ND MAY

19 19

SIT EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

Given the

political structure of our country, it is

unlikely the situation will change. Lacy

added, “impossible.”

Bottom line: We simply have an insufficiency of savings and

it cannot be corrected.

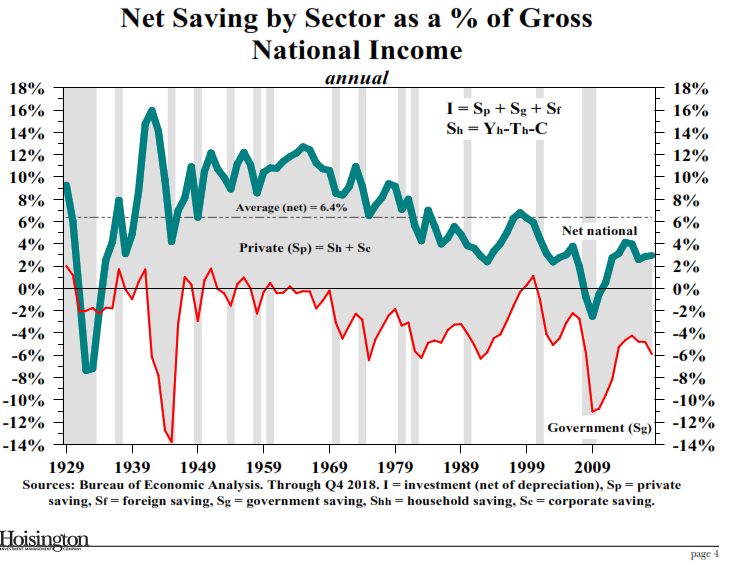

This is one of the most important charts in economics:

- The green line shows the national savings rate. It is currently at 3%. It is historically 6%. We are running half of normal. The shaded area shows the private sector, which is running at 9%. That’s pretty good. The red line shows the government sector and it is running at -6% and dragging down national savings. That is where the problem lies.

- But it is not going to stay there – the government deficit is moving even lower into negative territory.

- The government deficit will continue to grow. Tax cuts and the bipartisan agreed-upon increase in spending do not lead to deficit reduction.

- Bottom line: What it says is there is an insufficiency of savings to absorb ever-larger budget deficits. National savings is not staying at 3%, it is going to decline. Real investment is going to decline. It is possible the private sector will save more but that means there will be less consumption.

- In other words, the public sector is going to constrain the private sector and the economy. (SB: Debt acts as a noose around the economy’s neck.)… and guess which sector provides the basis for better growth, the private sector or the public sector?

- In other words, the government sector’s budget deficits are too large for the level of savings

See Chart:

NET

SAVINGS by Sector as a % of Gross National Income (annual)

{kind=link}

Bottom line: We simply have an insufficiency of savings and it cannot be corrected.

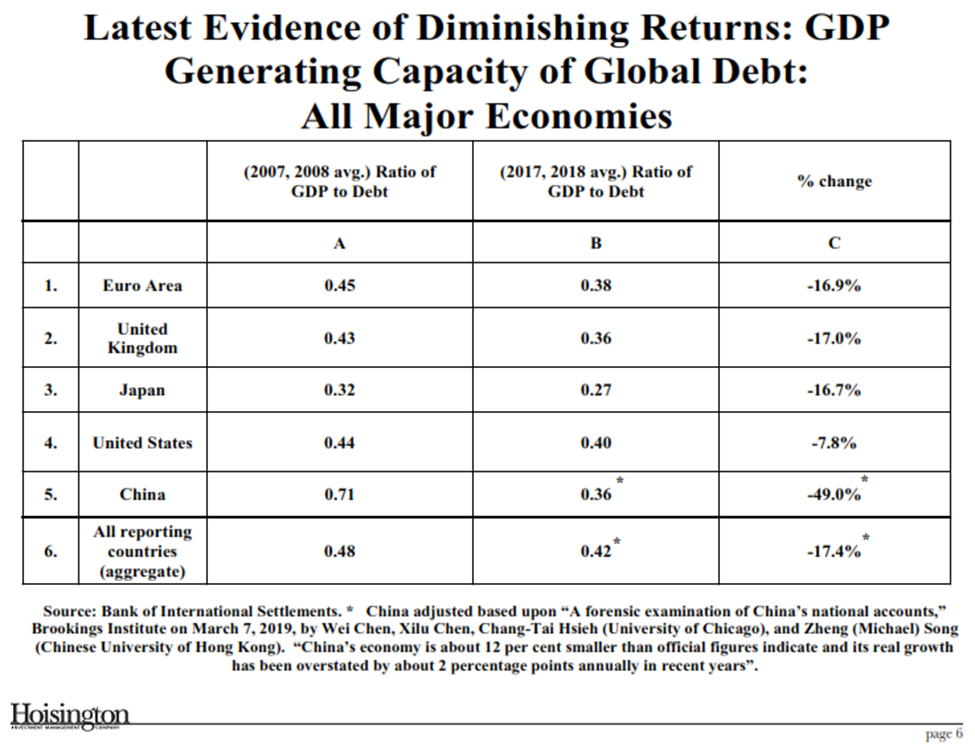

The Production Function – it is dependent upon technology and the three

factors of production: land, labor and capital.

- The production function states that if you overuse one of the three factors of production, output will initially rise and will then flatten out and then turn down.

- In other words, there is a non-linear relationship between debt and economic activity.

- The simple-minded solution that if a $3 trillion program doesn’t work you try a $6 trillion program… that doesn’t work when diminishing returns takes effect.

- The evidence here is increasingly dire.

Latest Evidence of Diminishing Returns:

- The good news. If you want to call it that, is the US is the best in town.

- Meaning we are not as far along the diminishing returns path as the rest of the world.

See table:

Latest Evidence of Diminishing Returns: GDP

generating capacity for Global debt

All Major Economies

{kind=link}

Irving Fisher (1934), in

perhaps his most important piece said, “When economies are highly indebted, economies slow.”

….

----

----

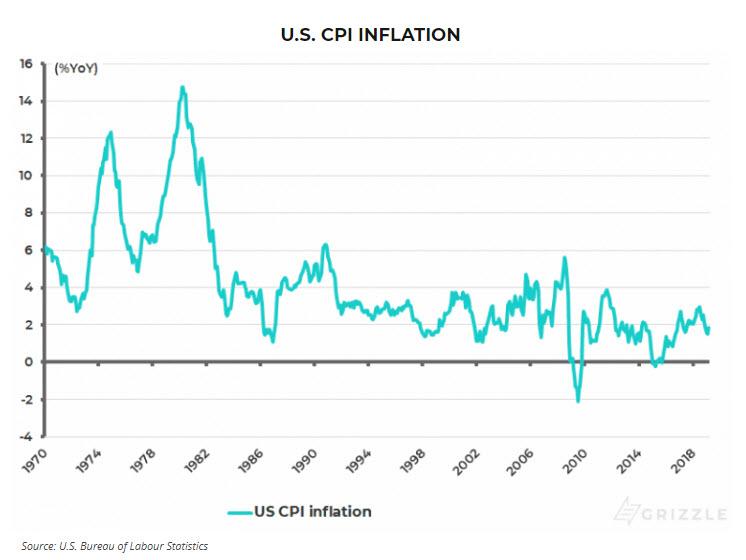

The reality : inflation chaos

can cause the uprising of people against Trump.

[ In “academic” language:]

IF inflation does suddenly return, it

will only be by a change in mass psychology which causes velocity, or the turnover of money in circulation, suddenly to surge.

….

[ The more inflated the Econ.. the

more deflated the Politics. Does Trump lost faith in Elect?.. OR: Is he planning WW3

before elections? .. IF he already

received a death threat (deep-state/Sec apparatus) .. this

would mean = IF I DIE.. ALL WILL DIE:

what degree of Paranoia Schizophrenic is

this?. I guess, the 1est prevention is not to give him/team the codes of

Nuke-missiles launching.]

See

Chart:

US CPI INFLATION

{kind=link}

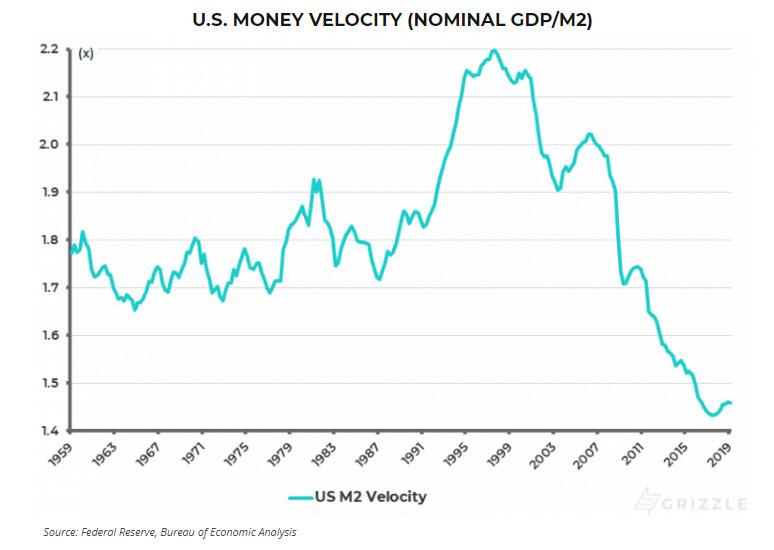

The reality is that if inflation does suddenly return, it will only be by

a change in mass psychology which causes velocity,

or the turnover of money in circulation, suddenly to surge. At that point the surge in narrow money supply of the past

ten years, with monetary base rising from US$900 billion in September 2008 to

US$3.3 trillion in April 2019 (see following chart), will act like kindling

wood on a fire.

See Chart:

US

Money Velocity ( Nominal GDP/M2)

{kind=link}

….

----

----

With the

first quarter earnings´season almost over, we can say that the risk of an imminent earnings recession is

far greater than what is discounted by an optimistic market...

With the first quarter

earnings´season almost over, we can say that the risk of an imminent earnings recession is far

greater than what is discounted by an optimistic market.

We must start by understanding

that the “positive” surprise seen in this earnings’ season in the US has been driven by two dangerous factors: The first, a very low base, as consensus has

consistently downgraded estimates prior to the publication of Q1 results. The second is buybacks. Almost the entire EPS

surprise in the S&P 500 comes from buybacks.

An earnings recession cannot be ruled out at all. It

is true that, meanwhile, fund flows have shown outflows from equities and into

bonds and that sovereign yields have been compressed even more. This is not a sign of optimism, but of caution and rising

perception of risk.

Global markets rise and fall with money supply

growth:

See Chart:

Global stocks vs. Global money Supply

{kind=link}

Conclusion:

With the placebo effects of monetary policy delivering diminishing

results, it is important to pay attention to the risk of an earnings’

recession, because it can be the beginning of a severe

downturn as companies find it increasingly difficult to support valuations with

buybacks and liquidity injections.

….

----

----

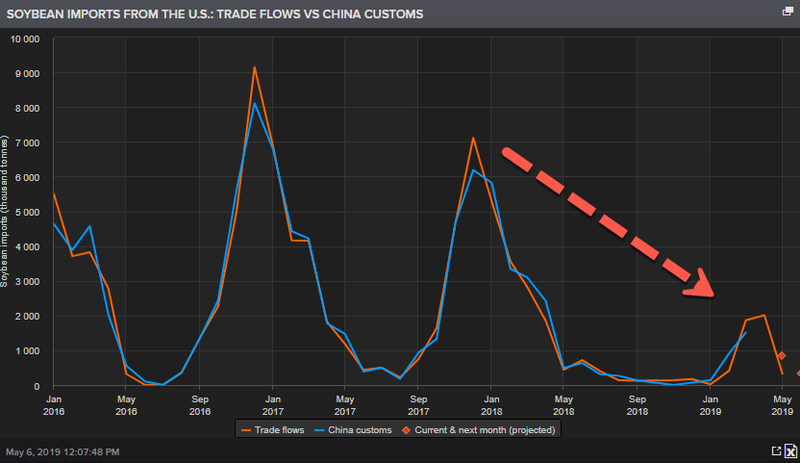

We are already losing the trade

war with China. Military blackmail didn’t work

Deere warned last week that shipments

of its tractors would decline by 20%

YoY in 2H19.

Heavy flooding in the last

several months across the Midwest, a deepening

trade war with China, depressed commodity prices, skyrocketing fuel costs,

declining land values, and massive debt loads have squeezed

farmers so much that Deere slashed production last week to deal with the

downturn.

See

Chart:

CBOT Soybean Futture

{kind=link}

There could be widespread pain

across the Midwest in 2H19. Over $76 billion of corn

and soybeans are in storage, according to the Farm Bureau, as China slashes

imports of grains from North America amid a deepening trade war.

See Chart:

{kind=link}

If

trade disputes continue to escalate and no resolution is seen by 2H19, the

replacement cycle for farmers could be several years out, likely to send

Deere's equity to the $100-80 range.

….

----

----

“INVESTORS”: BELIEVERS OF

CYNICISM

"If you’re in between and

believe in a world of consequences, you can understand why the Nasdaq can

continue higher in the current market/policy construct while not believing its

sustainable in any real way."

“The Taylor Rule with its

neutral 2% r-star interest rate may have worked better than the global monetary

policy we implemented over the last few decades,” said the CIO. “But it didn’t

allow for financial rescues or policy choices - maybe stocks fell and the Fed

wanted them to rally, or the ECB wanted to rescue the Eurozone, so they

deviated from Taylor and slashed rates.” With each cycle, leverage increased

and this lowered r-star either consciously or unconsciously. “WE ENDED UP

WITH A SYSTEM WHERE MONETARY POLICY IS NOW ONE-SIZE-FITS-NONE.”

See Table:

US Equilibrium Real Interest Rate

{kind=link}

"Policy

is too tight for those who don’t get the full pass-through of lower rates; much

of rural America, small businesses, emerging markets,” continued the same CIO. “But policy is too loose for urban housing and large cap growth

companies."

This creates a

self-perpetuating dynamic.: "Investors see that the ability to normalize monetary policy

declines as leverage rises, which suppresses interest rates, which lowers the

cost of capital for growth companies, and this subsidizes their rising market

share without requiring profits, which reduces inflation expectations, which

reduces r-star and gives investors confidence to increase leverage.”

"So what’s an investor to

do in this world?” asked the CIO. “Be a

true believer or an extreme cynic?” [[ Of course both, is the answer: believer of cynicism ]]

“But if you’re in between and believe in a world of consequences, you can

understand why the Nasdaq can continue higher in the current market/policy

construct while not believing its sustainable in any real way,” he

said, frustrated, waiting around for consequences, with no position.

….

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is

obsolete; it’s full of frauds & corruption. Urge cambio

"Our continued wasteful regime change wars have been

counterproductive to the interests of the American people..."

====

Fed Chair Jerome Powell is preaching economic nonsense...

====

A vicious battle between reality and make

belief is unfolding before our very eyes...

====

The world of payments is evolving,

and Flexa could be part of a massive shift towards crypto-currency

point-of-sale terminals at major retailers.

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

"Enlightenment

from this film to Chinese: there's no

equal negotiation without fighting."

----

----

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

VIENTO SUR

====

RT EN ESPAÑOL

El matón del

mundo busca guerra y no hay quien arme a IR con balist-nuke

- Comandante iraní: "Teherán no busca la guerra, pero no la teme"

- Varios países del golfo Pérsico permiten desplegar tropas a EE.UU. con las miras puestas en Irán

- Roger Waters, Pamela Anderson y Susan Sarandon cuestionan el silencio sobre Duma tras un informe de la OPAQ

- Google suspende negocios con Huawei tras incluir Trump a la compañía china en su 'lista negra'

- Diario chino: "El comportamiento bárbaro de EE.UU. con Huawei puede verse como declaración de guerra"

- Arabia Saudi aliado US "responderá con toda la fuerza" si lo hace Irán A esto apunta el US : a vender armas a los Saudis y otros peones el imperio. Big busin

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

PRESS

TV

Resume of Global News described

by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario