SEP 20 20 ND SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they documented with graphics

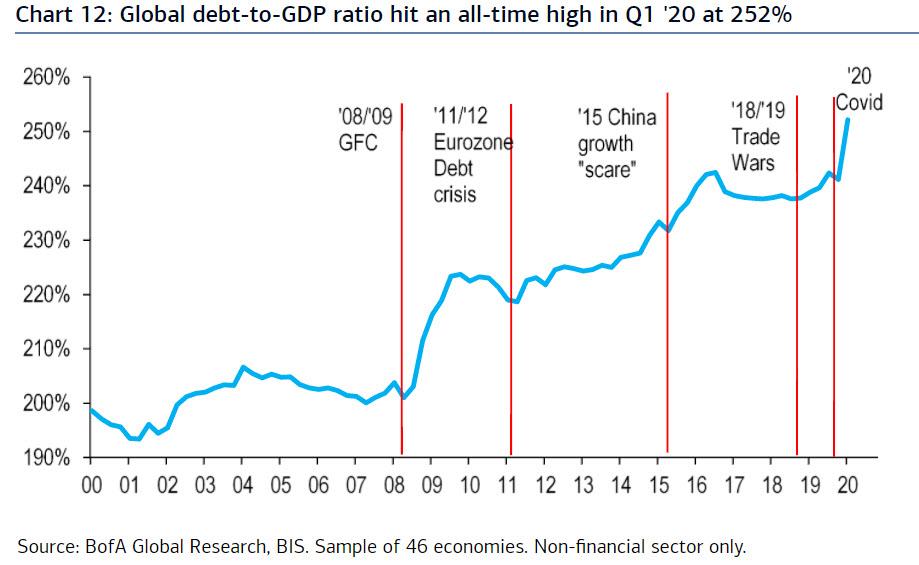

GLOBAL DEBT IS EXPLODING AT A SHOCKING RATE

The latest BIS data shows that global leverage rose 11% in Q1 '20, the largest quarterly jump on record.

Global debt/GDP surged to an all-time high in Q1 '20, with overall debt for the non-financial sector now worth 252% of global GDP. This is up from 241% at the end of 2019, the biggest quarterly jump ever according to BIS data.

SEE CHART:

https://www.zerohedge.com/s3/files/inline-images/global%20debt.jpg?itok=_NEl-EiU

{kind=link}

- The chart also confirms that central bank inflation targets are higher, much higher than the ""official 2%: to erase this debt, central banks needs inflation to be in the 10%+ range. Anything below that would require debt defaults instead of inflation to wipe away the debt... and that is unacceptable.

- This increase reflects the fallout from the first few weeks of the COVID crisis, with most advanced economies implementing total or partial lockdowns in March. Hence, the historical contraction in GDP growth observed worldwide in Q2 and the debt surge from both governments and non-financial corporations will translate into an even bigger rise in the global leverage ratio in Q2 '20.

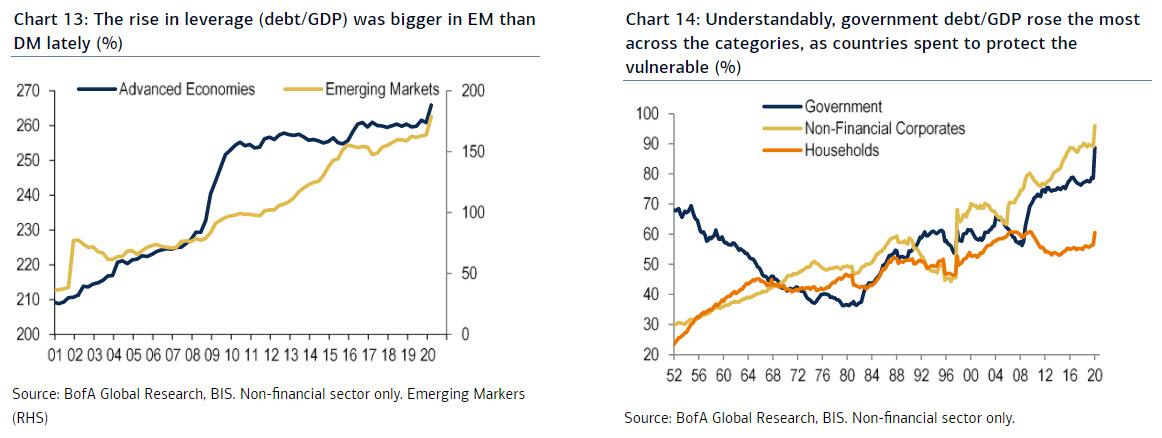

- Pre-existing vulnerabilities have been laid bare by the nature of the COVID shock. While both advanced economies (DM) and emerging markets (EM) have seen their leverage ratios jump, the latter have observed a rapid increase since 2012 (Chart 13). The relatively deeper COVID recession expected for some EM economies - the OECD Sep '2020 Economic Outlook sees India and South Africa GDP falling by 10.2% and 11.5%, respectively - will likely magnify the jump in some EM's leverage ratios.

SEE CHARTs:

1-The rise in leverage (debt/GDP) was bigger in EM than DM lately (5)

2-Stand to reason Govt debt/GDP rose the most across categories

https://www.zerohedge.com/s3/files/inline-images/rise%20in%20leverage.jpg?itok=d1yRymc0

{kind=link}

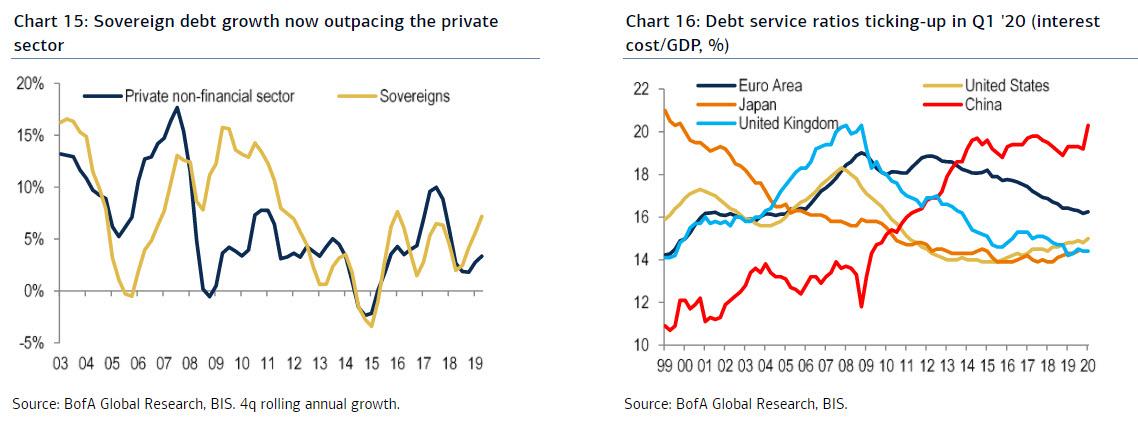

- By sectors, governments drove the big uptick in debt/GDP in Q1 '20. The global sovereign debt-to-GDP ratio has reached 89%, up 10 percentage points,the largest quarterly rise on record.

- Debt service ratios ticked up, but only marginally, reflective of the tremendous QE support unleashed by central banks this year.

SEE CHART:

1- Sovereign debt growth now outpacing the private sector

2- Dbt service rations ticking up in Q1 ’20 (interest cost GDP)

https://www.zerohedge.com/s3/files/inline-images/sovereign%20debt%20bofa.jpg?itok=0ZGD5yBw

{kind=link}

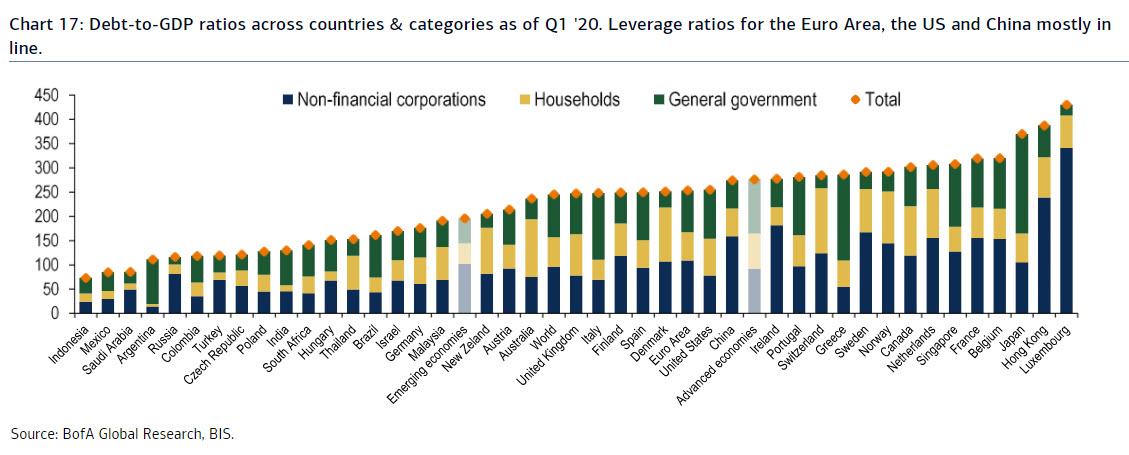

Total non-financial debt/GDP across countries and segments is shown in the BofA chart below;

SEE CHART:

Debt to GDP ratios across countries

https://www.zerohedge.com/s3/files/inline-images/debt%20to%20gdp%20ratios.jpg?itok=_QOvnHGX

{kind=link}

- The total leverage ratio for Euro Area, China and the US are mostly in line now;

- In Europe, a number of core countries (Belgium, Finland and Norway) saw a bigger increase in their total debt/GDP ratio than in the periphery in Q1 '20;

- While the rise in household debt has generally been more modest as consumers have moved into wait-and-see mode, China household debt/GDP rose 3.1% QoQ in Q1 '20

Finally, the table below show global debt/GDP leverage ratio across the globe, broken down by countries and segments.

See Table:

https://www.zerohedge.com/s3/files/inline-images/global%20debt%20ratio.jpg?itok=b7m9oEv9

{kind=link}

….

SOURCE: https://www.zerohedge.com/markets/global-debt-exploding-shocking-rate

----

----

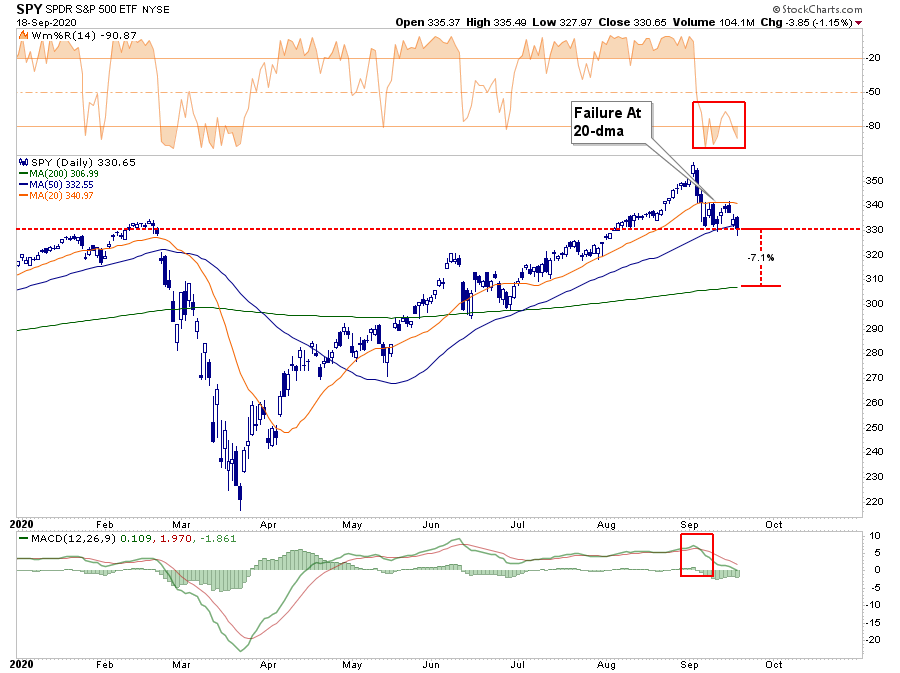

THE PRE-ELECTION CORRECTION CONTINUES, IS IT OVER?

Of course, it never hurts to always “wear your seatbelt.”

Authored by Lance Roberts via RealInvestmentAdvice.com,

The good news, if you want to call it that, is the market did hold a previous level of minor support and remains oversold short-term.

See Chart:

https://www.zerohedge.com/s3/files/inline-images/SP500-MarketUpdate-1-091820.png?itok=6DZ4m6IW

{kind=link}

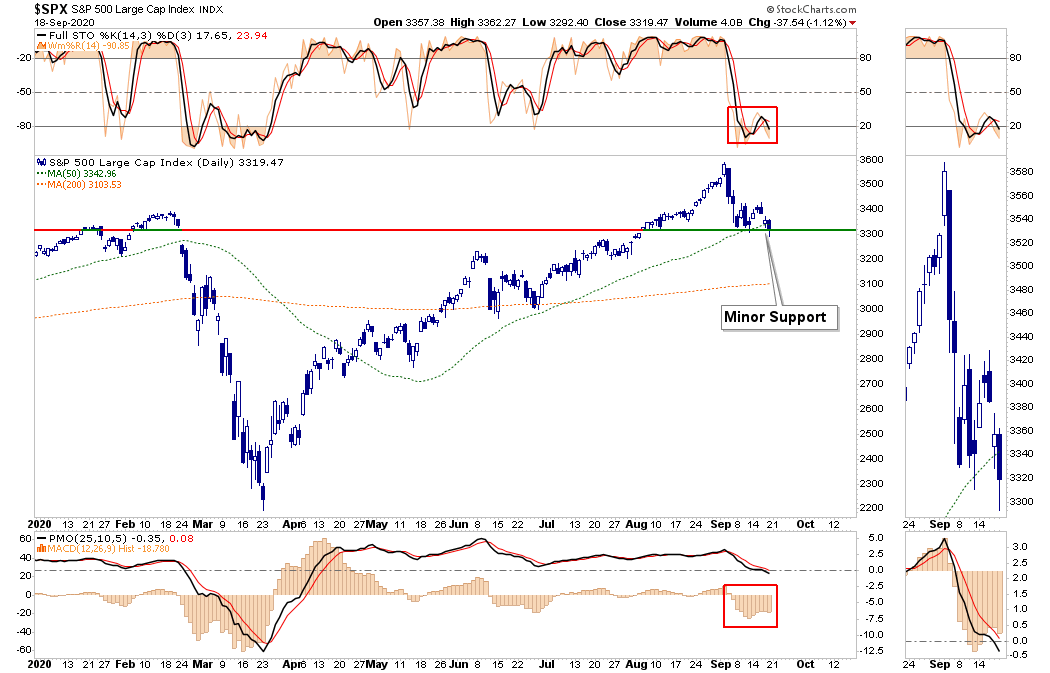

However, as shown below, the markets are very oversold short-term, so a tradeable “bounce” remains very likely in the next few days. If the bounce fails at either the 50- or 20-dma’s overhead, as shown above, such could well confirm an ongoing correction process.

See Chart:

https://www.zerohedge.com/s3/files/inline-images/SP500-MarketUpdate-2-091820.png?itok=e8-3H2hs

{kind=link}

Since President Rosevelt’s victory in 1944, there have only been two losses during presidential election years: 2000 and 2008. Those two years corresponded with the “Dot.com Crash” and the “Financial Crisis.” On average, stocks produced their second-best performance in Presidential election years.

See Charts:

{kind=link}

However, I would caution completely dismissing the not so insignificant 24% chance that a bear market could reassert itself, given the current economic weakness.

Will Policies Matter

The short answer is, “Yes.” However, not in the short-term.

Presidential platforms are primarily “advertising” to get your vote.

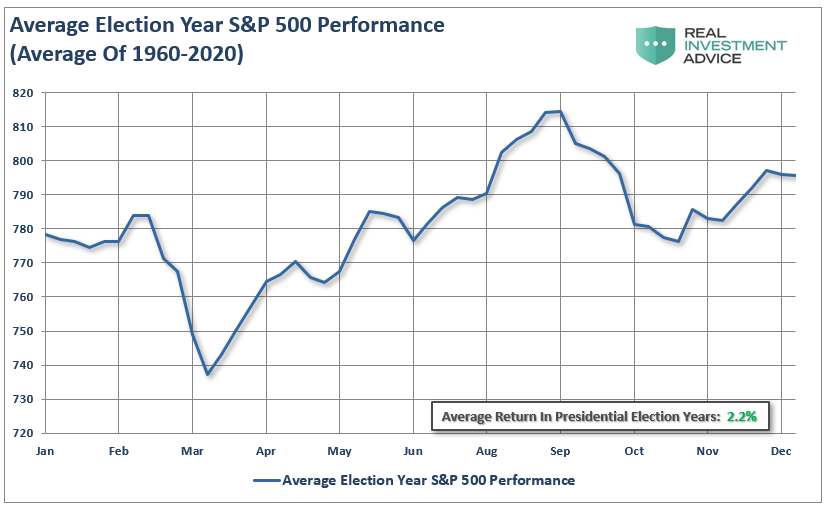

A look back at all election years since 1960 shows an average increase in the market of nearly 2.2% annually.

See Chart:

Average Election Year S&P 500 Performance

{kind=link}

Importantly, note in both cases the slump in returns during September and October. As we stated above, the current market correction falls nicely in line with historical norms.

See Chart: Election Year Returns – Bear Market

{kind=link}

Such is particularly the case today.

“For the second election in a row, voters will cast ballots for the candidate they dislike less, not whose policies they like more.” – Lance Roberts, Real Investment Show

See Charts:

https://www.zerohedge.com/s3/files/inline-images/Political-Polarization.png?itok=kuTUCiRd

{kind=link}

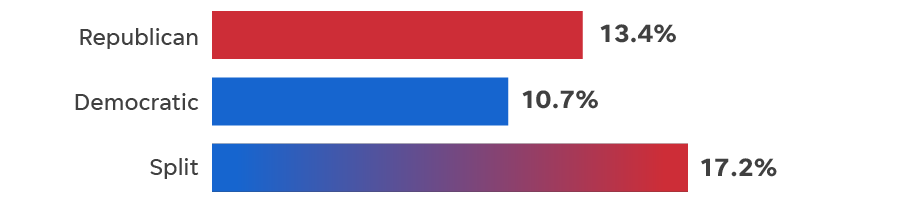

The one thing markets do seem to prefer – “political gridlock.”

“A split Congress historically has been better for stocks, which tend to like that one party doesn’t have too much sway. Stocks gained close to 30% in 1985, 2013 and 2019, all under a split Congress, according to LPL Financial. The average S&P 500 gain with a divided Congress was 17.2% while GDP growth averaged 2.8%.” – USA Today

See Chart:

Rps-Dems Split

https://www.zerohedge.com/s3/files/inline-images/Split-Congress.png?itok=hek4VSK3

{kind=link}

It’s Not A Risk-Free Outcome

Furthermore, from the election and 2021, outcomes are overly dependent on many things continuing to go “right.”

See List:

- Avoidance of a “double-dip” recession. (Without more Fiscal stimulus, this is a plausible risk.)

- The Fed continues expanding monetary policy. (There is currently no indication of this.)

- The consumer will need to expand their current debt-driven consumption. (This is a risk without more fiscal stimulus or sustainable economic growth.)

- There is a marked improvement in both corporate earnings and profitability. (This will likely be the case as mass layoffs will benefit bottom-line profitability. However, top-line sales remain at risk due to items #1 and #3.)

- A sharp improvement in employment, rising wages, and falling jobless claims will signal a sustainable economic recovery. (There is currently little indication this is the case outside the bounce from the March shutdown.)

These risks are all undoubtedly possible.

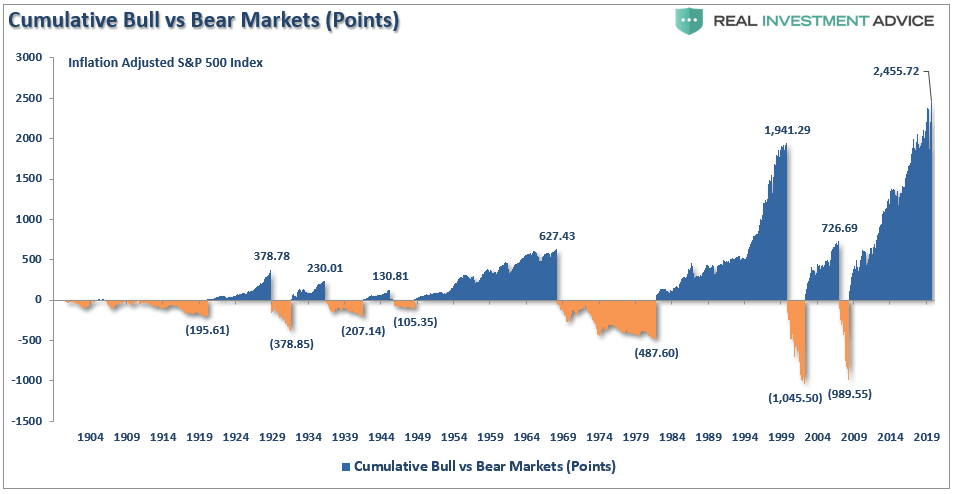

However, when combined with the longest-running bull market in history, high-valuations, and excessive speculation, the risks of something going wrong indeed have risen.

See Chart:

Cumulative Bull vs Bear Market

{kind=link}

As we have laid out, the historical odds suggest that markets will rise regardless of the electoral outcome. However, those are averages. In 2000 and 2008, investors didn’t get the “average.”

That is why it is always important to prepare for the unexpected.

It never hurts to always “wear your seatbelt.”

….

SOURCE: https://www.zerohedge.com/markets/pre-election-correction-continues-it-over

----

----

...either cascading defaults will accompany a recession, or government fiscal and monetary policy coordination is applied to eventually inflate it away...

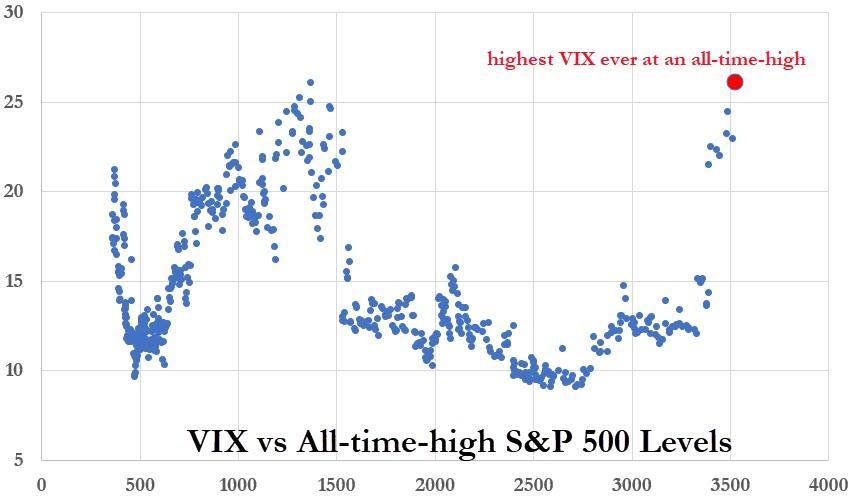

S&P 500 implied volatility remained unusually elevated even as the index erased Q1 losses and hit all-time highs. Like most things in markets, there are no definitive explanations, only theories. The Nov 3rd election supports implied vol (election-day vol implies a 5.6% S&P and 7% Nasdaq move up or down – 2.4x the presidential election avg). And the disconnect between economic fundamentals and equity prices leaves uneasy investors eager to own protection. Then there’s the institutional option buying, Softbank, retail speculation

A higher vol regime appeared inevitable because decades of increasingly aggressive monetary interventions left the system ever more dependent, just as the Fed has grown impotent.

See Chart:

VIX vs All-time-high S&P 500 levels

https://www.zerohedge.com/s3/files/inline-images/VIX%20at%20ATH_1.jpg?itok=F87F9mee

{kind=link}

The Fed understands this even as they deny it, which is why they’ve increasingly called on politicians to support monetary easing with increased deficit spending.

Monetary/fiscal coordination in a world of Fed impotence transfers power from central bankers to politicians, because it is the latter who control spending. This leaves the Fed as a political entity that to a greater or lesser degree monetizes government debt. Once this role is broadly understood, the Fed’s independence is lost. We’re nearly there.

When economy-wide debt reaches levels where each incremental dollar yields very little real economic growth, either cascading defaults will accompany a recession, or government fiscal and monetary policy coordination is applied to obfuscate the problem and eventually inflate it away. And on each, heightened volatility is inevitable. That is my bias.

….

SOURCE: https://www.zerohedge.com/markets/bias

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption. Urge cambio

THE BEST AND WORST STATES FOR HOMESCHOOL FREEDOM

Pennsylvania is among the most restrictive states when it comes to the freedom to homeschool your children.

====

Billonaires run our Econ: they bought gold & now sell bad assets to get cash 4 new invt

"HE NEEDS CASH": RON PERELMAN'S LEVERAGED EMPIRE COLLAPSES IN A DELUGE OF FIRE SALES

"At least nine banks" have claims to Perelman's assets...

Perelman said publicly: “We quickly took significant steps to react to the unprecedented economic environment that we were facing. I have been very public about my intention to reduce leverage, streamline operations, sell some assets and convert those assets to cash in order to seek new investment opportunities and that is exactly what we are doing.”

Perelman, under pressure due to his crashing stake in Revlon, has seen his fortune drop from $19 billion to just $4.2 billion over the last two years, according to the Bloomberg Billionaire's Index. His investment company, MacAndrews & Forbes, said it needed to "rework its holdings" back in July due to the pandemic.

Perelman has his skeptics, including R Hack, who wrote a book about him.

Hack concluded: “If you want a simpler life, you go buy a farm in Oklahoma, not sell a painting out of your townhouse in Manhattan. If he’s selling his art, it’s because he needs cash.”

[ Imagine what Perelman will do if USD go back to its base in gold.. He will buy the Presidency , if not doing it now. The conversion of USD to gold base is comi]

----

----

I guess Trump is also swimming over gold. He don’t need the Presid. He is on his own.

CENTRAL BANKS TELL MARKETS: "YOU’RE ON YOUR OWN NOW"

Without additional monetary support, risky assets are left on their own now. The lack of fiscal stimulus in the U.S. underscores the risk heading into the presidential election.

Without additional monetary support, risky assets are left on their own now.

The lack of fiscal stimulus in the U.S. underscores the risk heading into the presidential election.

====

FORMER FDA DIRECTOR EXPECTS "AT LEAST ONE MORE CYCLE" OF COVID-19 BEFORE VACCINE APPROVAL

"I don't believe a vaccine will be licensed for general use by the population until the end of the 2nd quarter of 2021, or perhaps a little later than that..."

====

Both Biden & Trump are going to get their balls busted since the night after Elect

BIDEN GETS SOFTBALLS, WHILE TRUMP GETS BALLS BUSTED

The are going to be called EUNUCHES or EUNUCOS

And nobody will say that "The media is broken..."

Others will say: A ESOS LE FALTARON HUEVOS to acept their debacle

Socialist REFERENDUM will put down the obsolete duopoly system (R+D)

====

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State socialis+K-, D rest in limbo

What if they already have nuke with long distance missiles?

US BELIEVES IRAN LIKELY TO HAVE ENOUGH FISSILE MATERIAL FOR NUCLEAR BOMB BY YEAR'S END

Same 'anonymous officials say'... different election year.

====

DOZENS OF US TANKER TRUCKS FILLED WITH OIL LEAVE SYRIA FOR IRAQ

Syrian official media charges that US occupation has begun transferring stolen oil abroad...

====

US CLOSE TO DECLARING QATAR MAJOR NON-NATO ALLY, DEEPENING MILITARY TIES

Iran will see this as a direct threat following Qatar's role in Syrian regime change efforts...

====

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars & danger of WW3

-Joint Russian-Turkish Military Training Session Held in Idlib

-Trump Says He May Ink Executive Order to Stop Biden From Running in Nov Elect

-Almost Dozen Participants in Anti-Government Demonstrations in Israel Arrested

-Over 20 Black Sea Fleet Ships Take Part in Kavkaz-2020 Drills - RU Defense Min

-US Stresses Importance of Reducing Violence Amid Afghan Peace Talks

-Iran Could Have Nuclear Weap by End of Year Through Cooperat With North Korea

-France, Germany, Romania Plan Observation Flight Over Russia

-Biden Calls For Postponement of Senate Vote on Supreme Court Nominee

-Pompeo Slams EU Countries For Failing to Support Reinstating UN Sanct on Iran

-Pelosi Not Ruling Out Impeachment Effort to Stop Senate Vote on Supreme Court

====

====

THE REST FOR TOMORROW

No hay comentarios:

Publicar un comentario