ND MAY 23 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

"Growth

Scare" -

PMIs in Japan, Europe, and US

all collapsed and risk-asset markets are suddenly waking from their delusions.

Well that

escalated quickly

WTI Crude

crashed to a $57 handle (its worst day of 2019)...

See Chart:

{kind=link}

US

equities suffered after Huawei headlines signaled US-China trade tensions are

escalating fast (and a base-case 'deal' is disappearing). "Trade

War"-related stocks have given up over half their

post-December-collapse gains...

See Chart:

{kind=link}

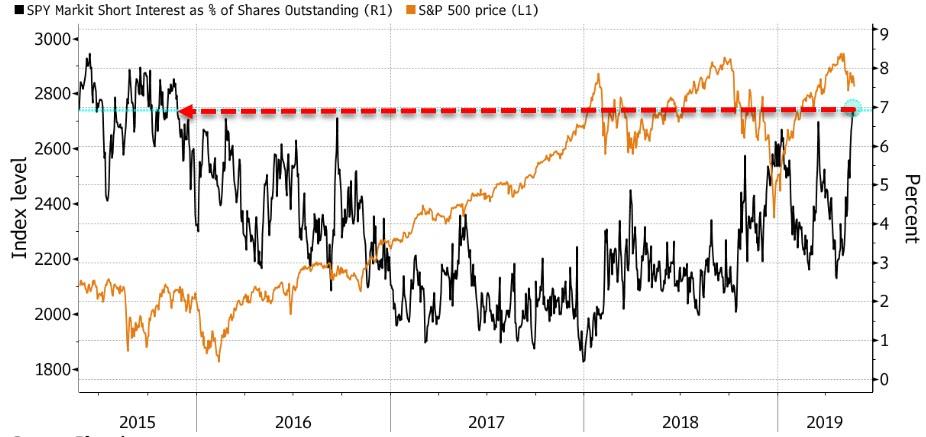

And as,

Bloomberg's Sarah Ponczek notes, investors haven’t been this keen to short

the U.S. stock market since the Federal Reserve started raising interest rates.

See Chart:

{kind=link}

Short interest as a

percentage of shares outstanding on the SPDR S&P 500 ETF Trust, or

SPY, climbed as high as 7% this week, according to data from IHS Markit Ltd.

That’s the highest share since 2015, when the benchmark gauge for American

equities slipped into a correction as Fed officials began boosting rates from

near zero.

“There are some clouds forming on the horizon,”

China was ugly overnight as Huawei headlines hit...

Europe was ugly, not helped by dismal confidence and PMIs in Germany

And US equities were a bloodbath with tech wrecking once

again...Trannies are the worst on the week, and The Dow is outperforming

(though all are red on the week)...

See Chart:

{kind=link}

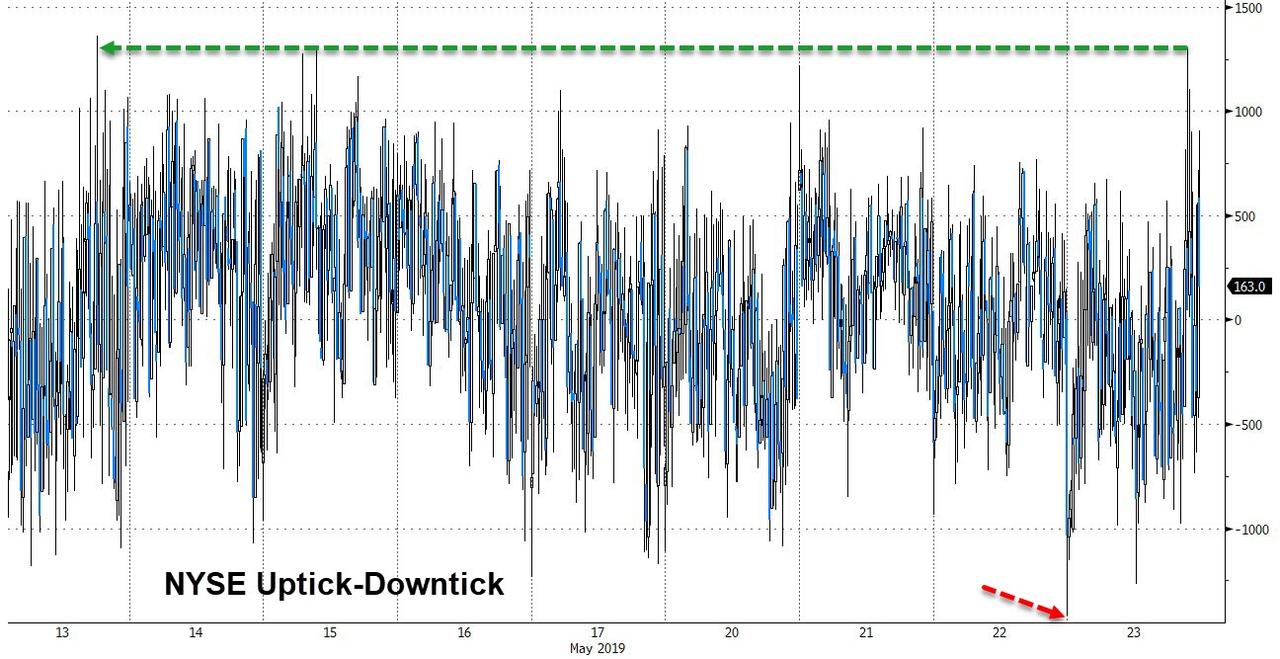

This was

the biggest buy program in over a week at 320pmET (after the biggest sell at

the open since January)... All is possible by printing dollars from the

thin air

See Chart:

NYSE

Uptick-Downtick

{kind=link}

Get the

normal size in the source below.. This chart has been damaged intentionally

Remember: we live in a free Nation (for billionaires) not for you.

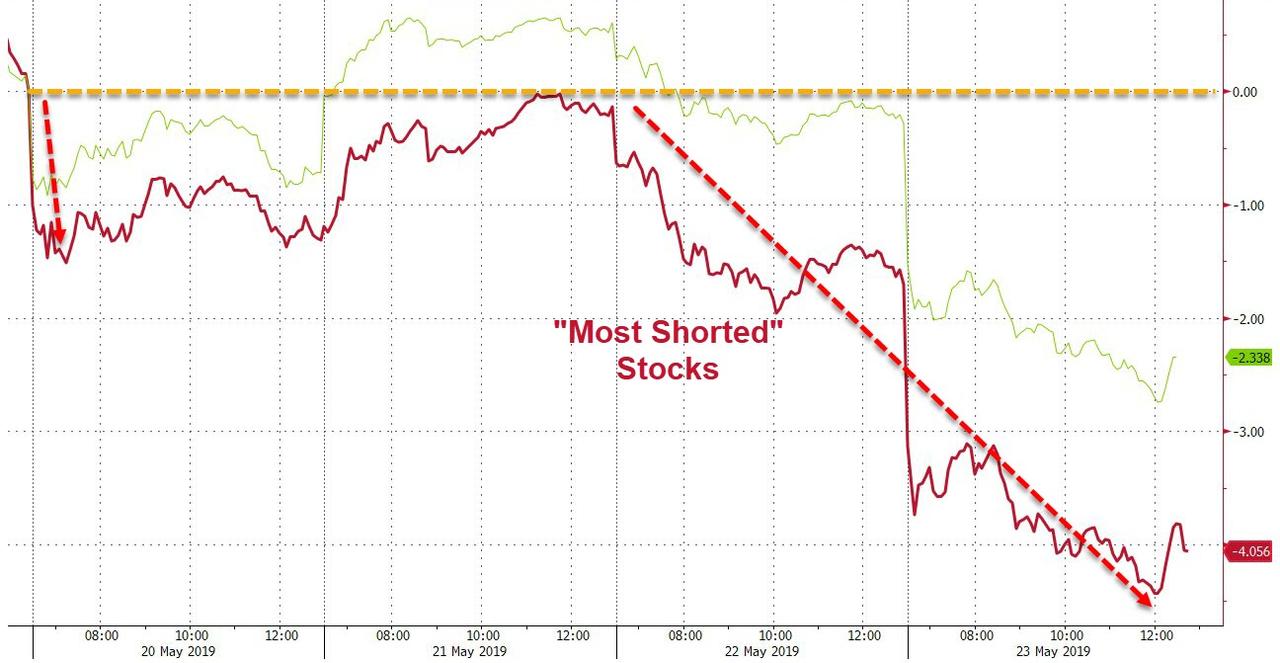

Small Caps

plunged to their lowest since January...

{kind=link}

This is

the biggest two-day drop in "Most Shorted" stocks since the Dec

24th lows...

See Chart:

{kind=link}

And

overall tech stocks wrecked...

See Chart:

{kind=link}

Before we leave

equity land, this stunning chart from Bloomberg strategist Cameron Crise

exposes the odd regime shift of the last few

weeks... Day after day, we see overnight selling pressure, only to be bid back

at the cash open. One could be forgiven for thinking the trade war is

being played out between The Plunge Protection Team and The National Team battling to show how trade tensions are not affecting

their stock markets. Think we're crazy?

The US stock markets are sliding as investors fear over China-US trade

war. The real situation could be even worse. The only room left for manoeuvre

is the leaders of the two countries still maintain personal respect for each

other.

But, as Crise

notes, these huge opening down gaps are pretty

clearly a sign of trouble, and we're now at the point that we've exceeded

anything observed during the crisis...

See Chart:

{kind=link}

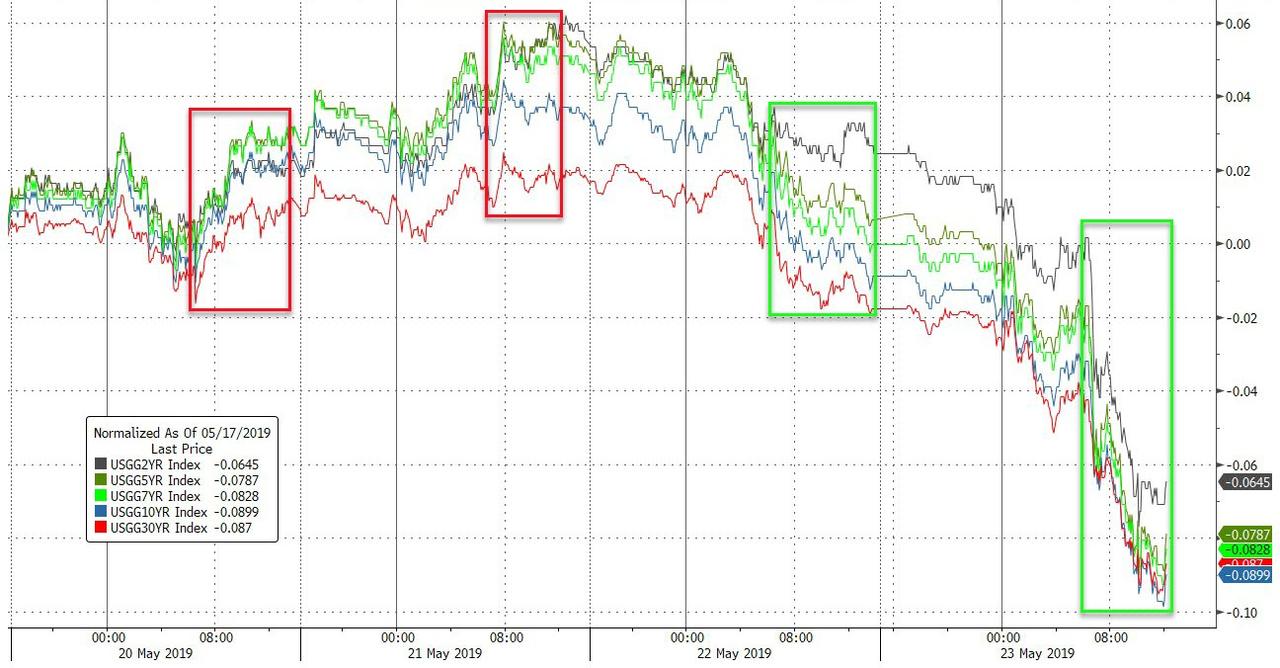

Treasury

yields tumbled on the day...

See Chart:

{kind=link}

Across the

curve this was new cycle lows for yields (5Y and 30Y lowest since Dec

2017, 10Y lowest since Nov 2017, 2Y lowest since Feb 2018)...

See Chart:

{kind=link}

The 10Y

Yield plunged below 2.30%!!

See Chart:

{kind=link}

The yield

curve crashed back into inversion...

See Chart:

{kind=link}

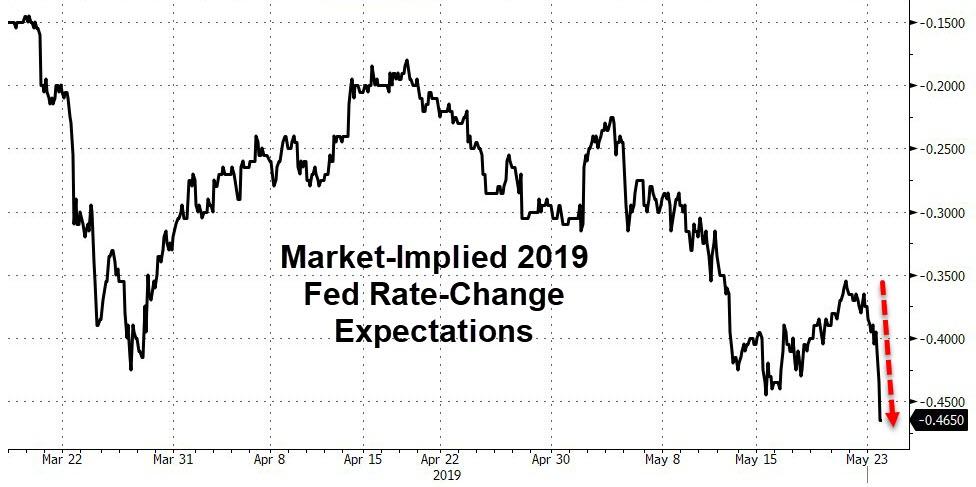

Finally,

before we leave rates-land, market expectations for 2019 Fed rate actions have

collapsed to a stunning 46bps rate-cut expectation...

See Chart:

Market-

implied 2019 Fed Rate- Change

Expectations

{kind=link}

The DXY

Dollar Index shot up overnight to fresh 24-month highs, and then plunged...

See Chart:

DXY Dollar

Index

{kind=link}

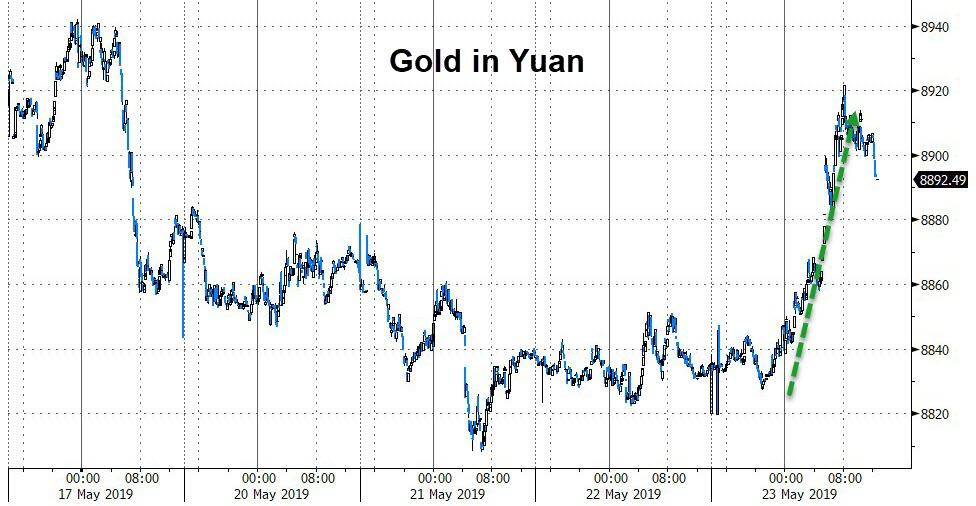

Gold

jumped against the yuan and dollar...

See Chart:

{kind=link}

Are we seeing a similar breakdown of various "leading" market

based indicators as last summer, before the equity market crash in Q4?

See Chart:

Early warning

indicators

{kind=link}

….

----

----

"there

are certain days when the price action itself is the key development – Thursday

fits this characterization."

What was behind today's furious buying and/or short-covering

frenzy in US Treasurys, which sent the 10Y yield briefly below 2.30%, the

lowest since 2017, inverted the 3M-10Y curve and pushed

all bond yields left of the 30Y below the Fed Funds rate?

See Chart:

{kind=link}

That was the question on every bond trader's lips today,

when as stocks were tumbling, capital seemed to flood into rates. One

explanation, or attempt thereof, came from BMO's Ian Lyngen, who writes that

"there are certain days when the

price action itself is the key development – Thursday fits this

characterization." In short, the price made the price,

which makes sense since there was no notable, fundamental developments to

justify the third biggest percentage drop in 10Y yields in the past 12 months.

The chart below shows that as of

today, the market is pricing in an average inflation rate of 1.76% over the

next 10 years, a sharp drop from the 1.98% on April 25.

See Chart:

10-Y Breakevens

{kind=link}

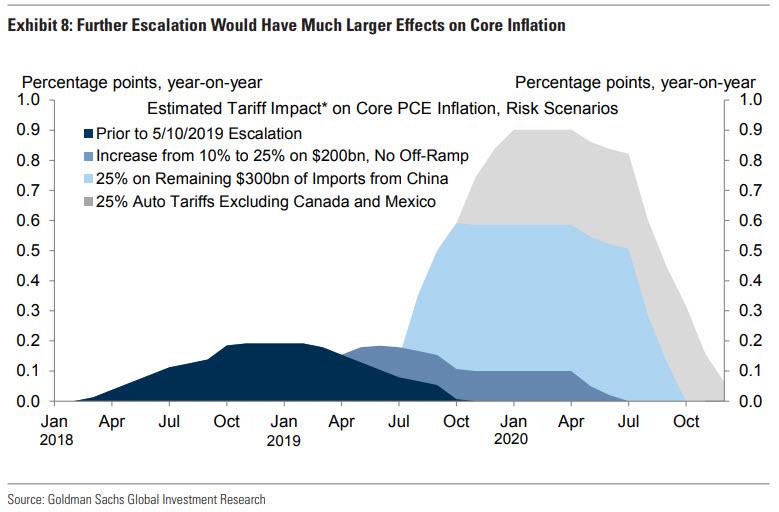

Which is odd, considering that an increasingly

greater number of strategists concede that a full

blown trade war which includes tariffs on all Chinese exports, would result in

sharply higher, if "transitory" inflation.

See Chart:

Further escalation would have much

larger effects on core inflation

{kind=link}

In any case, Ian Lyngen, who

writes that "there are certain days when the price action itself is the key

development – Thursday fits this characterization." continues,

noting that "if the fall in

inflation compensation continues, expect the Fed to respond in force,

unlike other central banks, they still have significant monetary policy space

to employ. At this juncture, that means rate cuts, or more precisely guidance

toward rate cuts. We’re skeptical that a June policy adjustment is seriously on

the table outside a true collapse in inflation expectations in the next four

weeks, though even a hint

from Powell that easing is coming later in 2019 should serve to temporarily

reassert inflation compensation toward a more comfortable level.

That being said, one possible explanation of today’s price

action – though not one we subscribe to – is a monetary policy error trade as

the Fed is letting itself get behind the curve. To this point, the May FOMC

Minutes contained no discussion of cuts, but it’s important to emphasize how stale that

meeting’s context was as it occurred before the recent deterioration in talks

between Washington and Beijing. Uncertainty looms large at this

point, leading to our increasingly

high conviction that real yields are set to move a leg lower. This repricing may end up being

thematic in the lead up to the June FOMC meeting."

The BMO strategist the notes that he was asked what was

responsible for the aggressive bidding behavior, and offers two related

explanations for the strong result.

- Firstly, with inflation compensation so low – 5-year breakevens are implying 1.3% PCE on average until 2024 – there is at least some of a “only one way to go from here” mentality. Let us not forget the trade war and what that might mean for pricing pressures and any flow through tariffs may have into CPI. This would open the possibility of TIPS outperforming their nominal cousins in coming weeks.

- Secondly, from fundamental perspective, at 57 bp over ten years, the inflation protected security surely holds an abundance of appeal give the list of things that can move real yields meaningfully higher at this stage seems to be growing shorter. Rather, a look at real rates since the end of March shows a decided move sideways and a drop to a new lower plateau as the new path of least resistance. Keep in mind that 5-year real yields were negative less than two years ago, and it’s a very live possibility that they may fall below 0 bp before the end of the year.

Another interesting point: while the rate rally occurred

with strong volumes as cash traded at 131% of the 10-day moving average, there

was no particular sense of panic in the move. But as Lyngen notes, this is not

to say that no major asset classes are exhibiting dramatic trading behavior. Indeed, one

point of recent selling has been WTI – down nearly 6% on Thursday, 13% from

recent highs, and 21% YoY. Although

it’s fair that prices are up YTD, this overstates the optimism surrounding

global growth. Indeed, a broader look at the Bloomberg commodity index shows a

modest increase of only 2% YTD, vs. a YoY drop of 14%. As BMO summarizes, "This is yet

another disinflationary impulse for the Fed to contend with."

One final observation, echoing what Michael Every said

earlier, is that "for

all the volatility and activity Thursday in the Treasury market – its

intriguing that one asset in particular was little changed, the renminbi." This is how Lyngen explains this bizarre calm

in the currency which so many expect will make a run fro 7.00:

The stabilization this week contrasts sharply with the

narrative of deteriorating trade negotiations which is spilling over into US

rates and risk assets. This indicates a willingness for now to hold the line

below the symbolic 7-handle.

The slightly

more cynical take from Rabobank's Every is below:

Ladies and gentlemen, the Tech Cold War has begun. Of course, there was

no reaction from CNH this morning despite China’s industrial crème-de-la-crème

about to be potentially defenestrated. But, as I keep stating, that underlines the whole problem

And so, with hopes that the above makes sense in explaining

today's violent move in the world's most liquidity security, Lyngen concludes

that all of this happens ahead of the long weekend "as a possible bullish risk in coming

weeks that would catalyze a rather sharp flight-to-quality and likely push part

of the Treasury market back below 2%. "

….

----

----

Expert

calls 90% of pot stocks frauds. Former hedge fund manager reveals the 10% most

likely to succeed.

====

"At 25 percent, we will need topass on the pricing to our consumers."

====

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

Must read as: Pelosi is agaisnt the impeach of Trump

'Bring it

Nancy'

====

Abuse + Abuse = fascism. This is what J Assange is being

suffering

The worst

fears of Assange's legal team have just been confirmed.

====

Nothing new. A report suggested that Penta & Saudi

jihadist participate in 9/11

Tax-funded DoD research is the backbone of the

modern, hi-tech economy. But

these technologies are dual-use. The companies that many of us take for granted

are connected directly to the US

military-intelligence complex.

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

With regional tensions already high, the risks of an incident between U.S. and Chinese forcescould increase

even further...

Markets are still

coming to grips with the reality of the trade war after many months of

complacency.

The first

trade war since the 1930s has escalated and may continue for years to come.

Trump has never wavered in his belief that China and other countries are

taking advantage of the U.S.’ low tariffs to export to the U.S., hurt U.S.

industry and steal U.S. jobs and intellectual property.

This month the conventional wisdom proved wrong — again —

and the stock market has now been forced to shift its

view. Just look at the market reaction since Trump began tweeting that a deal

was unlikely earlier this month.

Yesterday the market recovered some of Monday’s heavy

losses. But I don’t place much stock in yesterday’s market rally. There are fundamental differences

in the U.S. and Chinese positions that cannot easily be negotiated away.

But today,

China has much more leverage than Japan ever had. China is also in a much more adversarial posture toward the

U.S. than Japan was. The U.S. basically defends Japan and maintains several

military bases on Japanese territory. Despite some local frictions, Japan

welcomes the U.S. presence as a counter to Chinese ambitions in the region.

These

realities mean that China will not acquiesce but will retaliate for any actions

taken by the U.S.

With regional tensions already high, the risks of an incident between U.S. and Chinese

forces could increase even further.

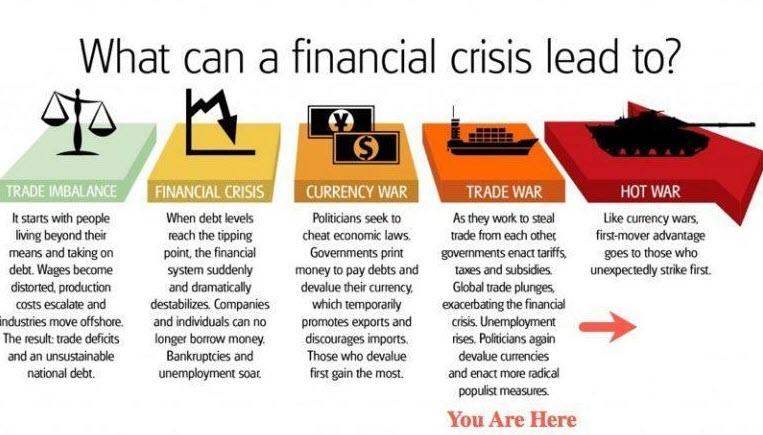

One of my major theses is that in times of too much debt and

too little growth, countries resort first to currency wars and then to trade

wars and then finally to shooting wars to steal growth from trading partners

and geopolitical rivals.

The problem with currency wars is

that all advantage is temporary and is quickly erased by retaliation.

Not only is the world not better off, but it is worse off because of the costs

and uncertainty resulting from the currency manipulations. Eventually, the world wakes up to this reality and moves to

the trade war stage. Then to the shooting war stage.

This new trade war

will get ugly fast and the world economy, which is already slowing, will be collateral

damage.

Markets

still are not fully prepared for this, but

you can be. Now is a good time to increase your cash allocation to reduce

volatility and increase your exposure to gold as a safe haven.

Let’s pray

the shooting wars are not hot on the heels of this coming trade war.

See Chart:

What ca a

financial crisis lead to?

{kind=link}

….

SOURCE: https://www.zerohedge.com/news/2019-05-23/trump-vs-world-jim-rickards-warns-will-get-ugly-fast

----

----

"You

can have your Frankfurter, and eat it too."

====

"If

you’re a Chinese company, there’s no way in hell you’re buying anything in the

U.S., not even the trash can, for the foreseeable future."

====

DARPA is seeking

noninvasive ways “to achieve high levels of

brain-system communications without surgery.” The techniques would “allow precise, high-quality connections to specific neurons

or groups of neurons.”

====

Common problem to face together without WW3

It looks like global food

production could be well below expectations in 2019, and that could

spell big trouble in

the months ahead...

====

Ladies and

gentlemen, the Tech Cold War has begun.

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

====

ALAI ORG

====

RT EN

ESPAÑOL

- Trump: "Huawei es algo muy peligroso"

- El jefe del Estado Mayor iraní promete una "respuesta dura, aplastante y devastadora" si su país es agredido

- Chinos renuncian en masa a sus iPhones en favor de Huawei

- La brutalidad de las 'guarimbas' opositoras en dos muertes que aún conmocionan a Venezuela

- "El fascismo moderno está saliendo al descubierto": Periodistas reaccionan tras los nuevos cargos criminales contra Assange

- Más allá de EE.UU.: ¿Quién empezó la caza сontra Huawei y por qué temen al gigante tecnológico asiático?

- Qué es el microbioma y por qué abre la puerta a curar diversas enfermedades

- Un masivo asteroide con 'luna' propia se aproximará a la Tierra esta semana

- Estas son las principales revelaciones de WikiLeaks

- Keiser Report "El dólar es un edificio a punto de someterse a una voladura controlada"

----

----

COUNTER PUNCH

Analysis on US Politics & Geopolitics

Kenn Orphan The Belligerence of

Empire

Tom Engelhardt Living

in a Nation of Political Narcissists

Chuck Collins Ending

the Generational Abuse of Student Debt

Robert J. Burrowes Understanding

NATO, Ending War

----

----

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more

business-wars from US-NATO allies

----

----

DEMOCRACY NOW

Amy Goodman’ team

----

----

PRESS TV

Resume of Global News described by Iranian observers..

This is the most obscene anti-fem attack on a human been.

She has been converted in an object to be used for Econ

&

Political gains.This is fascist-terrorism never seen in

W-hist.

Trump just renounced to be American. He must be impeached

Must read as: Pelosi is begging NO to impeach Trump

Both Dems & Reps go hand on hand supporting fascist wars

abroad

----

===

No hay comentarios:

Publicar un comentario