivoting back “positive” to+1 from -25 on Jan 3rd) or even

accelerates higher, we re-enter that "tighter financial conditions" negative

feedback loop, as the Fed is ultimately forced back-into the picture;

Conversely,

if the data were to again slow further from here, it confirms that “glass

half-empty” current investor view that “the best is behind us” and that we have

“overtightened ourselves into a slowdown”

Essentially, for the Fed to "get more dovish" at this

point - which also includes potentially conceding on balance sheet tapering

- it would require a major

downdraft in U.S. economic data or another market volatility spasm—which is NOT something that is

going to help the mood. BofA agrees with this, and notes that "a

broader decline in risk assets could also cause the Fed to reconsider its

balance-sheet plans, particularly if it believes that the balance sheet policy

is a culprit for market stress."

Stated

simply, for the Fed to be ready to announce a pause, or

end, to Quantitative Tightening, stocks have to tumble once again, just so they

can then be then rescued again by the Fed during the next

sharp market drop.

…

SOURCE: https://www.zerohedge.com/news/2019-01-29/fed-will-massively-disappoint-markets-tomorrow-heres-why

----

----

"A remarkable 87% of all MSCI World stocks are up to

year-to-date" which would rank January as one of one of the best months

ever for positive stock performance; this leaves investors facing a difficult

dilemma...

See

Charts:

{kind=link}

….

----

----

"Central bankers still don’t understand bonds because they don’t do money. They

remain devoted to their outdated textbook. Don’t take my word for it, trust the curves inverted or not..."

It was

the most common catchphrase of 2017, interest rates have nowhere to go but up. Maybe it was doomed from the

start given that Alan Greenspan was among the more prominent commentators

expressing this view. In his mind, the bond market was in a bubble and the

party was already over.

Decoding curves is essential to framing

actual conditions, therefore the start of any rational analysis.

An excerpt from my presentation in Vancouver last weekend:

See

Chart:

{kind=link}

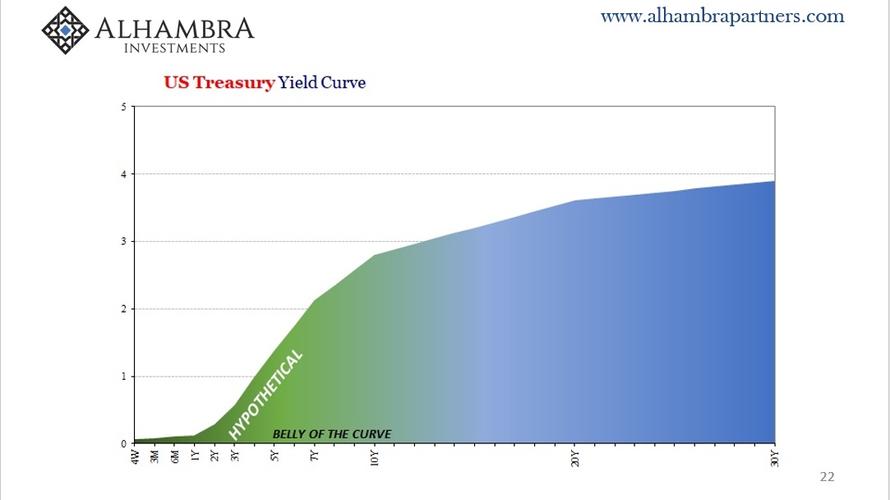

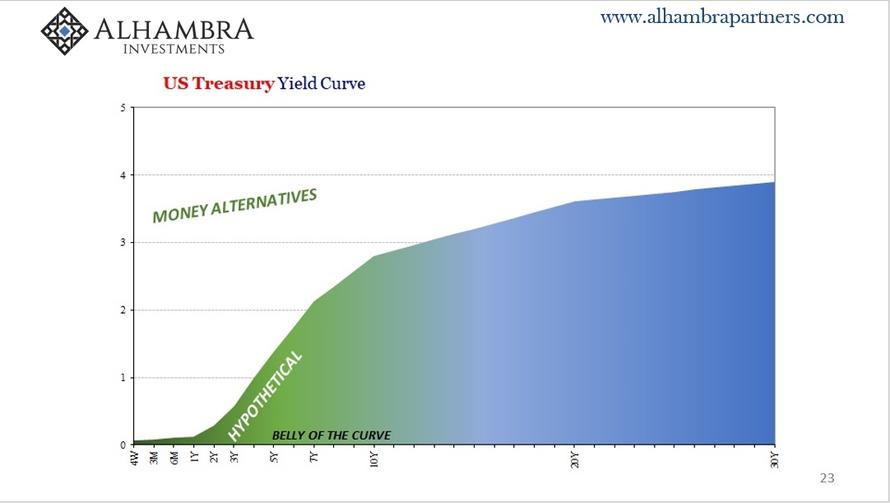

A yield curve isn’t a single thing. It is a spectrum that coalesces

in competing directions, a bipolar mechanism for setting probabilities about

two very complex arrangements.

See

Chart:

{kind=link}

In

academia, the Fed sets the money rate and then banks perform based on it. This is called maturity transformation, which simply means

that banks borrow funds short-term and lend them long-term. It is therefore

expected that short-term money rates...

See

Chart:

{kind=link}

The interaction between the short end and long end is therefore not

always direct and immediate. The long end can and does interpret the conditions

of the short end independently of what has become mainstream convention.

See

Chart:

{kind=link}

The short end of the UST curve is highly

influenced by the Federal Reserve’s monetary policies while the long end

clarifies those policies through the prism of risk/return.

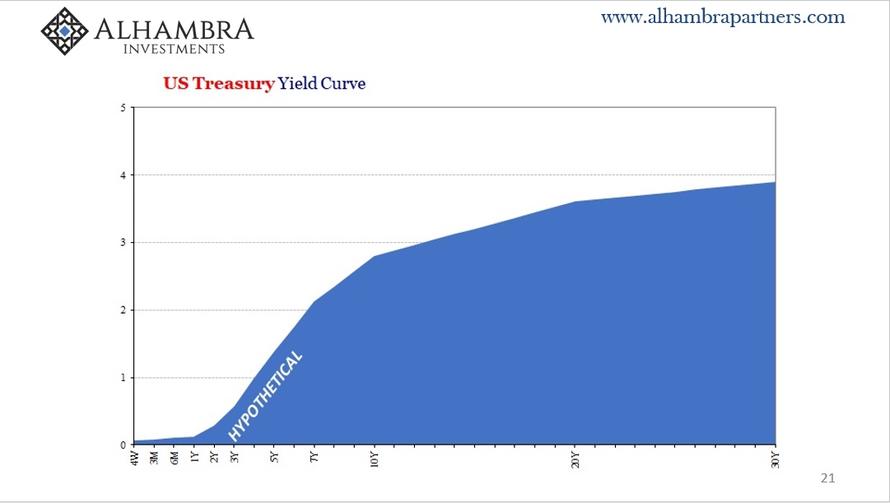

A steep

yield curve, like the one picture here, is one that suggests a low rate,

accommodative monetary policy that is likely to work over time. This accounts

for the curve’s steepness. A flat and inverted curve is the opposite. Whatever monetary policy is being conducted, the long end is

interpreting that policy as well as other conditions as being highly suspect.

See

Chart:

{kind=link}

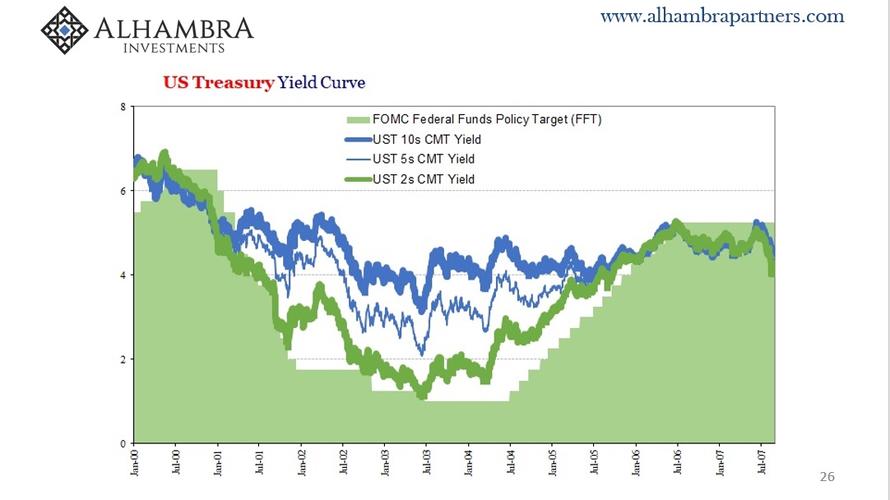

When we

look back on the curve history through the middle 2000’s, we find these

competing dynamics in perfect practice. The Fed set the federal funds target,

one form of self-fulfilled monetary alternate at the short end, the 2-year US

Treasury yield more closely aligned with it, while the long end rates moved

independently from either of them.

What

sticks out is how no matter what happened during this period, the long end, in

this case represented by the benchmark 10-year yield, barely moved. The maestro

didn’t appear to have much if any influence, the curve flattening dramatically

before ultimately inverting.

See Chart:

US Treasury Yield Curve

{kind=link}

Policymakers were all too ready to dismiss several years of this

contrary signal because in their view the world was getting better. That’s why

Greenspan was raising rates in the first place.

…

----

----

US DOMESTIC POLITICS

Seudo

democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge

cambio

"This certification will help

Venezuela's legitimate government safeguard those assets for the

benefit of the Venezuelan people."

----

----

"ISIS is intent on resurging and

still commands thousands of fighters."

----

----

"We

have many young people in our country, and in the state of

Indiana, who do not know a lot of simple information on our

government and on our country and some of our history,"

----

----

Washington state recently introduced bills for some of the strictest

gun laws in the country but they have some very important opponents: the sheriffs...

----

----

US-WORLD ISSUES (Geo Econ,

Geo Pol & global Wars)

Global

depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

"The US government and its assorted client states have no business

whatsoever issuing orders and ultimatums decreeing that a

government of a sovereign nation must restructure itself, but here we are..."

My own

Australia has of course joined

the chorus of US lackeys who are refusing to recognize Venezuela’s

only legitimate and elected government,recognizing instead the

presidency of some guy named Juan who decided to name himself Venezuela’s

president with the blessing of the United States government.

----

----

The "arm the moderate rebels"

campaign is off to a slow start...

----

----

PDVSA's creditors already looking to

seize oil over unpaid bills...

----

----

Similar abuses to VEN could happen to other

countries

Mexico is in

the midst of a crisis again...And no, it doesn’t have anything to do

with the border wall... Or the economy. Or murders and violence. Or drug

trafficking. Or bird flu.

----

----

SPUTNIK and RT SHOWS

GEO-POL

n GEO-ECO ..Focus on neoliberal

expansion via wars & danger of WW3

----

----

----

----

----

----

----

----

----

----

----

----

----

SHOWS RT

----

----

----

----

NOTICIAS IN SPANISH

Lat Am

search f alternatives to neo-fascist regimes & terrorist imperial chaos

REBELION

----

----

USA DEBATE IMPERIAL David Brooks

La “tienda” de Trump está en quiebra Patricio Montesinos

----

----

----

----

----

----

----

----

----

----

----

----

ALAI NET

----

----

----

----

----

----

----

----

----

RT EN ESPAÑOL

----

----

----

----

----

----

----

----

----

----

INFORMATION CLEARING HOUSE

Deep on

the US political crisis: neofascism & internal conflicts that favor WW3

86% of Ven Oppose Military Intervention By Ben Norton

----

‘5,000 troops to Colombia’: By Eli Rosenberg and Dan Lamothe

----

----

----

US Sanctions Against

Ven Caus Econ and Humanit Crisis Must Read - By Staff

----

Bernie and Dems Flunk

Trump’s Test On Ven’s Coup By

Shamus Cooke

----

In Case You

Missed it

Why We're at War? Confessions of a USA Economic Hit Man By Sam Elfassy

Why We're at War? Confessions of a USA Economic Hit Man By Sam Elfassy

----

Has the Arms Industry

Captured Trump’s Pentagon? By Mandy

S & William H

----

----

GLOBAL RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

----

----

----

----

----

----

PRESS TV

Resume

of Global News described by Iranian observers..

----

----

----

----

----

===

No hay comentarios:

Publicar un comentario